PET Packaging Market

PET Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704140 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

PET Packaging Market Size

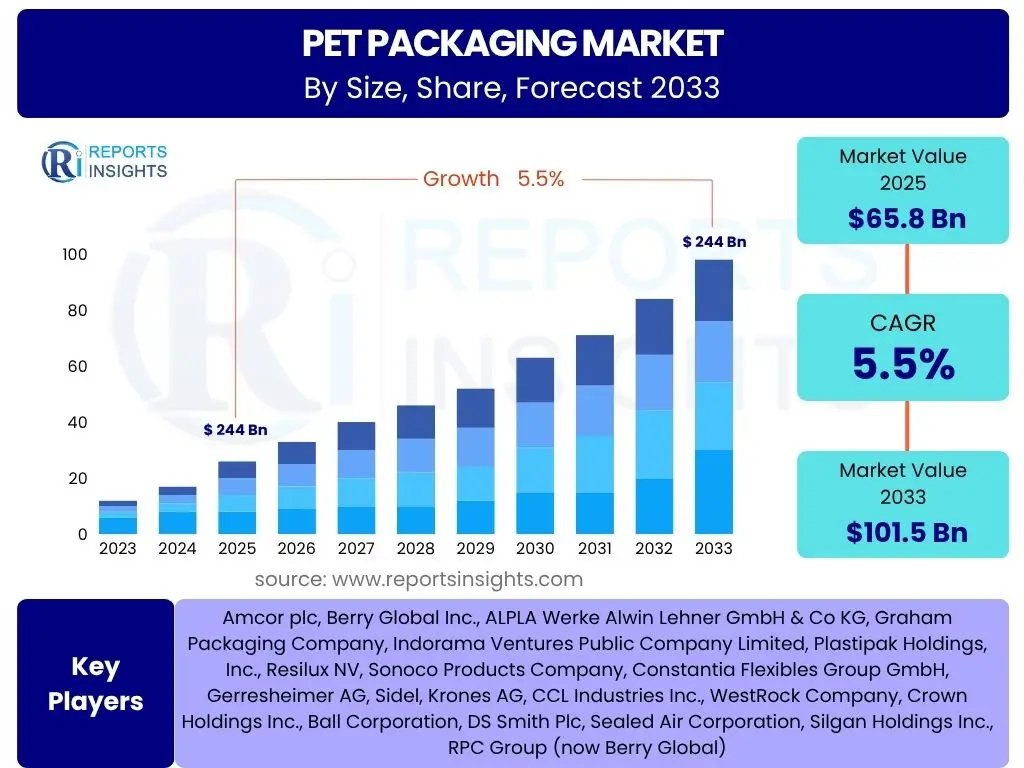

According to Reports Insights Consulting Pvt Ltd, The PET Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 65.8 Billion in 2025 and is projected to reach USD 101.5 Billion by the end of the forecast period in 2033.

Key PET Packaging Market Trends & Insights

The PET packaging market is currently shaped by several transformative trends driven by evolving consumer preferences, regulatory pressures, and technological advancements. A primary focus for users revolves around the integration of sustainable practices, particularly the adoption of recycled PET (rPET) and design for recyclability, as environmental consciousness becomes a paramount concern across industries. Furthermore, the expansion of e-commerce continues to drive demand for lightweight, durable, and secure packaging solutions that can withstand the rigors of shipping while minimizing material use. Innovations in barrier technologies are also gaining significant traction, enabling PET to expand its application into sensitive product categories that require extended shelf life and protection against oxygen, moisture, and UV light.

Users are also keenly interested in how aesthetic appeal and brand differentiation are influencing PET packaging design. There is a growing demand for customized shapes, colors, and textures that allow brands to stand out on crowded shelves and enhance consumer engagement. The shift towards smaller, single-serving portions in various product categories, particularly in beverages and food, contributes to the demand for compact and convenient PET solutions. Additionally, the increasing focus on supply chain efficiency and cost optimization is prompting manufacturers to explore lightweighting techniques without compromising structural integrity, which reduces transportation costs and carbon footprint. These trends collectively underscore a dynamic market where sustainability, functionality, and consumer appeal are key drivers of innovation and growth.

- Increased adoption of Recycled PET (rPET)

- Focus on lightweighting for cost and environmental benefits

- Growth in e-commerce driving demand for durable packaging

- Advancements in barrier technologies for extended shelf life

- Rising demand for customized and aesthetically appealing designs

- Shift towards smaller, convenient packaging formats

AI Impact Analysis on PET Packaging

The integration of Artificial Intelligence (AI) within the PET packaging industry is a subject of growing interest, with common user questions focusing on its potential to revolutionize operational efficiency, quality control, and sustainable practices. Users are eager to understand how AI algorithms can optimize manufacturing processes, from predictive maintenance of machinery to intelligent inventory management, thereby reducing downtime and material waste. There is also significant curiosity about AI's role in enhancing design and prototyping, allowing for faster iterations and simulations of new packaging forms and functionalities, which can lead to more innovative and consumer-centric products.

Furthermore, the impact of AI on supply chain visibility and optimization is a key concern, as businesses seek to improve logistics, reduce transportation costs, and minimize their carbon footprint through intelligent routing and demand forecasting. Users also inquire about AI's capacity for advanced quality inspection, where machine vision systems powered by AI can detect microscopic defects at high speeds, ensuring product integrity and reducing recalls. While concerns exist regarding potential job displacement in certain operational roles, the overarching expectation is that AI will empower a more agile, efficient, and sustainable PET packaging ecosystem by automating repetitive tasks, providing actionable insights, and enabling data-driven decision-making across the entire value chain.

- Enhanced predictive maintenance and operational efficiency in manufacturing.

- Optimized supply chain and logistics through intelligent demand forecasting.

- Improved quality control and defect detection via AI-powered vision systems.

- Accelerated R&D and design processes for new packaging solutions.

- Data-driven insights for sustainable material usage and waste reduction.

Key Takeaways PET Packaging Market Size & Forecast

An analysis of common user questions regarding the PET packaging market size and forecast reveals a strong emphasis on understanding the underlying growth drivers, the impact of sustainability, and the long-term viability of PET as a primary packaging material. Users frequently inquire about the segments exhibiting the most robust growth, such as the food and beverage sector, and how evolving consumer lifestyles are influencing demand patterns. The consistent growth trajectory projected for the market underscores the material's enduring appeal due to its versatility, lightweight properties, and cost-effectiveness compared to alternative packaging options. The market's expansion is intrinsically linked to rising disposable incomes in developing regions and the increasing urbanization leading to greater consumption of packaged goods.

A significant takeaway for users is the critical role of recycling infrastructure and technological advancements in recycled PET (rPET) in sustaining market growth amidst environmental scrutiny. The forecast indicates that investments in collection, sorting, and reprocessing technologies will be pivotal in meeting sustainability goals and regulatory mandates, thereby ensuring PET's continued market dominance. Furthermore, the market's resilience is bolstered by its continuous innovation in barrier technologies and customizability, allowing it to adapt to diverse product requirements and brand strategies. Overall, the market is poised for steady expansion, driven by a confluence of strong end-use demand, technological progress, and a concerted industry effort towards enhancing sustainability credentials, making it an attractive sector for strategic investments and partnerships.

- Robust and consistent market growth projected through 2033.

- Sustainability, particularly rPET adoption, is a key growth determinant.

- Food and beverage sector remains the largest end-use segment.

- Asia Pacific is a primary growth engine due to increasing consumption.

- Technological advancements in barrier properties and lightweighting enhance market appeal.

PET Packaging Market Drivers Analysis

The PET packaging market is primarily propelled by the burgeoning demand from the food and beverage industry, which relies heavily on PET for bottles, jars, and containers due to its transparency, barrier properties, and shatter resistance. The global shift towards packaged and convenience foods, coupled with rising disposable incomes in emerging economies, significantly contributes to this demand. Furthermore, the lightweight nature of PET reduces transportation costs and fuel consumption, appealing to both manufacturers seeking operational efficiencies and consumers looking for portable options.

Another significant driver is the increasing focus on sustainability and recycling initiatives worldwide. PET is one of the most widely recycled plastics, and advancements in recycling technologies, particularly for rPET, are enabling brands to meet their sustainability commitments and consumer demand for eco-friendlier packaging. The material's versatility also allows for innovative designs and enhanced shelf appeal, which are crucial for brand differentiation in competitive markets, further stimulating its adoption across various end-use sectors including pharmaceuticals, personal care, and household products.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from Food & Beverage industry | +1.2% | Global, particularly Asia Pacific & Latin America | Short to Long Term (2025-2033) |

| Increasing adoption in Pharmaceutical and Personal Care | +0.8% | North America, Europe, Emerging Markets | Medium to Long Term (2027-2033) |

| Advantages of lightweighting and cost-effectiveness | +0.9% | Global | Short to Medium Term (2025-2030) |

| Rising focus on sustainability and rPET integration | +1.0% | Europe, North America, parts of Asia Pacific | Medium to Long Term (2026-2033) |

PET Packaging Market Restraints Analysis

Despite its numerous advantages, the PET packaging market faces several significant restraints that could impede its growth trajectory. One primary concern is the fluctuating prices of raw materials, particularly crude oil and natural gas derivatives, which directly impact the cost of PET resin. These price volatilities can lead to unpredictable manufacturing costs, making it challenging for producers to maintain stable profit margins and potentially discouraging long-term investments in new production capacities. Such economic uncertainties compel companies to explore alternative materials or cost-saving measures, which can divert resources from PET innovations.

Furthermore, increasing environmental scrutiny and stringent regulatory frameworks regarding single-use plastics pose a considerable challenge. While PET is recyclable, concerns about plastic waste pollution, especially in marine environments, have led to bans or taxes on certain plastic products in various regions, and increased pressure for higher recycling rates. This public perception and legislative action can negatively impact consumer preference for PET, encouraging a shift towards other packaging materials like glass, metal, or paper, even in applications where PET offers superior performance. The competition from these alternative packaging materials, which are sometimes perceived as more sustainable, also acts as a restraint, forcing PET manufacturers to continuously innovate and highlight the material's environmental benefits and circular economy potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuating raw material prices (e.g., crude oil) | -0.7% | Global | Short to Medium Term (2025-2028) |

| Stringent environmental regulations and plastic bans | -0.8% | Europe, North America, parts of Asia | Medium to Long Term (2026-2033) |

| Competition from alternative packaging materials (glass, metal, paper) | -0.5% | Global | Medium Term (2027-2030) |

| Limitations in recycling infrastructure in some regions | -0.4% | Developing Economies | Long Term (2028-2033) |

PET Packaging Market Opportunities Analysis

The PET packaging market is presented with significant opportunities, largely driven by the continuous innovation in material science and processing technologies. The increasing demand for sustainable packaging solutions opens a vast avenue for advancements in recycled PET (rPET) technologies, including chemical recycling that can produce virgin-quality PET from waste. This not only addresses environmental concerns but also allows brands to meet ambitious sustainability targets and consumer expectations. Expanding the collection and recycling infrastructure globally, particularly in developing economies, represents a crucial opportunity to increase the supply of high-quality rPET and foster a truly circular economy for PET packaging, reducing reliance on virgin plastics.

Another promising opportunity lies in the burgeoning market for specialized and high-barrier PET packaging. As industries like pharmaceuticals, food, and beverages seek extended shelf life for sensitive products without compromising clarity or integrity, innovations in barrier coatings, multi-layer PET structures, and active packaging solutions offer substantial growth potential. Furthermore, the integration of smart packaging features, such as QR codes, NFC tags, or temperature sensors, can provide enhanced consumer engagement, supply chain traceability, and anti-counterfeiting measures. This digital transformation of packaging adds significant value beyond mere containment, opening new revenue streams and applications for PET, and appealing to a tech-savvy consumer base seeking convenience and transparency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Recycled PET (rPET) and chemical recycling | +1.0% | Global, particularly Europe & North America | Medium to Long Term (2026-2033) |

| Development of high-barrier PET for sensitive products | +0.8% | Global, particularly Pharmaceuticals & Food | Short to Medium Term (2025-2030) |

| Expansion into emerging markets with growing middle class | +0.9% | Asia Pacific, Latin America, MEA | Long Term (2027-2033) |

| Integration of smart packaging technologies (e.g., IoT) | +0.7% | North America, Europe, Developed Asia | Medium to Long Term (2027-2033) |

PET Packaging Market Challenges Impact Analysis

The PET packaging market faces several notable challenges that necessitate strategic responses from industry players. One significant hurdle is the persistent issue of inadequate waste management infrastructure in many parts of the world. While PET is highly recyclable, the lack of efficient collection, sorting, and reprocessing facilities, particularly in developing nations, means a substantial portion of PET waste ends up in landfills or the environment. This infrastructure deficit directly impacts the availability of high-quality recycled PET (rPET) feedstock, making it challenging for companies to meet ambitious recycled content targets and undermining the material's circular economy potential.

Another major challenge is the ongoing negative public perception surrounding plastics, which often fails to differentiate between various plastic types or acknowledge PET's recyclability. This broad-brush condemnation can lead to consumer backlash against PET products and influence purchasing decisions, despite the material's environmental benefits when properly recycled. Moreover, intense competition from alternative materials, often perceived as more environmentally friendly (such as glass, aluminum cans, or cardboard), continues to exert pressure on the PET market, requiring continuous innovation and clear communication about PET's life cycle advantages to retain market share. Addressing these challenges requires collaborative efforts across the value chain, from manufacturers and brands to consumers and policymakers, to improve recycling rates, educate the public, and foster a more sustainable narrative for PET packaging.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inadequate recycling infrastructure in various regions | -0.6% | Developing Economies (Asia, Africa, LatAm) | Long Term (2028-2033) |

| Negative public perception of plastics and sustainability concerns | -0.7% | Global, particularly Developed Markets | Short to Long Term (2025-2033) |

| High energy consumption during PET production processes | -0.3% | Global | Medium Term (2026-2030) |

| Ensuring food safety and compliance with evolving regulations | -0.2% | Global | Ongoing (2025-2033) |

PET Packaging Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global PET Packaging Market, offering a detailed understanding of its dynamics, trends, and future projections. The scope encompasses a thorough examination of market size estimations, historical data, and forecast period assessments, providing valuable insights into growth drivers, restraints, opportunities, and challenges influencing the industry. It segments the market by product type, end-use industry, and geography, offering granular insights into specific market performances and opportunities across diverse regions. Furthermore, the report identifies and profiles key market players, competitive landscape analysis, and strategic developments shaping the future of PET packaging, making it an essential resource for stakeholders seeking to navigate and capitalize on market opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.8 Billion |

| Market Forecast in 2033 | USD 101.5 Billion |

| Growth Rate | 5.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Graham Packaging Company, Indorama Ventures Public Company Limited, Plastipak Holdings, Inc., Resilux NV, Sonoco Products Company, Constantia Flexibles Group GmbH, Gerresheimer AG, Sidel, Krones AG, CCL Industries Inc., WestRock Company, Crown Holdings Inc., Ball Corporation, DS Smith Plc, Sealed Air Corporation, Silgan Holdings Inc., RPC Group (now Berry Global) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The PET packaging market is comprehensively segmented to provide granular insights into its diverse applications and market dynamics. This segmentation facilitates a deeper understanding of specific growth drivers and challenges within various product types, end-use industries, capacities, and aesthetic preferences. Analyzing these segments helps stakeholders identify lucrative niches, adapt product offerings, and tailor marketing strategies to specific consumer needs and industry requirements, thereby optimizing market penetration and competitive positioning. Each segment possesses unique characteristics and growth potentials, driven by consumer behavior, technological advancements, and regional economic factors, contributing to the overall market complexity and opportunities.

By dissecting the market along these lines, the report offers a strategic framework for businesses to assess their competitive advantages and explore untapped areas for expansion. For instance, the Food & Beverages segment, particularly beverages, consistently dominates due to high consumption rates and the material's suitability for liquid containment. The increasing demand for smaller, convenient packaging drives growth in lower capacity segments, while innovations in films and sheets cater to flexible packaging trends. Understanding these specific segment performances is crucial for forecasting future trends, allocating resources efficiently, and developing targeted solutions that resonate with particular market demands.

- By Type:

- Bottles & Jars: Dominant segment, widely used for beverages, food, pharmaceuticals.

- Films & Sheets: Growing segment for flexible packaging, thermoforming.

- Trays: Used for fresh produce, ready meals, and other food applications.

- Others: Includes containers, cups, and custom molded products.

- By End-use Industry:

- Food & Beverages: Largest and fastest-growing segment including water, carbonated soft drinks, juices, edible oils, and condiments.

- Pharmaceutical: Packaging for syrups, tablets, and medical devices, prioritizing safety and barrier properties.

- Personal Care & Cosmetics: Used for lotions, shampoos, and other beauty products due to aesthetic appeal and light weight.

- Household Care: Packaging for cleaning agents, detergents, and other home care products.

- Others: Industrial chemicals, automotive fluids, and various consumer goods.

- By Capacity:

- Up to 500 ml: Driven by single-serving and convenience formats.

- 501 ml to 1000 ml: Popular for everyday beverages and food items.

- 1001 ml to 2000 ml: Standard for family-size beverages and bulk food.

- Above 2000 ml: Used for large volume applications and bulk industrial products.

- By Color:

- Transparent: Preferred for visibility and aesthetic appeal, especially in beverages.

- Opaque: Used for light-sensitive products or brand differentiation.

- Others: Includes custom colored or tinted PET for specific branding needs.

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing regional market, driven by increasing disposable incomes, rapid urbanization, and a burgeoning middle class in countries like China, India, and Southeast Asian nations. High demand from the food and beverage industry, coupled with expanding pharmaceutical and personal care sectors, fuels significant growth. Investments in manufacturing capabilities and a rising consumer base contribute to its dominance.

- North America: A mature market characterized by innovation in sustainable PET solutions, including a strong emphasis on rPET adoption and lightweighting technologies. Consumer preference for convenient and healthy packaged foods, alongside stringent recycling mandates, shapes market dynamics. The region sees steady demand from established end-use industries and a focus on circular economy initiatives.

- Europe: This region is at the forefront of sustainability, with robust regulatory frameworks promoting circularity and high recycling targets for PET. Innovation in barrier technologies and bio-based PET is prominent. While growth rates may be lower than in APAC, the market is characterized by high value-added products, advanced recycling infrastructure, and a strong push towards reducing virgin plastic consumption.

- Latin America: Experiencing substantial growth fueled by increasing consumer spending, urbanization, and the expansion of the organized retail sector. Countries like Brazil and Mexico are key contributors, driven by demand for bottled beverages and packaged food products. The region presents significant opportunities for market penetration and investment, though challenges in recycling infrastructure remain.

- Middle East and Africa (MEA): An emerging market with considerable potential, driven by population growth, economic diversification, and increasing consumption of packaged goods, particularly in the UAE, Saudi Arabia, and South Africa. Investments in infrastructure and manufacturing are supporting market expansion, with a growing awareness of sustainability leading to the gradual adoption of more eco-friendly PET solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the PET Packaging Market.- Amcor plc

- Berry Global Inc.

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Graham Packaging Company

- Indorama Ventures Public Company Limited

- Plastipak Holdings, Inc.

- Resilux NV

- Sonoco Products Company

- Constantia Flexibles Group GmbH

- Gerresheimer AG

- Sidel

- Krones AG

- CCL Industries Inc.

- WestRock Company

- Crown Holdings Inc.

- Ball Corporation

- DS Smith Plc

- Sealed Air Corporation

- Silgan Holdings Inc.

- RPC Group (now Berry Global)

Frequently Asked Questions

What is PET packaging and why is it widely used?

PET (Polyethylene Terephthalate) packaging refers to containers and films made from a lightweight, strong, and transparent plastic polymer. It is widely used due to its excellent barrier properties against gas and moisture, shatter resistance, cost-effectiveness, and high recyclability, making it ideal for beverages, food, pharmaceuticals, and personal care products.

How sustainable is PET packaging, and what is rPET?

PET is considered one of the most sustainable plastics due to its high recyclability, often recycled back into new bottles or other products. rPET, or recycled PET, is PET material derived from post-consumer waste, significantly reducing the demand for virgin plastic, energy consumption, and greenhouse gas emissions, thereby enhancing its environmental profile.

What are the primary drivers of growth in the PET packaging market?

Key growth drivers include the increasing demand from the food and beverage industry, particularly for bottled water and soft drinks, rising consumer preference for lightweight and convenient packaging, growing awareness and adoption of recycled content (rPET), and expansion into emerging markets with increasing disposable incomes and urbanization.

What are the main challenges facing the PET packaging industry?

The industry faces challenges such as fluctuating raw material prices, persistent negative public perception of plastics despite PET's recyclability, and the need for improved waste collection and recycling infrastructure globally. Competition from alternative packaging materials also presents a continuous challenge.

How is technology impacting the future of PET packaging?

Technological advancements are driving innovations in PET packaging, including enhanced barrier properties for extended shelf life, lightweighting to reduce material usage and transport costs, and the integration of smart packaging features like QR codes for traceability and consumer engagement. AI and automation are also optimizing production and quality control processes, fostering greater efficiency and sustainability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted