Food Gum Market

Food Gum Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710338 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

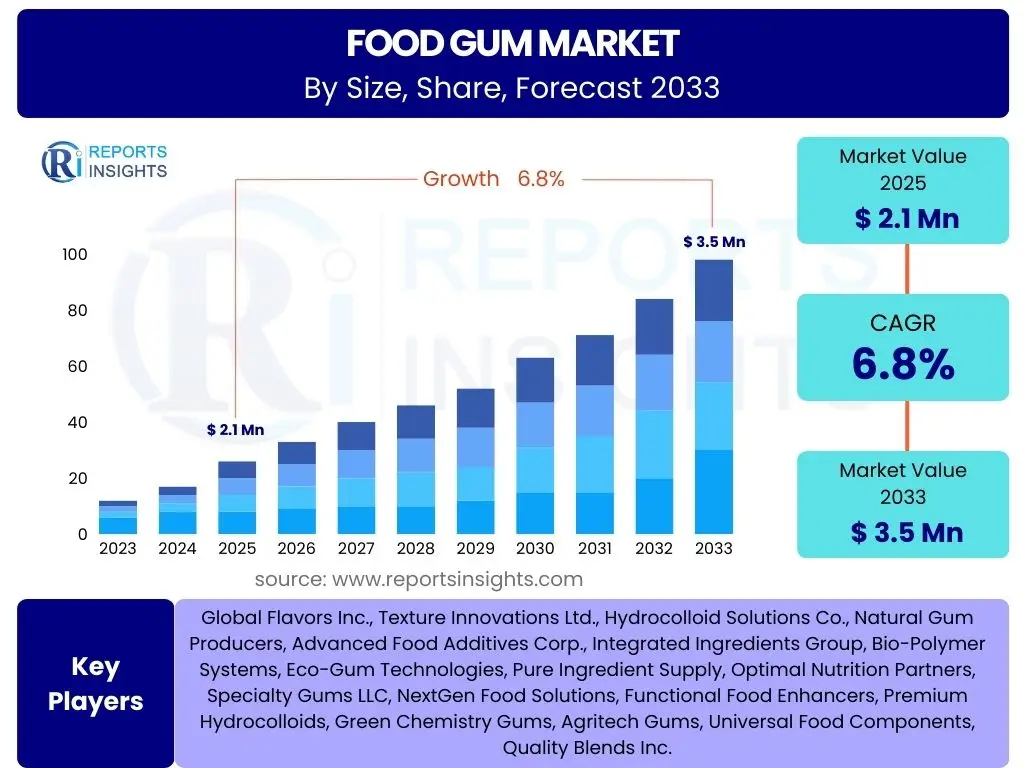

Food Gum Market Size

According to Reports Insights Consulting Pvt Ltd, The Food Gum Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 3.5 Billion by the end of the forecast period in 2033.

Key Food Gum Market Trends & Insights

The Food Gum Market is experiencing dynamic shifts driven by evolving consumer preferences and technological advancements. A primary trend involves the escalating demand for clean label ingredients, compelling manufacturers to favor natural and plant-derived gums over synthetic alternatives. Consumers are increasingly scrutinizing product labels for ingredients that are recognizable, minimally processed, and perceived as healthier, directly influencing sourcing and formulation strategies within the industry.

Furthermore, the rapid expansion of plant-based and vegan food sectors significantly contributes to market growth. Food gums play a crucial role in mimicking the texture, mouthfeel, and stability often provided by animal-derived ingredients, making them indispensable in alternative meat, dairy, and confectionery products. This trend not only opens new application avenues for existing gums but also spurs innovation in developing novel gum functionalities tailored to these specific dietary needs. Concurrently, advancements in processing technologies are enabling more efficient extraction and modification of gums, enhancing their performance and cost-effectiveness in diverse food matrices.

Another significant insight revolves around the increasing focus on functional food ingredients. Beyond their traditional roles as thickeners and stabilizers, food gums are being explored for added health benefits, such as prebiotic properties or fiber content. This trend aligns with a broader consumer desire for foods that offer more than basic nutrition, pushing manufacturers to research and develop gums that can contribute positively to gut health, satiety, or other wellness attributes. The interplay of these trends—clean label, plant-based innovation, and functional enhancements—is reshaping the competitive landscape and driving the overall trajectory of the food gum market.

- Escalating demand for clean label and natural ingredients in food products.

- Rapid growth in the plant-based and vegan food and beverage sectors.

- Increased focus on functional food gums offering health benefits like prebiotic fiber.

- Advancements in gum extraction and modification technologies enhancing performance.

- Rising consumer awareness regarding ingredient origin and sustainability.

- Shift towards specific texture profiles and improved sensory experiences in food formulation.

AI Impact Analysis on Food Gum

Artificial Intelligence (AI) is beginning to revolutionize various stages of the food gum lifecycle, from research and development to quality control and supply chain management. In the realm of R&D, AI algorithms can analyze vast datasets of ingredient interactions, predict optimal gum combinations for desired textures and stability, and even simulate the performance of new formulations. This significantly accelerates the product development cycle, allowing manufacturers to innovate faster and bring tailor-made solutions to market more efficiently, addressing specific sensory and functional requirements with unprecedented precision.

Moreover, AI plays a pivotal role in enhancing quality assurance and process optimization within food gum production. Machine learning models can monitor real-time production parameters, detecting anomalies and predicting potential quality deviations before they occur. This predictive capability ensures consistent product quality, minimizes waste, and optimizes resource utilization. For instance, AI-driven systems can analyze raw material characteristics, such as viscosity or purity, to adjust processing conditions dynamically, thereby maintaining batch consistency and adherence to stringent food safety standards. The ability to monitor and control complex variables accurately is paramount in maintaining the efficacy and reliability of food gum products.

Looking ahead, AI's influence extends to supply chain transparency and sustainability efforts. By leveraging AI-powered analytics, companies can forecast demand more accurately, optimize inventory levels, and track the origin and journey of raw materials more effectively. This not only reduces logistical costs but also supports ethical sourcing and sustainability initiatives by providing clearer insights into the supply chain's environmental and social footprint. While the initial adoption of AI may involve substantial investment in data infrastructure and skilled personnel, its long-term benefits in terms of efficiency, innovation, and compliance are poised to drive significant competitive advantages in the food gum sector.

- Accelerated R&D and formulation optimization through predictive modeling of ingredient interactions.

- Enhanced quality control and consistency in production via real-time monitoring and anomaly detection.

- Optimized supply chain management, including demand forecasting and raw material traceability.

- Improved process efficiency and reduced waste through AI-driven parameter adjustments.

- Personalized ingredient solutions for specific dietary or functional requirements.

- Potential for novel gum discovery and functional property enhancements through bioinformatics.

Key Takeaways Food Gum Market Size & Forecast

The Food Gum Market is poised for substantial growth through 2033, driven by a confluence of factors including evolving consumer dietary preferences, the imperative for clean label ingredients, and ongoing innovations in food processing. A primary takeaway is the market's resilience and adaptability, as manufacturers continuously respond to shifts towards plant-based diets, gluten-free options, and functional foods. This adaptability underpins the projected Compound Annual Growth Rate (CAGR) of 6.8%, indicating a robust expansion trajectory over the forecast period, reflecting sustained demand across various food applications.

Another critical insight is the increasing valuation of the market, moving from an estimated USD 2.1 Billion in 2025 to a projected USD 3.5 Billion by 2033. This growth is not merely volumetric but also qualitative, emphasizing the rising value contribution of high-performance and specialized gums. The market's expansion is particularly notable in emerging economies where rising disposable incomes and changing consumption patterns fuel demand for processed and convenience foods that rely heavily on gum ingredients for texture, stability, and shelf-life extension. Strategic investments in these regions are expected to yield significant returns for market participants.

Ultimately, the key takeaways underscore a market characterized by innovation and strategic diversification. Companies focusing on sustainable sourcing, developing multifunctional gum solutions, and leveraging advanced technologies like AI in formulation will be best positioned for future success. The market's future will largely be shaped by its ability to deliver ingredients that meet the dual demands of enhanced functionality and consumer-friendly profiles, ensuring food gums remain indispensable in the evolving global food landscape. Understanding these dynamics is crucial for stakeholders aiming to capitalize on the upcoming opportunities and navigate potential challenges effectively.

- Significant market expansion expected with a CAGR of 6.8% from 2025 to 2033.

- Market value projected to increase from USD 2.1 Billion in 2025 to USD 3.5 Billion by 2033.

- Demand for clean label and natural food gums is a primary growth catalyst.

- Growth heavily influenced by the proliferation of plant-based and functional food products.

- Innovation in gum functionalities and sourcing methods will be crucial for competitive advantage.

- Emerging economies present substantial growth opportunities due to changing dietary habits.

Food Gum Market Drivers Analysis

The Food Gum Market is propelled by several robust drivers, fundamentally rooted in evolving consumer demands and advancements in food technology. A significant driver is the global surge in demand for processed and convenience foods, where food gums are indispensable for achieving desired textures, stability, and extended shelf life. As lifestyles become more fast-paced, consumers increasingly rely on ready-to-eat meals, baked goods, and snack products, all of which heavily incorporate various gums to maintain quality and sensory appeal. This pervasive application across a broad spectrum of food categories provides a consistent and expanding baseline for market growth.

Furthermore, the growing consumer preference for clean label and natural ingredients acts as a powerful catalyst. There is a perceptible shift away from synthetic additives towards ingredients derived from natural sources, such as plants or microbes. This trend has spurred innovation and increased the adoption of natural food gums like xanthan, guar, and acacia gum, which are perceived as healthier and more consumer-friendly. Manufacturers are actively reformulating products to meet these transparency demands, thereby increasing the reliance on naturally sourced gum ingredients to achieve desired functional properties without compromising on label appeal.

Another key driver is the explosive growth of the plant-based food and beverage industry. As more consumers adopt vegetarian, vegan, or flexitarian diets, there is a heightened need for ingredients that can replicate the textural and structural properties of animal-derived products. Food gums effectively serve as texturizers, emulsifiers, and stabilizers in plant-based milks, meat alternatives, and dairy-free desserts, making them critical for the success and market acceptance of these innovative products. This burgeoning sector represents a substantial and continually expanding application area for the food gum market, driving both volume and value growth across various regions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for clean label and natural ingredients | +1.5% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

| Rising consumption of convenience and processed foods | +1.2% | Global | Long-term (2025-2033) |

| Expansion of the plant-based food and beverage industry | +1.8% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Technological advancements in food processing and formulation | +0.8% | Global | Mid to Long-term (2026-2033) |

| Increased focus on functional food products with health benefits | +0.7% | Developed Economies | Short to Mid-term (2025-2030) |

Food Gum Market Restraints Analysis

Despite its robust growth trajectory, the Food Gum Market faces several significant restraints that could temper its expansion. One prominent challenge is the price volatility of raw materials, particularly for natural gums whose availability can be affected by climatic conditions, geopolitical issues, and agricultural yields. Fluctuations in the cost of key inputs such as guar seeds, acacia trees, or seaweed directly impact production costs for manufacturers, leading to unstable pricing for end-users and potentially affecting profit margins across the value chain. This unpredictability makes long-term planning and consistent pricing strategies challenging for market participants.

Another substantial restraint is the complex and stringent regulatory landscape governing food additives, including gums, across different regions. Each country or economic bloc has its own set of approval processes, maximum usage levels, and labeling requirements. Navigating these diverse regulations can be time-consuming and costly, particularly for companies operating on a global scale. The need for extensive safety assessments and compliance documentation for novel gum applications or new markets can significantly delay product launches and limit market access, especially for smaller or emerging players. This regulatory burden can stifle innovation and market entry.

Furthermore, consumer perception regarding food additives, even natural ones, can act as a restraint. While there is a strong demand for clean label products, some consumers remain skeptical about ingredients they do not recognize, leading to a general preference for products with the fewest possible ingredients. Misinformation or negative media coverage, however isolated, can also impact the reputation of certain gums, leading to reduced consumer acceptance. Overcoming these perception hurdles requires continuous education and transparent communication from manufacturers, which represents an ongoing effort and a potential barrier to widespread adoption in certain product categories.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Price volatility of raw materials for natural gums | -0.9% | Global, particularly emerging markets | Short to Mid-term (2025-2030) |

| Stringent and complex regulatory approval processes | -0.7% | Europe, North America, China | Long-term (2025-2033) |

| Negative consumer perception regarding certain food additives | -0.5% | Developed Markets | Mid-term (2026-2031) |

| Competition from alternative texturizing agents and starches | -0.4% | Global | Long-term (2025-2033) |

Food Gum Market Opportunities Analysis

The Food Gum Market presents several compelling opportunities for growth and innovation, driven by evolving dietary trends and technological advancements. One significant area of opportunity lies in the burgeoning demand for plant-based and alternative protein products. As consumers increasingly seek substitutes for meat and dairy, food gums become essential for replicating the desired texture, stability, and mouthfeel in products like vegan burgers, plant-based yogurts, and non-dairy cheeses. Developing specialized gum blends that excel in these applications can unlock substantial market share and drive significant revenue growth, particularly in regions with high adoption rates of plant-forward diets.

Another key opportunity emerges from the rising consumer interest in functional foods and beverages. Beyond their traditional roles, food gums are being explored for added health benefits, such as their potential as prebiotics or sources of dietary fiber. Innovations in modifying existing gums or discovering novel natural hydrocolloids that offer these functional properties can cater to a growing segment of health-conscious consumers. This trend allows manufacturers to position food gums not just as ingredients for texture, but as contributors to digestive health, satiety, or other wellness attributes, thereby expanding their value proposition and market applications.

Furthermore, geographic expansion, particularly into emerging economies, represents a substantial growth avenue. Regions in Asia Pacific, Latin America, and the Middle East and Africa are experiencing rapid urbanization, rising disposable incomes, and a corresponding increase in demand for processed and convenience foods. As food processing industries in these regions mature, the need for high-quality food gums for stabilization, thickening, and gelling will escalate. Companies that establish strong distribution networks and tailor their product offerings to local culinary preferences and regulatory frameworks can capitalize on these untapped or under-penetrated markets, ensuring long-term sustainable growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of specialized gums for plant-based food industry | +1.3% | North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| Introduction of functional gums with added health benefits | +1.0% | Developed Economies | Short to Mid-term (2025-2030) |

| Expansion into emerging markets and developing regions | +1.5% | Asia Pacific, Latin America, MEA | Long-term (2027-2033) |

| Sustainable sourcing and production practices for enhanced brand value | +0.6% | Global | Mid-term (2026-2031) |

| Customized gum blends for niche applications and specific dietary needs | +0.5% | North America, Europe | Short to Mid-term (2025-2029) |

Food Gum Market Challenges Impact Analysis

The Food Gum Market, while promising, is not without its significant challenges that demand strategic navigation from industry players. One of the primary hurdles is ensuring consistent quality and purity of natural gum raw materials. Sourcing from diverse geographical locations, often subject to varying agricultural practices, environmental conditions, and processing standards, can lead to inconsistencies in the chemical composition and functional properties of the gums. Maintaining strict quality control throughout the supply chain, from harvesting to final processing, is crucial to meet the demanding specifications of food manufacturers and regulatory bodies, yet it represents a considerable logistical and technical challenge.

Another notable challenge stems from the intense competition from alternative texturizing and stabilizing agents, including modified starches, cellulose derivatives, and synthetic hydrocolloids. While natural gums benefit from clean label trends, these alternatives often offer cost advantages, easier availability, or specific functional properties that might be preferred in certain applications. This competitive landscape necessitates continuous innovation from food gum manufacturers to differentiate their products, demonstrate superior performance, and justify potential price premiums, thereby preventing market share erosion to substitute ingredients.

Furthermore, the high research and development costs associated with discovering novel gums or enhancing the functionalities of existing ones pose a significant barrier, especially for smaller market entrants. Developing new gum products requires substantial investment in scientific research, clinical trials for safety and efficacy, and extensive regulatory approval processes. This often lengthy and capital-intensive R&D cycle, coupled with the uncertainties inherent in innovation, means that only well-resourced companies can effectively pursue breakthrough advancements, potentially limiting the overall pace of transformative innovation in the broader market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring consistent quality and purity of natural raw materials | -0.8% | Global, particularly supply chain dependent regions | Long-term (2025-2033) |

| Competition from alternative texturizing and stabilizing agents | -0.6% | Global | Long-term (2025-2033) |

| High R&D costs for new gum functionalities and novel discoveries | -0.5% | Developed Markets | Mid to Long-term (2027-2033) |

| Supply chain disruptions due to climate change or geopolitical events | -0.7% | Global | Short-term (2025-2028) |

| Difficulty in achieving desired sensory attributes in complex food matrices | -0.4% | Global | Mid-term (2026-2031) |

Food Gum Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Food Gum Market, providing a detailed analysis of market size, growth projections, key trends, and the competitive landscape. It offers an in-depth segmentation based on gum type, application, function, and source, alongside an exhaustive regional analysis. The report's scope is designed to equip stakeholders with critical insights into market drivers, restraints, opportunities, and challenges, facilitating informed strategic decision-making within this evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 3.5 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Flavors Inc., Texture Innovations Ltd., Hydrocolloid Solutions Co., Natural Gum Producers, Advanced Food Additives Corp., Integrated Ingredients Group, Bio-Polymer Systems, Eco-Gum Technologies, Pure Ingredient Supply, Optimal Nutrition Partners, Specialty Gums LLC, NextGen Food Solutions, Functional Food Enhancers, Premium Hydrocolloids, Green Chemistry Gums, Agritech Gums, Universal Food Components, Quality Blends Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

A granular segmentation analysis is crucial for understanding the intricate dynamics and diverse opportunities within the Food Gum Market. This detailed breakdown allows for a comprehensive assessment of how various gum types, applications, functional roles, and sources contribute to the overall market landscape. By dissecting the market along these critical dimensions, stakeholders can identify high-growth niches, understand specific consumer demands, and pinpoint areas for strategic investment and product development. This approach provides a clearer picture of market evolution and competitive positioning.

The segmentation by type, for instance, highlights the dominance and growth rates of traditional hydrocolloids like xanthan and guar gum versus emerging novel gums, indicating shifts in material preference driven by performance and cost efficiencies. Application-based segmentation reveals which food and beverage sectors are most reliant on food gums and where innovation is most impactful, such as the increasing role of gums in plant-based alternatives or functional beverages. Furthermore, analyzing the market by function underscores the versatility of gums, from their primary roles in thickening and gelling to more advanced applications in emulsifying, encapsulating, and fat/sugar replacement, reflecting their critical role in modern food science. Lastly, source-based segmentation distinguishes between natural and synthetic gums, reflecting the clean label trend and demand for sustainable sourcing.

Each segment and its sub-segments are thoroughly examined to provide a holistic view of market performance and potential. This deep dive into segmentation enables businesses to tailor their strategies, optimize their product portfolios, and effectively target specific end-user industries or consumer groups. Understanding these segmented dynamics is paramount for any entity looking to gain a competitive edge or expand its footprint within the expansive and technologically evolving Food Gum Market.

- By Type: Xanthan Gum, Guar Gum, Arabic Gum, Carrageenan, Locust Bean Gum (LBG), Gellan Gum, Agar, Alginates, Pectin, Cellulose Gums (CMC, MCC), Starch-based Gums, Other Hydrocolloids.

- By Application: Confectionery, Bakery, Dairy Products, Meat & Poultry, Beverages, Sauces & Dressings, Snacks, Processed Foods, Others (e.g., Pet Food, Pharmaceuticals).

- By Function: Thickening, Gelling, Stabilizing, Emulsifying, Encapsulating, Texturizing, Binding, Fat Replacement, Sugar Replacement, Shelf-life Extension, Water Retention.

- By Source: Natural Gums, Synthetic Gums.

Regional Highlights

- North America: This region holds a significant share of the Food Gum Market, driven by high consumption of processed foods, a strong demand for clean label ingredients, and rapid growth in the plant-based food sector. The U.S. and Canada are major contributors, with increasing innovation in functional food applications and advanced food processing technologies.

- Europe: Europe represents another substantial market, characterized by stringent food safety regulations and a strong consumer preference for natural and organic products. Countries like Germany, the UK, and France are leading in the adoption of food gums for confectionery, bakery, and dairy alternative products, propelled by a growing vegan population and sustainability initiatives.

- Asia Pacific (APAC): Expected to be the fastest-growing region, APAC is driven by rapid urbanization, increasing disposable incomes, and changing dietary habits, leading to higher consumption of convenience and Western-style processed foods. China and India are key markets with immense potential due to their large populations and expanding food industries. The region also benefits from being a major source of several natural gums.

- Latin America: This region is experiencing steady growth in the Food Gum Market, primarily due to expanding food processing industries and rising demand for packaged foods. Brazil and Mexico are prominent markets, with increasing adoption of food gums in beverages, dairy, and confectionery products, fueled by economic development and evolving consumer preferences.

- Middle East and Africa (MEA): The MEA region presents emerging opportunities, influenced by population growth, urbanization, and a developing food and beverage sector. While starting from a smaller base, demand for food gums is increasing in processed meat, dairy, and bakery products, alongside rising health awareness and modern retail expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Food Gum Market.- Global Flavors Inc.

- Texture Innovations Ltd.

- Hydrocolloid Solutions Co.

- Natural Gum Producers

- Advanced Food Additives Corp.

- Integrated Ingredients Group

- Bio-Polymer Systems

- Eco-Gum Technologies

- Pure Ingredient Supply

- Optimal Nutrition Partners

- Specialty Gums LLC

- NextGen Food Solutions

- Functional Food Enhancers

- Premium Hydrocolloids

- Green Chemistry Gums

- Agritech Gums

- Universal Food Components

- Quality Blends Inc.

Frequently Asked Questions

Analyze common user questions about the Food Gum market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Food Gum Market?

The Food Gum Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated value of USD 3.5 Billion by 2033.

What are the primary drivers for the Food Gum Market's growth?

Key drivers include the increasing global demand for clean label and natural ingredients, the rapid expansion of the plant-based food industry, and the rising consumption of convenience and processed foods, all of which rely heavily on food gums for texture and stability.

Which regions are expected to show the most significant growth?

The Asia Pacific (APAC) region is anticipated to be the fastest-growing market, driven by urbanization, increasing disposable incomes, and evolving dietary preferences, particularly in countries like China and India.

How is AI impacting the Food Gum Market?

AI is accelerating research and development, optimizing formulations, enhancing quality control through real-time monitoring, and improving supply chain efficiency in the Food Gum Market, leading to faster innovation and consistent product quality.

What types of food gums are most prevalent in the market?

Hydrocolloids such as Xanthan Gum, Guar Gum, Arabic Gum, Carrageenan, and Locust Bean Gum are among the most prevalent types, widely used for their versatile thickening, gelling, and stabilizing properties across various food applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted