Fossil Fuel Fired Water Heater Market

Fossil Fuel Fired Water Heater Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706875 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

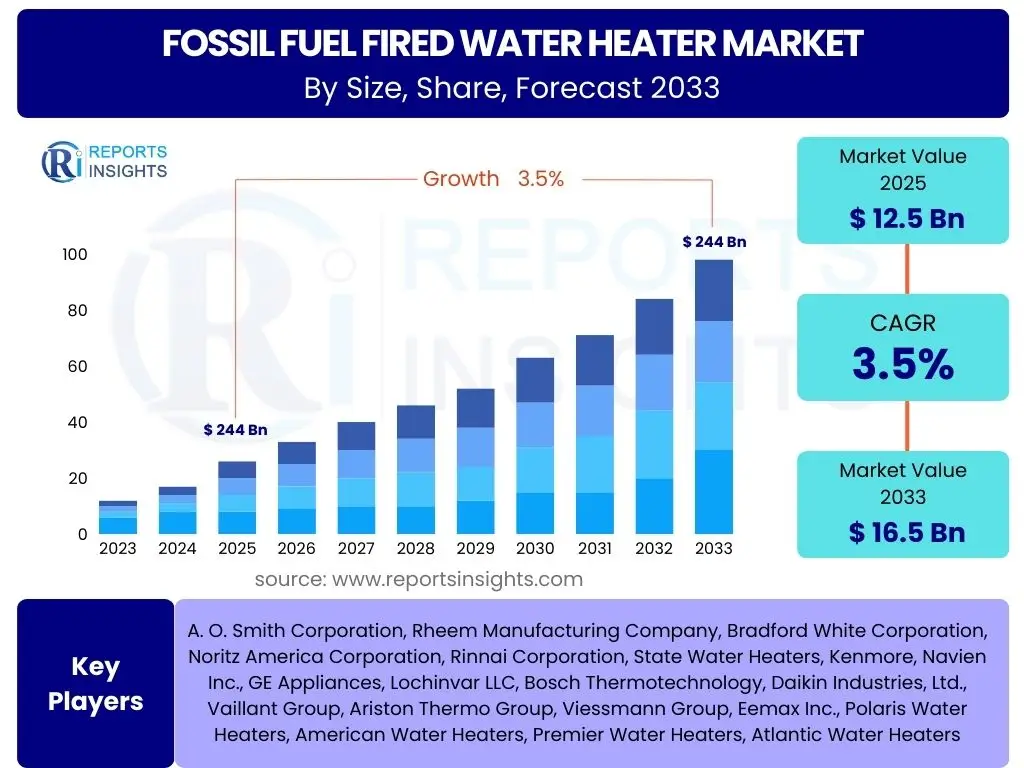

Fossil Fuel Fired Water Heater Market Size

According to Reports Insights Consulting Pvt Ltd, The Fossil Fuel Fired Water Heater Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.5% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 16.5 Billion by the end of the forecast period in 2033.

Key Fossil Fuel Fired Water Heater Market Trends & Insights

The fossil fuel fired water heater market is experiencing a confluence of trends, driven by evolving consumer demands, technological advancements, and increasing environmental consciousness. A significant trend involves the continuous drive towards enhanced energy efficiency. Manufacturers are integrating advanced combustion technologies and improved insulation to minimize heat loss and maximize energy utilization, responding to both regulatory pressures and consumer desires for lower operating costs. This focus on efficiency is crucial for the continued relevance of fossil fuel systems in an energy-conscious world, extending their competitive edge against alternative heating solutions.

Another emerging trend is the integration of smart technologies into fossil fuel water heaters. Connectivity features, such as remote monitoring and control via smartphone applications, are becoming more common. These smart capabilities allow users to optimize energy consumption, schedule heating cycles, and receive maintenance alerts, thereby enhancing convenience and improving overall system performance. Furthermore, the market is witnessing a regional divergence in demand, with developing economies maintaining strong reliance on fossil fuel options due due to existing infrastructure and cost-effectiveness, while developed nations increasingly prioritize decarbonization, leading to a focus on replacement markets and hybrid solutions.

- Enhanced energy efficiency through advanced combustion and insulation.

- Integration of smart technologies for remote monitoring and control.

- Increased adoption of hybrid water heating systems combining fossil fuels with renewable sources.

- Growing emphasis on regulatory compliance and emissions reduction.

- Shift towards demand-side management and personalized heating solutions.

AI Impact Analysis on Fossil Fuel Fired Water Heater

The integration of Artificial Intelligence (AI) into the fossil fuel fired water heater market, while not as immediately apparent as in other high-tech sectors, is poised to bring transformative changes, primarily in terms of operational efficiency, predictive maintenance, and optimized energy consumption. Users frequently inquire about how AI can make these traditional systems smarter and more environmentally friendly. AI algorithms can analyze usage patterns, weather data, and energy tariffs to predict hot water demand and adjust heating cycles accordingly, significantly reducing fuel consumption and operational costs. This capability moves beyond simple scheduling, offering a dynamic and responsive heating solution that adapts to real-time conditions.

Furthermore, AI plays a crucial role in predictive maintenance, a key concern for consumers looking to maximize the lifespan and reliability of their water heaters. AI-powered sensors can continuously monitor system performance, detect anomalies, and predict potential failures before they occur, enabling proactive servicing and preventing costly breakdowns. This not only enhances customer satisfaction but also extends the operational life of the unit, promoting sustainability through longevity. While not directly altering the fundamental combustion process, AI's indirect impact on efficiency, reliability, and informed consumer behavior presents a compelling value proposition for the market's evolution.

- Predictive maintenance for enhanced system reliability and longevity.

- Optimized energy consumption through AI-driven demand forecasting and adaptive heating cycles.

- Real-time diagnostics and anomaly detection for proactive servicing.

- Integration with smart home ecosystems for seamless energy management.

- Improved supply chain and inventory management for manufacturers and distributors.

Key Takeaways Fossil Fuel Fired Water Heater Market Size & Forecast

The fossil fuel fired water heater market, despite global decarbonization efforts, is expected to exhibit stable growth, driven largely by replacement demand, particularly in mature economies, and continued adoption in developing regions where these systems offer cost-effective and readily available heating solutions. User questions often highlight concerns about the longevity of this market given environmental pressures. The forecast indicates that while the market won't experience explosive growth, its foundational role in residential and commercial sectors, especially where infrastructure for electric or renewable alternatives is limited or expensive, ensures its sustained presence. The emphasis shifts towards efficiency upgrades and compliance with evolving environmental standards, rather than outright displacement.

A significant takeaway is the dual market dynamic: mature markets will focus on high-efficiency replacements and hybrid solutions to meet stricter regulations and consumer demands for lower carbon footprints, while emerging markets will continue to prioritize initial affordability and reliable heating. The competitive landscape will intensify, with manufacturers investing in product differentiation through smart features, improved efficiency, and reduced emissions to maintain market share. The market's resilience is tied to its established infrastructure and the practical realities of heating needs across diverse economic and climatic regions, making efficiency and lifecycle cost paramount considerations for both consumers and businesses.

- Steady growth projected, primarily driven by replacement demand and new construction in developing regions.

- Market resilience despite increasing competition from electric and renewable heating solutions.

- Emphasis on energy efficiency and emissions reduction as critical competitive factors.

- Regional disparities in adoption rates and regulatory impacts.

- Technological advancements, including smart features and hybrid systems, will define future offerings.

Fossil Fuel Fired Water Heater Market Drivers Analysis

The fossil fuel fired water heater market is significantly influenced by several key drivers that ensure its continued relevance in the global heating landscape. A primary driver is the widespread availability and established infrastructure for natural gas and propane distribution in many regions. This readily accessible fuel source makes fossil fuel water heaters a convenient and often cost-effective choice for both new installations and replacements, particularly in areas with limited or unstable electrical grids. The familiarity of installers and service technicians with these systems further contributes to their appeal, ensuring reliable maintenance and support.

Another crucial driver is the ongoing demand for hot water in residential, commercial, and industrial sectors, where fossil fuel water heaters consistently deliver high recovery rates and large volumes of hot water, meeting diverse application needs efficiently. While environmental concerns are rising, for many consumers and businesses, the lower upfront cost and robust performance of fossil fuel units, especially when replacing older inefficient models, present a compelling economic argument. Furthermore, population growth and urbanization in developing regions continue to fuel demand for reliable heating solutions, often leaning towards fossil fuel options due to their immediate availability and proven track record.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Established Fuel Infrastructure & Affordability | +1.2% | North America, Parts of Europe, APAC (China, India) | Long-term (2025-2033) |

| Consistent Hot Water Demand & High Recovery Rates | +0.8% | Global | Ongoing |

| Replacement of Aging Units | +1.0% | North America, Europe | Mid-term (2025-2029) |

| Lower Upfront Costs (compared to some alternatives) | +0.5% | Developing Economies (APAC, Latin America, MEA) | Long-term (2025-2033) |

Fossil Fuel Fired Water Heater Market Restraints Analysis

Despite the inherent advantages, the fossil fuel fired water heater market faces significant restraints, primarily stemming from global environmental mandates and shifting consumer preferences. Growing concerns over climate change and air quality are leading to increasingly stringent regulations aimed at reducing carbon emissions from residential and commercial heating systems. Governments worldwide are implementing policies that favor renewable energy sources and incentivize the adoption of electric or solar-powered water heaters, thereby creating a challenging regulatory landscape for fossil fuel alternatives. These regulations can include stricter efficiency standards, carbon taxes, or outright bans on new installations in specific contexts, directly impacting market growth.

Another substantial restraint is the volatile nature of fossil fuel prices. Fluctuations in the cost of natural gas, propane, and fuel oil can significantly impact the operational expenses for consumers, making alternative heating solutions with stable or lower long-term energy costs more appealing. This unpredictability adds a layer of financial risk for end-users and can deter investment in new fossil fuel systems. Furthermore, intense competition from cleaner, more energy-efficient alternatives such as electric heat pump water heaters, solar thermal systems, and tankless electric units presents a formidable challenge, as these technologies gain wider acceptance and benefit from supportive government incentives and advancements in their own efficiency and affordability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations & Decarbonization Goals | -1.5% | Europe, North America, Japan | Long-term (2025-2033) |

| Volatile Fossil Fuel Prices | -0.8% | Global | Mid-term (2025-2029) |

| Growing Competition from Electric & Renewable Alternatives | -1.0% | Global | Long-term (2025-2033) |

| Negative Public Perception & ESG Pressures | -0.5% | Developed Economies | Long-term (2025-2033) |

Fossil Fuel Fired Water Heater Market Opportunities Analysis

Despite the prevailing challenges, the fossil fuel fired water heater market presents several avenues for growth and innovation. A significant opportunity lies in the development and adoption of hybrid water heating systems that combine fossil fuel heating with renewable energy sources, such as solar thermal or electric heat pumps. These hybrid solutions offer a pathway to reduce overall carbon emissions while leveraging the reliability and high recovery rates of fossil fuels when needed. This approach allows manufacturers to cater to environmentally conscious consumers without fully abandoning established technologies, bridging the gap towards a more sustainable future for water heating.

Another promising opportunity involves the retrofitting and upgrading of existing fossil fuel water heaters to enhance their energy efficiency and performance. With a vast installed base of older, less efficient units globally, there is a substantial market for advanced combustion technologies, improved insulation, and smart controls that can be integrated into current systems. This not only extends the lifespan of existing infrastructure but also helps property owners meet evolving efficiency standards and reduce operating costs. Furthermore, growth in industrial and large-scale commercial applications where high demand and continuous hot water supply are critical, and where electric alternatives may be cost-prohibitive or impractical, continues to offer a stable segment for fossil fuel fired solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Hybrid Water Heating Systems | +0.9% | Global (especially Europe, North America) | Mid-to-Long-term (2027-2033) |

| Retrofitting & Upgrading Existing Units for Efficiency | +0.7% | North America, Europe | Short-to-Mid-term (2025-2029) |

| Growth in Industrial & Large Commercial Applications | +0.6% | Global (especially APAC, MEA) | Long-term (2025-2033) |

| Expansion in Developing Economies with Nascent Infrastructure | +0.8% | APAC, Latin America, Africa | Long-term (2025-2033) |

Fossil Fuel Fired Water Heater Market Challenges Impact Analysis

The fossil fuel fired water heater market faces several significant challenges that could impede its growth and evolution. Foremost among these is the accelerating global drive towards decarbonization and net-zero emissions targets. This overarching environmental goal places considerable pressure on industries reliant on fossil fuels, leading to policy initiatives and public sentiment that favor cleaner energy sources. As a result, the market must contend with potential regulatory hurdles, such as phase-out mandates, increased taxation on carbon emissions, or reduced incentives for fossil fuel-based installations, making it increasingly difficult for manufacturers to justify long-term investments in purely fossil fuel-driven technologies.

Another critical challenge is the intense and growing competition from electric and renewable energy alternatives. As technologies like heat pump water heaters and solar thermal systems become more efficient, affordable, and widely supported by government incentives, they pose a direct threat to the market share of fossil fuel units. This competition extends beyond residential applications into commercial and industrial sectors, where energy efficiency and long-term cost savings are increasingly prioritized. Furthermore, the public perception of fossil fuels as environmentally detrimental continues to shift, influencing consumer choices and potentially creating brand image challenges for manufacturers primarily offering these solutions, compelling them to invest heavily in efficiency improvements and sustainable messaging to maintain relevance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization & Net-Zero Targets | -1.8% | Global (especially Developed Nations) | Long-term (2025-2033) |

| Intensifying Competition from Green Alternatives | -1.2% | Global | Long-term (2025-2033) |

| Shifting Consumer Preferences Towards Sustainability | -0.9% | Developed Economies | Mid-to-Long-term (2027-2033) |

| Potential Supply Chain Disruptions & Material Costs | -0.6% | Global | Short-to-Mid-term (2025-2027) |

Fossil Fuel Fired Water Heater Market - Updated Report Scope

This report provides a comprehensive analysis of the Fossil Fuel Fired Water Heater Market, encompassing market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It offers an in-depth examination of the market's current landscape and future growth prospects, incorporating detailed quantitative forecasts and qualitative insights into the factors shaping industry dynamics. The scope includes an assessment of technological advancements, the impact of artificial intelligence, and competitive analysis of leading market players, aimed at providing stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 16.5 Billion |

| Growth Rate | 3.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | A. O. Smith Corporation, Rheem Manufacturing Company, Bradford White Corporation, Noritz America Corporation, Rinnai Corporation, State Water Heaters, Kenmore, Navien Inc., GE Appliances, Lochinvar LLC, Bosch Thermotechnology, Daikin Industries, Ltd., Vaillant Group, Ariston Thermo Group, Viessmann Group, Eemax Inc., Polaris Water Heaters, American Water Heaters, Premier Water Heaters, Atlantic Water Heaters |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fossil Fuel Fired Water Heater Market is comprehensively segmented to provide a granular understanding of its dynamics across various dimensions, reflecting diverse consumer needs, technological preferences, and application areas. This segmentation allows for a detailed analysis of specific market niches and their respective growth trajectories, offering insights into which segments are driving demand and where future opportunities lie. Understanding these breakdowns is crucial for manufacturers to tailor their product offerings and for investors to identify high-potential areas within the market landscape.

Key segmentation categories include fuel type, capacity, application, technology, and end-use. The fuel type segmentation distinguishes between natural gas, propane, and fuel oil systems, each with unique regional prevalences and infrastructure dependencies. Capacity segments address varying hot water demands, from small residential needs to large commercial and industrial requirements. Application and end-use categories help differentiate between new installations and the significant replacement market, which remains a cornerstone of demand in mature regions. Lastly, the technology segmentation highlights the distinctions between traditional storage tank heaters and the increasingly popular tankless (on-demand) systems, driven by efficiency and space-saving benefits.

- By Fuel Type:

- Natural Gas

- Propane

- Fuel Oil

- By Capacity:

- Less than 50 Gallons

- 50-80 Gallons

- Greater than 80 Gallons

- By Application:

- Residential

- Commercial

- Industrial

- By Technology:

- Tankless (On-demand)

- Storage Tank

- By End-Use:

- New Construction

- Retrofit/Replacement

Regional Highlights

The global fossil fuel fired water heater market exhibits distinct regional dynamics, shaped by factors such as existing infrastructure, regulatory environments, economic development, and cultural preferences. North America, particularly the United States and Canada, represents a mature market characterized by a substantial installed base of fossil fuel water heaters. Demand in this region is predominantly driven by replacement cycles, as homeowners and businesses upgrade older, less efficient units to newer, more efficient models often mandated by updated energy codes. While there's a growing interest in electric alternatives, the extensive natural gas pipeline infrastructure and the reliability of fossil fuel systems ensure their continued preference in many areas, particularly for larger homes or commercial applications with high hot water demand. Emphasis here is on high-efficiency condensing units and smart home integration.

Europe presents a complex landscape, with strong governmental pushes towards decarbonization and renewable energy sources. Countries like Germany and the UK are implementing stringent emissions regulations and offering incentives for heat pumps and solar thermal systems, which are gradually impacting the market for new fossil fuel water heater installations. However, in regions with colder climates and well-established gas networks, particularly Central and Eastern Europe, fossil fuel heaters remain a practical and cost-effective choice for many existing buildings. The market here is increasingly focused on hybrid solutions that combine fossil fuels with renewable energy to meet efficiency targets and reduce carbon footprints, allowing for a phased transition rather than an abrupt shift.

The Asia Pacific (APAC) region is poised for significant growth, driven by rapid urbanization, increasing disposable incomes, and the expansion of residential and commercial construction in developing economies such as China and India. While developed nations in APAC like Japan and South Korea are adopting stricter energy efficiency standards and exploring alternatives, the sheer scale of new construction and the existing reliance on natural gas and LPG infrastructure in the broader region contribute substantially to the demand for fossil fuel fired water heaters. Affordability and the ability to meet high hot water demands in multi-family dwellings are key factors, making these systems a prevalent choice. The market in APAC also sees a growing trend towards tankless water heaters due to space constraints and a desire for energy savings.

Latin America and the Middle East & Africa (MEA) represent emerging markets where the growth of the fossil fuel fired water heater market is strongly tied to economic development, infrastructure expansion, and access to fuel sources. In Latin America, the availability of natural gas varies by country, influencing adoption patterns, but overall increasing construction and middle-class expansion contribute to demand. In MEA, particularly in regions with abundant natural gas reserves, fossil fuel water heaters are widely adopted due to their cost-effectiveness and reliability. Infrastructure development projects and rising living standards are key drivers, though water scarcity concerns in some parts of MEA are also influencing discussions around overall energy and water consumption, pushing for more efficient solutions.

- North America: Dominant replacement market, focus on high efficiency and smart features, strong natural gas infrastructure.

- Europe: Challenged by decarbonization goals, growth in hybrid systems, varied regional adoption influenced by policy.

- Asia Pacific (APAC): Significant growth due to urbanization, new construction, and expanding middle class, increasing adoption of tankless heaters.

- Latin America: Growth driven by economic development and infrastructure, affordability is a key factor.

- Middle East & Africa (MEA): Consistent demand due to energy availability and construction boom, focus on traditional, robust solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fossil Fuel Fired Water Heater Market.- A. O. Smith Corporation

- Rheem Manufacturing Company

- Bradford White Corporation

- Noritz America Corporation

- Rinnai Corporation

- State Water Heaters

- Kenmore

- Navien Inc.

- GE Appliances

- Lochinvar LLC

- Bosch Thermotechnology

- Daikin Industries, Ltd.

- Vaillant Group

- Ariston Thermo Group

- Viessmann Group

- Eemax Inc.

- Polaris Water Heaters

- American Water Heaters

- Premier Water Heaters

- Atlantic Water Heaters

Frequently Asked Questions

What is the projected growth rate of the Fossil Fuel Fired Water Heater Market?

The Fossil Fuel Fired Water Heater Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.5% between 2025 and 2033, reaching an estimated USD 16.5 Billion by 2033.

How do environmental regulations impact the Fossil Fuel Fired Water Heater Market?

Environmental regulations, including stricter emissions standards and decarbonization goals, are a significant restraint, pushing manufacturers towards more efficient models and prompting consumers to consider alternative heating solutions. This leads to a greater focus on replacement markets and hybrid systems rather than new installations in highly regulated regions.

What are the primary drivers of the Fossil Fuel Fired Water Heater Market?

Key drivers include the extensive established fuel infrastructure, the consistent demand for high volumes of hot water, the affordability of these systems compared to some alternatives, and the ongoing need for replacement of aging units across residential and commercial sectors globally.

What role does AI play in the Fossil Fuel Fired Water Heater Market?

AI is increasingly integrated for predictive maintenance, optimizing energy consumption through smart demand forecasting, and enabling real-time diagnostics. This enhances system reliability, reduces operational costs, and contributes to more efficient energy management.

Which regions are key contributors to the Fossil Fuel Fired Water Heater Market?

North America and Europe are significant mature markets driven by replacement demand and efficiency upgrades. Asia Pacific (APAC) is a key growth region propelled by rapid urbanization and new construction, while Latin America and MEA also contribute due to economic development and energy availability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted