Heavy Duty Battery Market

Heavy Duty Battery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709349 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

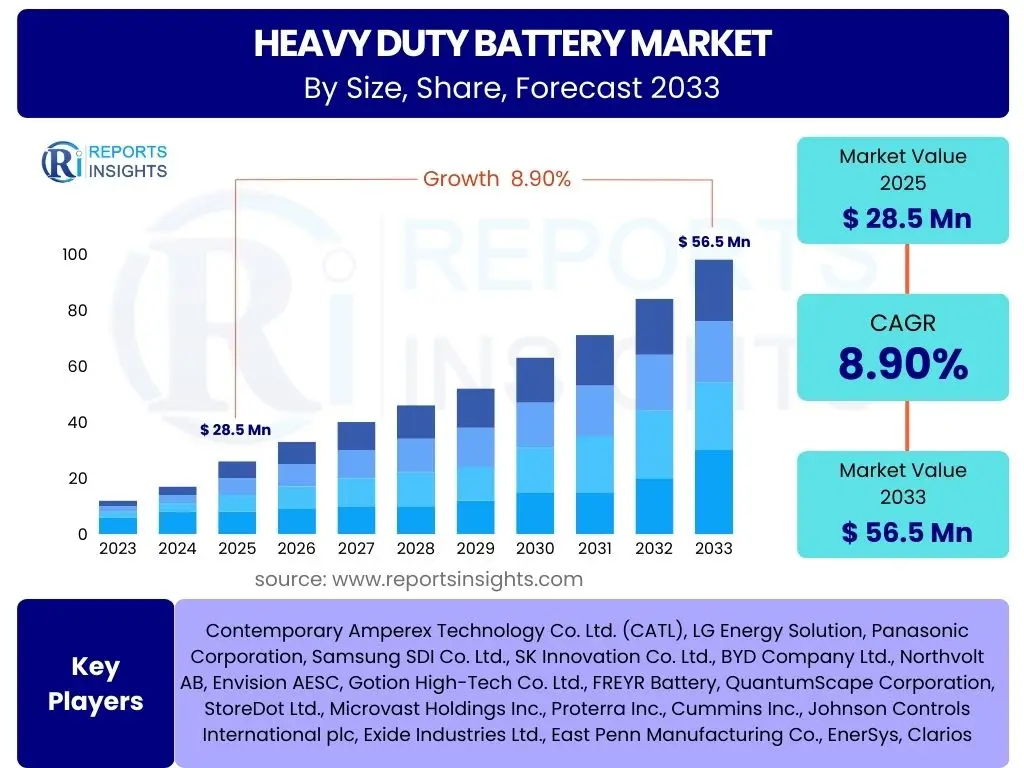

Heavy Duty Battery Market Size

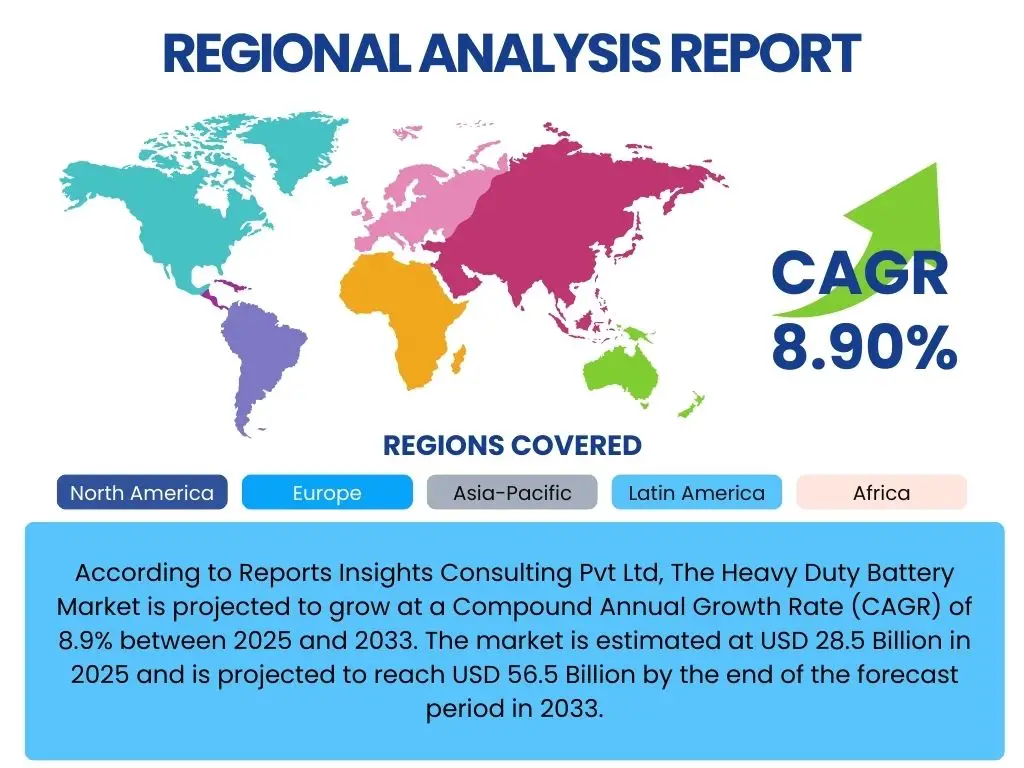

According to Reports Insights Consulting Pvt Ltd, The Heavy Duty Battery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 28.5 Billion in 2025 and is projected to reach USD 56.5 Billion by the end of the forecast period in 2033.

Key Heavy Duty Battery Market Trends & Insights

The heavy-duty battery market is currently undergoing significant transformation, driven by a confluence of technological advancements, evolving regulatory landscapes, and increasing demand from various industrial sectors. Users frequently inquire about the shift towards sustainable energy solutions, the impact of electrification on commercial fleets, and the innovation in battery chemistry. Insights suggest a strong push towards higher energy density, longer cycle life, and faster charging capabilities to meet the rigorous demands of heavy-duty applications. Furthermore, the integration of smart battery management systems (BMS) and predictive analytics is emerging as a critical trend, optimizing performance and extending operational lifespans.

There is also considerable interest in the diversification of battery technologies beyond traditional lead-acid, with lithium-ion variants gaining substantial traction across commercial vehicles, industrial machinery, and grid storage for heavy loads. The global supply chain dynamics, including raw material sourcing and geopolitical factors, are also frequently discussed topics, as they directly influence market stability and pricing. Overall, the market is characterized by a drive for efficiency, durability, and environmental responsibility, shaping the developmental trajectory of new battery solutions for heavy-duty applications worldwide.

- Electrification of commercial and industrial vehicle fleets (trucks, buses, construction equipment).

- Transition from lead-acid to advanced battery chemistries, primarily Lithium-ion (Li-ion).

- Development of solid-state and other next-generation battery technologies for enhanced safety and energy density.

- Integration of sophisticated Battery Management Systems (BMS) for optimized performance, diagnostics, and longevity.

- Increasing focus on battery recycling and second-life applications to promote circular economy principles.

- Advancements in fast-charging infrastructure and swappable battery solutions for heavy-duty applications.

- Deployment of heavy-duty batteries in renewable energy grid storage for industrial and utility-scale uses.

- Rising demand for customized battery solutions tailored to specific heavy-duty operational requirements.

AI Impact Analysis on Heavy Duty Battery

Users frequently express curiosity regarding how artificial intelligence (AI) will influence the design, manufacturing, and operational efficiency of heavy-duty batteries. The primary themes revolve around predictive maintenance, optimization of charging cycles, and enhanced battery life. AI algorithms are increasingly being deployed to analyze vast datasets collected from battery performance in real-world heavy-duty applications. This analysis enables real-time monitoring, identifies anomalies indicative of potential failures, and predicts the remaining useful life of batteries, thereby minimizing downtime and reducing operational costs for fleet operators and industrial users.

Furthermore, AI plays a crucial role in optimizing battery charging and discharging strategies to maximize efficiency and extend cycle life. Through machine learning models, AI can adapt to varying operational conditions, temperature fluctuations, and load demands, ensuring that batteries operate within optimal parameters. In the manufacturing sector, AI is being explored for quality control, material optimization, and accelerating the research and development of new battery chemistries, promising faster innovation cycles and more reliable products. The expectations are high for AI to significantly enhance the overall value proposition of heavy-duty battery solutions, making them more intelligent, resilient, and cost-effective.

- Predictive maintenance and fault detection for heavy-duty battery systems, reducing downtime.

- Optimization of charging and discharging cycles through AI algorithms, extending battery lifespan.

- Enhanced battery management systems (BMS) with AI for real-time performance monitoring and anomaly detection.

- AI-driven design and simulation for new battery chemistries and architectures, accelerating R&D.

- Improved supply chain management and inventory optimization for battery components and raw materials using AI.

- Personalized energy management strategies for diverse heavy-duty applications based on AI analysis of usage patterns.

- Automation and quality control in battery manufacturing processes facilitated by AI and machine vision.

Key Takeaways Heavy Duty Battery Market Size & Forecast

Common user questions regarding market size and forecasts often center on the primary growth drivers, the segments showing the most promise, and the overall trajectory of market expansion. The key takeaway is the robust growth propelled by the global imperative for decarbonization and the extensive electrification across commercial and industrial sectors. The market is not merely expanding in volume but also undergoing a significant qualitative shift towards advanced battery technologies with superior performance characteristics. This fundamental transformation underpins the substantial projected growth figures and highlights a sustained period of innovation and adoption.

The forecast period indicates a continued acceleration in demand, primarily fueled by supportive government policies, increasing corporate commitments to sustainability, and technological breakthroughs that are steadily lowering the total cost of ownership for electric heavy-duty vehicles and machinery. Geographically, certain regions are emerging as hotspots for adoption due to stringent emissions regulations and significant investment in charging infrastructure. Understanding these dynamics is critical for stakeholders looking to capitalize on the market's upward trend and identify lucrative opportunities within this evolving landscape.

- Significant Compound Annual Growth Rate (CAGR) projected at 8.9% from 2025 to 2033, indicating strong market expansion.

- Market valuation expected to nearly double from USD 28.5 Billion in 2025 to USD 56.5 Billion by 2033.

- Electrification of heavy-duty transportation and industrial equipment is the primary growth catalyst.

- Lithium-ion batteries are expected to dominate market share due to superior energy density and cycle life.

- Emerging markets and regions with strict emissions regulations will contribute significantly to demand.

- Continued R&D in battery technology, including solid-state and advanced chemistries, will drive further innovation and market penetration.

- Investment in robust charging infrastructure and battery swapping solutions is crucial for sustained market growth.

- The market's long-term sustainability will rely on advancements in recycling and second-life applications.

Heavy Duty Battery Market Drivers Analysis

The heavy-duty battery market is significantly propelled by the global movement towards electrification and decarbonization across various industries. Regulatory pressures, government incentives, and corporate sustainability mandates are forcing fleet operators and industrial companies to transition from fossil fuel-powered heavy equipment to electric alternatives. This shift necessitates the deployment of robust and high-capacity battery solutions capable of meeting the demanding operational requirements of trucks, buses, construction machinery, and material handling equipment. Consequently, the demand for reliable, long-lasting, and powerful heavy-duty batteries is experiencing unprecedented growth.

Technological advancements in battery chemistry, particularly within the lithium-ion segment, are also major drivers. Improvements in energy density, power output, charging speed, and cycle life have made heavy-duty electric vehicles and machinery more viable and competitive. These innovations reduce the total cost of ownership (TCO) by lowering fuel expenses and maintenance requirements, making the switch to electric more economically attractive for businesses. Furthermore, the expansion of renewable energy generation and the need for utility-scale energy storage solutions for grid stability also contribute to the demand for heavy-duty batteries, showcasing the market's multifaceted growth catalysts.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Electrification of Commercial & Industrial Fleets | +2.5% | North America, Europe, Asia Pacific | Short to Long-term |

| Stringent Emission Regulations & Carbon Neutrality Goals | +2.0% | Europe, China, California (USA) | Mid to Long-term |

| Advancements in Battery Technology (Energy Density, Life Cycle) | +1.8% | Global | Short to Mid-term |

| Decreasing Total Cost of Ownership (TCO) for Electric Vehicles | +1.5% | Global | Mid to Long-term |

| Growing Demand for Renewable Energy Storage Solutions | +1.0% | North America, Europe, Australia | Mid to Long-term |

Heavy Duty Battery Market Restraints Analysis

Despite the robust growth trajectory, the heavy-duty battery market faces several significant restraints that could temper its expansion. One of the primary concerns is the high initial capital investment required for electric heavy-duty vehicles and their associated battery systems, which often exceeds the cost of traditional fossil fuel-powered counterparts. This upfront cost can be a substantial barrier to adoption for small and medium-sized enterprises (SMEs) or those operating on thin margins, particularly in less developed regions. While the total cost of ownership may decrease over time due to lower operational costs, the initial outlay remains a critical hurdle.

Another major restraint involves the limitations of current charging infrastructure for heavy-duty applications. The sheer power requirements and longer charging times for large battery packs necessitate specialized high-power charging stations, which are not yet widely available or standardized across all regions. This lack of adequate infrastructure creates range anxiety and operational inefficiencies for fleet managers. Furthermore, concerns regarding the safety of high-energy-density batteries, particularly in demanding heavy-duty environments, as well as the environmental impact and ethical sourcing of raw materials like lithium, cobalt, and nickel, also present significant challenges that require ongoing innovation and regulatory oversight.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure for Battery Systems | -1.5% | Global, particularly Emerging Markets | Short to Mid-term |

| Limited Heavy-Duty Charging Infrastructure Availability | -1.2% | Global, varies by region | Short to Mid-term |

| Concerns Regarding Battery Range and Charging Time | -1.0% | Global | Short to Mid-term |

| Supply Chain Volatility and Raw Material Sourcing Issues | -0.8% | Global | Short to Mid-term |

| Challenges in Battery Recycling and Disposal | -0.5% | Global | Long-term |

Heavy Duty Battery Market Opportunities Analysis

The heavy-duty battery market is rich with opportunities, primarily stemming from the increasing global commitment to sustainable development and the rapid pace of technological innovation. One significant opportunity lies in the development of next-generation battery technologies, such as solid-state batteries, which promise higher energy density, faster charging, and enhanced safety compared to current lithium-ion chemistries. Investment in these advanced materials and designs could unlock new performance benchmarks, making electric heavy-duty applications even more competitive and widespread. Furthermore, the expansion into new application areas beyond traditional transportation, such as marine, aviation, and heavy mining equipment, presents substantial untapped market potential.

Another key opportunity is the development of robust and scalable charging infrastructure solutions specifically tailored for heavy-duty vehicles. This includes ultra-fast charging stations, smart grid integration, and battery-swapping technologies, which can significantly address range and downtime concerns. Moreover, the circular economy offers immense potential through advanced battery recycling and second-life applications, where used heavy-duty batteries can be repurposed for less demanding roles like stationary energy storage. This not only reduces waste but also provides a sustainable revenue stream and mitigates concerns regarding raw material scarcity, positioning the market for long-term growth and environmental responsibility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Generation Battery Technologies (Solid-State) | +2.2% | Global (with R&D hubs in APAC, Europe, North America) | Mid to Long-term |

| Expansion into New Heavy-Duty Application Segments | +1.8% | Global | Mid to Long-term |

| Growth of Advanced Charging Infrastructure & Smart Grid Integration | +1.5% | North America, Europe, China | Short to Mid-term |

| Implementation of Battery Recycling & Second-Life Programs | +1.0% | Europe, North America, Japan | Long-term |

| Strategic Partnerships & Collaborative R&D Initiatives | +0.8% | Global | Short to Mid-term |

Heavy Duty Battery Market Challenges Impact Analysis

The heavy-duty battery market faces several daunting challenges that require concerted efforts from manufacturers, policymakers, and infrastructure developers. One significant challenge revolves around thermal management and safety concerns associated with high-power, high-capacity battery packs operating in extreme conditions typical of heavy-duty applications. Ensuring the thermal stability and preventing runaway reactions in large battery arrays, especially under heavy loads or rapid charging, remains a complex engineering hurdle. Additionally, the weight and volume of current battery technologies can still pose limitations, impacting payload capacity and design flexibility for certain heavy-duty vehicles, demanding continuous innovation in energy density.

Another crucial challenge is the ongoing volatility and ethical concerns surrounding the supply chain of critical raw materials such as lithium, cobalt, and nickel. Geopolitical tensions, mining practices, and market speculation can lead to price fluctuations and supply disruptions, affecting production costs and scalability. Furthermore, the standardization of charging interfaces and communication protocols across different manufacturers and regions is a significant obstacle. Lack of interoperability can hinder widespread adoption and complicate infrastructure development, requiring industry-wide collaboration to establish universal standards that facilitate seamless integration and operation across the heavy-duty electric ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management & Safety Concerns in High-Density Batteries | -1.8% | Global | Short to Mid-term |

| High Raw Material Costs and Supply Chain Volatility | -1.5% | Global | Short to Mid-term |

| Standardization of Charging Infrastructure and Protocols | -1.2% | Global, particularly Europe and North America | Short to Mid-term |

| Weight and Volume Limitations of Current Battery Systems | -1.0% | Global | Short to Mid-term |

| Regulatory Complexities and Permitting for New Infrastructure | -0.7% | Regional/Country Specific | Mid-term |

Heavy Duty Battery Market - Updated Report Scope

This report provides a comprehensive analysis of the Heavy Duty Battery Market, encompassing market size estimations, growth forecasts, key trends, drivers, restraints, and opportunities. It details the impact of emerging technologies and regulatory landscapes on market dynamics across various segments and major geographical regions. The scope also includes an in-depth profiling of leading market players, offering insights into their strategies and competitive positioning. The objective is to equip stakeholders with actionable intelligence for strategic decision-making in this rapidly evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 56.5 Billion |

| Growth Rate | 8.9% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Contemporary Amperex Technology Co. Ltd. (CATL), LG Energy Solution, Panasonic Corporation, Samsung SDI Co. Ltd., SK Innovation Co. Ltd., BYD Company Ltd., Northvolt AB, Envision AESC, Gotion High-Tech Co. Ltd., FREYR Battery, QuantumScape Corporation, StoreDot Ltd., Microvast Holdings Inc., Proterra Inc., Cummins Inc., Johnson Controls International plc, Exide Industries Ltd., East Penn Manufacturing Co., EnerSys, Clarios |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The heavy-duty battery market is broadly segmented by battery type, vehicle type, application, and capacity, reflecting the diverse demands and technological considerations across various heavy-duty sectors. This segmentation allows for a granular understanding of market dynamics, identifying specific growth pockets and technological preferences. The choice of battery type, for instance, significantly impacts performance, cost, and lifecycle, with lithium-ion variants rapidly gaining dominance due to their superior energy density and longer lifespan compared to traditional lead-acid batteries. Each segment presents unique operational requirements and market drivers, influencing the adoption rates of different battery technologies.

Analyzing these segments helps in understanding how various industrial and commercial sectors are transitioning towards electrification and the specific battery solutions they require. For example, commercial trucks and buses demand high-capacity, fast-charging batteries for extended ranges, while material handling equipment may prioritize robustness and deep-cycle capabilities. The detailed segmentation also provides insights into regional variations in adoption, driven by local regulations, infrastructure development, and economic factors. This comprehensive approach to market segmentation is crucial for stakeholders to tailor their product offerings and market strategies effectively.

- By Battery Type: Lead-Acid Batteries, Lithium-ion Batteries (LFP, NMC, LTO), Nickel-Metal Hydride Batteries, Solid-State Batteries, Others

- By Vehicle Type: Commercial Trucks (Light, Medium, Heavy-Duty), Buses (City, Coach, School), Construction & Mining Equipment, Material Handling Equipment (Forklifts, Stackers), Agricultural Machinery, Marine Vessels, Others

- By Application: Transportation (Road, Off-Road), Industrial (Manufacturing, Warehousing), Grid Energy Storage, Defense, Others

- By Capacity: Below 100 kWh, 100 kWh - 300 kWh, Above 300 kWh

Regional Highlights

- Asia Pacific: Expected to be the largest and fastest-growing market, driven by robust industrial growth, rapid urbanization, significant government investments in electric vehicle (EV) infrastructure, and stringent emission standards in countries like China, India, and Japan. The region is a major manufacturing hub for batteries and electric vehicles.

- Europe: Demonstrates strong growth due to ambitious decarbonization targets, supportive regulatory frameworks, and substantial investments in electric truck and bus fleets. Countries such as Germany, France, and the UK are leading in the adoption of electric heavy-duty vehicles and advanced battery technologies.

- North America: Significant market potential fueled by increasing adoption of electric school buses, last-mile delivery trucks, and heavy-duty vehicles, particularly in California and other states with progressive environmental policies. Investments in charging infrastructure and federal incentives are key growth enablers.

- Latin America: Emerging market with increasing interest in electric buses for public transport and heavy-duty applications in mining. Growth is moderate but expected to accelerate with favorable government policies and growing environmental awareness.

- Middle East and Africa (MEA): Nascent market with growing awareness and initial investments in electric public transport and industrial applications. Future growth is tied to diversification of economies, renewable energy projects, and infrastructure development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Heavy Duty Battery Market.- Contemporary Amperex Technology Co. Ltd. (CATL)

- LG Energy Solution

- Panasonic Corporation

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- BYD Company Ltd.

- Northvolt AB

- Envision AESC

- Gotion High-Tech Co. Ltd.

- FREYR Battery

- QuantumScape Corporation

- StoreDot Ltd.

- Microvast Holdings Inc.

- Proterra Inc.

- Cummins Inc.

- Johnson Controls International plc

- Exide Industries Ltd.

- East Penn Manufacturing Co.

- EnerSys

- Clarios

Frequently Asked Questions

What are the primary factors driving the growth of the heavy-duty battery market?

The market's growth is primarily driven by the global push for electrification of commercial and industrial fleets, stringent emission regulations, advancements in battery technology offering higher energy density and longer life, and the decreasing total cost of ownership for electric heavy-duty vehicles compared to traditional alternatives.

Which battery technologies are most prevalent in the heavy-duty sector?

Currently, Lithium-ion batteries, including chemistries like LFP (Lithium Iron Phosphate) and NMC (Nickel Manganese Cobalt), are the most prevalent due to their superior energy density, cycle life, and power output. Lead-acid batteries still hold a share in certain cost-sensitive or less demanding applications, while solid-state batteries are an emerging technology with significant future potential.

What are the main challenges facing the heavy-duty battery market?

Key challenges include the high initial capital expenditure for battery systems, the limited availability and standardization of heavy-duty charging infrastructure, concerns regarding battery range and charging time for long-haul applications, and the volatility in the supply chain for critical raw materials such like lithium and cobalt.

How is AI impacting the development and operation of heavy-duty batteries?

AI is significantly impacting the market by enabling predictive maintenance for battery systems, optimizing charging and discharging cycles to extend battery lifespan, enhancing Battery Management Systems (BMS) for real-time performance monitoring, and accelerating the R&D of new battery chemistries through advanced simulation and design. It aims to make batteries more intelligent and efficient.

Which regions are expected to lead the heavy-duty battery market growth?

Asia Pacific is projected to be the largest and fastest-growing market due to rapid industrialization, supportive government policies, and extensive EV infrastructure investments, particularly in China and India. Europe and North America also show strong growth driven by ambitious decarbonization goals and the increasing adoption of electric commercial and industrial vehicles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted