High Barrier Thermoformable Film Market

High Barrier Thermoformable Film Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700347 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

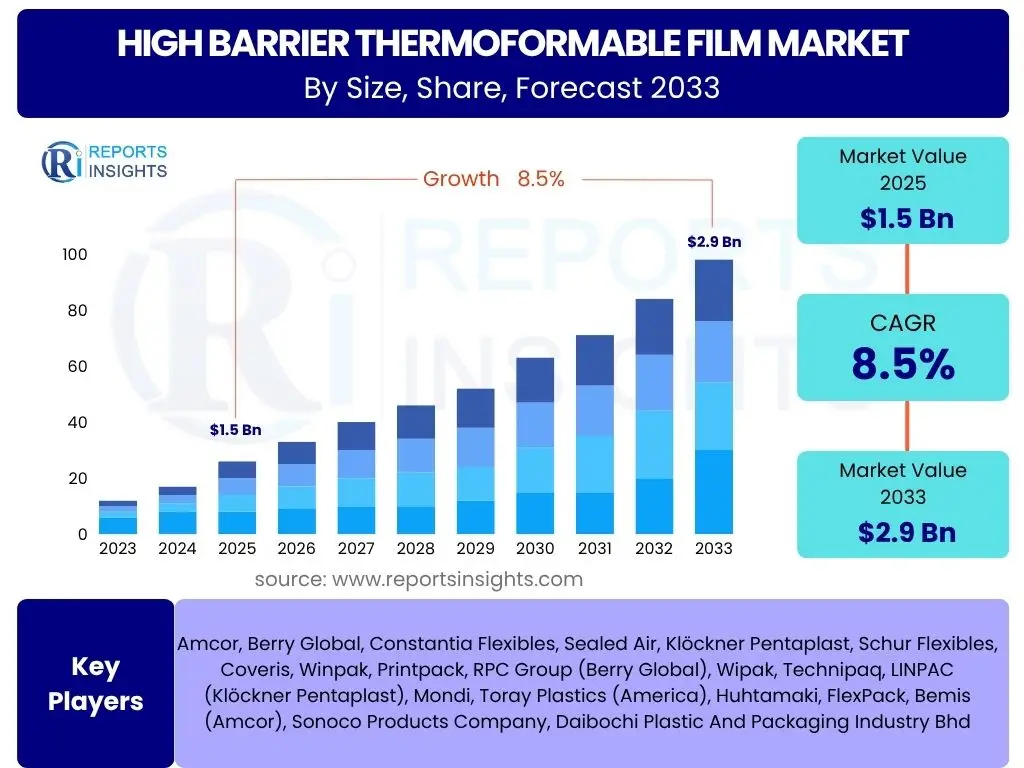

High Barrier Thermoformable Film Market Size

High Barrier Thermoformable Film Market is projected to grow at a Compound annual growth rate (CAGR) of 8.5% between 2025 and 2033, reaching an estimated USD 1.5 Billion in 2025 and is projected to grow to approximately USD 2.9 Billion by 2033, the end of the forecast period.

Key High Barrier Thermoformable Film Market Trends & Insights

The High Barrier Thermoformable Film Market is undergoing significant transformation driven by evolving consumer demands, stringent regulatory frameworks, and technological advancements. A dominant trend is the increasing demand for extended shelf life of perishable goods, particularly in the food and beverage sector, which directly fuels the adoption of high barrier films. Alongside this, there is a pronounced shift towards sustainable and eco-friendly packaging solutions, pushing manufacturers to innovate in bio-based or recyclable barrier materials. The rapid expansion of e-commerce also contributes to market growth, necessitating robust and protective packaging that can withstand complex supply chain logistics, ensuring product integrity from dispatch to delivery.

- Growing demand for extended shelf life in food and beverage products.

- Increasing focus on sustainable and recyclable barrier film solutions.

- Expansion of e-commerce requiring durable and protective packaging.

- Advancements in co-extrusion and lamination technologies.

- Rising consumer awareness regarding food safety and freshness.

- Shift towards smaller, portion-sized packaging formats.

AI Impact Analysis on High Barrier Thermoformable Film

Artificial Intelligence (AI) is poised to significantly revolutionize various facets of the High Barrier Thermoformable Film market, from production efficiencies to waste management and supply chain optimization. In manufacturing, AI-powered systems can enable predictive maintenance for machinery, minimizing downtime and optimizing production lines for higher throughput and reduced energy consumption. Furthermore, AI can enhance quality control through real-time defect detection during film extrusion and thermoforming, ensuring consistent barrier properties and reducing material waste. This capability directly improves product reliability and adherence to strict industry standards.

Beyond the factory floor, AI's analytical prowess extends to supply chain management, where it can optimize logistics, forecast demand more accurately, and reduce inventory holding costs for both raw materials and finished products. AI-driven insights can also inform product development, identifying optimal material compositions and processing parameters for novel barrier films with enhanced properties or improved sustainability profiles. Ultimately, the integration of AI can lead to more efficient, sustainable, and responsive production ecosystems within the high barrier thermoformable film industry.

- Optimized production processes and predictive maintenance for machinery.

- Enhanced quality control through real-time defect detection.

- Improved supply chain efficiency and demand forecasting.

- Accelerated material innovation and film property customization.

- Reduced waste and energy consumption in manufacturing.

Key Takeaways High Barrier Thermoformable Film Market Size & Forecast

- Market projected to reach approximately USD 2.9 Billion by 2033, growing at an 8.5% CAGR from 2025.

- Food and pharmaceutical packaging are primary growth drivers due to shelf-life extension needs.

- Sustainability initiatives are reshaping product development towards eco-friendly materials.

- Technological advancements in film properties and manufacturing processes are crucial for market expansion.

- E-commerce growth is increasing the demand for robust and protective packaging solutions.

High Barrier Thermoformable Film Market Drivers Analysis

The growth of the High Barrier Thermoformable Film Market is significantly propelled by several key factors that underscore its indispensable role in modern packaging solutions. One of the most prominent drivers is the increasing global demand for extended shelf life in perishable goods, particularly in the food and beverage industry. High barrier films effectively prevent spoilage by limiting the transmission of gases, moisture, and odors, thereby preserving freshness, nutritional value, and flavor, which is crucial for consumer satisfaction and waste reduction. This imperative extends to the pharmaceutical sector, where product integrity and protection from environmental degradation are paramount.

Furthermore, the rapid expansion of organized retail and the burgeoning e-commerce sector globally are driving the need for robust and reliable packaging. Products shipped through extensive supply chains require packaging that can withstand varied environmental conditions and handling, maintaining product quality upon arrival. High barrier thermoformable films provide this critical protection, ensuring that goods reach consumers in optimal condition. Additionally, evolving consumer lifestyles, characterized by a preference for convenience foods, single-serve portions, and ready-to-eat meals, further stimulate demand for packaging that offers both protection and ease of use, all of which are capabilities inherently offered by these advanced films.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Extended Shelf Life and Food Safety | +2.1% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Growth in Processed and Packaged Food Industry | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long-term |

| Rising E-commerce Penetration and Supply Chain Complexities | +1.5% | Global, especially urbanized regions | Medium-term |

| Technological Advancements in Film Manufacturing and Materials | +1.0% | North America, Europe, Asia Pacific (leading innovators) | Long-term |

| Increasing Pharmaceutical and Medical Packaging Applications | +1.0% | Global, particularly developed economies | Long-term |

High Barrier Thermoformable Film Market Restraints Analysis

Despite robust growth, the High Barrier Thermoformable Film Market faces several significant restraints that could temper its expansion. A primary concern revolves around the high manufacturing costs associated with these specialized films. The production of high barrier films often involves multi-layer co-extrusion or lamination processes using expensive barrier materials like EVOH or PVDC, which are inherently more costly than conventional packaging plastics. This higher production cost can limit adoption, particularly in price-sensitive emerging markets or for low-margin products, as businesses seek more economical packaging alternatives.

Another substantial restraint is the increasing environmental scrutiny and stringent regulations concerning plastic waste and sustainability. Governments and environmental organizations worldwide are imposing stricter policies on single-use plastics and promoting circular economy principles. While high barrier films are crucial for preserving goods, their multi-material, multi-layer composition often makes them challenging to recycle effectively, leading to concerns about their environmental footprint. This regulatory pressure and growing consumer preference for eco-friendly packaging solutions compel manufacturers to invest heavily in research and development for sustainable alternatives, which can be a costly and time-consuming endeavor, potentially slowing market growth if not adequately addressed.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost of Barrier Materials and Processes | -1.5% | Global, affects adoption in price-sensitive markets | Long-term |

| Environmental Concerns and Stringent Regulations on Plastic Waste | -1.8% | Europe, North America, parts of Asia Pacific (e.g., China) | Medium to Long-term |

| Lack of Developed Recycling Infrastructure for Multi-layer Films | -1.2% | Global, particularly developing nations | Long-term |

| Competition from Alternative Packaging Solutions | -0.8% | Global | Medium-term |

High Barrier Thermoformable Film Market Opportunities Analysis

The High Barrier Thermoformable Film Market is poised to capitalize on several significant opportunities driven by evolving consumer preferences, technological advancements, and untapped regional potential. A key opportunity lies in the burgeoning development and adoption of sustainable barrier film solutions. As environmental awareness grows and regulatory pressures mount, there is a substantial demand for films that are recyclable, compostable, or made from bio-based materials while still maintaining excellent barrier properties. Innovations in mono-material barrier films or the integration of advanced coating technologies to enhance biodegradability present a significant avenue for market expansion and competitive differentiation.

Furthermore, the untapped potential of emerging economies, particularly in Asia Pacific, Latin America, and the Middle East & Africa, represents a substantial growth opportunity. These regions are experiencing rapid urbanization, increasing disposable incomes, and a rising demand for packaged and processed foods, pharmaceuticals, and consumer goods. As cold chain infrastructure develops and retail networks expand in these areas, the need for high-performance packaging to ensure product integrity and extend shelf life will accelerate, providing new markets for high barrier thermoformable films. Additionally, the integration of smart packaging features, such as QR codes for traceability or temperature indicators, offers another niche for value-added products that can enhance consumer engagement and product safety.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Sustainable and Recyclable Barrier Films | +2.0% | Global, especially Europe, North America | Long-term |

| Expansion into Emerging Markets with Growing Packaged Food Demand | +1.7% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long-term |

| Technological Innovations in Barrier Coatings and Functional Additives | +1.2% | North America, Europe, Asia Pacific (R&D hubs) | Medium-term |

| Increasing Demand for Advanced Packaging in Healthcare Sector | +0.8% | Global | Long-term |

High Barrier Thermoformable Film Market Challenges Impact Analysis

The High Barrier Thermoformable Film Market faces several inherent challenges that demand strategic responses from industry players to sustain growth. One significant challenge is the volatility of raw material prices. The production of these films relies on petrochemical-derived polymers and specialized barrier resins, whose costs are subject to fluctuations in global oil prices, supply chain disruptions, and geopolitical events. This instability directly impacts manufacturing costs and profit margins for film producers, making it difficult to maintain consistent pricing and potentially deterring new investments in the sector.

Another major challenge stems from the escalating environmental concerns surrounding plastic consumption and waste. While high barrier films are essential for product preservation, their multi-layered composition often poses difficulties for traditional recycling processes, leading to increased landfill waste or incineration. This has led to mounting pressure from regulatory bodies, consumers, and environmental groups for more sustainable packaging solutions, forcing manufacturers to innovate rapidly in areas like mono-material designs or bio-based alternatives. Navigating this transition while maintaining performance standards and cost-effectiveness presents a complex hurdle. Additionally, intense competition within the packaging industry, coupled with the need for high capital investment in specialized machinery, can limit market entry for new players and pressure existing ones to continuously innovate while optimizing costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.3% | Global | Short to Medium-term |

| Pressure for Sustainable Alternatives and Circular Economy Models | -1.6% | Europe, North America, increasingly Asia Pacific | Medium to Long-term |

| Complexities in Recycling Multi-layer Barrier Films | -1.0% | Global | Long-term |

| High Capital Investment and Research & Development Costs | -0.7% | Global | Long-term |

High Barrier Thermoformable Film Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the High Barrier Thermoformable Film Market, offering critical insights into its current landscape, historical performance, and future projections. The report is meticulously crafted to empower stakeholders with actionable intelligence, covering market size estimations, growth drivers, restraints, opportunities, and challenges. It delves into detailed segmentation analysis by material, application, end-use, and region, providing a holistic view of market dynamics. Furthermore, the report profiles key industry players, offering strategic insights into their competitive strategies, product portfolios, and recent developments, ensuring a thorough understanding of the market's competitive intensity and future trajectories.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.9 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor, Berry Global, Constantia Flexibles, Sealed Air, Klöckner Pentaplast, Schur Flexibles, Coveris, Winpak, Printpack, RPC Group (Berry Global), Wipak, Technipaq, LINPAC (Klöckner Pentaplast), Mondi, Toray Plastics (America), Huhtamaki, FlexPack, Bemis (Amcor), Sonoco Products Company, Daibochi Plastic And Packaging Industry Bhd |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The High Barrier Thermoformable Film Market is comprehensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates targeted analysis and strategic decision-making for stakeholders across the value chain, identifying specific growth avenues and areas of competition.

The market is primarily segmented by material type, which differentiates films based on their chemical composition and inherent barrier properties. Key materials include Polyamide (PA) or Nylon, Ethyl Vinyl Alcohol (EVOH), Polyvinylidene Chloride (PVDC), Polyethylene Terephthalate (PET), Polypropylene (PP), and Polyethylene (PE), among others. Each material offers a unique balance of barrier effectiveness, mechanical strength, and cost-efficiency, catering to distinct packaging requirements. For instance, EVOH is highly effective against oxygen permeation, making it ideal for oxygen-sensitive foods, while PVDC provides excellent moisture and gas barrier properties. The selection of material is crucial as it directly impacts the film's performance and suitability for specific applications.

Further segmentation is based on application, delineating the various industries and product categories where high barrier thermoformable films are predominantly utilized. Food packaging represents the largest application segment, encompassing diverse sub-segments such as meat, poultry, and seafood, dairy and beverages, fresh produce, and ready meals and snacks. These sub-segments each have unique barrier requirements influenced by the product's perishability and desired shelf life. Beyond food, the market extends to pharmaceutical packaging, where the integrity and sterility of medical products are paramount, and medical packaging for devices and disposables. Industrial packaging applications also leverage these films for sensitive components requiring protection from environmental factors. The end-use industry segmentation directly correlates with these applications, covering broad sectors like Food & Beverage, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, and Industrial & Others, providing a macro-level view of market adoption.

Additionally, the market is segmented by film thickness, as this parameter significantly influences barrier performance, material consumption, and cost. Categories typically include films up to 50 microns, films between 50-100 microns, and films above 100 microns. Thicker films generally offer superior barrier properties and mechanical strength but come with higher material costs. This segmentation helps in understanding the demand for different film gauges across various applications, reflecting industry trends towards lightweighting while maintaining barrier integrity. This detailed segmentation allows for a granular analysis of market trends, technological preferences, and growth opportunities across specific product types and end-user demands, providing a robust framework for strategic planning.

- By Material:

- PA (Nylon)

- EVOH

- PVDC

- PET

- PP

- PE

- Others (e.g., COC, Silica-coated films)

- By Application:

- Food Packaging

- Meat, Poultry, & Seafood

- Dairy & Beverages

- Fresh Produce

- Ready Meals & Snacks

- Others

- Pharmaceutical Packaging

- Medical Packaging

- Industrial Packaging

- Food Packaging

- By End-Use Industry:

- Food & Beverage

- Pharmaceuticals & Healthcare

- Personal Care & Cosmetics

- Industrial & Others

- By Thickness:

- Up to 50 Microns

- 50-100 Microns

- Above 100 Microns

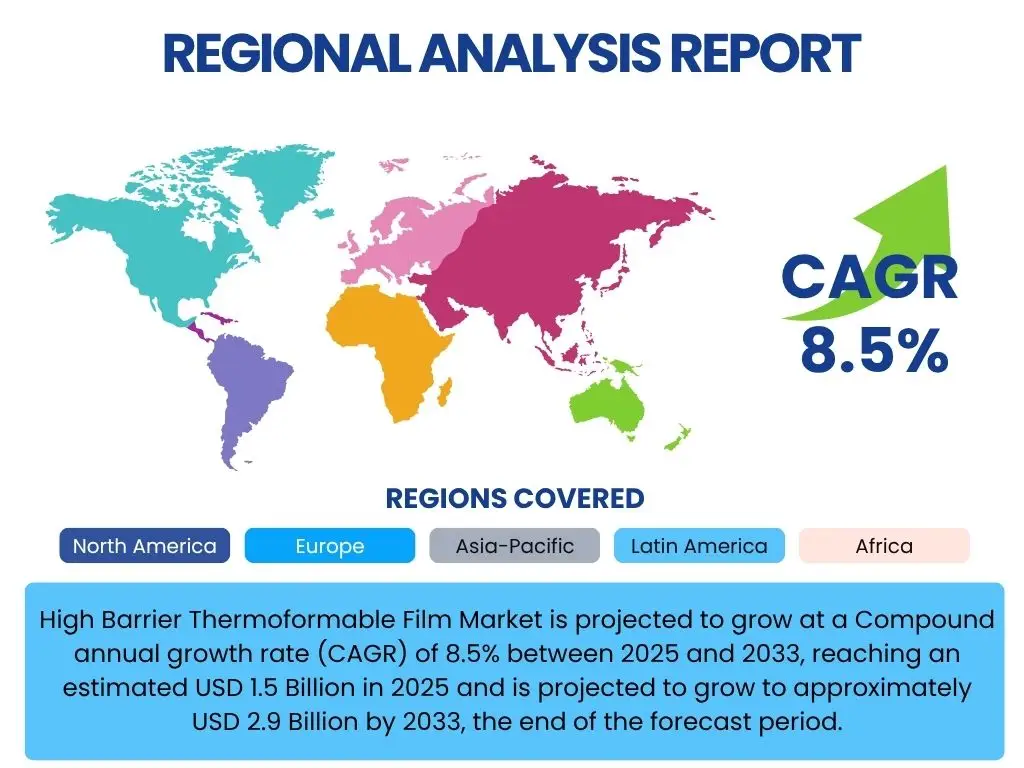

Regional Highlights

The global High Barrier Thermoformable Film Market exhibits varied growth patterns and drivers across different geographical regions, influenced by economic development, regulatory environments, and consumer preferences. Understanding these regional dynamics is crucial for strategic market penetration and investment decisions.

- North America: This region holds a significant market share, driven by a high demand for packaged and convenience foods, stringent food safety regulations, and robust growth in the pharmaceutical sector. The presence of key market players and advanced manufacturing capabilities further contributes to its dominance. Innovation in sustainable packaging solutions and increasing adoption of modified atmosphere packaging (MAP) systems are key trends fueling growth. Consumers' strong emphasis on food freshness and waste reduction also propels the demand for high barrier films.

- Europe: Europe is a mature market for high barrier thermoformable films, characterized by stringent environmental regulations and a strong focus on sustainability. The region is at the forefront of developing recyclable and bio-based barrier film technologies. Growth is fueled by the robust processed food industry, especially in countries like Germany, France, and the UK, and the increasing demand for high-quality packaging for dairy, meat, and pharmaceutical products. The push towards a circular economy significantly influences product development and market dynamics in this region.

- Asia Pacific (APAC): Expected to be the fastest-growing region, APAC offers immense opportunities due to its rapidly expanding population, increasing disposable incomes, and urbanization. Countries like China, India, Japan, and Southeast Asian nations are witnessing a surge in the consumption of packaged foods, ready-to-eat meals, and pharmaceutical products. The region's developing retail infrastructure, coupled with the rising awareness about food safety and hygiene, drives the adoption of advanced barrier packaging solutions. Significant investments in food processing and pharmaceutical industries further bolster market expansion.

- Latin America: This region is experiencing steady growth in the high barrier thermoformable film market, primarily driven by the expansion of the food processing industry and increasing foreign investments. Countries like Brazil, Mexico, and Argentina are key contributors, with rising consumer demand for packaged meat, dairy, and confectionery products. The need for extended shelf life to manage warmer climates and developing supply chains also plays a crucial role in market adoption.

- Middle East and Africa (MEA): The MEA market is projected to witness considerable growth, albeit from a smaller base. Factors such as increasing population, improving economic conditions, and rising demand for packaged and processed foods are driving market expansion. Investments in food security initiatives and the establishment of local manufacturing facilities are creating new avenues for high barrier film applications, particularly in Saudi Arabia, UAE, and South Africa.

Top Key Players:

The market research report covers the analysis of key stake holders of the High Barrier Thermoformable Film Market. Some of the leading players profiled in the report include -

- Amcor

- Berry Global

- Constantia Flexibles

- Sealed Air

- Klöckner Pentaplast

- Schur Flexibles

- Coveris

- Winpak

- Printpack

- RPC Group (Berry Global)

- Wipak

- Technipaq

- LINPAC (Klöckner Pentaplast)

- Mondi

- Toray Plastics (America)

- Huhtamaki

- FlexPack

- Bemis (Amcor)

- Sonoco Products Company

- Daibochi Plastic And Packaging Industry Bhd

Frequently Asked Questions:

What is high barrier thermoformable film?

High barrier thermoformable film is a specialized plastic film designed to provide superior protection against gases (like oxygen and nitrogen), moisture, and odors. It can be heated and molded into various shapes for packaging applications, particularly for perishable products requiring extended shelf life.

What are the primary applications of high barrier thermoformable film?

The primary applications include packaging for fresh and processed meats, poultry, seafood, dairy products, ready-to-eat meals, snacks, medical devices, and pharmaceuticals. These films are crucial for preserving product freshness, preventing spoilage, and maintaining product integrity.

What are the key drivers of market growth for high barrier thermoformable film?

Key drivers include the increasing global demand for extended shelf life of perishable goods, the rapid growth of the processed and packaged food industry, the expansion of e-commerce necessitating robust packaging, and stringent food safety regulations. Technological advancements in film materials and manufacturing also contribute significantly.

What are the main challenges faced by the high barrier thermoformable film market?

Major challenges include the high manufacturing costs associated with specialized barrier materials, increasing environmental concerns and stringent regulations regarding plastic waste, and the complexities in recycling multi-layer film structures. Volatility in raw material prices also poses a consistent challenge.

How is sustainability impacting the high barrier thermoformable film market?

Sustainability is a significant factor, driving innovation towards recyclable, bio-based, and compostable barrier film solutions. Manufacturers are focusing on developing mono-material films or advanced coatings to improve recyclability, aligning with global efforts to reduce plastic waste and promote a circular economy in packaging.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted