Hybrid Memory Cube and High Bandwidth Memory Market

Hybrid Memory Cube and High Bandwidth Memory Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710166 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Hybrid Memory Cube and High Bandwidth Memory Market Size

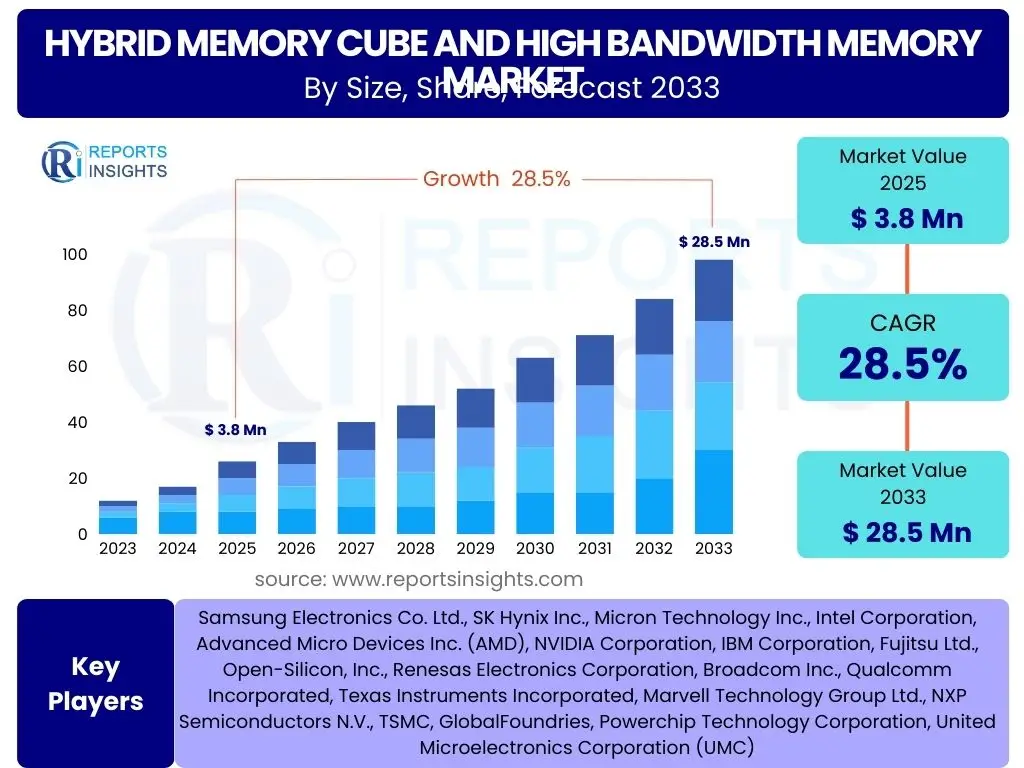

According to Reports Insights Consulting Pvt Ltd, The Hybrid Memory Cube and High Bandwidth Memory Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 28.5 Billion by the end of the forecast period in 2033.

Key Hybrid Memory Cube and High Bandwidth Memory Market Trends & Insights

The Hybrid Memory Cube (HMC) and High Bandwidth Memory (HBM) market is undergoing significant transformation, primarily fueled by the escalating global demand for high-performance computing (HPC) solutions. These advanced memory technologies are becoming indispensable for applications that require massive parallel processing and ultra-fast data access, such as artificial intelligence, machine learning, and sophisticated data analytics. A pivotal trend involves the continuous advancements in HBM standards, with newer generations like HBM3 and HBM3E offering significantly higher bandwidth, improved power efficiency, and increased capacity, consistently pushing the boundaries of memory-intensive workloads.

The industry is also witnessing a robust trend toward the direct integration of HBM onto processor packages, a strategy that effectively reduces latency and optimizes overall system performance, which is a critical factor for next-generation data centers and specialized accelerators. Furthermore, the market is characterized by a strategic emphasis on innovations in packaging technologies, such as 2.5D and 3D stacking, alongside enhanced thermal management solutions. These developments are essential for effectively handling the increased memory density and demanding operational conditions inherent in these stacked memory architectures, ensuring reliability and sustained performance in high-stress environments.

- Escalating demand for high-performance computing (HPC) across various sectors.

- Proliferation of Artificial Intelligence (AI) and Machine Learning (ML) workloads.

- Continuous evolution and rapid adoption of newer HBM standards (HBM2E, HBM3, HBM3E, HBM4).

- Growing integration of HBM with CPUs and GPUs through advanced packaging solutions.

- Increased focus on power efficiency and robust thermal management for stacked memory modules.

- Expansion into emerging applications, including autonomous vehicles and edge computing devices.

- Strategic partnerships and collaborations driving technological innovation and market adoption.

AI Impact Analysis on Hybrid Memory Cube and High Bandwidth Memory

The explosive proliferation of Artificial Intelligence (AI) has profoundly impacted the Hybrid Memory Cube and High Bandwidth Memory market, fundamentally transforming both demand dynamics and developmental priorities. AI workloads, characterized by their immense data parallelism and computational intensity, necessitate memory solutions capable of delivering unprecedented bandwidth and remarkably low latency. HBM, in particular, alongside HMC to a lesser extent, is uniquely positioned to meet these stringent requirements, acting as a critical enabler for next-generation AI accelerators, deep learning processors, and sophisticated neural network training systems. User inquiries frequently center on how these memory types will effectively scale with increasingly complex AI models and their indispensable role in achieving superior computational efficiency.

Furthermore, AI's influence extends significantly to the design, optimization, and manufacturing processes of HBM and HMC technologies themselves. AI-driven simulation and optimization tools are increasingly being employed to refine memory stacking, interconnections, and thermal properties, thereby accelerating development cycles and substantially improving yield rates. The integration of AI directly into advanced chip design workflows is leading to more efficient memory controller designs that can intelligently manage data flow, further enhancing the symbiotic relationship between compute and memory in high-performance AI systems. This powerful synergy ensures that as AI capabilities continue their rapid advancement, the demand for sophisticated memory solutions like HBM will surge, cementing their status as foundational components of the ongoing AI revolution.

- Essential for meeting the high-bandwidth and low-latency requirements of AI/ML accelerators.

- Enables efficient processing of massive datasets crucial for deep learning and neural networks.

- Drives demand for higher capacity and faster HBM generations, such as HBM3 and HBM3E.

- Facilitates tighter integration with specialized AI processors and high-performance GPUs.

- Influences memory architecture design to optimize performance for AI-specific workloads.

- Supports the exponential growth of AI applications in data centers, edge devices, and autonomous systems.

Key Takeaways Hybrid Memory Cube and High Bandwidth Memory Market Size & Forecast

The Hybrid Memory Cube and High Bandwidth Memory market represents a foundational pillar for the future of high-performance computing, with its robust growth trajectory underpinned by accelerating technological demands. Key insights indicate that High Bandwidth Memory (HBM) is rapidly becoming the de facto standard for memory-intensive applications, largely superseding Hybrid Memory Cube (HMC) in most new designs due to its superior bandwidth scalability, enhanced power efficiency, and broader industry adoption. The market’s significant expansion is inextricably linked to the rapid advancements in AI, machine learning, and cloud computing, all of which require increasingly sophisticated memory solutions to process vast amounts of data efficiently and at unprecedented speeds. This dynamic environment suggests a sustained period of innovation and substantial investment, particularly in higher-density and more power-efficient HBM variants.

Strategic partnerships between leading memory manufacturers, advanced processor developers, and major end-users are proving pivotal in driving wider adoption and refining product roadmaps to consistently meet evolving performance benchmarks. Furthermore, the persistent emphasis on advanced packaging technologies, such as 2.5D and 3D stacking, will continue to profoundly shape the market by enabling closer, more efficient integration of memory with logic components. This integration minimizes latency, optimizes overall system-level performance, and reduces power consumption. The compelling market forecast underscores the critical and foundational role of these advanced memory technologies in facilitating the next generation of data-driven innovations across a diverse array of sectors, from scientific research to enterprise solutions.

- Significant market expansion driven by the relentless demand from data-intensive applications.

- High Bandwidth Memory (HBM) dominates due to superior bandwidth, power efficiency, and strong industry support.

- Crucial for enabling and advancing Artificial Intelligence, Machine Learning, and High-Performance Computing.

- Continuous innovation in HBM standards and advanced packaging technologies is a primary growth factor.

- Strategic importance for leading semiconductor manufacturers, data center operators, and cloud service providers.

- Projected long-term growth is firmly anchored by the requirements of next-generation computing paradigms.

- The market shift from HMC to HBM is largely complete, with HBM continuing its rapid evolution.

Hybrid Memory Cube and High Bandwidth Memory Market Drivers Analysis

The Hybrid Memory Cube and High Bandwidth Memory market is propelled by a confluence of powerful technological and application-specific drivers that underscore the critical need for advanced memory solutions. The escalating demands of high-performance computing (HPC) across scientific research, complex simulations, and enterprise workloads necessitate memory capable of feeding data to processors at extreme speeds. Concurrently, the exponential growth of artificial intelligence (AI) and machine learning (ML) algorithms, particularly deep learning, creates an insatiable demand for memory with ultra-high bandwidth to process massive datasets and intricate neural networks efficiently.

Further amplifying these drivers is the rapid expansion of data centers and cloud infrastructure globally, as businesses and consumers increasingly rely on cloud-based services and data analytics. These facilities require memory solutions that can enhance throughput, reduce latency, and improve energy efficiency to handle ever-increasing data traffic. Moreover, advancements in high-end gaming and graphics rendering, demanding realistic visuals and immersive experiences, push the boundaries of memory performance, with HBM becoming a standard in high-end GPUs. These interconnected factors collectively fuel the robust growth trajectory of the HBM and HMC market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased demand from High-Performance Computing (HPC) for scientific research and complex simulations. | +7.5% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

| Proliferation of Artificial Intelligence (AI) and Machine Learning (ML) applications across industries. | +8.0% | North America, Asia Pacific (China, South Korea), Europe | Short to Long-term (2025-2033) |

| Significant growth in data center and cloud infrastructure to handle exponential data volumes. | +6.8% | Global, with strong focus in North America, Asia Pacific | Mid-term (2027-2031) |

| Advancements in high-end gaming and professional graphics rendering requiring extreme memory bandwidth. | +5.5% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

Hybrid Memory Cube and High Bandwidth Memory Market Restraints Analysis

Despite the substantial growth drivers, the Hybrid Memory Cube and High Bandwidth Memory market faces several significant restraints that could temper its expansion. One of the primary inhibitors is the inherently high manufacturing cost associated with these advanced memory technologies. The intricate processes involved in 3D stacking, through-silicon via (TSV) fabrication, and advanced packaging techniques contribute significantly to the overall production expenses, making them more expensive than traditional memory solutions like DDR. This elevated cost can limit their adoption in price-sensitive segments or for applications where ultra-high bandwidth is not an absolute necessity.

Furthermore, the complex integration requirements pose another substantial restraint. Incorporating HBM or HMC into system designs often necessitates significant redesigns of motherboards and processing units, as well as specialized thermal management solutions due to their high power density. The limited supply chain, with only a few dominant manufacturers capable of producing these advanced memory modules, creates potential bottlenecks and vulnerabilities, impacting availability and pricing stability. Addressing these technical and economic hurdles will be crucial for the market to achieve its full potential and broaden its applicability beyond premium, high-performance segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High manufacturing cost and complexity involved in 3D stacking and advanced packaging. | -4.0% | Global, affecting all regions equally | Long-term (2025-2033) |

| Significant thermal management challenges due to high power density in compact stacked designs. | -3.2% | Global, critical for dense data center environments | Mid-term (2026-2030) |

| Limited number of specialized manufacturers contributing to supply chain vulnerabilities. | -2.8% | Primarily Asia Pacific (manufacturing hubs) | Mid-term (2026-2029) |

Hybrid Memory Cube and High Bandwidth Memory Market Opportunities Analysis

The Hybrid Memory Cube and High Bandwidth Memory market is rich with opportunities stemming from technological advancements and the emergence of new, demanding applications. A significant opportunity lies in the burgeoning field of edge AI and Internet of Things (IoT) devices, where localized, real-time data processing requires high-bandwidth, low-power memory solutions. As AI moves closer to the data source, HBM’s efficiency and performance become increasingly valuable, enabling advanced analytics and decision-making directly on devices without constant cloud connectivity.

Furthermore, continuous advancements in packaging technologies, such as Chip-on-Wafer-on-Substrate (CoWoS) and Intel’s Foveros, present opportunities to further optimize HBM integration, reducing latency and increasing overall system performance and power efficiency. These innovations facilitate closer integration with custom silicon, opening doors for highly optimized application-specific integrated circuits (ASICs) in AI and HPC. The rapid development of the autonomous vehicles sector also represents a substantial long-term opportunity, as these vehicles require immense computational power and ultra-fast memory to process sensor data in real-time for safe and reliable operation. Embracing these opportunities through strategic research and development, alongside cross-industry collaborations, will be key to unlocking significant market expansion and innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Edge AI and advanced Internet of Things (IoT) devices requiring localized high-bandwidth memory. | +6.0% | Global, particularly in industrial and consumer sectors | Mid to Long-term (2027-2033) |

| Ongoing advancements in sophisticated packaging technologies like CoWoS, enabling denser and more efficient integration. | +5.5% | Global, with key innovation hubs in Asia Pacific and North America | Short to Mid-term (2025-2030) |

| Growth in the autonomous vehicles sector, demanding high-speed memory for real-time sensor data processing. | +4.8% | North America, Europe, Asia Pacific (China) | Long-term (2028-2033) |

| Development of new computing paradigms like quantum computing and neuromorphic computing. | +3.0% | Global (Research & Development focus) | Long-term (2030-2033) |

Hybrid Memory Cube and High Bandwidth Memory Market Challenges Impact Analysis

The Hybrid Memory Cube and High Bandwidth Memory market, despite its promising growth trajectory, confronts several formidable challenges that necessitate strategic planning and substantial investment. A significant hurdle is the intense requirement for continuous research and development investment. The rapid pace of technological evolution, particularly with new HBM standards and advanced packaging techniques, demands substantial capital expenditure and a highly specialized workforce to maintain a competitive edge and address evolving performance needs.

Furthermore, optimizing yield rates in the complex 3D stacking and TSV fabrication processes remains a persistent challenge. Even minor defects at any layer can render an entire stack unusable, directly impacting manufacturing costs and profitability. This complexity requires highly advanced fabrication facilities and stringent quality control measures. Another challenge stems from the intensifying competition from alternative memory architectures, such as GDDR6/GDDR7 and emerging CXL (Compute Express Link) attached memory, which offer compelling performance-to-cost ratios for various applications. These alternatives can potentially divert market share, particularly for applications where HBM's absolute bandwidth advantage may be overkill or cost-prohibitive. Successfully navigating these challenges requires robust innovation pipelines and astute market positioning.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High capital expenditure and intense Research and Development (R&D) investment required for continuous innovation. | -3.5% | Global, impacting all major semiconductor companies | Long-term (2025-2033) |

| Difficulties in achieving optimal yield rates in complex 3D stacking and through-silicon via (TSV) fabrication. | -3.0% | Global, primarily affecting manufacturing hubs in Asia Pacific | Short to Mid-term (2025-2029) |

| Intense competition from alternative memory architectures like GDDR6/GDDR7 and CXL-attached memory. | -2.5% | Global, particularly in consumer graphics and server markets | Mid to Long-term (2027-2033) |

| Managing increasing power consumption requirements at higher bandwidths and densities. | -2.0% | Global, critical for data centers and mobile applications | Mid-term (2026-2030) |

Hybrid Memory Cube and High Bandwidth Memory Market - Updated Report Scope

This comprehensive market report offers an updated and in-depth analysis of the Hybrid Memory Cube (HMC) and High Bandwidth Memory (HBM) market, providing critical insights into its current size, historical trends, and future growth projections. The scope encompasses detailed segmentation by type, application, and end-use industry, alongside an extensive regional analysis to highlight key market dynamics across different geographies. It thoroughly examines the impact of Artificial Intelligence, key market drivers, restraints, opportunities, and challenges influencing the industry landscape, offering a holistic view for strategic decision-making. The report also profiles leading market players, presenting a competitive analysis to understand their market positioning and strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 28.5 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Electronics Co. Ltd., SK Hynix Inc., Micron Technology Inc., Intel Corporation, Advanced Micro Devices Inc. (AMD), NVIDIA Corporation, IBM Corporation, Fujitsu Ltd., Open-Silicon, Inc., Renesas Electronics Corporation, Broadcom Inc., Qualcomm Incorporated, Texas Instruments Incorporated, Marvell Technology Group Ltd., NXP Semiconductors N.V., TSMC, GlobalFoundries, Powerchip Technology Corporation, United Microelectronics Corporation (UMC) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Hybrid Memory Cube and High Bandwidth Memory market is comprehensively segmented to provide granular insights into its diverse applications and ongoing technological evolution. This segmentation typically includes a detailed analysis by memory type, specific application areas, and the overarching end-use industries, allowing for a multifaceted understanding of market dynamics across various sectors. By type, the market distinctively differentiates between the various generations of HBM, such as HBM2, HBM2E, HBM3, and the emerging HBM3E and HBM4 standards, which directly reflect the rapid pace of technological advancement in memory bandwidth, capacity, and efficiency. Hybrid Memory Cube (HMC), while an earlier innovation, continues to retain a specialized market niche, particularly in specific high-performance computing environments where its unique architecture aligns optimally with existing system requirements.

Furthermore, the application-based segmentation vividly highlights the primary use cases that are driving widespread adoption, encompassing crucial areas like high-performance computing (HPC), advanced artificial intelligence and machine learning (AI/ML) systems, hyperscale data centers, and high-end graphics processing units (GPUs) utilized in professional workstations and immersive gaming. These demanding applications are consistently pushing the boundaries of memory performance, directly influencing the demand for more advanced HMC and HBM solutions. The segmentation by end-use industry further refines this perspective, illustrating precisely how sectors such as IT & telecommunications, automotive (for ADAS and infotainment), consumer electronics, and industrial automation are strategically integrating these advanced memory technologies to significantly enhance their product offerings and operational capabilities. A thorough understanding of these intricate segments is paramount for stakeholders to effectively identify nascent growth opportunities and strategically position their innovative solutions within this rapidly evolving market landscape.

- By Type

- Hybrid Memory Cube (HMC)

- High Bandwidth Memory (HBM)

- HBM2

- HBM2E

- HBM3

- HBM3E

- HBM4 (Emerging)

- By Application

- High-Performance Computing (HPC)

- Artificial Intelligence (AI) and Machine Learning (ML) Accelerators

- Data Centers and Cloud Infrastructure

- Graphics Processing Units (GPUs) for Gaming and Professional Workstations

- Networking and Telecommunications Equipment

- Automotive (Advanced Driver-Assistance Systems - ADAS, In-vehicle Infotainment)

- Consumer Electronics (High-end Gaming Consoles, Virtual/Augmented Reality)

- By End-Use Industry

- IT and Telecommunications

- Automotive

- Gaming

- Industrial and Manufacturing

- Aerospace and Defense

- Healthcare and Medical Imaging

Regional Highlights

The global Hybrid Memory Cube and High Bandwidth Memory market exhibits distinct regional dynamics, significantly influenced by local technological infrastructure, substantial investment in advanced computing capabilities, and the robust presence of key industry players. North America currently leads the market, primarily driven by its highly developed ecosystem of hyperscale data centers, pervasive cloud service providers, and extensive research and development in AI and high-performance computing. The region's proactive adoption of cutting-edge technologies and substantial venture capital investments into semiconductor innovation contribute significantly to its market dominance. Major hyperscalers and leading GPU developers, predominantly located in this region, are instrumental in driving the immense demand for HBM.

Asia Pacific is rapidly emerging as a powerful force in the market, propelled by its massive semiconductor manufacturing capabilities, flourishing consumer electronics market, and burgeoning AI adoption, particularly within technologically advanced nations like China, South Korea, and Japan. The region benefits from substantial government support for technological advancement and boasts a large pool of highly skilled engineering talent. Europe, while currently holding a smaller market share, demonstrates strong growth in specialized niches such as scientific research, automotive for advanced driver assistance systems, and industrial automation, leveraging its inherent strengths in precision engineering and advanced manufacturing. Latin America, the Middle East, and Africa are also showing nascent but promising growth, primarily driven by increasing digitalization initiatives and strategic investments in critical data infrastructure. Each region contributes uniquely to the overall global market, reflecting their diverse economic landscapes, technological capabilities, and strategic priorities.

- North America: Dominates the market due to a strong presence of hyperscale data centers, leading AI/ML research institutions, and major GPU manufacturers. It is an early and consistent adopter of advanced computing technologies.

- Asia Pacific (APAC): Exhibits significant growth fueled by robust semiconductor manufacturing capabilities, an expanding consumer electronics market, and increasing AI adoption, particularly in key countries like China, South Korea, and Japan.

- Europe: Demonstrates growing demand from high-performance computing centers, influential scientific research institutions, and the automotive sector for sophisticated ADAS and autonomous driving applications.

- Latin America, Middle East, and Africa (MEA): Represents emerging markets with increasing investments in digital infrastructure and data center development, offering substantial future growth potential as digitalization accelerates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hybrid Memory Cube and High Bandwidth Memory Market.- Samsung Electronics Co. Ltd.

- SK Hynix Inc.

- Micron Technology Inc.

- Intel Corporation

- Advanced Micro Devices Inc. (AMD)

- NVIDIA Corporation

- IBM Corporation

- Fujitsu Ltd.

- Open-Silicon, Inc.

- Renesas Electronics Corporation

- Broadcom Inc.

- Qualcomm Incorporated

- Texas Instruments Incorporated

- Marvell Technology Group Ltd.

- NXP Semiconductors N.V.

- TSMC (Taiwan Semiconductor Manufacturing Company)

- GlobalFoundries

- Powerchip Technology Corporation

- United Microelectronics Corporation (UMC)

- Cadence Design Systems, Inc.

Frequently Asked Questions

Analyze common user questions about the Hybrid Memory Cube and High Bandwidth Memory market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary driver of the Hybrid Memory Cube and High Bandwidth Memory market growth?

The primary driver is the accelerating demand for high-performance computing (HPC) across artificial intelligence (AI), machine learning (ML), and large-scale data center applications. These fields require ultra-high memory bandwidth and exceptionally low latency for efficient, rapid data processing, which HBM and HMC are uniquely positioned to provide.

How does High Bandwidth Memory (HBM) technologically differ from traditional memory like DDR?

HBM significantly differs by vertically stacking multiple memory dies on an interposer, connected via through-silicon vias (TSVs). This innovative 3D architecture enables a much wider memory interface and far greater bandwidth compared to traditional DDR memory, while simultaneously consuming less power and occupying a smaller physical footprint.

What specific role does Artificial Intelligence (AI) play in the increasing adoption of HBM and HMC technologies?

AI plays a pivotal role, as AI workloads and complex deep learning models demand immense memory bandwidth to process vast datasets quickly and efficiently. HBM, in particular, is crucial for enabling the high-performance capabilities of AI accelerators and advanced GPUs, directly supporting the continuous advancements in AI and its widespread industry implementation.

What are the main challenges currently faced by the HBM and HMC market?

Key challenges include the high manufacturing costs and inherent complexity associated with 3D stacking and advanced packaging techniques, intricate thermal management requirements for densely packed memory, and the continuous need for substantial research and development investments to maintain technological leadership and address evolving performance demands.

What are the future prospects for Hybrid Memory Cube and High Bandwidth Memory technologies?

The future prospects for HBM and HMC are highly positive, driven by continuous innovation in HBM standards (e.g., HBM3E, HBM4) promising even greater bandwidth and efficiency. The market is set to expand into emerging applications like edge AI, autonomous vehicles, and the ongoing proliferation of data centers, ensuring sustained growth and critical importance for next-generation computing paradigms.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted