Generation IV reactor Market

Generation IV reactor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710300 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

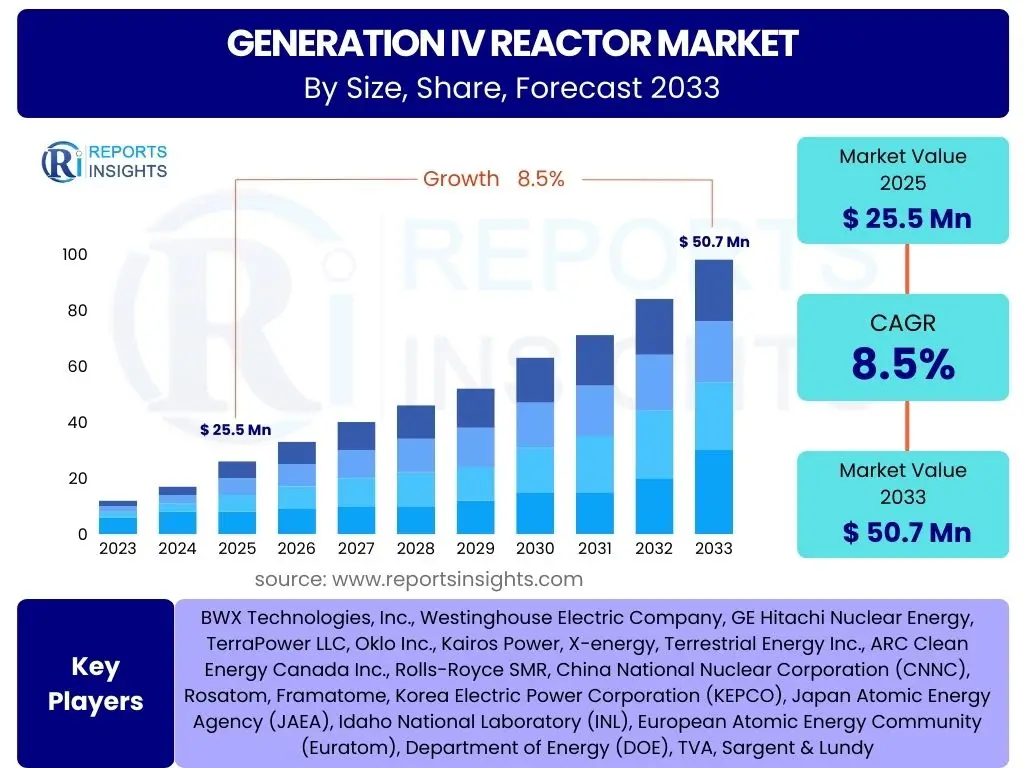

Generation IV reactor Market Size

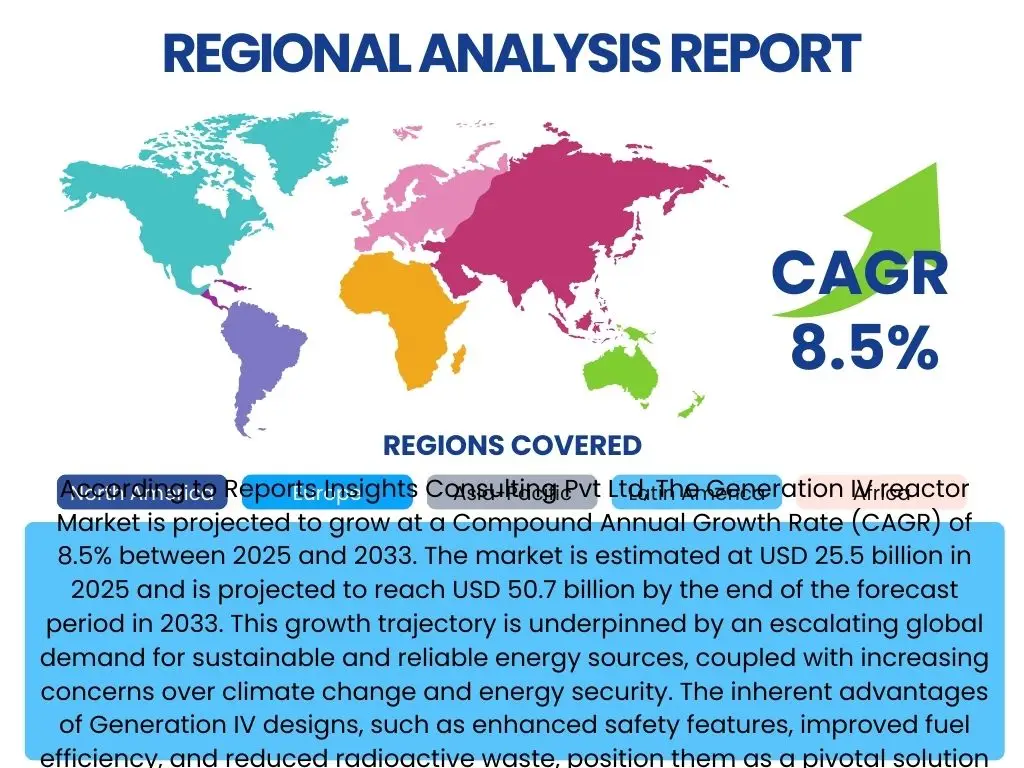

According to Reports Insights Consulting Pvt Ltd, The Generation IV reactor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 25.5 billion in 2025 and is projected to reach USD 50.7 billion by the end of the forecast period in 2033. This growth trajectory is underpinned by an escalating global demand for sustainable and reliable energy sources, coupled with increasing concerns over climate change and energy security. The inherent advantages of Generation IV designs, such as enhanced safety features, improved fuel efficiency, and reduced radioactive waste, position them as a pivotal solution in the future energy landscape.

The substantial market expansion is further driven by significant governmental and private investments in nuclear research and development, particularly in advanced reactor technologies. Regulatory bodies are also adapting frameworks to accommodate these innovative designs, paving the way for their commercial deployment. As existing nuclear fleets age and the push for decarbonization intensifies, Generation IV reactors are poised to capture a significant share of the global energy market, offering a long-term, low-carbon power generation alternative that addresses both environmental and economic imperatives.

Key Generation IV reactor Market Trends & Insights

User queries regarding Generation IV reactor market trends frequently center on their potential to revolutionize nuclear energy, focusing on aspects like enhanced safety, economic viability, waste management, and the integration of these technologies into existing energy grids. The prevailing sentiment indicates strong interest in how these advanced designs will address the historical challenges associated with nuclear power, particularly concerning public perception and regulatory approval. There is also significant curiosity about the leading reactor types and the regions spearheading their development and deployment.

The market is witnessing several transformative trends. Firstly, there is a distinct shift towards designs that offer improved passive safety features, minimizing the risk of accidents and enhancing public confidence. Secondly, economic competitiveness is a major driver, with developers focusing on designs that promise lower operational costs, higher efficiency, and scalability, including smaller modular units. Thirdly, the push for more sustainable fuel cycles, including the ability to utilize spent nuclear fuel, is gaining traction to reduce long-lived radioactive waste. Lastly, international collaboration and standardization efforts are accelerating, aiming to streamline regulatory processes and facilitate global deployment.

- Emphasis on enhanced passive and inherent safety features to mitigate operational risks.

- Development of more efficient fuel cycles, including capabilities for waste reduction and resource utilization.

- Growing interest in Small Modular Reactors (SMRs) based on Gen IV designs for scalability and flexible deployment.

- Increased government funding and private investment in advanced nuclear research and demonstration projects.

- Strategic international collaborations aimed at standardizing designs and accelerating commercialization.

- Focus on economic competitiveness through lower construction and operational costs per unit of energy.

- Integration of advanced manufacturing techniques and digital technologies in reactor design and construction.

- Exploration of non-electricity generation applications, such as industrial heat, hydrogen production, and desalination.

AI Impact Analysis on Generation IV reactor

Common user questions regarding AI's impact on Generation IV reactors largely revolve around its potential to enhance safety, optimize operational efficiency, accelerate design and development, and strengthen cybersecurity. Users are keen to understand how artificial intelligence can make these complex systems more reliable, reduce human error, and provide predictive capabilities that were previously unattainable. There is also a notable interest in AI's role in processing vast amounts of sensor data for real-time diagnostics and its application in advanced materials research for reactor components.

AI is emerging as a transformative force in the development and operation of Generation IV reactors, offering unparalleled capabilities for optimization and safety. Its application spans across various stages, from initial design and simulation to construction, operation, and maintenance. By leveraging machine learning algorithms, AI can analyze complex data sets to predict component failure, optimize fuel management strategies, and detect anomalies before they escalate into critical issues. This not only enhances the safety profile of these reactors but also contributes significantly to their economic viability by reducing downtime and operational costs. Furthermore, AI-driven simulations can accelerate the design process, allowing for rapid iteration and optimization of reactor characteristics, leading to more robust and efficient designs.

- Accelerated Design and Simulation: AI algorithms significantly reduce the time required for complex reactor design optimizations and safety simulations, enabling faster development cycles.

- Enhanced Operational Efficiency: Predictive analytics and machine learning optimize fuel loading, power output, and system parameters, leading to higher capacity factors and lower operational costs.

- Advanced Safety Monitoring: AI-powered sensor networks provide real-time anomaly detection and predictive maintenance, drastically reducing the risk of failures and improving overall plant safety.

- Robotics and Automation: AI-controlled robotics can perform routine inspections and maintenance in hazardous environments, minimizing human exposure and increasing operational reliability.

- Cybersecurity Fortification: AI-driven threat detection systems strengthen the cybersecurity posture of control systems, protecting against potential digital attacks.

- Fuel Cycle Optimization: AI can model and optimize advanced fuel cycles, improving resource utilization and reducing the volume and radiotoxicity of nuclear waste.

- Material Science Advancements: AI accelerates the discovery and testing of novel materials resistant to extreme conditions, critical for next-generation reactor components.

- Training and Knowledge Transfer: AI-based intelligent tutoring systems can aid in training the specialized workforce required for operating and maintaining Generation IV reactors.

Key Takeaways Generation IV reactor Market Size & Forecast

User inquiries about key takeaways from the Generation IV reactor market size and forecast consistently highlight the desire for a concise understanding of the market's growth potential, the primary factors driving this growth, and the most significant challenges that need to be overcome. There is a strong focus on identifying the compelling reasons for investing in or developing these technologies, as well as understanding the long-term implications for global energy security and environmental sustainability. The summary must distill the complex market dynamics into actionable insights for stakeholders.

The Generation IV reactor market is on a robust upward trajectory, projected to more than double in value by 2033, driven by an urgent global need for clean, reliable, and sustainable energy solutions. This growth is primarily fueled by the inherent benefits of these advanced designs, including superior safety, enhanced fuel efficiency, and a drastic reduction in nuclear waste, aligning perfectly with global decarbonization goals. While significant capital investment and regulatory harmonization remain critical hurdles, the long-term energy security benefits and environmental advantages are creating an undeniable imperative for their adoption. Stakeholders should recognize the substantial long-term investment opportunities and the pivotal role these reactors will play in shaping the future energy landscape.

- The market is poised for significant expansion, with a projected CAGR of 8.5% through 2033, indicating strong investor confidence and technological maturity.

- Decarbonization efforts and the global imperative to combat climate change are primary drivers, positioning Generation IV reactors as a cornerstone of future clean energy grids.

- Technological advancements in safety, fuel efficiency, and waste reduction are key differentiators, making these reactors more publicly acceptable and economically viable.

- Strategic government support, R&D funding, and international collaborations are crucial accelerators for commercialization and deployment.

- While high upfront costs and complex regulatory frameworks present challenges, the long-term benefits in energy security, sustainability, and waste management outweigh these initial hurdles.

- The synergy with Small Modular Reactors (SMRs) is a significant opportunity, enabling flexible deployment and potentially reducing capital expenditure barriers.

Generation IV reactor Market Drivers Analysis

The global energy landscape is undergoing a profound transformation, characterized by an urgent need for decarbonization and enhanced energy security. Generation IV reactors are uniquely positioned to address these challenges, offering a low-carbon, highly efficient, and reliable power source that is not dependent on intermittent renewable energy fluctuations. Governments worldwide are increasingly recognizing the strategic importance of nuclear power in their energy portfolios, leading to a resurgence of interest and support for advanced reactor designs. This political and environmental impetus is a primary driver for market growth.

Furthermore, the inherent design improvements of Generation IV reactors, such as enhanced safety features, more efficient fuel utilization, and the ability to reduce or even consume nuclear waste, directly address many of the historical concerns associated with conventional nuclear power. These technological advancements not only improve public perception but also offer compelling economic advantages through extended operational lifetimes and reduced fuel costs. The potential for these reactors to provide high-temperature process heat for industrial applications and hydrogen production also expands their market utility beyond mere electricity generation, creating new avenues for growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization and Climate Change Goals | +2.5% | Global, particularly Europe, North America, Asia Pacific | Medium to Long-term (2025-2033) |

| Enhanced Energy Security and Independence | +2.0% | Europe, North America, East Asia | Medium to Long-term (2025-2033) |

| Improved Safety Features and Public Acceptance | +1.5% | Global, especially Western Europe, North America | Medium to Long-term (2025-2033) |

| Increased Fuel Efficiency and Waste Reduction Capabilities | +1.0% | Global | Long-term (2028-2033) |

| Governmental Support and R&D Funding for Advanced Nuclear | +1.5% | USA, Canada, China, Russia, UK, France | Short to Medium-term (2025-2029) |

Generation IV reactor Market Restraints Analysis

Despite the promising outlook, the Generation IV reactor market faces several significant restraints that could temper its growth trajectory. The most prominent among these is the exceptionally high upfront capital expenditure required for the research, development, and construction of these advanced nuclear facilities. Unlike conventional energy projects, Generation IV reactors demand substantial, long-term investments, which can deter potential private investors and pose challenges for public funding, especially in economies with tighter fiscal policies. This financial barrier prolongs the development timeline and increases the risk profile of projects.

Another critical restraint involves the complex and often protracted regulatory approval processes. Nuclear safety regulations are inherently stringent, and the novel designs of Generation IV reactors require extensive review, testing, and validation by regulatory bodies. This can lead to lengthy licensing periods, cost overruns, and uncertainty for developers. Furthermore, public perception, although improving due to enhanced safety features, still presents a challenge in some regions, with lingering concerns about nuclear waste disposal and the risks associated with proliferation. The need for a highly specialized workforce and the development of a robust supply chain capable of handling unique materials and components also pose significant hurdles.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Costs and Investment Risks | -1.8% | Global | Short to Medium-term (2025-2030) |

| Complex and Protracted Regulatory Approval Processes | -1.5% | North America, Europe | Medium to Long-term (2025-2033) |

| Public Perception and Lingering Safety Concerns | -1.0% | Western Europe, North America, Japan | Medium-term (2025-2030) |

| Long Development and Construction Timelines | -1.2% | Global | Medium to Long-term (2025-2033) |

| Skilled Workforce Shortage and Supply Chain Limitations | -0.8% | Global, especially developed economies | Short to Medium-term (2025-2029) |

Generation IV reactor Market Opportunities Analysis

The Generation IV reactor market is rich with opportunities, particularly in addressing the evolving global energy mix and technological advancements. One significant area of opportunity lies in the replacement of aging conventional power infrastructure, including older nuclear plants and fossil fuel facilities, with new, more efficient, and sustainable Generation IV designs. The inherent flexibility of some Generation IV concepts, particularly Small Modular Reactors (SMRs), allows for their deployment in various locations, including remote communities and industrial sites, opening up new market segments that were previously inaccessible to large-scale nuclear power.

Moreover, the advanced capabilities of Generation IV reactors extend beyond electricity generation. Their ability to produce high-temperature process heat positions them as a key solution for energy-intensive industries such as hydrogen production, chemical manufacturing, and desalination. This diversification of application significantly broadens the market potential and economic viability of these technologies. Furthermore, ongoing innovation in advanced fuel cycles, including thorium utilization and the reprocessing of spent nuclear fuel, presents an opportunity to create a more closed and sustainable nuclear fuel economy, minimizing waste and enhancing resource security, which could garner greater public and political support.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Renewable Energy Grids for Stability | +1.8% | Europe, North America, Asia Pacific | Medium to Long-term (2026-2033) |

| Emerging Economies' Growing Energy Demand | +2.0% | Asia Pacific (China, India), Africa, Latin America | Medium to Long-term (2027-2033) |

| Synergy with Small Modular Reactor (SMR) Development | +2.2% | Global | Short to Medium-term (2025-2030) |

| Expansion into Industrial Heat and Hydrogen Production | +1.5% | Global, especially industrial hubs | Medium to Long-term (2028-2033) |

| Advanced Fuel Cycles and Waste Minimization | +1.0% | Global | Long-term (2030-2033) |

Generation IV reactor Market Challenges Impact Analysis

The Generation IV reactor market faces several formidable challenges that require innovative solutions and concerted efforts from stakeholders. One primary challenge is securing the substantial and long-term financial investment necessary for both the initial research and development phases and the eventual commercial deployment. The novelty and complexity of these technologies often translate into higher perceived risks for investors, making it difficult to attract capital at competitive rates. This financial hurdle is compounded by the extended timelines typical for nuclear projects, pushing returns further into the future.

Another significant challenge lies in the development of a robust and specialized supply chain capable of producing the unique materials and components required for Generation IV designs. Many of these reactors utilize advanced materials and manufacturing techniques that are not yet widely commercialized or readily available, leading to potential bottlenecks and increased costs. Additionally, the industry grapples with the global shortage of a highly skilled workforce, including nuclear engineers, scientists, and specialized technicians, essential for the design, construction, operation, and maintenance of these sophisticated systems. Overcoming these technical and human capital challenges will be crucial for the successful maturation and broad deployment of Generation IV reactor technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Attracting and Securing Long-term Investment Capital | -1.7% | Global | Short to Medium-term (2025-2030) |

| Technological Complexity and Novelty Risks | -1.3% | Global, particularly pioneering nations | Short to Medium-term (2025-2029) |

| Development of Specialized Supply Chains | -1.0% | Global | Medium-term (2026-2031) |

| Management and Disposal of Advanced Nuclear Waste | -0.9% | Global | Long-term (2030-2033) |

| Skilled Workforce Shortage and Knowledge Transfer | -0.7% | Developed economies | Short to Medium-term (2025-2029) |

Generation IV reactor Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Generation IV reactor market, providing critical insights into its current size, historical performance, and future growth projections up to 2033. The scope encompasses detailed segmentation by reactor type, coolant, fuel, application, and geographical regions, offering a granular view of market dynamics. It further delves into the key drivers, restraints, opportunities, and challenges shaping the industry, alongside a meticulous examination of the competitive landscape, profiling leading market players to provide a holistic understanding for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 billion |

| Market Forecast in 2033 | USD 50.7 billion |

| Growth Rate | 8.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BWX Technologies, Inc., Westinghouse Electric Company, GE Hitachi Nuclear Energy, TerraPower LLC, Oklo Inc., Kairos Power, X-energy, Terrestrial Energy Inc., ARC Clean Energy Canada Inc., Rolls-Royce SMR, China National Nuclear Corporation (CNNC), Rosatom, Framatome, Korea Electric Power Corporation (KEPCO), Japan Atomic Energy Agency (JAEA), Idaho National Laboratory (INL), European Atomic Energy Community (Euratom), Department of Energy (DOE), TVA, Sargent & Lundy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Generation IV reactor market is comprehensively segmented to provide a detailed understanding of its diverse components and growth opportunities. This segmentation considers various technological approaches and applications that define the landscape of advanced nuclear power. Each segment represents distinct design philosophies or operational capabilities, catering to specific energy needs and regulatory environments globally. Understanding these segments is crucial for identifying key areas of innovation, investment, and market penetration, allowing stakeholders to strategically position themselves within this evolving industry.

The market's intricate structure, comprising different reactor types, coolants, fuel cycles, and applications, reflects the broad scope of Generation IV technologies. For instance, some reactors prioritize waste reduction, while others focus on high-temperature heat for industrial processes. This granular breakdown helps in assessing the competitive intensity, technological maturity, and regional adoption patterns across various advanced nuclear solutions. The analysis of these segments highlights the versatility of Generation IV reactors in addressing multifaceted energy challenges, from clean electricity generation to industrial decarbonization.

- By Reactor Type: This segment includes Sodium-cooled Fast Reactors (SFR), Lead-cooled Fast Reactors (LFR), Gas-cooled Fast Reactors (GFR), Very-high-temperature Reactors (VHTR), Molten Salt Reactors (MSR), and Supercritical Water Reactors (SCWR), each with unique characteristics and development stages.

- By Coolant Type: Categorization based on the primary coolant used, such as Liquid Metal (Sodium, Lead), Gas (Helium), Molten Salt, and Supercritical Water, influencing reactor design and operational parameters.

- By Fuel Type: Segmentation by the type of nuclear fuel utilized, including Uranium-Plutonium (MOX), Thorium, and capabilities for Spent Fuel Reprocessing, indicating different fuel cycle strategies.

- By Application: This covers the primary end-use sectors, including Electricity Generation, Industrial Heat supply, Hydrogen Production, Desalination, and Other niche applications.

- By Region: Geographic segmentation across North America, Europe, Asia Pacific (APAC), Latin America, and Middle East & Africa (MEA) provides insight into regional market dynamics and adoption rates.

Regional Highlights

- North America: The United States and Canada are prominent leaders in Generation IV reactor research and development, driven by strong government support, private sector innovation, and a robust regulatory framework. Significant investments are being made in SMRs and advanced reactor demonstrations, with a strong focus on achieving energy independence and decarbonization.

- Europe: Countries like France, the UK, and Russia have long-standing nuclear programs and are actively investing in Generation IV technologies, particularly in fast reactors and molten salt reactors. The region emphasizes reducing reliance on fossil fuels, managing nuclear waste, and ensuring long-term energy security through advanced nuclear solutions.

- Asia Pacific (APAC): China, India, Japan, and South Korea are rapidly advancing their Generation IV reactor programs due to escalating energy demand, ambitious climate goals, and a need for energy diversification. China is particularly aggressive in deploying and testing various advanced reactor designs, positioning itself as a key global player.

- Latin America: While nascent, interest is growing in countries like Brazil and Argentina, which are exploring nuclear power to meet increasing electricity needs and reduce carbon emissions. Collaborations with technologically advanced nations are key to their progress in adopting Generation IV technologies.

- Middle East & Africa (MEA): The region is beginning to explore nuclear power for both electricity generation and desalination. Countries like the UAE and Saudi Arabia are investing in nuclear energy infrastructure, with potential future applications for Generation IV reactors to ensure long-term water and energy security.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Generation IV reactor Market.- BWX Technologies, Inc.

- Westinghouse Electric Company

- GE Hitachi Nuclear Energy

- TerraPower LLC

- Oklo Inc.

- Kairos Power

- X-energy

- Terrestrial Energy Inc.

- ARC Clean Energy Canada Inc.

- Rolls-Royce SMR

- China National Nuclear Corporation (CNNC)

- Rosatom

- Framatome

- Korea Electric Power Corporation (KEPCO)

- Japan Atomic Energy Agency (JAEA)

- Idaho National Laboratory (INL)

- European Atomic Energy Community (Euratom)

- Department of Energy (DOE)

- TVA

- Sargent & Lundy

Frequently Asked Questions

Analyze common user questions about the Generation IV reactor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Generation IV reactors and how do they differ from existing nuclear plants?

Generation IV reactors are a set of six advanced nuclear reactor designs selected for their potential to offer significant improvements over current (Generation II and III) reactors. Key differences include enhanced safety features, higher fuel efficiency, reduced radioactive waste generation, and potential for proliferation resistance. They often operate at higher temperatures and can utilize diverse fuel cycles, including spent nuclear fuel, for more sustainable energy production.

When are Generation IV reactors expected to be commercially available?

While some prototype and demonstration Generation IV reactors are already in operation or under construction, widespread commercial deployment is generally anticipated between 2030 and 2040. The timeline varies by reactor type and country, depending on regulatory approvals, financing, and technological maturity. Small Modular Reactors (SMRs) based on Gen IV designs may see earlier commercialization due to their smaller footprint and modular construction advantages.

Are Generation IV reactors safer than previous generations?

Yes, Generation IV reactors are designed with significantly enhanced safety features, often incorporating passive safety systems that rely on natural forces like gravity or convection to prevent accidents, rather than active systems requiring human intervention or external power. These designs aim to virtually eliminate the possibility of a large-scale radioactive release, even in extreme circumstances, thereby drastically improving their inherent safety profile.

How do Generation IV reactors address the issue of nuclear waste?

Generation IV reactors aim to dramatically reduce the volume and radiotoxicity of nuclear waste through more efficient fuel utilization and advanced fuel cycles. Some designs, particularly fast neutron reactors, are capable of "burning" or recycling long-lived radioactive isotopes from spent fuel of existing reactors, thereby minimizing the amount of high-level waste that requires long-term disposal and reducing its hazardous lifetime.

What role will Generation IV reactors play in combating climate change?

Generation IV reactors are crucial for combating climate change as they provide a reliable, dispatchable, and virtually carbon-free source of electricity and heat. Their high efficiency and ability to replace fossil fuel power plants will significantly reduce greenhouse gas emissions. Moreover, their potential for industrial heat and hydrogen production can decarbonize sectors beyond electricity, making them a cornerstone of a comprehensive global decarbonization strategy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted