Floating Storage and Regasification Unit Market

Floating Storage and Regasification Unit Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701509 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Floating Storage and Regasification Unit Market Size

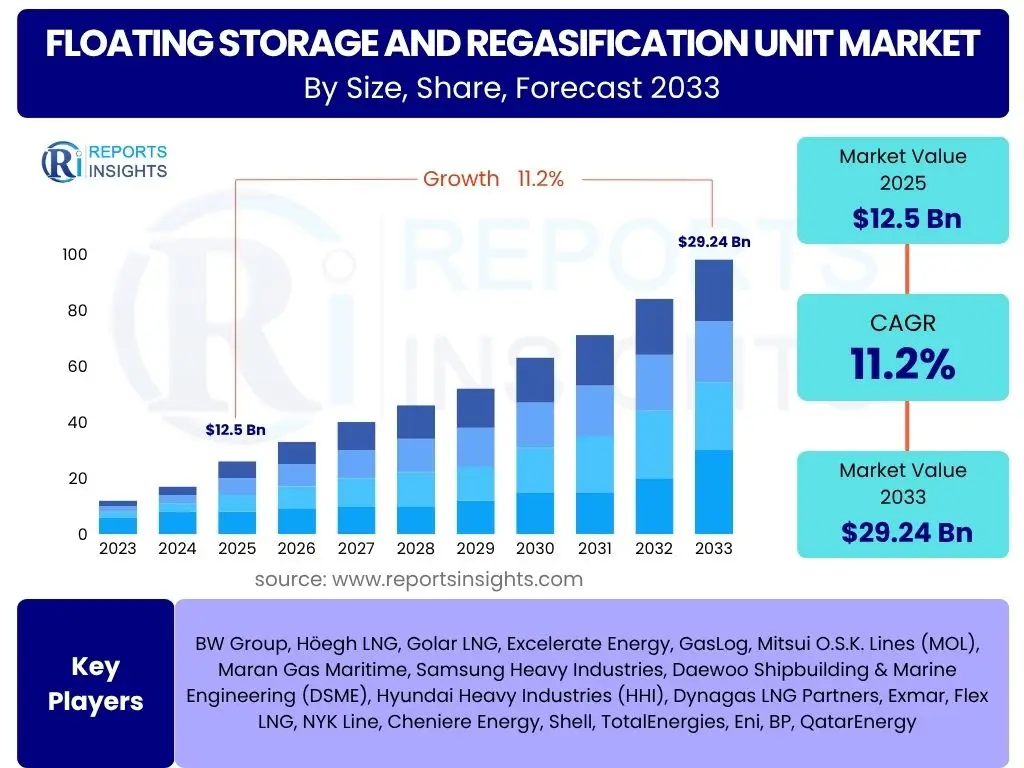

According to Reports Insights Consulting Pvt Ltd, The Floating Storage and Regasification Unit Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.2% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 29.24 Billion by the end of the forecast period in 2033.

Key Floating Storage and Regasification Unit Market Trends & Insights

The Floating Storage and Regasification Unit (FSRU) market is currently undergoing significant transformation, driven by an evolving global energy landscape and the pressing need for flexible and rapid energy infrastructure solutions. Key inquiries from market participants often revolve around the factors influencing deployment speed, the shift towards cleaner energy sources, and the geopolitical impacts on natural gas supply chains. Stakeholders are keen to understand how FSRUs are adapting to increasing environmental scrutiny and what innovations are emerging to enhance their efficiency and sustainability, particularly in regions with developing energy import capabilities or those seeking to diversify their energy mix.

There is a strong interest in understanding the role of FSRUs in facilitating the transition away from coal and oil, especially in developing economies where traditional pipeline infrastructure is limited or cost-prohibitive. Furthermore, the market is observing a trend towards smaller, more agile FSRUs that can serve niche markets or provide temporary solutions, offering greater adaptability to fluctuating demand and regulatory environments. This adaptability is crucial in a market characterized by high volatility in energy prices and an increasing emphasis on energy security.

User queries also highlight the growing importance of integration capabilities, such as the potential for FSRUs to support offshore renewable energy projects or to serve as hubs for broader energy complexes. This reflects a broader industry movement towards integrated energy solutions and a desire to maximize the utility and longevity of floating infrastructure assets. The insights gathered suggest a market poised for sustained growth, underpinned by technological advancements and strategic geopolitical considerations that position FSRUs as a vital component of future global energy security.

- Accelerated deployment timelines for energy security and supply diversification.

- Growing demand for flexible, cost-effective LNG import solutions.

- Increased adoption in emerging markets with limited onshore infrastructure.

- Focus on FSRUs as bridging solutions during energy transition.

- Technological advancements enhancing operational efficiency and environmental performance.

- Integration with renewable energy projects and hydrogen infrastructure exploration.

AI Impact Analysis on Floating Storage and Regasification Unit

The integration of Artificial intelligence (AI) within the Floating Storage and Regasification Unit (FSRU) sector is a subject of increasing curiosity among industry stakeholders, who frequently inquire about its potential to revolutionize operational efficiency, reduce costs, and enhance safety. Common user questions focus on how AI can enable predictive maintenance, optimize energy consumption, and improve decision-making in complex maritime and energy environments. There is a strong expectation that AI will move beyond basic automation to provide deeper analytical insights, transforming how FSRUs are managed and deployed globally.

Specifically, users are interested in AI's role in real-time performance monitoring, forecasting demand fluctuations for natural gas, and optimizing logistics for LNG supply chains linked to FSRUs. The potential for AI-driven systems to predict equipment failures, thereby minimizing downtime and ensuring continuous energy supply, is a particularly compelling aspect. Furthermore, queries often highlight the application of AI in enhancing safety protocols through advanced anomaly detection and remote monitoring capabilities, which are crucial for high-value and high-risk assets like FSRUs. The discussions indicate a clear industry recognition of AI as a transformative force, capable of unlocking new levels of efficiency and resilience in FSRU operations.

Beyond operational improvements, the broader impact of AI on strategic planning and investment decisions within the FSRU market is also a prominent area of interest. Users seek to understand how AI-powered market analytics can inform optimal FSRU deployment locations, capacity sizing, and long-term investment strategies. This reflects a shift towards data-driven decision-making, where AI's ability to process vast datasets quickly can provide a competitive edge. The overarching theme from user inquiries is a strong belief that AI will be instrumental in future-proofing FSRU operations, making them more responsive, efficient, and aligned with sustainable energy goals.

- Predictive maintenance for critical FSRU components, reducing downtime.

- Optimization of regasification processes and energy consumption.

- Real-time performance monitoring and anomaly detection for enhanced safety.

- Improved logistics and supply chain management for LNG deliveries.

- Data-driven decision-making for FSRU deployment and capacity planning.

- Autonomous or semi-autonomous operations in specific FSRU functions.

Key Takeaways Floating Storage and Regasification Unit Market Size & Forecast

Market participants and potential investors frequently seek concise summaries of the Floating Storage and Regasification Unit (FSRU) market's trajectory, focusing on its growth drivers and long-term viability. User inquiries consistently highlight the need to understand why the market is expanding at a significant rate and what factors underpin its projected financial performance. The core insights desired often relate to the strategic importance of FSRUs in global energy security, their economic advantages, and their role in facilitating the broader energy transition, especially in regions with burgeoning energy demands.

A key takeaway often emphasized is the robust growth trajectory of the FSRU market, projected to more than double its value by 2033. This substantial expansion is primarily attributed to the increasing global demand for natural gas as a transition fuel, coupled with the inherent flexibility and rapid deployment capabilities of FSRUs compared to traditional onshore infrastructure. Furthermore, the market's resilience against geopolitical fluctuations and its ability to offer diversified energy import options are frequently cited as significant advantages, attracting sustained investment and fostering new project developments across various geographies.

The continuous innovation within the FSRU sector, focusing on enhanced efficiency, reduced environmental footprint, and integration with diverse energy sources, is also a critical insight. This forward-looking approach ensures the FSRU market remains dynamic and adaptable to evolving energy policies and technological advancements. These insights collectively affirm the FSRU market's strategic importance and its promising future, positioning it as a pivotal component of the global energy infrastructure for the foreseeable future.

- Significant market growth, projected to more than double by 2033.

- FSRUs are crucial for global energy security and supply diversification.

- Cost-effectiveness and rapid deployment are key competitive advantages.

- Strong demand from emerging economies and energy-deficit regions.

- Continued innovation in FSRU technology and operational efficiency.

Floating Storage and Regasification Unit Market Drivers Analysis

The Floating Storage and Regasification Unit (FSRU) market is propelled by a confluence of global energy demands, strategic infrastructure needs, and the inherent flexibility of these floating terminals. A primary driver is the escalating global demand for natural gas, driven by industrial growth, urbanization, and the increasing adoption of cleaner fuels for power generation. FSRUs offer a highly adaptable and rapid solution to meet this demand, especially in regions where conventional onshore regasification terminals are not feasible due to financial constraints, land availability issues, or lengthy permitting processes. Their ability to be deployed quickly and relocate easily provides unparalleled flexibility in a dynamic energy market.

Another significant driver is the heightened focus on energy security and diversification of supply sources among nations. Geopolitical events and supply chain vulnerabilities have underscored the importance of securing reliable energy imports. FSRUs enable countries to establish new LNG import capabilities swiftly, bypassing the need for extensive onshore infrastructure development and reducing reliance on traditional pipeline networks. This strategic advantage allows nations to respond rapidly to changing energy landscapes and secure their domestic energy supply with greater autonomy.

Furthermore, the environmental benefits of natural gas as a transition fuel also contribute to the market's expansion. As countries commit to reducing carbon emissions, natural gas is increasingly viewed as a cleaner alternative to coal and oil. FSRUs facilitate the wider adoption of LNG by providing the necessary infrastructure for import and distribution, thereby supporting global efforts towards decarbonization and sustainable energy practices while offering a bridge towards a fully renewable energy future.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Natural Gas Demand | +2.1% | Asia Pacific, Europe, Latin America | 2025-2033 |

| Enhanced Energy Security and Diversification | +1.8% | Europe, Middle East, Southeast Asia | 2025-2030 |

| Cost-Effectiveness and Rapid Deployment | +1.5% | Emerging Markets, Island Nations | 2025-2033 |

| Role as a Bridge Fuel in Energy Transition | +1.2% | Global, especially developing economies | 2025-2033 |

| Limited Onshore Infrastructure Availability | +0.9% | Africa, Southeast Asia, South America | 2025-2030 |

Floating Storage and Regasification Unit Market Restraints Analysis

Despite their numerous advantages, the Floating Storage and Regasification Unit (FSRU) market faces several significant restraints that can impede its growth trajectory. One primary concern is the substantial capital expenditure required for FSRU projects. The acquisition or conversion of an FSRU, along with associated mooring and pipeline infrastructure, involves considerable upfront investment, which can be a barrier for potential developers, particularly in developing economies or those with limited access to financing. This high initial cost often necessitates long-term contracts and robust financial backing, adding complexity to project development.

Another critical restraint is the fluctuating and often volatile nature of global LNG prices. As FSRUs are intrinsically linked to the LNG trade, significant shifts in LNG supply and demand dynamics, influenced by geopolitical events, production capacities, and seasonal variations, can directly impact the economic viability of FSRU projects. Periods of exceptionally high or low LNG prices can deter new investments or make existing projects less profitable, leading to delays or cancellations. This price sensitivity introduces an element of financial risk that stakeholders must carefully manage.

Furthermore, regulatory complexities and environmental opposition pose significant challenges. FSRU projects often require a myriad of permits and approvals from various governmental and environmental agencies, which can be time-consuming and subject to changes. Environmental groups may raise concerns about the impact of FSRU operations on marine ecosystems, greenhouse gas emissions, or safety, leading to public opposition and prolonged legal battles. These factors can increase project timelines and costs, creating uncertainty for developers and potentially limiting the adoption of FSRU technology in certain regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Financing Needs | -1.5% | Global, particularly emerging markets | 2025-2033 |

| Volatile LNG Prices and Supply Dynamics | -1.3% | Global | 2025-2030 |

| Regulatory Hurdles and Permitting Delays | -1.0% | Europe, North America, Southeast Asia | 2025-2033 |

| Environmental Concerns and Public Opposition | -0.8% | Europe, North America, Australia | 2025-2030 |

| Competition from Onshore LNG Terminals | -0.5% | Developed Regions, established gas markets | 2028-2033 |

Floating Storage and Regasification Unit Market Opportunities Analysis

The Floating Storage and Regasification Unit (FSRU) market is ripe with opportunities driven by evolving energy demands, technological advancements, and strategic geopolitical shifts. A significant opportunity lies in the expanding demand from emerging markets, particularly in Southeast Asia, Africa, and Latin America. Many of these regions possess rapidly growing economies and increasing energy needs but lack the extensive onshore pipeline and regasification infrastructure. FSRUs offer a practical and swift solution to meet these energy deficits, enabling quick access to cleaner natural gas for power generation, industrial use, and residential consumption, thereby opening new frontiers for deployment and investment.

Another promising avenue is the potential for FSRU integration with renewable energy projects and the burgeoning hydrogen economy. As the world transitions towards more sustainable energy sources, FSRUs can serve as a flexible backup or complementary energy source for intermittent renewables like offshore wind or solar. Furthermore, there is growing interest in utilizing FSRUs for the storage and regasification of green hydrogen or its derivatives, such as ammonia, once these technologies scale up. This positions FSRUs as a future-proof asset, capable of adapting to the evolving energy mix and supporting the long-term decarbonization goals of various nations.

The trend towards small-scale and modular FSRU solutions also presents a considerable opportunity. These smaller units can cater to niche markets, remote communities, or serve as temporary solutions during infrastructure development, offering greater flexibility and lower upfront costs. This approach broadens the applicability of FSRU technology beyond large-scale industrial consumers to include decentralized energy systems. Additionally, the conversion of existing LNG carriers into FSRUs offers a cost-effective and faster alternative to newbuilds, capitalizing on existing maritime assets and reducing lead times for project delivery, thus stimulating market activity and innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging and Underserved Markets | +2.0% | Southeast Asia, Africa, Latin America | 2025-2033 |

| Integration with Renewable Energy and Hydrogen Infrastructure | +1.7% | Europe, North America, East Asia | 2028-2033 |

| Development of Small-Scale and Modular FSRUs | +1.4% | Island Nations, Remote Regions, Niche Markets | 2025-2033 |

| Conversion of Existing LNG Carriers to FSRUs | +1.0% | Global | 2025-2030 |

| Strategic Partnerships and Collaborations | +0.7% | Global | 2025-2033 |

Floating Storage and Regasification Unit Market Challenges Impact Analysis

The Floating Storage and Regasification Unit (FSRU) market, while promising, contends with several operational and market-related challenges that can impact project viability and overall growth. A significant hurdle is the potential for supply chain disruptions and the availability of specialized equipment and skilled labor. The construction and maintenance of FSRUs rely on a complex global supply chain for critical components, and any geopolitical tensions, trade disputes, or logistical bottlenecks can lead to delays and cost overruns. Moreover, the highly specialized nature of FSRU operations necessitates a workforce with niche maritime and gas processing expertise, which can be challenging to source and retain, leading to potential operational inefficiencies or safety concerns.

Another major challenge is the inherent technical complexities and high maintenance costs associated with FSRU operations. These vessels are sophisticated engineering marvels, requiring continuous monitoring, advanced safety systems, and regular maintenance to ensure optimal performance and compliance with stringent maritime regulations. The harsh marine environment, coupled with the cryogenic temperatures involved in LNG handling, imposes significant wear and tear, leading to substantial ongoing operational and maintenance expenditures. These costs can erode profit margins and make FSRU projects less attractive compared to alternative energy solutions, particularly for long-term deployments.

Furthermore, intense competition from alternative energy sources and infrastructure solutions presents a persistent challenge. As renewable energy technologies become more cost-effective and efficient, and as pipeline networks expand in certain regions, FSRUs may face increased competition for investment and market share. The perception of natural gas as a transitional fuel, rather than a permanent solution, can also influence policy decisions and investor sentiment, potentially leading to a shorter operational lifespan for some FSRU projects. Navigating this evolving energy landscape requires strategic positioning and a continuous demonstration of FSRUs' unique value proposition to remain competitive.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Equipment Availability | -1.2% | Global | 2025-2030 |

| Technical Complexities and High Maintenance Costs | -1.0% | Global | 2025-2033 |

| Skilled Labor Shortages and Training Requirements | -0.7% | Global | 2025-2033 |

| Competition from Alternative Energy Sources | -0.5% | Europe, North America, East Asia | 2028-2033 |

| Geopolitical Risks and Regional Instability | -0.4% | Specific conflict zones, energy trade routes | 2025-2030 |

Floating Storage and Regasification Unit Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Floating Storage and Regasification Unit (FSRU) market, offering critical insights into its current state, historical performance, and future projections. The report meticulously details market size estimations, growth drivers, key restraints, emerging opportunities, and prevailing challenges influencing the industry landscape. It incorporates a thorough segmentation analysis across various parameters, alongside a detailed regional outlook, to provide a holistic understanding of market dynamics. Furthermore, the report profiles key market players, offering competitive intelligence crucial for strategic decision-making within the FSRU sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 29.24 Billion |

| Growth Rate | 11.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BW Group, Höegh LNG, Golar LNG, Excelerate Energy, GasLog, Mitsui O.S.K. Lines (MOL), Maran Gas Maritime, Samsung Heavy Industries, Daewoo Shipbuilding & Marine Engineering (DSME), Hyundai Heavy Industries (HHI), Dynagas LNG Partners, Exmar, Flex LNG, NYK Line, Cheniere Energy, Shell, TotalEnergies, Eni, BP, QatarEnergy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Floating Storage and Regasification Unit (FSRU) market is broadly segmented based on several key characteristics that define project scope, technical specifications, and end-use applications. This segmentation provides a granular view of market dynamics, allowing for a more precise understanding of demand patterns and strategic investment areas. Analyzing these segments helps stakeholders identify lucrative opportunities and tailor solutions to specific market needs, whether driven by the type of FSRU, its capacity, or the primary application it serves.

The "By Type" segmentation distinguishes between newly constructed FSRUs, designed from the ground up for their specific purpose, and converted FSRUs, which are repurposed LNG carriers modified to include regasification capabilities. Converted FSRUs often offer advantages in terms of faster deployment and lower capital costs, making them attractive for immediate energy needs, while newbuilds can be optimized for specific long-term operational requirements and larger capacities. The "By Capacity" segment categorizes FSRUs based on their LNG storage volume, impacting their ability to serve different scales of demand, from smaller regional projects to large-scale industrial or national grid supply. This allows for tailored solutions addressing varying energy consumption profiles.

Further segmentation by "Application" reveals the primary end-uses of regasified natural gas, including power generation, industrial feedstock, and residential and commercial consumption. This highlights the diverse roles FSRUs play in a nation's energy infrastructure. Finally, the "By Ownership" segment differentiates between FSRUs that are owned directly by the operator or energy company versus those that are leased, reflecting different financing and operational models prevalent in the market. Understanding these segments is crucial for navigating the FSRU market effectively and developing targeted business strategies.

- By Type: Newbuild FSRUs, Converted FSRUs

- By Capacity: Up to 130,000 cbm, 130,000-170,000 cbm, Above 170,000 cbm

- By Application: Power Generation, Industrial Feedstock, Residential & Commercial, Others

- By Ownership: Owned, Leased

Regional Highlights

- North America: The region is experiencing a renewed interest in FSRUs, particularly in the US, as a means to enhance energy security and support gas exports to global markets, driven by abundant shale gas resources. The focus here is on leveraging FSRUs for flexibility in LNG trade and potential re-export capabilities, complementing established pipeline networks and existing onshore terminals.

- Europe: Driven by geopolitical events and the imperative to diversify natural gas supply sources away from traditional pipeline imports, Europe has rapidly embraced FSRUs. Countries like Germany, Finland, and the Netherlands have quickly deployed FSRUs to secure alternative LNG supplies, making Europe a significant growth hub for FSRU utilization as a strategic energy import solution.

- Asia Pacific (APAC): APAC remains a dominant market for FSRUs due to burgeoning energy demand, rapid industrialization, and a growing reliance on LNG imports in countries such as China, India, Pakistan, Bangladesh, and the Philippines. The region's diverse energy landscapes and varying levels of onshore infrastructure development make FSRUs an ideal solution for quick and flexible energy access.

- Latin America: Several Latin American countries, including Brazil, Argentina, and Colombia, utilize FSRUs to supplement domestic gas production and manage seasonal demand fluctuations. The region values FSRUs for their ability to provide rapid and flexible energy solutions, particularly in coastal areas with limited conventional infrastructure.

- Middle East and Africa (MEA): The MEA region presents significant opportunities for FSRU deployment. While the Middle East is a major LNG producer, some countries are exploring FSRUs for domestic consumption or re-export flexibility. In Africa, FSRUs are critical for countries like South Africa, Ghana, and Senegal, which are transitioning to natural gas for power generation and industrial growth, leveraging FSRUs to overcome infrastructure deficits.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Floating Storage and Regasification Unit Market.- BW Group

- Höegh LNG

- Golar LNG

- Excelerate Energy

- GasLog

- Mitsui O.S.K. Lines (MOL)

- Maran Gas Maritime

- Samsung Heavy Industries

- Daewoo Shipbuilding & Marine Engineering (DSME)

- Hyundai Heavy Industries (HHI)

- Dynagas LNG Partners

- Exmar

- Flex LNG

- NYK Line

- Cheniere Energy

- Shell

- TotalEnergies

- Eni

- BP

- QatarEnergy

Frequently Asked Questions

Analyze common user questions about the Floating Storage and Regasification Unit market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Floating Storage and Regasification Unit (FSRU)?

An FSRU is a special type of ship that can store liquefied natural gas (LNG) and then convert it back into gaseous form (regasification) for delivery into a pipeline network. Essentially, it functions as a floating LNG import terminal, offering flexibility and rapid deployment compared to fixed onshore facilities.

What are the primary advantages of FSRUs over traditional onshore LNG terminals?

FSRUs offer several key advantages, including significantly faster deployment times, lower capital costs, greater flexibility to relocate, and reduced environmental impact compared to large-scale onshore terminals. They are ideal for markets with urgent energy needs, seasonal demand, or limited onshore space.

Where are FSRUs primarily deployed and why?

FSRUs are primarily deployed in regions with growing energy demand, limited natural gas infrastructure, or a strategic need for energy supply diversification. Key regions include Asia Pacific (e.g., Bangladesh, Pakistan, Philippines), Europe (e.g., Germany, Finland), Latin America (e.g., Brazil), and parts of Africa, driven by the need for quick and reliable access to natural gas.

How do FSRUs contribute to energy security?

FSRUs enhance energy security by enabling countries to quickly establish new LNG import capabilities, thereby diversifying their energy supply sources and reducing reliance on traditional pipeline imports. Their rapid deployment allows nations to respond swiftly to energy crises or changing geopolitical landscapes, ensuring a stable energy supply.

What is the future outlook for the FSRU market?

The FSRU market is projected for robust growth, driven by increasing global natural gas demand, energy security concerns, and the ongoing energy transition. Future trends include the development of smaller, more flexible units, potential integration with hydrogen infrastructure, and continued deployment in emerging economies seeking reliable and efficient energy solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted