Ground based Laser Designator Market

Ground based Laser Designator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700572 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

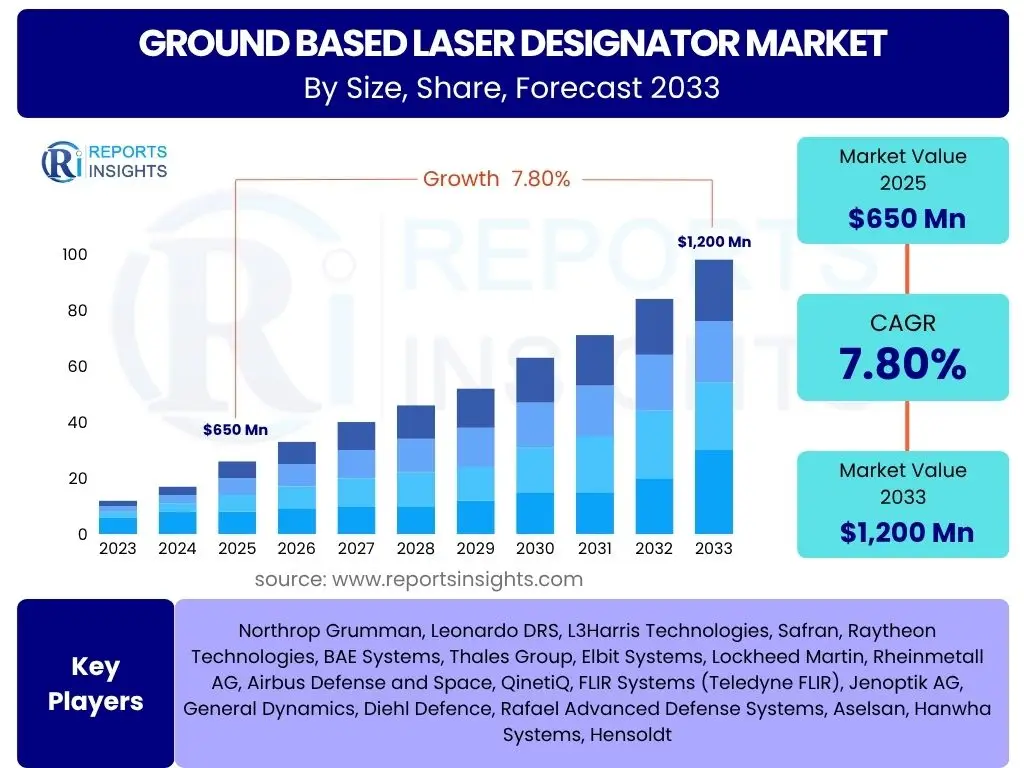

Ground based Laser Designator Market Size

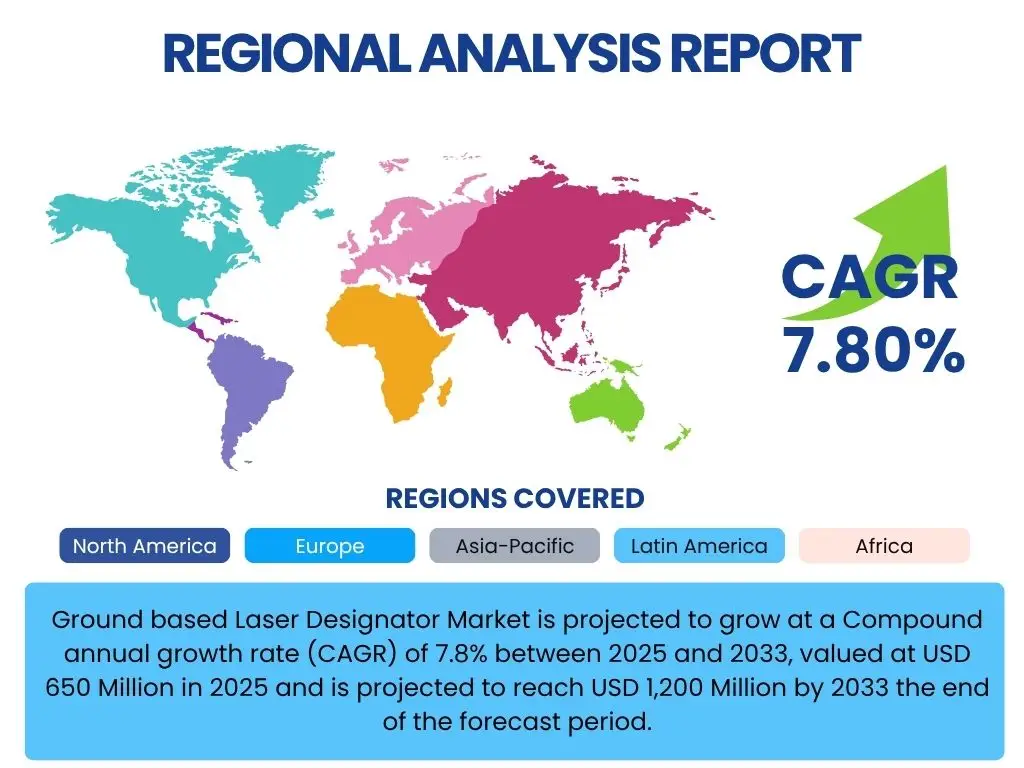

Ground based Laser Designator Market is projected to grow at a Compound annual growth rate (CAGR) of 7.8% between 2025 and 2033, valued at USD 650 Million in 2025 and is projected to reach USD 1,200 Million by 2033 the end of the forecast period.

Key Ground based Laser Designator Market Trends & Insights

The Ground based Laser Designator market is witnessing several transformative trends driven by evolving military doctrines, technological advancements, and the increasing demand for precision strike capabilities. Key trends include the miniaturization of designator systems, enabling greater portability and integration into diverse platforms, and the development of multi-functional designators that combine targeting, range-finding, and imaging capabilities. Furthermore, there is a growing emphasis on enhancing the accuracy and range of these systems, alongside improved resistance to environmental factors and jamming. The integration of advanced networking capabilities to facilitate seamless data exchange between ground forces, air assets, and command centers is also a significant trend, promoting synchronized operations and enhanced battlefield awareness.

- Miniaturization and portability advancements

- Integration of multi-functional capabilities

- Enhanced precision and extended range

- Improved environmental resilience

- Advanced networking and data fusion

AI Impact Analysis on Ground based Laser Designator

Artificial Intelligence (AI) is poised to revolutionize the Ground based Laser Designator market by significantly enhancing operational efficiency, decision-making, and autonomous capabilities. AI algorithms can optimize target recognition and tracking, allowing for faster and more accurate engagement by automatically distinguishing between friendly forces, civilians, and hostile targets, even in complex environments. Moreover, AI can predict optimal designation angles and power outputs based on real-time environmental conditions and target movement, minimizing human error and improving first-shot effectiveness. The integration of AI also facilitates advanced data analytics from sensor inputs, enabling predictive maintenance for designator systems and providing real-time intelligence for tactical planning, thereby ensuring higher system reliability and operational readiness. AI-driven systems can also learn from past engagements to refine targeting parameters, making future operations more precise and reducing collateral damage risks.

- Enhanced autonomous target recognition and tracking

- Optimized designation parameters in real-time

- Predictive maintenance for system reliability

- Real-time intelligence and tactical planning support

- Adaptive learning for improved precision

Key Takeaways Ground based Laser Designator Market Size & Forecast

- Market size projected to reach USD 1,200 Million by 2033.

- CAGR of 7.8% anticipated from 2025 to 2033.

- Growing demand for precision-guided munitions driving market expansion.

- Technological advancements in miniaturization and multi-functionality are key.

- AI integration is set to boost accuracy and operational efficiency.

- Increased geopolitical tensions stimulate military spending on modern targeting systems.

- North America and Asia Pacific expected to lead market growth.

- Emphasis on networked capabilities for enhanced battlefield synergy.

- Portable and vehicle-mounted systems are gaining prominence.

Ground based Laser Designator Market Drivers Analysis

The Ground based Laser Designator market is significantly propelled by several critical factors that underscore its growing importance in modern military operations. The global surge in demand for precision-guided munitions (PGMs) is a primary driver, as laser designators are indispensable for accurately guiding these weapons to their targets, thereby minimizing collateral damage and enhancing combat effectiveness. Furthermore, escalating geopolitical tensions and regional conflicts worldwide compel nations to modernize their defense capabilities, leading to increased procurement of advanced targeting systems. Technological advancements, particularly in making designators more compact, lighter, and capable of longer ranges and higher accuracy, also contribute significantly to market growth by expanding their utility across various operational scenarios. The increasing focus on networked warfare and interoperability among different military branches further fuels demand for designators that can seamlessly integrate into complex command and control structures, enabling synchronized operations and improved situational awareness on the battlefield.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for Precision-Guided Munitions | +2.1% | Global, particularly North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Increasing Geopolitical Tensions and Conflicts | +1.8% | Europe, Middle East, Asia Pacific | Medium to Long Term (2026-2033) |

| Military Modernization and Defense Spending Increases | +1.7% | Global, notably Asia Pacific, North America | Short to Medium Term (2025-2030) |

| Technological Advancements (Miniaturization, Range, Accuracy) | +1.5% | Global, driven by R&D hubs in North America, Europe | Long Term (2028-2033) |

| Growth in Network-Centric Warfare Adoption | +0.7% | North America, Europe, select Asian countries | Medium to Long Term (2027-2033) |

Ground based Laser Designator Market Restraints Analysis

Despite significant growth drivers, the Ground based Laser Designator market faces several formidable restraints that could impede its expansion. High acquisition and maintenance costs associated with advanced laser designator systems represent a major barrier, particularly for developing nations with limited defense budgets. These sophisticated systems require significant investment in research, development, and manufacturing, which translates into elevated procurement prices. Furthermore, stringent export control regulations and geopolitical restrictions on the sale of military-grade technologies can limit market access and hinder international trade for these sensitive devices. The operational complexity of laser designators, requiring extensive training for personnel and specialized technical support, also acts as a restraint, increasing the overall cost of ownership and deployment. Moreover, the risk of technological obsolescence due to rapid advancements in counter-measures, such as advanced jamming techniques or alternative targeting solutions, necessitates continuous investment in upgrades, posing a financial challenge for long-term strategic planning. Environmental factors, such as fog, smoke, and adverse weather conditions, can also limit the effective range and accuracy of laser designators, posing operational constraints.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Acquisition and Maintenance Costs | -1.9% | Global, particularly emerging economies | Short to Medium Term (2025-2029) |

| Stringent Export Control Regulations and Trade Barriers | -1.5% | Global, especially between certain political blocs | Medium to Long Term (2026-2033) |

| Complexity of Operation and Training Requirements | -1.0% | Global, affects military readiness | Short to Medium Term (2025-2030) |

| Vulnerability to Environmental Interference (e.g., fog, smoke) | -0.8% | Global, especially in challenging climates | Ongoing, Long Term (2025-2033) |

| Threat of Technological Obsolescence and Counter-Measures | -0.7% | Global, impacts R&D investment cycles | Medium to Long Term (2027-2033) |

Ground based Laser Designator Market Opportunities Analysis

The Ground based Laser Designator market presents several compelling opportunities for growth and innovation, driven by evolving military needs and technological advancements. One significant opportunity lies in the increasing demand for integrated defense systems, where laser designators can be seamlessly combined with other sensors, communication systems, and weapon platforms to create a cohesive and highly effective battlefield ecosystem. This integration enhances overall situational awareness and streamlines targeting processes. Furthermore, the burgeoning demand for unmanned aerial vehicles (UAVs) and autonomous ground vehicles (AGVs) creates a lucrative avenue for miniaturized and remote-operable laser designators, expanding their application beyond traditional manned operations. The development of dual-use technologies, allowing laser designators to serve both military and niche civilian applications such as surveying or scientific research, could also unlock new market segments and revenue streams. Strategic partnerships and collaborations between defense contractors and technology firms focusing on optics, photonics, and AI represent another critical opportunity to accelerate innovation and develop next-generation designator capabilities that are more precise, resilient, and cost-effective. Lastly, emerging markets, particularly in Asia Pacific and Latin America, are increasingly investing in modernizing their defense forces, offering significant untapped potential for market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Unmanned Systems (UAVs, UGVs) | +1.8% | Global, significant in North America, Asia Pacific | Medium to Long Term (2027-2033) |

| Development of Multi-role and Dual-use Designators | +1.5% | Global, driven by innovation hubs | Medium Term (2026-2030) |

| Expansion into Emerging Defense Markets | +1.2% | Asia Pacific, Latin America, parts of Africa | Long Term (2028-2033) |

| Strategic Partnerships and Technology Collaborations | +1.0% | North America, Europe, leading technology nations | Short to Medium Term (2025-2029) |

| Advancements in AI and Machine Learning Integration | +0.8% | Global, particularly advanced military powers | Medium to Long Term (2027-2033) |

Ground based Laser Designator Market Challenges Impact Analysis

The Ground based Laser Designator market encounters several significant challenges that necessitate strategic responses from manufacturers and defense stakeholders. One major challenge is the intense competition from alternative targeting technologies, such as GPS-guided systems or advanced optical sensors, which may offer different advantages or cost structures, potentially diverting investment away from laser designators. Furthermore, the ethical and legal implications surrounding the use of advanced targeting systems, particularly concerning civilian casualties and compliance with international humanitarian law, pose a challenge for widespread adoption and public acceptance. Supply chain disruptions, often exacerbated by geopolitical instability or global events, can significantly impact the availability of critical components and raw materials required for laser designator manufacturing, leading to production delays and increased costs. Counter-laser technologies, including sophisticated jamming devices and obscurants designed to disrupt laser designation, also present a persistent threat, compelling continuous research and development to maintain operational superiority. Lastly, the inherent technical complexity involved in developing and manufacturing high-precision laser systems, combined with the need for highly specialized expertise, presents a significant barrier to entry for new players and demands substantial ongoing investment from established market participants to remain competitive.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Alternative Targeting Technologies | -1.6% | Global, particularly in budget-constrained defense sectors | Medium to Long Term (2026-2033) |

| Ethical and Legal Scrutiny of Targeting Systems | -1.2% | Global, especially in Western nations and international bodies | Ongoing, Long Term (2025-2033) |

| Supply Chain Disruptions and Component Scarcity | -1.0% | Global, affects manufacturing hubs | Short to Medium Term (2025-2029) |

| Development of Advanced Counter-Laser Technologies | -0.9% | Global, impacts military readiness and R&D | Medium to Long Term (2027-2033) |

| High Technical Complexity and R&D Investment | -0.7% | Global, particularly for new entrants and innovators | Ongoing, Long Term (2025-2033) |

Ground based Laser Designator Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Ground based Laser Designator market, covering historical data, current market dynamics, and future projections. It offers strategic insights for businesses and decision-makers, highlighting key growth drivers, challenges, opportunities, and the impact of emerging technologies like AI. The report delves into market segmentation by type, application, and end-user, providing a granular view of market trends across various regions and countries. It also profiles leading market players, offering an understanding of their strategies and competitive landscape. This updated scope ensures a thorough examination of the market's trajectory and potential for innovation.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650 Million |

| Market Forecast in 2033 | USD 1,200 Million |

| Growth Rate | 7.8% from 2025 to 2033 |

| Number of Pages | 278 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Northrop Grumman, Leonardo DRS, L3Harris Technologies, Safran, Raytheon Technologies, BAE Systems, Thales Group, Elbit Systems, Lockheed Martin, Rheinmetall AG, Airbus Defense and Space, QinetiQ, FLIR Systems (Teledyne FLIR), Jenoptik AG, General Dynamics, Diehl Defence, Rafael Advanced Defense Systems, Aselsan, Hanwha Systems, Hensoldt |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ground based Laser Designator market is comprehensively segmented to provide a detailed understanding of its diverse facets, enabling precise market analysis and strategic decision-making. These segmentations allow for a granular examination of market dynamics, growth patterns, and technological preferences across different applications and end-user groups. Understanding these distinctions is crucial for manufacturers to tailor their product offerings, for defense organizations to optimize procurement, and for investors to identify high-potential areas within the market landscape.

-

By Type:

- Portable Laser Designators: These are compact, handheld, or man-portable systems designed for infantry and special forces, emphasizing lightweight construction and ease of deployment in varied terrains.

- Vehicle-Mounted Laser Designators: Integrated onto ground vehicles such as armored personnel carriers, tanks, or utility vehicles, these systems offer enhanced power, range, and stability, often linked to the vehicle's targeting systems.

- Fixed-Site Laser Designators: Employed in static positions like observation posts or command centers, these are larger, more powerful systems providing long-range, continuous designation capabilities for strategic assets or border surveillance.

-

By Wavelength:

- 1064 nm (Nd:YAG): This remains a predominant wavelength due to its high power output, effectiveness in various atmospheric conditions, and widespread compatibility with existing laser-guided munitions.

- 1550 nm: These designators offer significant advantages in terms of eye safety, making them suitable for training exercises and operations where human eye exposure is a concern, though often with slightly reduced range compared to 1064 nm.

- Other Wavelengths: This category includes emerging laser technologies and niche wavelengths developed for specific operational requirements, potentially offering unique advantages in terms of stealth, multi-spectral capabilities, or enhanced penetration through obscurants.

-

By Application:

- Target Designation: The primary application, involving the precise illumination of targets for laser-guided munitions, ensuring accuracy and minimizing collateral damage.

- Range Finding: Using laser pulses to accurately measure the distance to a target, crucial for ballistic calculations and engagement planning.

- Intelligence, Surveillance, and Reconnaissance (ISR): Employing laser systems for detailed observation, data collection, and identifying potential threats or targets, often integrated with advanced optics and thermal imagers.

- Battlefield Illumination: Providing covert illumination for night operations using infrared lasers, enhancing visibility for forces equipped with night vision devices without revealing their position.

- Target Tracking: Continuous monitoring of moving targets to maintain precise laser spot placement, critical for engaging dynamic threats effectively.

-

By End-User:

- Military & Defense: The largest end-user segment, encompassing armed forces, navies, and air forces requiring laser designators for various combat, training, and reconnaissance operations.

- Special Forces & Law Enforcement: Utilizing compact and highly specialized designators for covert operations, hostage rescue, counter-terrorism, and other specialized tactical scenarios.

- Homeland Security: Employing laser designators for border patrol, critical infrastructure protection, and surveillance activities, often integrated with broader security systems.

Regional Highlights

The global Ground based Laser Designator market exhibits distinct regional dynamics, influenced by defense budgets, geopolitical landscapes, technological advancements, and ongoing military modernization programs. Each region contributes uniquely to the market's overall growth, driven by specific strategic imperatives and procurement trends.- North America: This region stands as a dominant force in the Ground based Laser Designator market, primarily due to significant defense spending by the United States and Canada. The region benefits from a robust defense industrial base, continuous technological innovation, and a strong emphasis on developing and integrating advanced targeting systems. High investment in R&D, coupled with a focus on network-centric warfare and precision strike capabilities, ensures a steady demand for cutting-edge laser designators for both domestic use and export to allied nations. The presence of major market players and early adoption of AI integration further solidify its leading position.

- Europe: Europe represents a substantial market, driven by the modernization efforts of its armed forces and responses to evolving geopolitical threats, particularly in Eastern Europe. Countries like the United Kingdom, France, Germany, and Italy are heavily investing in upgrading their existing military equipment and acquiring new precision targeting systems. Collaborative defense initiatives and joint procurement programs within NATO and the European Union also contribute to market growth. There is a growing demand for compact, versatile, and interoperable laser designators that can be integrated into various European defense platforms and operational doctrines.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for Ground based Laser Designators. This growth is fueled by escalating defense budgets in countries like China, India, Japan, South Korea, and Australia, driven by regional territorial disputes and the modernization of their armed forces. The increasing adoption of advanced military technologies, coupled with a growing demand for precision-guided munitions, creates a significant market for laser designators. Countries in this region are actively seeking to enhance their strategic autonomy and combat capabilities, leading to substantial investments in advanced targeting solutions.

- Middle East and Africa (MEA): The MEA region is characterized by ongoing conflicts and heightened security concerns, which directly translate into increased military spending and a demand for advanced defense systems, including laser designators. Countries such as Saudi Arabia, UAE, and Israel are significant importers of defense technologies, seeking to enhance their precision strike capabilities and counter regional threats. While the market size may be smaller than other regions, the urgency of defense modernization drives consistent demand.

- Latin America: The Latin American market for Ground based Laser Designators is relatively smaller but shows steady growth. Countries in this region are focusing on modernizing their internal security forces and military capabilities, often driven by counter-insurgency operations, border security, and regional stability concerns. While budget constraints can be a factor, there is a gradual increase in the procurement of modern targeting equipment to enhance operational effectiveness.

Top Key Players:

The market research report covers the analysis of key stake holders of the Ground based Laser Designator Market. Some of the leading players profiled in the report include -- Northrop Grumman

- Leonardo DRS

- L3Harris Technologies

- Safran

- Raytheon Technologies

- BAE Systems

- Thales Group

- Elbit Systems

- Lockheed Martin

- Rheinmetall AG

- Airbus Defense and Space

- QinetiQ

- FLIR Systems (Teledyne FLIR)

- Jenoptik AG

- General Dynamics

- Diehl Defence

- Rafael Advanced Defense Systems

- Aselsan

- Hanwha Systems

- Hensoldt

Frequently Asked Questions:

What is a Ground based Laser Designator and how does it work?

A Ground based Laser Designator is a device used by ground forces to precisely mark a target with a laser beam for laser-guided munitions. It works by emitting a coded laser pulse that reflects off the target. This reflected energy is then detected by the seeker head of a laser-guided bomb, missile, or artillery shell, which then steers itself towards the designated spot, ensuring high accuracy in engagement.

What are the primary applications of Ground based Laser Designators?

The primary applications of Ground based Laser Designators include target designation for precision-guided munitions, accurate range finding for artillery and indirect fire, intelligence, surveillance, and reconnaissance (ISR) for detailed observation, battlefield illumination for covert night operations, and continuous target tracking for dynamic engagements. These applications are crucial for enhancing combat effectiveness and minimizing collateral damage.

What factors are driving the growth of the Ground based Laser Designator market?

The growth of the Ground based Laser Designator market is primarily driven by the increasing global demand for precision-guided munitions, rising geopolitical tensions and regional conflicts leading to military modernizations, and continuous technological advancements resulting in more compact, accurate, and multi-functional designator systems. The growing emphasis on network-centric warfare and interoperability also significantly contributes to market expansion.

How does AI impact the Ground based Laser Designator market?

AI significantly impacts the Ground based Laser Designator market by enabling more autonomous and precise operations. AI algorithms enhance target recognition and tracking, optimize designation parameters in real-time based on environmental conditions, facilitate predictive maintenance for system reliability, and improve real-time intelligence for tactical planning. This integration leads to higher accuracy, reduced human error, and improved operational efficiency.

What are the key challenges faced by the Ground based Laser Designator market?

Key challenges for the Ground based Laser Designator market include high acquisition and maintenance costs, stringent export control regulations, the inherent complexity of operation requiring extensive training, and vulnerability to environmental interferences like fog or smoke. Additionally, the development of advanced counter-laser technologies and competition from alternative targeting solutions pose significant hurdles for market growth and sustained innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted