Glass Packaging Market

Glass Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703789 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Glass Packaging Market Size

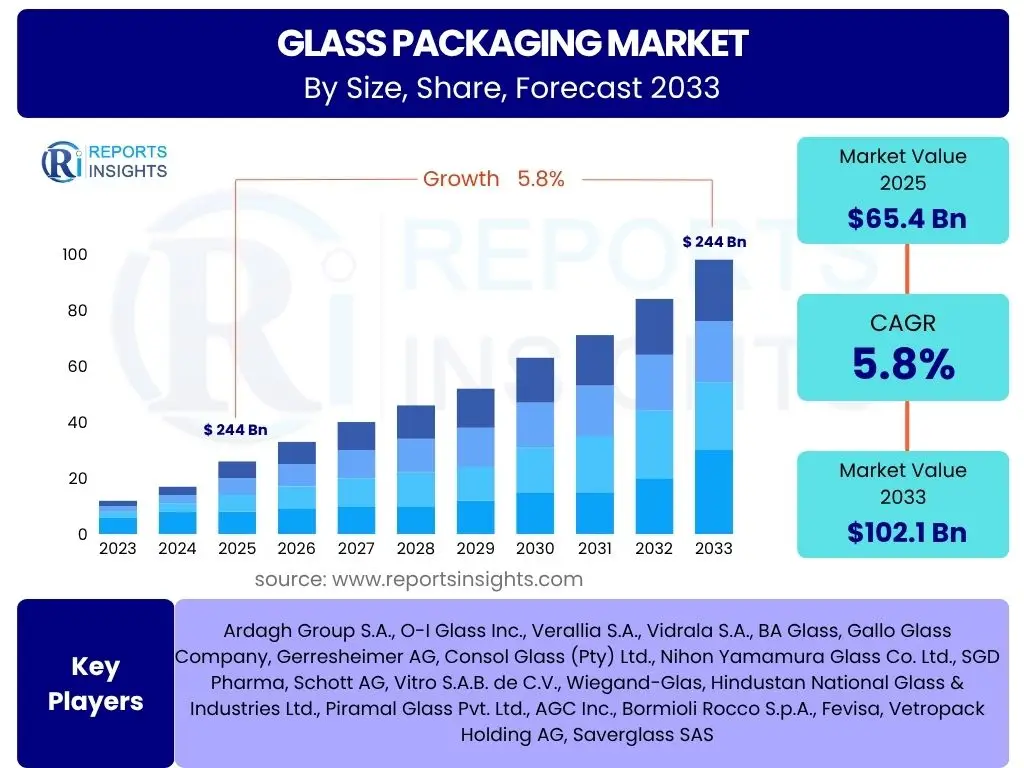

According to Reports Insights Consulting Pvt Ltd, The Glass Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 65.4 billion in 2025 and is projected to reach USD 102.1 billion by the end of the forecast period in 2033.

Key Glass Packaging Market Trends & Insights

The global glass packaging market is experiencing significant shifts driven by evolving consumer preferences and increasing sustainability mandates. A primary trend observed is the escalating demand for sustainable packaging solutions, with glass being inherently recyclable and reusable, making it a preferred choice over plastics. This is particularly evident in the food and beverage sectors, where brands are increasingly opting for glass to align with eco-conscious consumer values and regulatory pressures concerning plastic waste.

Furthermore, innovations in lightweighting technologies and design aesthetics are enhancing the appeal and functional versatility of glass packaging. Manufacturers are investing in research and development to produce lighter yet robust glass containers, reducing transportation costs and carbon footprint without compromising product integrity or premium perception. The market is also witnessing a surge in demand for smaller, single-serve glass packaging, catering to convenience-oriented lifestyles and portion control trends, especially in the beverage and pharmaceutical industries.

The premiumization trend across various consumer goods, including high-end spirits, gourmet foods, and luxury cosmetics, heavily favors glass packaging due to its inertness, barrier properties, and sophisticated appearance. This positions glass as a symbol of quality and purity, allowing brands to command higher prices. Concurrently, advancements in manufacturing processes, such as increased automation and digitalization, are improving production efficiency and cost-effectiveness, making glass a more competitive option against alternative packaging materials in certain applications.

- Growing emphasis on sustainability and recyclability.

- Increased adoption of lightweight glass technologies.

- Rising demand for premium and aesthetic packaging.

- Expansion of glass in pharmaceutical and cosmetic applications.

- Technological advancements in glass manufacturing processes.

- Shift towards smaller, convenient packaging formats.

- Enhanced focus on product safety and inertness.

AI Impact Analysis on Glass Packaging

The integration of Artificial Intelligence (AI) across the glass packaging value chain is poised to revolutionize traditional manufacturing processes, supply chain management, and quality control systems. Users are keenly interested in how AI can enhance operational efficiency, reduce waste, and improve product quality in an industry historically reliant on manual inspection and legacy equipment. AI-powered predictive maintenance, for instance, can anticipate equipment failures, minimizing downtime and optimizing production schedules, directly addressing concerns about manufacturing bottlenecks and costly repairs.

In quality assurance, AI vision systems offer unparalleled precision in detecting defects, far surpassing human capabilities and traditional optical methods. This leads to higher product consistency and reduced recall risks, a significant concern for brands prioritizing consumer safety and satisfaction. Moreover, AI algorithms can analyze vast datasets to optimize material usage, energy consumption, and even product design for optimal performance and sustainability. The ability of AI to model complex scenarios also allows for more accurate demand forecasting and inventory management, crucial for mitigating supply chain disruptions and enhancing responsiveness to market fluctuations.

Looking ahead, AI's role extends to enabling smarter, more connected packaging through integration with IoT devices, paving the way for innovations in traceability, anti-counterfeiting measures, and enhanced consumer engagement. While initial concerns may revolve around the capital investment required for AI implementation and the need for skilled labor, the long-term benefits in terms of cost savings, increased productivity, and competitive advantage are expected to drive widespread adoption. The industry is exploring AI to create a more resilient, efficient, and intelligent glass packaging ecosystem.

- Enhanced quality control through AI vision systems.

- Optimized production processes and predictive maintenance.

- Improved supply chain efficiency and demand forecasting.

- Reduced material waste and energy consumption.

- Development of smart and connected glass packaging.

- Advanced analytics for market trend identification.

- Automated defect detection and sorting systems.

Key Takeaways Glass Packaging Market Size & Forecast

The glass packaging market's trajectory towards substantial growth is underpinned by several critical factors, offering strategic insights for stakeholders. A primary takeaway is the inherent advantage of glass in meeting the escalating global demand for sustainable packaging solutions. Its infinitely recyclable nature and inert properties position it as a favorable alternative amidst increasing environmental scrutiny on plastic, suggesting a sustained competitive edge and market expansion, particularly within regulated markets and among environmentally conscious consumer bases.

Another significant insight derived from the market forecast is the pivotal role of innovation, especially in lightweighting and specialized coatings, in broadening glass packaging's applicability and appeal. These technological advancements address historical challenges related to weight and fragility, making glass a viable option for a wider range of products and distribution channels. This evolution is expected to unlock new market segments and applications, contributing significantly to the projected growth figures by enhancing efficiency and reducing the total cost of ownership for brands.

Furthermore, the market's resilience is evident in its adaptability to diverse end-use industries, including the robust pharmaceutical and premium beverage sectors, which consistently prioritize product integrity and brand image. The forecast indicates that these high-value applications will continue to be strong revenue drivers, cushioning the market against potential fluctuations in other segments. The strategic emphasis on regional manufacturing and localized supply chains, often influenced by geopolitical factors and trade policies, also emerges as a key takeaway, highlighting opportunities for localized investment and capacity expansion to serve specific market demands effectively.

- Glass packaging's inherent sustainability drives significant market growth.

- Technological advancements like lightweighting enhance market competitiveness.

- Strong demand from pharmaceutical and premium beverage sectors ensures stability.

- Increasing preference for inert and safe packaging materials.

- Emergence of customized and aesthetically appealing glass designs.

- Regional market dynamics heavily influence supply chain strategies.

- Digitalization and automation are improving manufacturing efficiency.

Glass Packaging Market Drivers Analysis

The global glass packaging market is primarily driven by an increasing consumer preference for sustainable and recyclable packaging materials. As environmental awareness grows and regulatory bodies worldwide impose stricter guidelines on plastic waste, brands are increasingly shifting towards glass, recognizing its infinite recyclability and lower environmental footprint. This shift is not merely compliance-driven but also a strategic move to align with consumer values, enhancing brand perception and market share for companies that prioritize eco-friendly solutions. The transparency and inertness of glass also appeal to consumers seeking purity and safety in their packaged goods.

Moreover, the robust growth in end-use industries such as food and beverage, pharmaceuticals, and cosmetics significantly propels the demand for glass packaging. In the food and beverage sector, glass is preferred for its ability to preserve taste, aroma, and freshness, crucial for premium products like wines, spirits, and specialty foods. The pharmaceutical industry relies on glass for its inertness, which prevents chemical interactions with sensitive drugs, ensuring product efficacy and safety. Similarly, in cosmetics, glass conveys a sense of luxury and quality, which aligns well with the premium branding strategies of many beauty product manufacturers. These sectors' expansion, fueled by rising disposable incomes and changing consumption patterns, directly translates to increased demand for glass packaging.

Technological advancements in glass manufacturing, including lightweighting techniques and improved production efficiencies, also act as significant drivers. Innovations that reduce the weight of glass containers without compromising strength lead to lower transportation costs and a reduced carbon footprint, making glass more competitive against alternative materials. Furthermore, advancements in decorative techniques and custom molding allow brands to create unique, eye-catching packaging that stands out on shelves, catering to the growing emphasis on product differentiation and aesthetic appeal in consumer markets. These advancements make glass a more versatile and economically attractive option for a wider range of applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Demand for Sustainable Packaging | +0.9% | Global, particularly Europe, North America, APAC | Long-term (2025-2033) |

| Growth in Food & Beverage Industry | +0.7% | Global, especially Asia Pacific, Latin America | Mid-term (2027-2030) |

| Expansion of Pharmaceutical Sector | +0.6% | North America, Europe, China, India | Long-term (2025-2033) |

| Premiumization and Brand Image | +0.5% | Europe, North America, Emerging Markets | Mid-term (2027-2030) |

| Technological Advancements (Lightweighting) | +0.4% | Global, particularly Developed Economies | Short-to-Mid-term (2025-2028) |

| Rising Disposable Income and Urbanization | +0.3% | Asia Pacific, Latin America, Middle East | Long-term (2025-2033) |

| Stringent Regulations on Plastic Use | +0.8% | Europe, North America, Specific Asian Countries | Mid-term (2026-2031) |

Glass Packaging Market Restraints Analysis

Despite its numerous advantages, the glass packaging market faces significant restraints, with the inherent fragility and weight of glass being primary concerns. The susceptibility of glass to breakage during transportation, handling, and storage leads to increased product losses and higher insurance costs for manufacturers and distributors. This fragility necessitates robust and often expensive secondary packaging, further adding to the overall supply chain costs. Moreover, the heavy weight of glass contributes to higher shipping expenses and a larger carbon footprint during transit, which can be a deterrent for companies looking to optimize logistics and reduce environmental impact associated with transportation.

Another substantial restraint is the relatively higher cost of glass packaging compared to alternative materials such as plastics and some metals. The energy-intensive manufacturing process of glass, coupled with the need for specialized equipment and skilled labor, contributes to elevated production costs. While glass offers long-term benefits in terms of recyclability and product integrity, the initial investment and per-unit cost can be prohibitive for certain product categories, particularly in price-sensitive markets. This cost disparity often compels brands to opt for more economical packaging solutions, especially for high-volume, low-margin consumer goods, thereby limiting the market penetration of glass.

Furthermore, intense competition from alternative packaging materials, including PET plastic, aluminum cans, and flexible packaging, poses a continuous challenge to the glass packaging market. These alternatives often offer advantages such as lighter weight, lower cost, greater durability, and sometimes more convenient design for specific applications. For instance, PET bottles are widely used in the beverage industry due to their shatter resistance and lower transportation costs. The ongoing innovation in these alternative materials, improving their sustainability profiles and functional performance, continually exerts pressure on the glass packaging industry to innovate and maintain its competitive edge, despite its established benefits.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Production and Transportation | -0.7% | Global, particularly Price-sensitive Markets | Long-term (2025-2033) |

| Fragility and Breakage Risk | -0.6% | Global, especially for Long-distance Shipping | Long-term (2025-2033) |

| Competition from Alternative Packaging Materials | -0.8% | Global, particularly for Mass Market Products | Long-term (2025-2033) |

| Energy-Intensive Manufacturing Process | -0.4% | Global, especially in regions with High Energy Costs | Mid-term (2027-2030) |

| Logistical Challenges Due to Weight | -0.3% | Global, particularly Remote Areas | Mid-term (2026-2031) |

| Limited Design Flexibility for Certain Applications | -0.2% | Specific Product Categories (e.g., highly portable) | Short-to-Mid-term (2025-2028) |

| Impact of Supply Chain Disruptions on Raw Materials | -0.5% | Global, particularly Europe and Asia | Short-term (2025-2026) |

Glass Packaging Market Opportunities Analysis

The burgeoning consumer demand for premium and aesthetically pleasing products presents a significant opportunity for the glass packaging market. Brands across the food, beverage, cosmetics, and spirits industries are increasingly leveraging packaging as a key differentiator to convey quality, purity, and exclusivity. Glass, with its superior clarity, elegant feel, and ability to be molded into intricate designs, inherently aligns with this premiumization trend. This allows manufacturers to command higher prices and strengthen brand identity, opening avenues for customized and high-value glass packaging solutions that cater to niche and luxury markets globally.

Furthermore, the growing focus on environmental sustainability and the circular economy models globally offer unparalleled opportunities for glass packaging. As governments and consumers increasingly prioritize recyclable and reusable packaging, glass stands out as an inherently circular material, capable of being recycled infinitely without loss of quality. This positions glass as a preferred choice over materials with limited recycling lifecycles or those contributing to plastic pollution. Innovations in recycled content utilization, closed-loop systems, and returnable glass bottle schemes present avenues for significant market expansion, aligning with global sustainability goals and consumer expectations for eco-friendly products.

Technological advancements, including lightweighting techniques, improved barrier coatings, and smart packaging integration, represent another robust area of opportunity. Lightweighting addresses the historical challenge of glass's weight, reducing transportation costs and carbon footprint, thereby making glass more competitive in broader applications. Advanced coatings can enhance glass's durability and provide UV protection, expanding its use for sensitive products. Moreover, the integration of smart technologies, such as QR codes or NFC tags, onto glass packaging allows for enhanced traceability, anti-counterfeiting measures, and interactive consumer engagement, unlocking new functionalities and value propositions in the evolving digital landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Premium Products | +0.8% | Global, particularly Developed and Emerging Markets | Long-term (2025-2033) |

| Increasing Focus on Circular Economy & Reusability | +0.9% | Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Technological Advancements in Lightweighting | +0.7% | Global, particularly Logistics-heavy Industries | Mid-term (2026-2031) |

| Expansion in Pharmaceutical and Healthcare Sectors | +0.6% | North America, Europe, Asia (China, India) | Long-term (2025-2033) |

| Shift to E-commerce and Direct-to-Consumer Models | +0.5% | Global, particularly Urban Centers | Mid-term (2027-2030) |

| Adoption of Smart Packaging Features | +0.4% | Developed Markets, Tech-forward Industries | Short-to-Mid-term (2025-2028) |

| Diversification into New End-Use Applications | +0.3% | Emerging Markets, Specialty Niches | Long-term (2028-2033) |

Glass Packaging Market Challenges Impact Analysis

The glass packaging market faces significant challenges related to the volatility of raw material prices and energy costs. The primary raw material for glass manufacturing, silica sand, along with other components like soda ash and limestone, can experience price fluctuations due to supply chain disruptions, geopolitical events, or changes in mining regulations. Furthermore, the glass production process is highly energy-intensive, relying heavily on natural gas and electricity. Therefore, spikes in energy prices directly translate to higher operational costs for glass manufacturers, which can erode profit margins and make glass a less competitive option compared to other packaging materials that have lower energy footprints. Managing these fluctuating input costs effectively is crucial for maintaining market stability and growth.

Another prominent challenge is the logistical complexity and environmental impact associated with the transportation of glass packaging. Due to its weight and fragility, glass requires more robust packaging and specialized handling during transit, leading to increased transportation costs and a larger carbon footprint per unit compared to lighter alternatives like plastic or aluminum. This poses a significant hurdle for companies aiming to reduce their overall environmental impact across their supply chain. Addressing these logistical inefficiencies and developing more sustainable transportation methods or localized manufacturing is vital for the long-term viability and attractiveness of glass packaging in a globalized market.

Moreover, intense competition from advanced alternative packaging materials, which are continually innovating to improve their sustainability and performance metrics, presents a persistent challenge. Plastics, metals, and flexible packaging solutions are becoming lighter, more durable, and increasingly recyclable, offering compelling cost and convenience advantages in various applications. For instance, the development of bio-based plastics or advanced composite materials offers new compromises between cost, weight, and environmental impact. The glass industry must continuously innovate in manufacturing efficiency, product design, and sustainability features to maintain its competitive edge against these rapidly evolving alternatives and prevent market erosion in segments where flexibility or weight is a critical factor.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Costs and Raw Material Price Volatility | -0.7% | Global, particularly Europe and Asia | Mid-to-Long-term (2026-2033) |

| Logistical Challenges and Carbon Footprint of Transportation | -0.6% | Global, especially for Export-oriented Businesses | Long-term (2025-2033) |

| Strong Competition from Advanced Alternative Materials | -0.8% | Global, particularly in Mass Market Segments | Long-term (2025-2033) |

| Need for High Capital Investment for New Facilities | -0.5% | Emerging Markets, Developing Economies | Long-term (2028-2033) |

| Managing Supply Chain Disruptions | -0.4% | Global, particularly for Niche Glass Products | Short-to-Mid-term (2025-2027) |

| Lack of Uniform Recycling Infrastructure in Some Regions | -0.3% | Developing Countries, Rural Areas | Long-term (2025-2033) |

| Perception of Fragility Among Consumers | -0.2% | Specific Product Categories (e.g., portable beverages) | Short-to-Mid-term (2025-2028) |

Glass Packaging Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global glass packaging market, providing an in-depth analysis of its size, trends, drivers, restraints, opportunities, and challenges. It offers a detailed forecast from 2025 to 2033, examining key segments by material type, product form, end-use application, and regional presence. The report further provides an exhaustive competitive landscape, profiling leading market players and their strategic initiatives, alongside an impact analysis of artificial intelligence on the industry. This study is designed to equip stakeholders with actionable insights for strategic decision-making and investment planning within the evolving glass packaging sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.4 billion |

| Market Forecast in 2033 | USD 102.1 billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 257 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Ardagh Group S.A., O-I Glass Inc., Verallia S.A., Vidrala S.A., BA Glass, Gallo Glass Company, Gerresheimer AG, Consol Glass (Pty) Ltd., Nihon Yamamura Glass Co. Ltd., SGD Pharma, Schott AG, Vitro S.A.B. de C.V., Wiegand-Glas, Hindustan National Glass & Industries Ltd., Piramal Glass Pvt. Ltd., AGC Inc., Bormioli Rocco S.p.A., Fevisa, Vetropack Holding AG, Saverglass SAS |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The glass packaging market is extensively segmented to provide a granular view of its diverse applications and material compositions, enabling a comprehensive understanding of market dynamics across various industries. These segmentations are crucial for identifying specific growth pockets, competitive landscapes, and consumer preferences within distinct categories. The primary layers of segmentation typically include material type, product form, and end-use industry, each broken down into further sub-segments that reflect the nuanced demands of the global market.

By delving into these detailed segments, market participants can pinpoint areas of high demand, emerging trends, and opportunities for product innovation. For instance, understanding the specific requirements of pharmaceutical glass (e.g., Type I borosilicate for injectables) versus beverage glass (e.g., soda-lime glass for bottles) allows manufacturers to tailor their production and marketing strategies. Similarly, analyzing the growth patterns within food packaging versus cosmetic packaging reveals different drivers and competitive intensities, guiding investment decisions and capacity expansion plans. This multi-layered segmentation ensures that the report captures the full complexity and diversity of the glass packaging ecosystem.

- By Material Type:

- Borosilicate Glass: Known for thermal shock resistance, ideal for pharmaceuticals.

- Soda-Lime Glass: Most common type, used for beverages, food, and general packaging.

- Lead Glass: Used in specialized applications, less common due to health concerns.

- Others: Includes specific glass formulations for niche uses.

- By Product Form:

- Bottles: Dominant segment for beverages, pharmaceuticals, cosmetics, and food liquids.

- Jars: Widely used for food products like jams, pickles, and sauces.

- Vials: Essential for pharmaceutical applications requiring small, sterile containers.

- Ampoules: Critical for single-dose pharmaceutical and cosmetic products.

- Containers: General purpose glass containers for various dry goods.

- Others: Specialty forms like carboys, laboratory glassware.

- By End-Use Industry:

- Food & Beverages: Largest segment, driven by alcoholic and non-alcoholic drinks, and packaged foods.

- Pharmaceuticals: High-growth segment due to sterile packaging requirements and drug stability.

- Cosmetics & Personal Care: Preferred for premium appeal and product preservation.

- Chemicals: Used for inert storage of industrial and household chemicals.

- Others: Includes applications in home care, lighting, and specialty industries.

Regional Highlights

The global glass packaging market exhibits distinct regional dynamics, influenced by varying regulatory landscapes, consumer preferences, economic development levels, and industrial infrastructure. North America is characterized by a strong demand for premium beverages and pharmaceuticals, alongside a growing emphasis on sustainable packaging, driving innovations in lightweighting and recycled content. The region's mature market often seeks value-added glass solutions that enhance brand appeal and meet stringent safety standards. Economic stability and high consumer purchasing power further bolster the market for high-quality glass packaging in this region.

Europe stands as a frontrunner in sustainable packaging initiatives, with robust regulations promoting recycling and circular economy principles. This has significantly accelerated the adoption of glass packaging across various sectors, particularly food, beverages, and pharmaceuticals. Countries like Germany, France, and Italy have well-established glass manufacturing infrastructures and high recycling rates, fostering continuous innovation in production efficiency and eco-friendly designs. The cultural preference for glass in traditional European beverages and gourmet foods also ensures sustained demand.

Asia Pacific is projected to be the fastest-growing region, propelled by rapid industrialization, increasing disposable incomes, and a burgeoning middle-class population. Countries like China and India are witnessing significant expansion in the food and beverage, pharmaceutical, and personal care industries, leading to a surge in demand for all types of packaging, including glass. While cost-effectiveness remains a key consideration, growing environmental awareness and the rising demand for premium products are gradually shifting preferences towards sustainable and higher-quality glass solutions across the region.

Latin America's glass packaging market is primarily driven by its large beverage industry, particularly beer and soft drinks, alongside a growing pharmaceutical sector. Economic recovery and expanding consumer markets are creating opportunities for both local and international glass manufacturers. However, infrastructure challenges and varying recycling capabilities across different countries can impact market development. The Middle East and Africa (MEA) region shows increasing potential, particularly with growing investments in the food and beverage industry and a rising tourism sector. The demand for glass packaging here is influenced by increasing urbanization, rising health consciousness, and the desire for premium goods, though market penetration varies significantly by country based on economic development and local manufacturing capabilities.

- North America: Strong demand from premium beverages and pharmaceuticals, focus on sustainability and lightweighting.

- Europe: Leading in circular economy initiatives, high recycling rates, established glass manufacturing, strong demand in food, beverage, and pharma.

- Asia Pacific (APAC): Fastest-growing region driven by urbanization, rising disposable incomes, and expanding food, beverage, and pharmaceutical industries, particularly China and India.

- Latin America: Significant growth in the beverage sector, increasing pharmaceutical demand, and developing local manufacturing capabilities.

- Middle East and Africa (MEA): Emerging market with growing demand from beverages, food, and increasing health consciousness, driven by urbanization and tourism.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Glass Packaging Market.- Ardagh Group S.A.

- O-I Glass Inc.

- Verallia S.A.

- Vidrala S.A.

- BA Glass

- Gallo Glass Company

- Gerresheimer AG

- Consol Glass (Pty) Ltd.

- Nihon Yamamura Glass Co. Ltd.

- SGD Pharma

- Schott AG

- Vitro S.A.B. de C.V.

- Wiegand-Glas

- Hindustan National Glass & Industries Ltd.

- Piramal Glass Pvt. Ltd.

- AGC Inc.

- Bormioli Rocco S.p.A.

- Fevisa

- Vetropack Holding AG

- Saverglass SAS

Frequently Asked Questions

What is the current market size and projected growth of the Glass Packaging Market?

The Glass Packaging Market is estimated at USD 65.4 billion in 2025 and is projected to reach USD 102.1 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 5.8% during the forecast period.

What are the primary drivers for the growth of the Glass Packaging Market?

Key drivers include the rising demand for sustainable and recyclable packaging, growth in the food and beverage and pharmaceutical industries, increasing consumer preference for premium products, and advancements in lightweight glass manufacturing technologies.

How does AI impact the Glass Packaging industry?

AI significantly impacts the glass packaging industry by enhancing quality control through vision systems, optimizing production processes, improving supply chain efficiency, enabling predictive maintenance, and contributing to the development of smart packaging solutions.

What are the main challenges facing the Glass Packaging Market?

Major challenges include the high cost of production due to energy intensity, the inherent fragility and weight of glass leading to higher transportation costs, and intense competition from lighter and cheaper alternative packaging materials like plastics and aluminum.

Which regions are key contributors to the Glass Packaging Market?

North America and Europe are significant contributors with established markets and strong sustainability focus, while Asia Pacific, particularly China and India, is emerging as the fastest-growing region due to rapid industrialization and increasing consumer demand.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted