Heavy Metal Recycling Market

Heavy Metal Recycling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701281 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

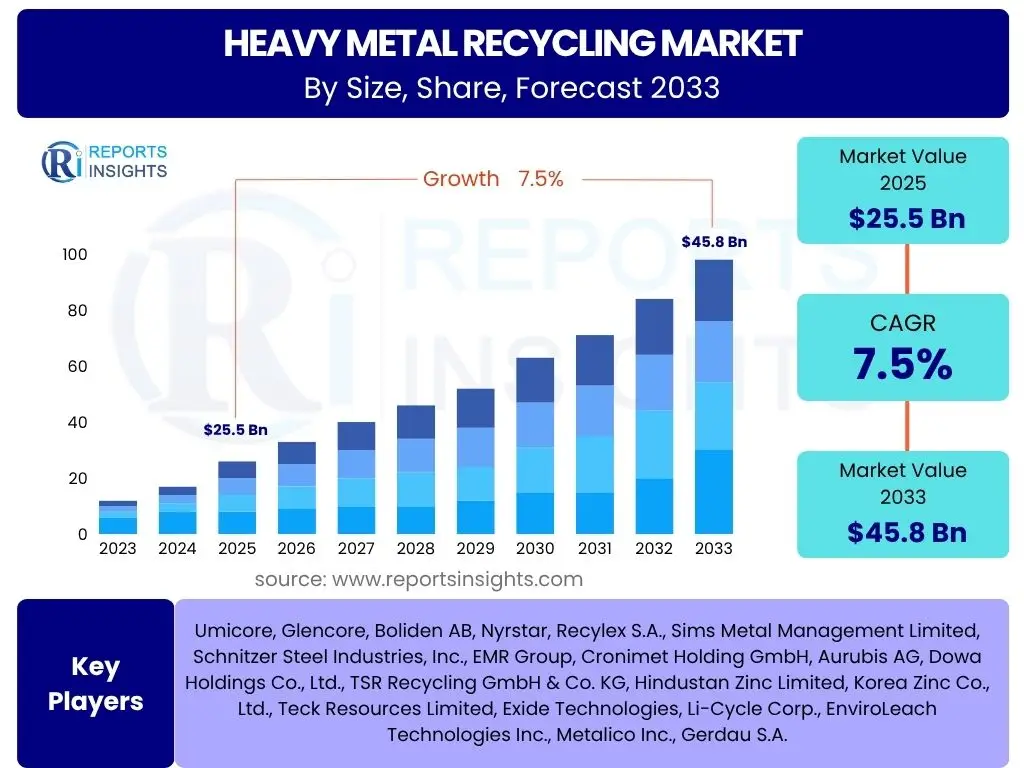

Heavy Metal Recycling Market Size

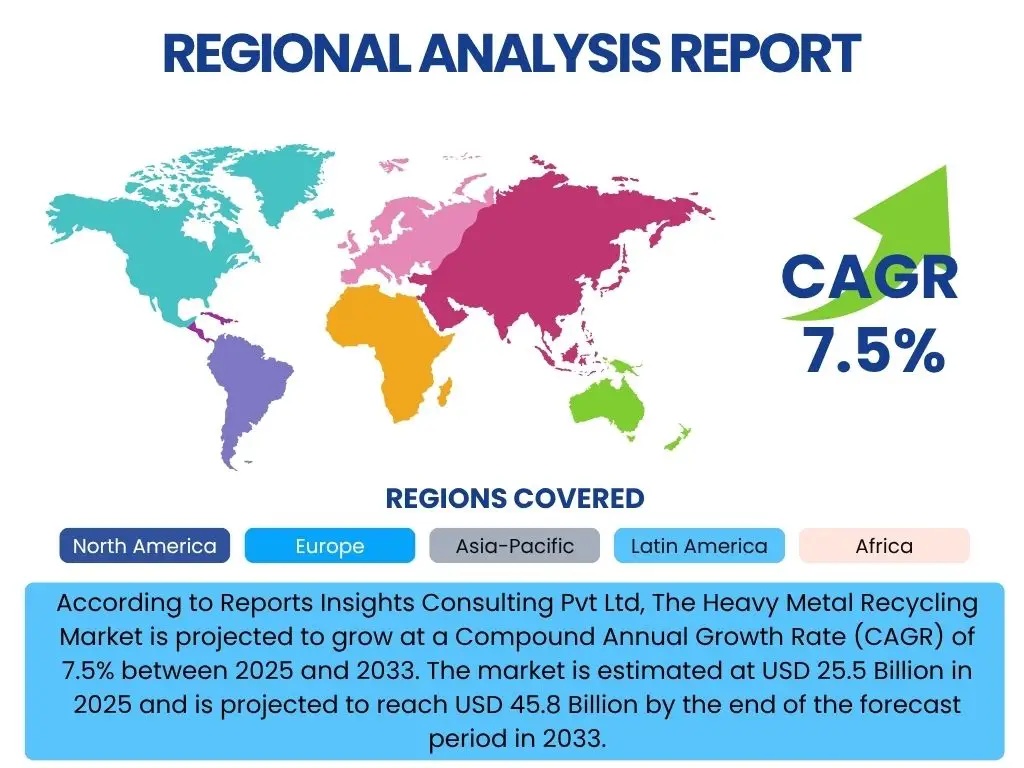

According to Reports Insights Consulting Pvt Ltd, The Heavy Metal Recycling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 25.5 Billion in 2025 and is projected to reach USD 45.8 Billion by the end of the forecast period in 2033.

Key Heavy Metal Recycling Market Trends & Insights

The heavy metal recycling market is experiencing significant shifts driven by evolving environmental regulations, increasing demand for sustainable resources, and technological advancements. Key stakeholder inquiries often revolve around the circular economy's impact, the rise of urban mining, and the implications of battery technology advancements for metal recovery. These trends underscore a broader industry movement towards more efficient, environmentally responsible, and economically viable recycling practices, aiming to reduce reliance on primary metal extraction and mitigate ecological footprints.

Furthermore, the market is witnessing a strong push towards advanced sorting and processing technologies, including sensor-based sorting and hydrometallurgical processes, which enhance recovery rates and purity. Geopolitical factors influencing raw material supply chains also contribute to the heightened interest in recycled metals, positioning them as a strategic resource. The integration of digital solutions and data analytics for supply chain optimization and material traceability is another prominent trend, addressing the complexity of diverse waste streams and supporting a more transparent recycling ecosystem.

- Growing emphasis on circular economy principles and resource efficiency.

- Development and adoption of advanced sorting and refining technologies.

- Increasing volume of End-of-Life Vehicles (ELVs) and Waste Electrical and Electronic Equipment (WEEE).

- Surging demand for critical and rare earth metals from renewable energy and electric vehicle sectors.

- Stringent environmental regulations promoting sustainable waste management.

AI Impact Analysis on Heavy Metal Recycling

User inquiries regarding AI's influence on heavy metal recycling frequently center on its potential to revolutionize operational efficiency, material identification, and process optimization. Stakeholders are keen to understand how artificial intelligence can address the inherent complexities of diverse waste streams, improve the purity of recovered metals, and enhance overall throughput. The consensus points towards AI as a critical enabler for predictive maintenance, intelligent automation, and data-driven decision-making within recycling facilities, ultimately leading to higher yields and reduced operational costs.

AI-powered vision systems, robotics, and machine learning algorithms are transforming traditional sorting processes, enabling faster and more accurate identification of specific metal types, including those within complex alloys or mixed waste. This precision significantly boosts the quality of recycled output, making it more attractive for high-value applications. Beyond the sorting line, AI contributes to optimizing logistics, managing inventory, and forecasting market demand for recycled metals, thereby creating a more responsive and resilient recycling supply chain. While initial investment and data management are considerations, the long-term benefits of AI in terms of efficiency, sustainability, and economic viability are widely recognized.

- Enhanced material identification and sorting accuracy using AI-powered vision systems and robotics.

- Optimization of recycling processes through machine learning for improved yield and efficiency.

- Predictive maintenance for recycling machinery, reducing downtime and operational costs.

- Automated quality control and real-time process adjustments for higher purity metals.

- Improved supply chain logistics and inventory management through AI-driven analytics.

Key Takeaways Heavy Metal Recycling Market Size & Forecast

Analysis of user questions concerning the heavy metal recycling market's size and forecast consistently highlights interest in the market's robust growth trajectory and the underlying drivers. A primary takeaway is the accelerating momentum of the market, driven by escalating demand for raw materials in industrial applications and the imperative for sustainable resource management. The forecast indicates significant expansion, underscoring the shift towards circular economy models and the strategic importance of recovering valuable heavy metals from waste streams to mitigate supply chain risks and environmental impact.

Furthermore, the market's projected growth is intrinsically linked to technological advancements that enhance the economic viability and efficiency of recycling processes. The increasing volume of end-of-life products, particularly from the automotive and electronics sectors, provides a consistent feedstock for the industry, ensuring sustained growth. These insights collectively emphasize that heavy metal recycling is not merely an environmental obligation but a pivotal economic sector, offering substantial opportunities for investment and innovation as global resource scarcity intensifies and sustainability goals become more stringent.

- The heavy metal recycling market is poised for substantial growth, driven by environmental mandates and resource scarcity.

- Technological advancements are critical enablers for improving recycling efficiency and expanding market scope.

- Growing industrial and consumer waste streams provide a stable and expanding supply of recyclable heavy metals.

- The market's expansion contributes significantly to circular economy initiatives and reduced reliance on virgin raw materials.

- Strategic investments in advanced recycling infrastructure and R&D are crucial for capitalizing on future opportunities.

Heavy Metal Recycling Market Drivers Analysis

The heavy metal recycling market is significantly propelled by a confluence of environmental, economic, and regulatory factors. Growing global awareness regarding the finite nature of natural resources and the detrimental environmental impact of mining and primary metal production is fostering a stronger emphasis on recycling. Governments worldwide are implementing more stringent regulations and policies, such as extended producer responsibility (EPR) schemes and landfill bans, which directly incentivize and often mandate the recycling of heavy metals from various waste streams. This regulatory push creates a structured framework for market growth and operational compliance.

Economically, the rising volatility and increasing prices of virgin metals on global markets make recycled metals an increasingly attractive and cost-effective alternative. Recycling heavy metals also conserves significant energy compared to primary production, offering an economic incentive for industries seeking to reduce operational costs and carbon footprints. Furthermore, the rapid growth of industries like electric vehicles, renewable energy, and electronics is fueling an unprecedented demand for critical and rare earth metals, many of which are heavy metals, and recycling offers a crucial supply source to meet this demand, reducing geopolitical supply risks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Policies | +1.5% | Europe, North America, Asia Pacific | Short to Medium Term (2025-2029) |

| Increasing Demand for Critical and Rare Earth Metals | +1.2% | Global, particularly Asia Pacific (China), Europe | Medium to Long Term (2027-2033) |

| Economic Benefits and Energy Savings of Recycling | +0.8% | Global | Ongoing |

| Growth in Automotive and Electronics Industries (End-of-Life Products) | +1.0% | Global | Short to Long Term (2025-2033) |

| Focus on Circular Economy and Resource Security | +0.9% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

| Technological Advancements in Recycling Processes | +0.7% | Global | Ongoing |

Heavy Metal Recycling Market Restraints Analysis

Despite significant growth drivers, the heavy metal recycling market faces several formidable restraints that can impede its full potential. A primary challenge is the high initial capital investment required for establishing advanced recycling infrastructure, including sorting, shredding, and refining facilities. This significant upfront cost can deter new entrants and limit expansion for smaller players, especially when coupled with the complexities of acquiring permits and adhering to rigorous environmental and safety standards.

Furthermore, the fluctuating prices of virgin metals introduce a degree of market volatility. When virgin metal prices drop significantly, the economic incentive for recycling can diminish, making recycled materials less competitive and impacting the profitability of recycling operations. Logistical complexities, such as the collection, transportation, and segregation of diverse heavy metal-containing waste from various sources (e.g., electronic waste, industrial sludge, automotive components), also pose considerable operational and financial burdens. Additionally, the presence of impurities and contamination in mixed waste streams necessitates advanced and often costly processing techniques to achieve high-purity recycled metals, further adding to operational expenses.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Operational Costs | -1.3% | Global, particularly developing regions | Short to Medium Term (2025-2029) |

| Volatility in Virgin Metal Prices | -1.0% | Global | Ongoing |

| Complexities of Waste Collection and Segregation | -0.8% | Global | Short to Medium Term (2025-2029) |

| Contamination and Impurity Challenges | -0.7% | Global | Ongoing |

| Lack of Standardized Recycling Infrastructure in Some Regions | -0.6% | Developing Economies, Rural Areas | Medium to Long Term (2027-2033) |

| High Energy Consumption in Certain Recycling Processes | -0.5% | Global | Ongoing |

Heavy Metal Recycling Market Opportunities Analysis

The heavy metal recycling market presents substantial opportunities driven by evolving industrial landscapes and a heightened focus on resource security. A significant avenue for growth lies in the burgeoning electric vehicle (EV) and renewable energy sectors, which heavily rely on critical heavy metals like lithium, cobalt, nickel, and rare earth elements for batteries and components. The recycling of EV batteries, in particular, is an emerging segment with immense potential, as millions of these vehicles reach their end-of-life in the coming years, creating a vast new stream of recyclable materials.

Furthermore, the concept of "urban mining," which involves recovering valuable metals from discarded electronic devices and infrastructure, offers a rich and readily accessible source of secondary raw materials, reducing the environmental impact and cost associated with traditional mining. Advancements in hydrometallurgical and pyrometallurgical processes, coupled with sensor-based sorting technologies, are continuously improving the efficiency and economic viability of extracting high-purity metals from complex waste streams. Strategic partnerships between recyclers, original equipment manufacturers (OEMs), and governments can also create closed-loop systems, ensuring a consistent supply of materials and fostering innovation in product design for recyclability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Electric Vehicle (EV) Battery Recycling | +1.8% | Global, particularly Europe, North America, Asia Pacific (China) | Medium to Long Term (2027-2033) |

| Expansion of Urban Mining Initiatives (WEEE, C&D Waste) | +1.5% | Developed Economies (Europe, North America, Japan) | Short to Long Term (2025-2033) |

| Development of Advanced & Cost-Effective Recycling Technologies | +1.0% | Global | Ongoing |

| Increasing Focus on Critical Raw Material Security | +0.9% | Europe, North America, Japan, South Korea | Medium to Long Term (2027-2033) |

| Public-Private Partnerships and Policy Support for Circular Economy | +0.7% | Global | Short to Medium Term (2025-2029) |

| Emerging Markets for Recycled Metals in Developing Economies | +0.6% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Medium to Long Term (2027-2033) |

Heavy Metal Recycling Market Challenges Impact Analysis

The heavy metal recycling market faces numerous challenges that can hinder its operational efficiency and scalability. One significant hurdle is the complexity and heterogeneity of heavy metal-containing waste streams. Products like electronics, batteries, and industrial catalysts often contain a diverse mix of metals and other materials, making their separation and purification challenging and energy-intensive. Achieving high purity levels for recovered metals requires sophisticated and often costly processes, impacting the economic viability of recycling, particularly for lower-value metals or highly contaminated streams.

Another major challenge involves the health and safety risks associated with handling hazardous heavy metal waste. Proper containment, specialized equipment, and trained personnel are essential to prevent exposure and environmental contamination, adding to operational costs and regulatory burdens. Furthermore, the informal recycling sector, particularly prevalent in developing countries, poses challenges through unsustainable practices that lead to environmental pollution and loss of valuable materials, undermining the efforts of formal, compliant recycling operations. Addressing these issues requires comprehensive policy frameworks, technological advancements, and robust enforcement mechanisms.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Diverse Waste Streams Composition | -1.1% | Global | Ongoing |

| Health, Safety, and Environmental Risks of Handling Hazardous Waste | -0.9% | Global | Ongoing |

| Competition from the Informal Recycling Sector (Developing Economies) | -0.8% | Asia Pacific, Latin America, Africa | Short to Medium Term (2025-2029) |

| High Energy Consumption for Certain Pyrometallurgical Processes | -0.7% | Global | Ongoing |

| Lack of Consumer Awareness and Proper Collection Systems | -0.6% | Developing Economies | Short to Medium Term (2025-2029) |

| Disposal of Residual Waste and By-Products | -0.5% | Global | Ongoing |

Heavy Metal Recycling Market - Updated Report Scope

This report offers a comprehensive analysis of the heavy metal recycling market, providing in-depth insights into market size, growth drivers, restraints, opportunities, and challenges. It covers detailed segmentation by metal type, source, and end-use industry across major global regions, offering a holistic view of the market dynamics from historical trends to future projections. The report is designed to assist stakeholders in making informed strategic decisions by understanding the competitive landscape, key trends, and emerging opportunities within the heavy metal recycling ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 45.8 Billion |

| Growth Rate | 7.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Umicore, Glencore, Boliden AB, Nyrstar, Recylex S.A., Sims Metal Management Limited, Schnitzer Steel Industries, Inc., EMR Group, Cronimet Holding GmbH, Aurubis AG, Dowa Holdings Co., Ltd., TSR Recycling GmbH & Co. KG, Hindustan Zinc Limited, Korea Zinc Co., Ltd., Teck Resources Limited, Exide Technologies, Li-Cycle Corp., EnviroLeach Technologies Inc., Metalico Inc., Gerdau S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The heavy metal recycling market is extensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates a detailed analysis of market performance across different metal types, sources of waste, and end-use applications, enabling stakeholders to identify specific growth areas and strategic opportunities. Each segment possesses unique characteristics, driven by varying demand patterns, regulatory landscapes, and technological requirements for efficient recycling.

Understanding these segments is crucial for market participants to tailor their strategies, invest in appropriate technologies, and optimize their supply chains. For instance, the recycling of critical and rare earth metals from electronic waste differs significantly from processing ferrous metals from construction demolition, necessitating distinct operational approaches and capital allocation. This comprehensive segmentation highlights the complexity and multifaceted nature of the heavy metal recycling industry, reflecting its vital role in modern industrial ecosystems and resource management.

- By Metal Type:

- Ferrous Metals (Iron, Steel)

- Non-Ferrous Metals (Aluminum, Copper, Lead, Zinc, Nickel, Tin, Titanium, Chromium)

- Precious Metals (Gold, Silver, Platinum, Palladium, Rhodium)

- Critical & Rare Earth Metals (Lithium, Cobalt, Neodymium, Dysprosium, Germanium)

- By Source:

- Automotive (End-of-Life Vehicles, Catalytic Converters, Batteries)

- Electrical & Electronic Equipment (WEEE)

- Industrial Waste (Slags, Sludges, Ash, Spent Catalysts)

- Construction & Demolition Waste

- Batteries (Lead-acid, Li-ion, Ni-Cd)

- Jewelry and Coinage

- By End-Use Industry:

- Automotive

- Building & Construction

- Electrical & Electronics

- Packaging

- Aerospace & Defense

- Battery Manufacturing

- Jewelry

- Others

Regional Highlights

The heavy metal recycling market exhibits distinct regional dynamics, influenced by varying industrialization levels, regulatory frameworks, technological adoption, and waste generation patterns. North America, with its established industrial base and stringent environmental regulations, demonstrates a mature heavy metal recycling market. The region benefits from advanced technological infrastructure and increasing emphasis on circular economy initiatives, particularly in automotive and electronics recycling. Robust governmental support for sustainable practices and investments in new recycling technologies are key drivers in this region, ensuring a steady stream of materials and demand for recycled content.

Europe stands as a frontrunner in heavy metal recycling, largely due to its ambitious environmental policies and pioneering circular economy directives. The European Union's directives on Waste Electrical and Electronic Equipment (WEEE), End-of-Life Vehicles (ELVs), and batteries have fostered a highly structured and efficient recycling ecosystem. Countries like Germany, Belgium, and Sweden are notable for their high collection and recycling rates, driven by strong public awareness and private sector innovation in resource recovery from complex waste streams, including critical raw materials for strategic autonomy.

Asia Pacific is projected to be the fastest-growing region in the heavy metal recycling market, primarily propelled by rapid industrialization, urbanization, and a massive increase in waste generation, particularly electronic waste. Countries such as China, Japan, South Korea, and India are investing heavily in establishing and upgrading their recycling infrastructure. While regulatory enforcement and informal recycling remain challenges in some parts of the region, the sheer volume of recyclable materials and the growing awareness of resource scarcity are driving significant market expansion and technological adoption, positioning APAC as a crucial hub for future growth in heavy metal recycling.

Latin America and the Middle East & Africa regions are emerging markets with considerable untapped potential. While currently characterized by less developed recycling infrastructure and a higher reliance on informal recycling, increasing foreign investments, rising environmental concerns, and a growing industrial base are gradually shifting these regions towards more formalized and efficient heavy metal recycling practices. The demand for metals in sectors like construction and automotive, coupled with the long-term vision for sustainable development, is expected to drive significant growth and development in these regions over the forecast period.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Heavy Metal Recycling Market.- Umicore

- Glencore

- Boliden AB

- Nyrstar

- Recylex S.A.

- Sims Metal Management Limited

- Schnitzer Steel Industries, Inc.

- EMR Group

- Cronimet Holding GmbH

- Aurubis AG

- Dowa Holdings Co., Ltd.

- TSR Recycling GmbH & Co. KG

- Hindustan Zinc Limited

- Korea Zinc Co., Ltd.

- Teck Resources Limited

- Exide Technologies

- Li-Cycle Corp.

- EnviroLeach Technologies Inc.

- Metalico Inc.

- Gerdau S.A.

Frequently Asked Questions

Analyze common user questions about the Heavy Metal Recycling market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is heavy metal recycling?

Heavy metal recycling is the process of collecting, processing, and reintroducing used or scrap heavy metals into the manufacturing cycle. This includes metals like lead, copper, zinc, nickel, and precious metals, recovering them from end-of-life products such as electronics, batteries, and automotive components to reduce reliance on virgin resources and minimize environmental impact.

Why is heavy metal recycling important?

Heavy metal recycling is crucial for several reasons: it conserves finite natural resources, significantly reduces energy consumption compared to primary metal production, mitigates environmental pollution from mining and landfilling, lowers greenhouse gas emissions, and provides a sustainable source of raw materials for various industries, enhancing resource security.

What are the primary sources of heavy metals for recycling?

The primary sources of heavy metals for recycling include End-of-Life Vehicles (ELVs), Waste Electrical and Electronic Equipment (WEEE) such as computers and mobile phones, industrial waste streams (slags, catalysts), spent batteries (lead-acid, lithium-ion), and construction and demolition waste materials. Urban mining from these waste streams is increasingly significant.

What technologies are used in heavy metal recycling?

Modern heavy metal recycling employs various technologies, including mechanical processes (shredding, crushing, sorting), pyrometallurgical methods (smelting, refining), hydrometallurgical methods (leaching, solvent extraction, electrolysis), and advanced sensor-based sorting using X-ray fluorescence (XRF) or near-infrared (NIR) to enhance separation efficiency and purity.

What is the future outlook for the heavy metal recycling market?

The future outlook for the heavy metal recycling market is highly positive, driven by increasing global demand for metals, stringent environmental regulations, and the expansion of electric vehicle and renewable energy sectors. Technological advancements and the growing emphasis on circular economy principles are expected to fuel substantial growth and innovation, making recycled metals a critical component of sustainable industrial supply chains.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted