High Performance Alloy Market

High Performance Alloy Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702965 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

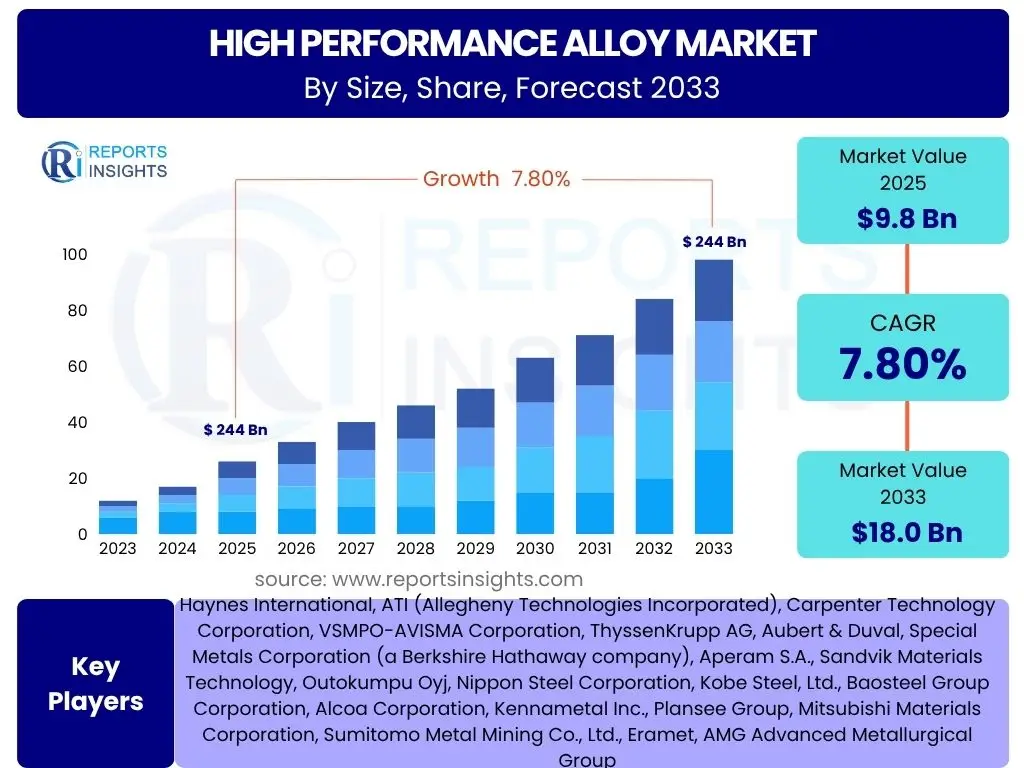

High Performance Alloy Market Size

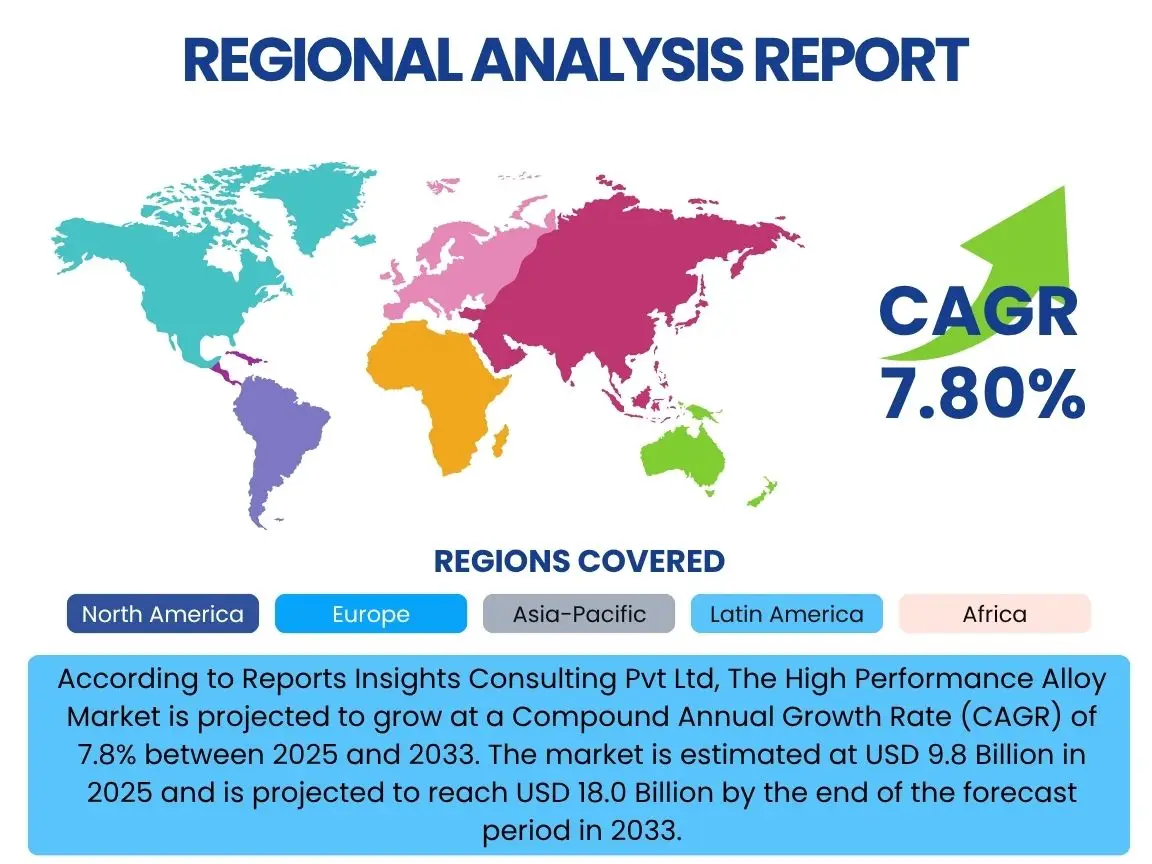

According to Reports Insights Consulting Pvt Ltd, The High Performance Alloy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 9.8 Billion in 2025 and is projected to reach USD 18.0 Billion by the end of the forecast period in 2033.

Key High Performance Alloy Market Trends & Insights

The high performance alloy market is currently experiencing significant shifts driven by evolving industrial demands and technological advancements. A primary trend involves the increasing adoption of these advanced materials in critical sectors such as aerospace, defense, and automotive, largely propelled by the imperative for lightweighting, enhanced fuel efficiency, and superior structural integrity. The demand from these industries is not only for traditional applications but also for emerging uses like electric vehicle components and advanced defense systems, requiring alloys capable of withstanding extreme conditions.

Another prominent trend is the growing integration of advanced manufacturing processes, particularly additive manufacturing (3D printing), which enables the creation of complex geometries and optimized designs with high-performance alloys, reducing waste and lead times. Concurrently, there is a strong emphasis on sustainability, leading to increased research and development in recyclable alloys and more environmentally friendly production methods. Digitalization, including material informatics and AI-driven design, is also revolutionizing how new alloys are discovered, developed, and brought to market, accelerating innovation cycles and improving material performance prediction.

- Additive Manufacturing Adoption for complex geometries and reduced waste.

- Lightweighting Imperatives in aerospace and automotive sectors for enhanced efficiency.

- Sustainable Alloy Development focusing on recyclability and eco-friendly production.

- Digital Material Design and Informatics accelerating R&D and property prediction.

- Increased Demand from Electrification in automotive and energy storage applications.

AI Impact Analysis on High Performance Alloy

Artificial Intelligence (AI) and machine learning are profoundly transforming the high performance alloy industry by revolutionizing material discovery, design, and optimization processes. AI algorithms can analyze vast datasets of material properties, processing parameters, and performance characteristics to identify novel alloy compositions with desired attributes much faster than traditional trial-and-error methods. This accelerates the development cycle for new alloys, allowing manufacturers to respond more quickly to market demands for materials with specific strength-to-weight ratios, corrosion resistance, or thermal stability, ultimately lowering research costs and time to market.

Beyond material discovery, AI is also enhancing manufacturing efficiency and quality control within the high performance alloy sector. Predictive analytics, powered by AI, can forecast equipment failures, optimize process parameters for melting, forging, and heat treatment, and identify potential defects in real-time. This leads to reduced scrap rates, improved consistency in product quality, and more energy-efficient production. Furthermore, AI-driven supply chain management tools are optimizing raw material procurement and logistics, minimizing disruptions and ensuring a steady flow of critical inputs for these complex and high-value materials.

- Accelerated Material Discovery and Design through data-driven insights.

- Predictive Performance Modeling to anticipate material behavior under various conditions.

- Optimized Manufacturing Processes leading to reduced waste and improved efficiency.

- Enhanced Quality Control and Defect Detection using real-time analytics.

- Supply Chain Optimization for raw material procurement and logistics.

Key Takeaways High Performance Alloy Market Size & Forecast

The high performance alloy market is poised for robust and sustained growth through 2033, driven by the indispensable nature of these advanced materials across a spectrum of high-tech and industrial applications. The projected significant increase in market value reflects a fundamental and enduring demand for materials that can withstand extreme environments, provide superior strength, and offer enhanced durability. This growth is underpinned by continuous innovation in material science and engineering, enabling the development of new alloys tailored for increasingly stringent performance requirements in critical sectors like aerospace, defense, and energy production.

A key takeaway from the market forecast is the strategic importance of high-performance alloys in global economic development and technological advancement. Their role in facilitating progress in areas such as efficient transportation, renewable energy infrastructure, and advanced medical devices positions them as a foundational component for future industrial growth. Furthermore, the market's resilience in the face of economic fluctuations highlights its criticality, as industries continue to prioritize performance and reliability, even amid cost pressures, ensuring a consistent and escalating demand for these specialized materials.

- Consistent Demand from Core Industries ensuring steady market expansion.

- High Growth Trajectory driven by innovation and new application areas.

- Innovation-Driven Market with continuous R&D fueling new product development.

- Strategic Importance of Alloys in enabling advanced technological progress.

High Performance Alloy Market Drivers Analysis

The high performance alloy market is primarily driven by the escalating demand from various high-growth and critical industries that require materials capable of operating under extreme conditions and offering superior properties. The aerospace and defense sectors, for instance, are constantly pushing the boundaries for lighter, stronger, and more heat-resistant materials to enhance fuel efficiency, payload capacity, and operational safety for aircraft and defense systems. This sector's continuous modernization efforts and increasing global air travel contribute significantly to the demand for advanced alloys.

Additionally, the global shift towards automotive electrification and advancements in medical technology are powerful drivers. Electric vehicles necessitate alloys that can manage high temperatures, offer corrosion resistance, and are lightweight for battery enclosures, motor components, and power electronics. In the medical field, the aging global population and continuous innovation in surgical implants and devices demand biocompatible, corrosion-resistant, and durable alloys. Furthermore, the energy sector, including traditional oil and gas as well as renewable energy (e.g., concentrated solar power, geothermal), relies heavily on these alloys for components that can withstand high temperatures and corrosive environments in turbines, reactors, and pipelines.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aerospace & Defense Sector Growth | +2.1% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Automotive Electrification & Lightweighting | +1.8% | Asia Pacific, Europe, North America | Medium-term (2025-2029) |

| Medical Device Advancement | +1.5% | North America, Europe | Long-term (2025-2033) |

| Increased Industrial Gas Turbines & Energy Demand | +1.3% | Middle East & Africa, Asia Pacific | Medium-term (2026-2031) |

High Performance Alloy Market Restraints Analysis

Despite robust growth drivers, the high performance alloy market faces significant restraints, primarily stemming from the inherent complexities and costs associated with these specialized materials. The production processes for high performance alloys are typically highly energy-intensive and require sophisticated equipment, leading to elevated manufacturing costs. Furthermore, the raw materials used, such as nickel, cobalt, titanium, and rare earth elements, are often expensive and subject to price volatility, directly impacting the final product cost and potentially limiting broader adoption in cost-sensitive applications.

Another major restraint is the volatility and vulnerability of the global supply chain for critical raw materials. Geopolitical tensions, trade disputes, and natural disasters can disrupt the availability and increase the price of essential metals, creating uncertainty for manufacturers and end-users. Additionally, the increasing stringency of environmental regulations regarding emissions, waste disposal, and resource consumption adds to the operational burden and compliance costs for alloy producers. Lastly, the emergence of alternative materials like advanced composites and ceramics, which can offer competitive performance benefits in certain niches at potentially lower costs, poses a threat of substitution, particularly in applications where the unique properties of alloys are not strictly indispensable.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs & Raw Material Prices | -1.9% | Global | Long-term (2025-2033) |

| Supply Chain Volatility & Geopolitical Risks | -1.6% | Global | Short-term to Medium-term (2025-2028) |

| Stringent Environmental Regulations | -1.2% | Europe, North America, China | Long-term (2025-2033) |

| Availability of Substitutes (e.g., Composites) | -0.8% | Global | Medium-term (2027-2032) |

High Performance Alloy Market Opportunities Analysis

The high performance alloy market presents several lucrative opportunities for growth and innovation, driven by technological advancements and evolving industrial needs. One significant opportunity lies in the burgeoning field of additive manufacturing (3D printing). This technology allows for the creation of complex geometries with reduced material waste and offers unprecedented design freedom for high-performance alloy components. As AM matures and its adoption expands across industries like aerospace and medical, it will open new avenues for customized and optimized alloy parts, driving demand for specialized alloy powders and wire forms.

Another major opportunity is presented by the global pivot towards a hydrogen economy. The development of hydrogen production, storage, and transportation infrastructure necessitates materials that can withstand high pressures, extreme temperatures, and hydrogen embrittlement. High-performance alloys are uniquely suited for these demanding applications, positioning them as critical enablers for the future of clean energy. Furthermore, the increasing focus on circular economy principles and sustainability creates opportunities for advanced recycling technologies for high-performance alloys, reducing reliance on virgin raw materials and mitigating environmental impact. Lastly, rapid industrialization and infrastructure development in emerging economies, particularly in Asia Pacific and parts of Latin America, represent untapped markets for high-performance alloys across diverse end-use sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Additive Manufacturing Expansion | +1.7% | Global | Medium-term to Long-term (2026-2033) |

| Growth of Hydrogen Economy Applications | +1.5% | Europe, Asia Pacific, North America | Long-term (2028-2033) |

| Circular Economy & Recycling Innovations | +1.2% | Europe, North America | Long-term (2027-2033) |

| Industrialization in Emerging Economies | +1.0% | Asia Pacific, Latin America | Long-term (2025-2033) |

High Performance Alloy Market Challenges Impact Analysis

The high performance alloy market faces several notable challenges that can impede its growth trajectory and operational efficiency. One primary concern is the inherent volatility in the prices of critical raw materials, such as nickel, cobalt, chromium, and molybdenum. These metals are often sourced from politically sensitive regions or are subject to global supply-demand imbalances, leading to unpredictable price fluctuations. Such volatility directly impacts manufacturing costs, profit margins, and the ability of producers to plan long-term investments, making it difficult to maintain competitive pricing and stable supply to customers.

Another significant challenge is the shortage of skilled labor and specialized expertise required for the research, development, and manufacturing of high-performance alloys. The intricate processes involved in alloying, melting, forging, and heat treatment demand highly trained metallurgists, engineers, and technicians. The scarcity of such specialized talent across the value chain can lead to higher labor costs, production inefficiencies, and a slower pace of innovation. Furthermore, geopolitical tensions and trade protectionism pose substantial risks, as they can disrupt established supply chains, impose tariffs, or create market access barriers, thereby impacting global trade flows and investment decisions within the high-performance alloy industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.5% | Global | Short-term (2025-2027) |

| Skilled Labor Shortage | -1.1% | North America, Europe | Long-term (2025-2033) |

| Geopolitical Tensions & Trade Barriers | -0.9% | Global | Short-term (2025-2027) |

| Intellectual Property Protection | -0.7% | Global | Long-term (2025-2033) |

High Performance Alloy Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the High Performance Alloy Market, offering critical insights into its current status, historical trends, and future growth projections. It covers market size estimations, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report is designed to assist stakeholders in understanding market dynamics, identifying lucrative opportunities, and making informed strategic decisions within the high performance alloy industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.8 Billion |

| Market Forecast in 2033 | USD 18.0 Billion |

| Growth Rate | 7.8% CAGR |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Haynes International, ATI (Allegheny Technologies Incorporated), Carpenter Technology Corporation, VSMPO-AVISMA Corporation, ThyssenKrupp AG, Aubert & Duval, Special Metals Corporation (a Berkshire Hathaway company), Aperam S.A., Sandvik Materials Technology, Outokumpu Oyj, Nippon Steel Corporation, Kobe Steel, Ltd., Baosteel Group Corporation, Alcoa Corporation, Kennametal Inc., Plansee Group, Mitsubishi Materials Corporation, Sumitomo Metal Mining Co., Ltd., Eramet, AMG Advanced Metallurgical Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The High Performance Alloy Market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market dynamics. This segmentation allows for targeted analysis of growth opportunities, challenges, and competitive landscapes across different material types, forms, and end-use applications. Understanding these segments is crucial for stakeholders to identify specific niches and tailor their strategies to meet the unique demands of various industries and technological requirements, ensuring efficient resource allocation and market penetration.

The market's segmentation by material type reflects the distinct properties and applications of different alloy families, while the segmentation by end-use industry highlights the primary demand drivers and application areas. Furthermore, the segmentation by form underscores the varied manufacturing processes and product formats prevalent in the industry, from bulk materials to specialized powders used in advanced manufacturing techniques like additive manufacturing. Each segment exhibits unique growth trajectories influenced by specific technological advancements, regulatory frameworks, and economic conditions within their respective domains.

- By Material Type:

- Superalloys

- Refractory Alloys

- Titanium Alloys

- Stainless Steel Alloys

- Other High Performance Alloys

- By End-Use Industry:

- Aerospace & Defense

- Industrial Gas Turbines

- Automotive

- Chemical Processing

- Medical

- Oil & Gas

- Electrical & Electronics

- Others

- By Form:

- Wrought

- Cast

- Powder

Regional Highlights

- North America: A mature market characterized by significant investments in aerospace, defense, and medical sectors. The region benefits from robust R&D infrastructure and early adoption of advanced manufacturing technologies, particularly in the US. Ongoing modernization of defense programs and growth in commercial aerospace production continue to drive demand.

- Europe: A leading region in automotive electrification, industrial gas turbines, and chemical processing. Stringent environmental regulations drive innovation towards more sustainable alloy solutions. Countries like Germany and France are key contributors, with strong manufacturing bases and emphasis on high-value industrial applications.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid industrialization, urbanization, and expanding manufacturing capabilities in countries such as China, India, and Japan. Increasing automotive production, significant infrastructure development, and growing aerospace and defense expenditures are boosting demand.

- Latin America: An emerging market with growing demand from the oil & gas and automotive sectors. Investment in renewable energy projects and industrial expansion also contribute to market growth, albeit at a slower pace compared to APAC. Brazil and Mexico are key markets within this region.

- Middle East and Africa (MEA): Driven by substantial investments in oil & gas infrastructure, power generation, and defense. Diversification efforts by economies in the GCC region into non-oil sectors are creating new opportunities for high-performance alloys in industries like aerospace and manufacturing.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the High Performance Alloy Market.- Haynes International

- ATI (Allegheny Technologies Incorporated)

- Carpenter Technology Corporation

- VSMPO-AVISMA Corporation

- ThyssenKrupp AG

- Aubert & Duval

- Special Metals Corporation (a Berkshire Hathaway company)

- Aperam S.A.

- Sandvik Materials Technology

- Outokumpu Oyj

- Nippon Steel Corporation

- Kobe Steel, Ltd.

- Baosteel Group Corporation

- Alcoa Corporation

- Kennametal Inc.

- Plansee Group

- Mitsubishi Materials Corporation

- Sumitomo Metal Mining Co., Ltd.

- Eramet

- AMG Advanced Metallurgical Group

Frequently Asked Questions

What is the High Performance Alloy market size?

The High Performance Alloy Market is projected to reach USD 18.0 Billion by 2033, growing from USD 9.8 Billion in 2025, at a Compound Annual Growth Rate (CAGR) of 7.8%.

Which industries drive the demand for High Performance Alloys?

The primary industries driving demand for High Performance Alloys include Aerospace & Defense, Industrial Gas Turbines, Automotive (especially electrification), Chemical Processing, and Medical devices, due to their need for materials with superior strength, corrosion resistance, and high-temperature performance.

What are the key trends shaping the High Performance Alloy market?

Key trends include the increasing adoption of additive manufacturing, growing emphasis on lightweighting for efficiency, development of sustainable and recyclable alloys, and the integration of digital material design and AI in research and production processes.

How does AI impact the High Performance Alloy industry?

AI significantly impacts the industry by accelerating material discovery and design, enabling predictive performance modeling, optimizing manufacturing processes for efficiency and quality, and enhancing supply chain management for critical raw materials.

What are the primary challenges in the High Performance Alloy market?

The market faces challenges such as high production costs and raw material price volatility, supply chain vulnerabilities, stringent environmental regulations, a shortage of skilled labor, and geopolitical tensions impacting trade and investment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted