Gaming Console Market

Gaming Console Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709542 | Last Updated : December 10, 2025 |

Format : ![]()

![]()

![]()

![]()

Gaming Console Market Size

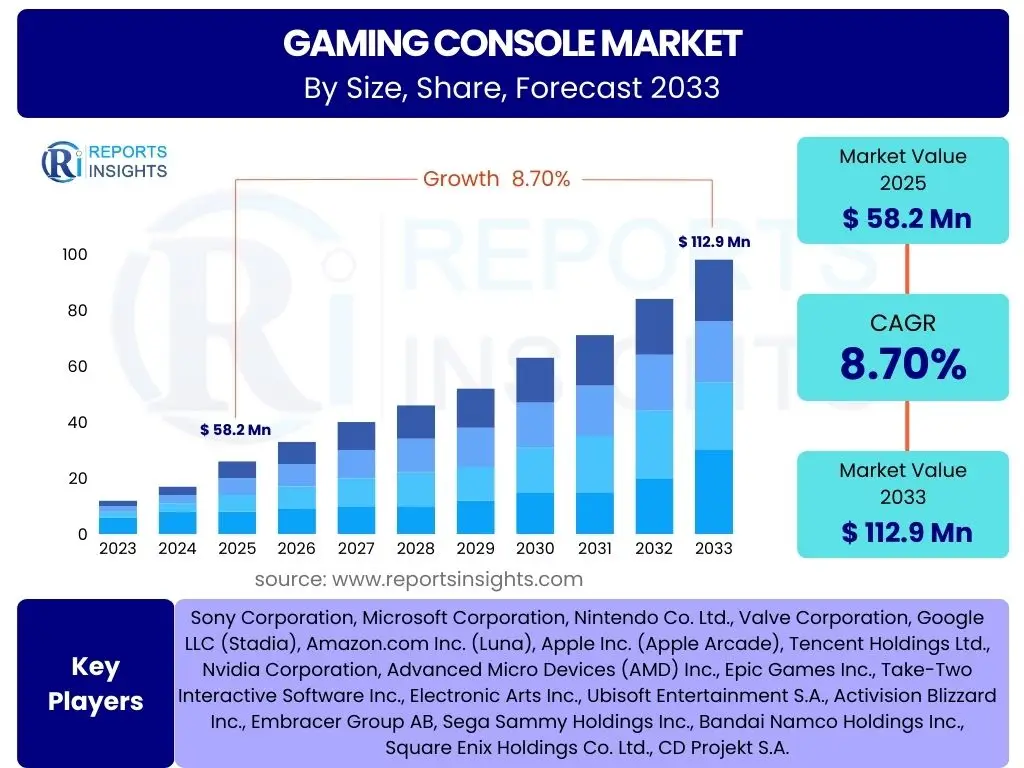

According to Reports Insights Consulting Pvt Ltd, The Gaming Console Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 58.2 billion in 2025 and is projected to reach USD 112.9 billion by the end of the forecast period in 2033.

Key Gaming Console Market Trends & Insights

Analysis of prevalent user inquiries regarding the gaming console market reveals a strong interest in the evolution of hardware capabilities, the impact of subscription services, and the shift towards cloud gaming. Users are keen to understand how technological advancements are shaping the gaming experience and what innovations are expected in the near future. There is also a notable focus on the accessibility of gaming, including concerns about console pricing and the availability of diverse game libraries. The rise of hybrid gaming models, blending traditional consoles with mobile and PC experiences, also frequently appears in discussions, indicating a desire for seamless cross-platform engagement.

The market is witnessing a profound shift driven by consumer demand for more immersive and flexible gaming environments. This includes advancements in graphics processing units (GPUs), central processing units (CPUs), and storage solutions, leading to higher fidelity visuals and faster load times. Furthermore, the strategic emphasis by major manufacturers on ecosystem development, encompassing both proprietary hardware and a robust suite of digital services, is a critical trend. This approach aims to foster customer loyalty and provide continuous value beyond the initial console purchase, creating a more interconnected and dynamic gaming experience.

- Enhanced Graphics and Processing Power: Continuous advancements in CPU and GPU technology for realistic visuals and fluid gameplay.

- Subscription Services Expansion: Growth of services like Xbox Game Pass and PlayStation Plus offering extensive game libraries.

- Rise of Cloud Gaming: Increasing adoption of streaming services, reducing reliance on local hardware.

- Hybrid Console Models: Blending portable and home console functionalities, exemplified by devices catering to diverse playstyles.

- Immersive Technologies Integration: Early stages of Virtual Reality (VR) and Augmented Reality (AR) adoption for deeper engagement.

- Digital Distribution Dominance: Shift from physical media to digital downloads for games and content.

- Cross-Platform Play and Progression: Growing demand for seamless gaming experiences across different devices and ecosystems.

AI Impact Analysis on Gaming Console

Common user questions concerning Artificial Intelligence (AI) in the gaming console sector often revolve around its potential to enhance gameplay, personalize user experiences, and streamline game development. Users frequently inquire about AI's role in creating more sophisticated Non-Player Characters (NPCs), dynamically adjusting game difficulty, and generating realistic environments. There is also interest in AI's application in optimizing console performance, predicting user preferences for content recommendations, and enabling more natural voice commands. Conversely, some concerns are raised about the potential for AI to diminish the creative role of human developers or to lead to less organic, algorithm-driven gameplay experiences.

The integration of AI into gaming consoles extends beyond in-game mechanics to impact the entire console ecosystem. AI algorithms are increasingly being used to manage system resources more efficiently, ensuring smoother performance even during graphically intensive sessions. Furthermore, AI-driven analytics are providing console manufacturers with deeper insights into player behavior, informing future hardware and software design decisions. This holistic application of AI aims to not only elevate the player's direct interaction with games but also to create a more responsive, adaptive, and intelligent console environment that anticipates user needs and continuously evolves.

- Advanced NPC Behavior: AI drives more realistic and adaptive enemy and ally behaviors in games.

- Procedural Content Generation: AI assists in creating vast, dynamic game worlds and content, reducing development time.

- Personalized Gaming Experiences: AI customizes game difficulty, recommendations, and narratives based on player skill and preferences.

- Optimized Console Performance: AI-driven algorithms manage system resources for improved efficiency and graphics rendering.

- Enhanced Accessibility: AI assists in features like adaptive controls, voice commands, and accessibility options for diverse players.

- Improved Graphics and Upscaling: AI-powered techniques (e.g., DLSS, FSR) enhance resolution and frame rates.

- Predictive Analytics for Content: AI analyzes player data to inform game development, marketing, and subscription offerings.

Key Takeaways Gaming Console Market Size & Forecast

Analysis of common user questions regarding the gaming console market size and forecast highlights a primary interest in understanding the long-term viability and growth trajectory of the industry amidst evolving technologies. Users are keen to know which segments—such as traditional home consoles versus handheld or cloud platforms—are projected to exhibit the strongest growth. There is significant curiosity about the factors driving market expansion, including innovation cycles, demographic shifts, and the impact of economic conditions. Furthermore, questions frequently arise about the potential for new market entrants or disruptive technologies to alter the competitive landscape and influence overall market valuation.

The market is poised for sustained growth, primarily fueled by ongoing technological advancements in hardware and the increasing penetration of high-speed internet, which facilitates digital distribution and cloud gaming. The strategic shift by leading players towards comprehensive ecosystem development, integrating hardware sales with recurring revenue from subscription services and digital content, is a key driver of this forecast. Emerging markets are also expected to play a crucial role, as rising disposable incomes and increasing access to gaming infrastructure broaden the global consumer base. These factors collectively indicate a robust and dynamic market outlook, characterized by innovation and expanding player engagement.

- Robust Market Expansion: The market is projected for significant growth, nearly doubling its valuation by 2033.

- Hardware Innovation as Core Driver: Continuous advancements in console processing, graphics, and storage will fuel sales.

- Subscription Model Dominance: Recurring revenue from services will become an increasingly vital component of market value.

- Cloud Gaming's Growing Influence: Cloud platforms are set to capture a larger share, expanding access to gaming.

- Emerging Markets Contribution: Asia Pacific and Latin America are expected to drive substantial demand and revenue growth.

- Strategic Ecosystem Development: Manufacturers are focusing on integrated hardware, software, and service offerings.

- Sustainable Growth Factors: A blend of technological evolution, digital adoption, and diverse content offerings supports long-term market health.

Gaming Console Market Drivers Analysis

The gaming console market's expansion is fundamentally driven by a confluence of technological advancements and evolving consumer behaviors. Innovations in hardware, particularly in processing power, graphics capabilities, and storage solutions, consistently compel consumers to upgrade to newer generations, ensuring a cyclical demand. Furthermore, the rapid growth of the gaming community, fueled by increased leisure time and a broader appeal of gaming as a form of entertainment, significantly contributes to market buoyancy. The proliferation of digital distribution channels and the rise of subscription-based gaming services also lower the barrier to entry for new players and enhance the value proposition for existing ones, thus expanding the market’s reach and revenue streams.

Beyond technological push and demographic pull, strategic business models adopted by leading console manufacturers play a pivotal role. The development of robust gaming ecosystems, including exclusive game titles, online multiplayer platforms, and value-added services, fosters brand loyalty and sustained engagement. The increasing affordability of entry-level consoles and the expanding availability of diverse gaming content cater to a wider spectrum of consumers, from casual to hardcore gamers. These factors collectively create a fertile ground for market growth, ensuring that the gaming console industry remains dynamic and responsive to both technological shifts and consumer preferences, underpinning its projected upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Advancements in Hardware (CPUs, GPUs, SSDs) | +1.8% | Global, particularly North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Increasing Adoption of Digital Distribution & Subscription Services | +1.5% | Global, strong in developed markets | Medium to Long Term (2027-2033) |

| Growth in the Gaming Population and Esports Popularity | +1.3% | Asia Pacific, North America, Europe | Medium to Long Term (2026-2033) |

| Expansion of Cloud Gaming Services | +1.2% | North America, Europe, East Asia | Medium to Long Term (2028-2033) |

Gaming Console Market Restraints Analysis

Despite its robust growth, the gaming console market faces several notable restraints that could temper its expansion. One significant challenge is the high initial cost of next-generation consoles, which can deter price-sensitive consumers, particularly in emerging markets. This upfront investment, coupled with the rising prices of AAA game titles, creates a substantial financial barrier. Furthermore, the market experiences intense competition from alternative gaming platforms, most notably PC gaming and mobile gaming, which offer diverse experiences, often with lower entry costs or free-to-play models. This fragmentation of the gaming landscape forces console manufacturers to continuously innovate and differentiate their offerings.

Another crucial restraint is the cyclical nature of console releases, which can lead to periods of market stagnation between new hardware generations. This pattern often results in lulls in consumer purchasing until a new, compelling console iteration is released. Supply chain disruptions, as evidenced by recent global events, also pose a significant threat, leading to manufacturing delays and product shortages that directly impact sales and market availability. Additionally, increasing concerns regarding digital addiction and screen time, alongside growing regulatory scrutiny in some regions, could gradually influence consumer spending habits and market perception, presenting a longer-term challenge for the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Console and Game Costs | -1.6% | Global, particularly emerging economies | Short to Medium Term (2025-2029) |

| Intense Competition from PC and Mobile Gaming | -1.4% | Global | Medium to Long Term (2026-2033) |

| Supply Chain Disruptions and Component Shortages | -1.0% | Global, impacts manufacturing hubs | Short Term (2025-2027) |

| Cyclical Nature of Console Releases and Market Saturation | -0.8% | Developed markets (North America, Europe) | Medium Term (2027-2030) |

Gaming Console Market Opportunities Analysis

The gaming console market is rich with opportunities, primarily stemming from the continued evolution of immersive technologies and the expansion into untapped demographics. The nascent but growing market for Virtual Reality (VR) and Augmented Reality (AR) gaming offers a significant avenue for console manufacturers to integrate these technologies, providing novel and deeply engaging experiences that differentiate their platforms. As these technologies mature and become more affordable, their adoption within the console ecosystem could unlock substantial new revenue streams and attract a segment of tech-savvy consumers eager for cutting-edge entertainment. Furthermore, the global expansion of internet infrastructure, especially in developing regions, broadens the potential consumer base for both hardware sales and digital content, including cloud gaming services.

Another crucial opportunity lies in enhancing console utility beyond traditional gaming. Integrating consoles more deeply into home entertainment systems, offering comprehensive media consumption platforms, and providing seamless access to a wide array of digital services can increase their value proposition to a broader audience. The growth of esports also presents an ongoing opportunity for console manufacturers to support competitive gaming, fostering community engagement and driving demand for high-performance hardware. Strategic partnerships with game developers to secure exclusive titles, alongside aggressive marketing in emerging markets, will be instrumental in capitalizing on these growth avenues. The continuous innovation in accessible gaming hardware and software, targeting diverse user needs, further solidifies the long-term potential for market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Virtual Reality (VR) and Augmented Reality (AR) Technologies | +2.2% | Global, high potential in developed markets | Medium to Long Term (2028-2033) |

| Expansion into Emerging Markets with Growing Middle Class | +1.9% | Asia Pacific, Latin America, MEA | Long Term (2029-2033) |

| Diversification of Console Functionality beyond Gaming (Media Hubs) | +1.5% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2030) |

| Development of Accessible Gaming Options for Diverse Audiences | +1.1% | Global | Medium Term (2027-2031) |

Gaming Console Market Challenges Impact Analysis

The gaming console market faces several significant challenges that demand strategic responses from industry players. One major hurdle is the rapid pace of technological obsolescence, where consoles, despite their advanced capabilities, can feel outdated within a few years due to advancements in PC hardware and cloud computing. This constant pressure to innovate and release new, compelling hardware generations creates substantial research and development costs and places a strain on manufacturers. Moreover, maintaining strong relationships with third-party game developers and securing exclusive content remains a persistent challenge, as developers increasingly explore multi-platform releases to maximize their audience reach and revenue.

Another critical challenge involves navigating evolving consumer expectations regarding digital rights management, content ownership, and platform interoperability. Users increasingly demand flexibility in how they access and play games, pushing against restrictive digital rights and proprietary ecosystems. Furthermore, the ethical implications surrounding in-game monetization, loot boxes, and predatory design practices present a growing regulatory and public relations challenge, particularly in regions with strong consumer protection laws. Addressing these issues while balancing profitability and innovation will be crucial for sustainable growth. Cybersecurity threats and the protection of user data also remain perpetual concerns that require continuous investment and vigilance from console providers to maintain user trust.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and High R&D Costs | -1.7% | Global | Medium Term (2026-2030) |

| Increasing Competition for Exclusive Game Titles and Content | -1.3% | Global, particularly competitive markets | Short to Medium Term (2025-2029) |

| Navigating Evolving Regulatory Landscapes (e.g., Loot Boxes, Data Privacy) | -1.1% | Europe, Asia Pacific, North America | Medium to Long Term (2027-2033) |

| Cybersecurity Threats and Data Privacy Concerns | -0.9% | Global | Continuous |

Gaming Console Market - Updated Report Scope

This report offers a comprehensive analysis of the global gaming console market, providing in-depth insights into its current size, historical performance, and future growth projections up to 2033. It covers key market trends, identifies the major drivers and restraints influencing the industry, and highlights emerging opportunities and challenges. The scope extends to a detailed segmentation analysis across various categories, including console type, component, end-user, and distribution channel, offering a granular view of market dynamics. Furthermore, the report provides a regional breakdown, pinpointing high-growth areas and the strategic landscape of prominent market players. This structured analysis aims to equip stakeholders with actionable intelligence for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 58.2 Billion |

| Market Forecast in 2033 | USD 112.9 Billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 250 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Sony Corporation, Microsoft Corporation, Nintendo Co. Ltd., Valve Corporation, Google LLC (Stadia), Amazon.com Inc. (Luna), Apple Inc. (Apple Arcade), Tencent Holdings Ltd., Nvidia Corporation, Advanced Micro Devices (AMD) Inc., Epic Games Inc., Take-Two Interactive Software Inc., Electronic Arts Inc., Ubisoft Entertainment S.A., Activision Blizzard Inc., Embracer Group AB, Sega Sammy Holdings Inc., Bandai Namco Holdings Inc., Square Enix Holdings Co. Ltd., CD Projekt S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The gaming console market is intricately segmented to reflect the diverse preferences of consumers and the technological breadth of offerings. These segmentations provide a granular view of market dynamics, enabling a precise understanding of which product categories, components, and user groups are driving growth and innovation. Analysis across these segments reveals shifts in consumer demand towards more versatile and technologically advanced systems, while also highlighting the enduring appeal of traditional console formats. Understanding these divisions is crucial for manufacturers to tailor product development, marketing strategies, and distribution channels to specific market niches, optimizing their competitive positioning and market penetration.

For instance, the segmentation by console type distinguishes between stationary home consoles, portable handheld devices, and emerging micro-consoles, each catering to different playstyles and environments. The component segmentation further dissects the market into hardware and software, emphasizing the critical role of high-performance processors, graphics units, and innovative game titles in shaping user experience. Similarly, segmenting by end-user, such as casual versus core gamers, helps identify key demographic targets and their specific needs, from accessibility features to competitive multiplayer functionalities. These detailed breakdowns are indispensable for strategic planning, allowing stakeholders to identify high-potential areas and anticipate future market shifts effectively.

- By Type: Home Consoles, Handheld Consoles, Micro Consoles, Dedicated Consoles

- By Component: Hardware (Processors, Memory, Storage, Peripherals), Software (Operating Systems, Games, Subscription Services)

- By End-User: Casual Gamers, Core/Enthusiast Gamers, Professional Gamers, Families

- By Distribution Channel: Online Retail (E-commerce, Digital Downloads), Offline Retail (Specialty Stores, Hypermarkets)

- By Resolution: HD, Full HD, 4K, 8K

Regional Highlights

- North America: This region represents a mature and highly lucrative market for gaming consoles, characterized by high disposable incomes, early adoption of new technologies, and a strong culture of competitive gaming and esports. The presence of major console manufacturers and game developers further solidifies its position as a key revenue generator, with strong demand for both hardware and digital content, including subscription services and cloud gaming.

- Europe: A diverse market with varying preferences across countries, Europe shows robust growth driven by a large gaming population, increasing internet penetration, and strong engagement with esports. Western European countries, in particular, exhibit high adoption rates for next-generation consoles and digital game sales, while Eastern Europe presents emerging opportunities for market expansion due to rising economic prosperity.

- Asia Pacific (APAC): The fastest-growing region, driven by its massive population, increasing middle-class income, and rapid urbanization. Countries like China, Japan, and South Korea are powerhouses in gaming, with strong local development scenes and a high propensity for mobile and console gaming. India and Southeast Asian nations are emerging as significant growth markets, fueled by improving internet infrastructure and increasing access to gaming devices.

- Latin America: This region is experiencing significant growth in the gaming console market, primarily due to expanding internet access, a youthful demographic, and rising discretionary spending. Brazil and Mexico are leading the charge, with increasing demand for affordable consoles and a growing interest in digital distribution and online multiplayer experiences.

- Middle East and Africa (MEA): While currently a smaller market, MEA offers considerable long-term potential. Growth is anticipated from increasing digital literacy, rising youth population, and government initiatives promoting technological infrastructure development. Countries like Saudi Arabia and the UAE are showing strong growth in gaming expenditure, driven by high disposable incomes and a strong interest in global entertainment trends.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gaming Console Market.- Sony Corporation

- Microsoft Corporation

- Nintendo Co. Ltd.

- Valve Corporation

- Google LLC

- Amazon.com Inc.

- Apple Inc.

- Tencent Holdings Ltd.

- Nvidia Corporation

- Advanced Micro Devices (AMD) Inc.

- Epic Games Inc.

- Take-Two Interactive Software Inc.

- Electronic Arts Inc.

- Ubisoft Entertainment S.A.

- Activision Blizzard Inc.

- Embracer Group AB

- Sega Sammy Holdings Inc.

- Bandai Namco Holdings Inc.

- Square Enix Holdings Co. Ltd.

- CD Projekt S.A.

Frequently Asked Questions

What is the projected growth rate for the Gaming Console Market?

The Gaming Console Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033.

What are the primary drivers of growth in the Gaming Console Market?

Key drivers include technological advancements in hardware, the expansion of digital distribution and subscription services, the growth of the global gaming population, and the rising popularity of cloud gaming.

How is AI impacting the Gaming Console industry?

AI is enhancing gaming through more realistic NPC behavior, procedural content generation, personalized player experiences, optimized console performance, and advanced graphics upscaling techniques.

Which regions are expected to drive the most growth in the Gaming Console Market?

Asia Pacific (APAC) is projected to be the fastest-growing region, followed by North America and Europe, due to increasing disposable incomes, technological adoption, and a vast gaming population.

What are the main challenges faced by the Gaming Console Market?

Significant challenges include the high initial cost of consoles and games, intense competition from PC and mobile gaming, potential supply chain disruptions, and the rapid pace of technological obsolescence requiring constant R&D investment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted