Finished Lubricant Market

Finished Lubricant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704906 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

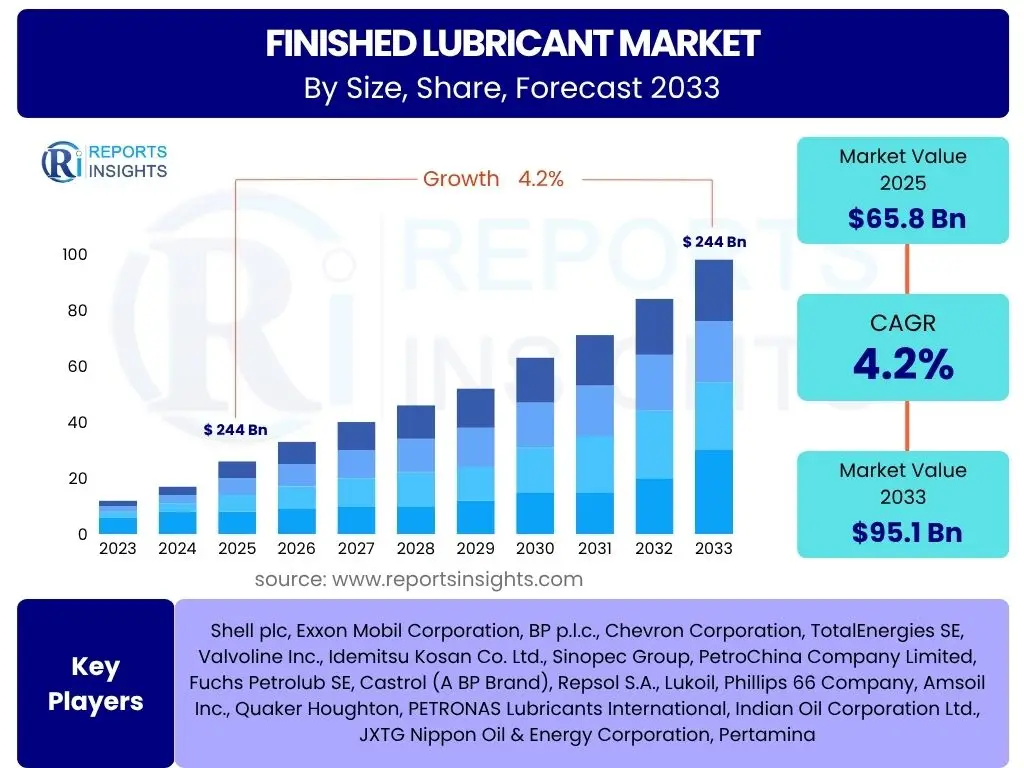

Finished Lubricant Market Size

According to Reports Insights Consulting Pvt Ltd, The Finished Lubricant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.2% between 2025 and 2033. The market is estimated at USD 65.8 Billion in 2025 and is projected to reach USD 95.1 Billion by the end of the forecast period in 2033.

Key Finished Lubricant Market Trends & Insights

The Finished Lubricant market is undergoing significant transformation, driven by evolving industry demands, stringent environmental regulations, and advancements in material science. Key trends include a pronounced shift towards high-performance and specialty lubricants, particularly synthetics and bio-based alternatives, which offer superior efficiency, extended drain intervals, and reduced environmental impact. The electrification of the automotive sector, while reducing traditional lubricant volumes for internal combustion engines, is simultaneously creating new opportunities for specialized e-fluids and thermal management lubricants.

Furthermore, digitalization and the integration of smart technologies are enhancing lubricant monitoring and predictive maintenance, allowing for optimized performance and reduced operational costs across industrial applications. Supply chain resilience and sustainability initiatives, such as re-refining and circular economy models, are also gaining traction. These trends collectively underscore an industry moving towards greater innovation, environmental responsibility, and efficiency, influencing product development, market strategies, and competitive landscapes globally.

- Growing demand for high-performance and specialty lubricants.

- Increased adoption of synthetic and bio-based lubricants driven by environmental concerns.

- Development of specialized e-fluids for electric vehicles (EVs).

- Integration of digitalization and IoT for predictive maintenance and lubricant monitoring.

- Focus on sustainability, circular economy models, and re-refining technologies.

- Consolidation among market players and strategic partnerships for technology development.

- Regional shifts in demand, with Asia Pacific leading in consumption and production.

AI Impact Analysis on Finished Lubricant

Artificial intelligence (AI) is poised to revolutionize various facets of the finished lubricant industry, from research and development to manufacturing, supply chain management, and end-user applications. Companies are exploring AI-driven solutions to accelerate the formulation of new lubricants by predicting material properties and optimizing additive packages, significantly reducing development cycles and costs. This predictive capability enables the creation of highly specialized lubricants tailored for specific industrial machinery or emerging automotive technologies.

In operational contexts, AI algorithms are enhancing predictive maintenance programs by analyzing sensor data from machinery to forecast equipment failures and optimize lubricant change intervals, thereby extending asset life and minimizing downtime. Moreover, AI can optimize supply chain logistics, manage inventory more efficiently, and improve quality control processes through advanced anomaly detection. While the initial investment in AI infrastructure and data integration poses a challenge, the long-term benefits in terms of efficiency, cost reduction, and product innovation are expected to drive its increasing adoption across the finished lubricant value chain.

- AI-driven optimization of lubricant formulations and additive packages.

- Enhanced predictive maintenance capabilities for industrial machinery and vehicles.

- Improved supply chain efficiency and inventory management through AI analytics.

- Automated quality control and anomaly detection in lubricant production.

- Personalized lubricant recommendations and customer support.

- Data-driven insights for market trend analysis and product demand forecasting.

- Potential for energy savings and reduced environmental impact through optimized lubricant use.

Key Takeaways Finished Lubricant Market Size & Forecast

The Finished Lubricant Market is positioned for robust growth through 2033, driven by ongoing industrial expansion, the evolving automotive landscape, and an increasing emphasis on performance and sustainability. The projected significant increase in market value reflects a dynamic industry adapting to technological shifts and regulatory pressures. While traditional segments continue to provide a stable foundation, the market's future growth is increasingly tied to the adoption of advanced synthetic and bio-based formulations, particularly in high-growth regions and specialized applications.

Strategic investments in research and development, coupled with a focus on sustainable practices and digital integration, will be crucial for companies aiming to capitalize on this growth. The forecast indicates sustained demand across industrial and automotive sectors, with emerging economies playing a pivotal role in market expansion. Stakeholders must strategically navigate the transition towards electric vehicles and the circular economy, recognizing that new market niches and technological solutions will redefine the competitive landscape.

- Market projected to reach USD 95.1 Billion by 2033, demonstrating substantial growth potential.

- CAGR of 4.2% indicates steady expansion, influenced by diverse end-use sectors.

- Significant shift towards high-value, high-performance synthetic and bio-based lubricants.

- Emerging economies, particularly in Asia Pacific, are central to future market expansion.

- Technological advancements and sustainability initiatives are key drivers shaping the market's trajectory.

Finished Lubricant Market Drivers Analysis

The Finished Lubricant market is propelled by a confluence of macroeconomic and industry-specific factors. Global industrialization and urbanization continue to drive demand for machinery and equipment, all of which require various types of lubricants for efficient operation and longevity. Rapid expansion in manufacturing, construction, mining, and power generation sectors, particularly in developing regions, directly translates into increased consumption of industrial lubricants. Simultaneously, the automotive sector remains a cornerstone of demand, with a growing global vehicle parc and the continuous evolution of engine technologies requiring increasingly sophisticated and performance-enhancing lubricants.

Furthermore, stringent regulatory frameworks focused on reducing emissions and improving fuel efficiency are compelling lubricant manufacturers to innovate. This pressure leads to the development and adoption of advanced, high-performance lubricants that offer superior wear protection, extended drain intervals, and reduced friction. The rising awareness and demand for energy efficiency across industries also contribute, as optimized lubrication can significantly lower energy consumption and operational costs. These combined forces create a consistent demand pull for innovative and efficient finished lubricant products.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industrialization and Manufacturing Growth | +0.7% | Asia Pacific, Latin America, Africa | Long-term |

| Growing Automotive Production and Vehicle Parc | +0.6% | Global, especially Asia Pacific | Medium-term |

| Increasing Demand for High-Performance Lubricants | +0.5% | North America, Europe, Asia Pacific | Long-term |

| Stringent Environmental Regulations and Fuel Efficiency Standards | +0.4% | Europe, North America, China | Medium-long term |

| Technological Advancements in Machinery and Engines | +0.3% | Global | Long-term |

Finished Lubricant Market Restraints Analysis

Despite robust growth drivers, the Finished Lubricant market faces several significant restraints that could impede its expansion. One primary concern is the volatility of raw material prices, particularly crude oil, which directly impacts the cost of base oils and additives. Fluctuations in these prices can compress profit margins for manufacturers and lead to price instability for end-users. Additionally, increasingly stringent environmental regulations, aimed at reducing emissions and promoting sustainability, impose higher compliance costs on lubricant producers, requiring significant investments in research and development for eco-friendlier formulations and sustainable manufacturing processes.

The rapid electrification of the global automotive fleet represents a long-term structural restraint. As electric vehicles (EVs) require significantly less engine oil and different types of specialized fluids compared to traditional internal combustion engine vehicles, the overall volume demand for conventional automotive lubricants is projected to decline over time. Furthermore, the economic slowdowns and geopolitical instabilities can negatively impact industrial output and automotive sales, thereby reducing the demand for lubricants. These factors combined create a complex environment that demands adaptability and innovation from market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Crude Oil) | -0.5% | Global | Short-medium term |

| Increasing Adoption of Electric Vehicles (EVs) | -0.4% | Global, especially Developed Economies | Long-term |

| Strict Environmental Regulations and Compliance Costs | -0.3% | Europe, North America, China | Long-term |

| Economic Slowdowns and Industrial Production Fluctuations | -0.2% | Global | Short-medium term |

| Extended Drain Intervals of Modern Lubricants | -0.1% | Global | Medium-long term |

Finished Lubricant Market Opportunities Analysis

Significant opportunities are emerging within the Finished Lubricant market, driven by technological advancements, sustainability mandates, and the untapped potential of developing economies. The growing emphasis on environmental sustainability is creating a strong market for bio-based and biodegradable lubricants, particularly in environmentally sensitive applications such as marine, agriculture, and forestry. These products offer a compelling alternative to conventional mineral oil-based lubricants, aligning with global green initiatives and consumer preferences.

Moreover, the continuous innovation in synthetic lubricants, designed for extreme operating conditions and specialized industrial applications (e.g., wind turbines, robotics, high-speed manufacturing), presents substantial growth avenues. These high-performance lubricants command premium prices and offer competitive advantages through enhanced efficiency and prolonged equipment life. The expanding industrial and automotive sectors in emerging economies, coupled with increasing disposable incomes and vehicle ownership, represent vast and relatively underserved markets for both conventional and advanced lubricants. Furthermore, the adoption of Industry 4.0 technologies, such as IoT and AI, opens opportunities for data-driven service offerings, predictive maintenance solutions, and customized lubricant formulations, transforming the traditional product-centric market into a more service-oriented ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Bio-based and Sustainable Lubricants | +0.8% | Europe, North America, Asia Pacific | Long-term |

| Growth in Specialty and High-Performance Synthetic Lubricants | +0.7% | Global | Long-term |

| Expansion in Emerging Economies (Industrial & Automotive) | +0.6% | Asia Pacific, Latin America, Africa | Long-term |

| Development of E-fluids for Electric Vehicle Applications | +0.5% | Global | Medium-long term |

| Integration of Digitalization and IoT for Value-Added Services | +0.4% | Developed Economies | Medium-long term |

Finished Lubricant Market Challenges Impact Analysis

The Finished Lubricant market is confronted by several complex challenges that necessitate strategic adaptation and innovation from market participants. A significant hurdle is the ongoing pressure to transition towards more sustainable and environmentally friendly products. This requires substantial investments in research and development to formulate lubricants with reduced environmental impact, often without compromising performance, and to comply with evolving global regulations, which can be costly and time-consuming. The rise of electric vehicles poses a unique long-term challenge, as it fundamentally alters the demand profile for traditional automotive lubricants, requiring manufacturers to pivot towards new e-fluid technologies or expand into non-automotive segments.

Intense market competition, characterized by numerous global and regional players, leads to price pressures and necessitates continuous differentiation through product innovation or service excellence. Furthermore, ensuring a resilient and efficient supply chain amidst geopolitical uncertainties and logistics disruptions remains a persistent challenge, impacting raw material availability and delivery timelines. Addressing these challenges effectively requires a proactive approach to R&D, strategic diversification, and robust supply chain management to maintain competitiveness and profitability in a rapidly evolving market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Navigating the Shift to Sustainable Formulations | -0.6% | Global | Long-term |

| Disruption from Electric Vehicle Adoption | -0.5% | Global | Long-term |

| Intense Market Competition and Price Pressures | -0.4% | Global | Ongoing |

| Supply Chain Volatility and Raw Material Sourcing | -0.3% | Global | Short-medium term |

| Managing Product Obsolescence and Innovation Pace | -0.2% | Global | Medium-long term |

Finished Lubricant Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Finished Lubricant market, covering historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges, leveraging robust methodologies and extensive primary and secondary research. The scope encompasses detailed segmentation across various types, applications, and end-use industries, offering a granular view of market trends and competitive landscapes. Furthermore, regional analyses highlight key market performance and growth prospects across major geographical segments, providing a holistic understanding for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.8 Billion |

| Market Forecast in 2033 | USD 95.1 Billion |

| Growth Rate | 4.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shell plc, Exxon Mobil Corporation, BP p.l.c., Chevron Corporation, TotalEnergies SE, Valvoline Inc., Idemitsu Kosan Co. Ltd., Sinopec Group, PetroChina Company Limited, Fuchs Petrolub SE, Castrol (A BP Brand), Repsol S.A., Lukoil, Phillips 66 Company, Amsoil Inc., Quaker Houghton, PETRONAS Lubricants International, Indian Oil Corporation Ltd., JXTG Nippon Oil & Energy Corporation, Pertamina |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Finished Lubricant market is meticulously segmented to provide a comprehensive understanding of its diverse components and drivers. These segmentations allow for a granular analysis of market dynamics, identifying growth pockets and specific industry needs. The primary segmentation categories include the type of lubricant, the application area where it is utilized, and the specific end-use industry that consumes the product. Each segment plays a crucial role in shaping the overall market landscape, driven by unique performance requirements, regulatory mandates, and technological advancements.

Analyzing these segments helps stakeholders understand consumer preferences, identify niche markets, and tailor product development strategies. For instance, the transition within the 'Type' segment towards synthetic and bio-based lubricants reflects environmental consciousness and performance demands, while the 'Application' and 'End-Use Industry' segments highlight the vast and varied requirements ranging from automotive engines to complex industrial machinery and specialized aerospace components. This detailed breakdown ensures a complete market perspective, crucial for competitive positioning and strategic planning.

- By Type:

- Mineral Oil Lubricants

- Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-based Lubricants

- By Application:

- Automotive

- Engine Oil

- Transmission Fluids

- Brake Fluids

- Greases

- Others

- Industrial

- Hydraulic Fluids

- Metalworking Fluids

- Compressor Oils

- Gear Oils

- Turbine Oils

- Greases

- Process Oils

- Others

- Automotive

- By End-Use Industry:

- Automotive

- Manufacturing

- Power Generation

- Construction

- Mining

- Marine

- Agriculture

- Aerospace

- Food & Beverages

- Others

Regional Highlights

- Asia Pacific (APAC): Dominates the global Finished Lubricant market in terms of consumption and production, driven by rapid industrialization, robust automotive manufacturing, and infrastructure development in countries like China, India, Japan, and South Korea. This region is also witnessing significant investments in advanced manufacturing and renewable energy, further fueling demand for specialized lubricants.

- North America: Characterized by a mature market with a high demand for high-performance and specialty lubricants. Stringent environmental regulations and a focus on advanced industrial applications, coupled with a robust automotive aftermarket, drive innovation and adoption of synthetic and bio-based products.

- Europe: A leading region for innovation in sustainable and high-quality lubricants due to stringent environmental policies, strong automotive industry (including a growing EV sector), and advanced manufacturing base. There is a strong emphasis on energy efficiency and circular economy principles, boosting the market for eco-friendly and longer-lasting lubricants.

- Latin America: Expected to show steady growth, particularly in automotive and industrial sectors, supported by economic development and increasing vehicle ownership in countries like Brazil and Mexico. The region presents opportunities for both conventional and new-generation lubricants as industrial processes modernize.

- Middle East and Africa (MEA): Emerging as a growth hub, especially driven by expanding industrial activities, construction booms, and increasing fleet sizes in the Middle East, along with developing manufacturing and mining sectors in Africa. Investment in infrastructure and diverse economic development initiatives contribute to rising lubricant demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Finished Lubricant Market.- Shell plc

- Exxon Mobil Corporation

- BP p.l.c.

- Chevron Corporation

- TotalEnergies SE

- Valvoline Inc.

- Idemitsu Kosan Co. Ltd.

- Sinopec Group

- PetroChina Company Limited

- Fuchs Petrolub SE

- Castrol (A BP Brand)

- Repsol S.A.

- Lukoil

- Phillips 66 Company

- Amsoil Inc.

- Quaker Houghton

- PETRONAS Lubricants International

- Indian Oil Corporation Ltd.

- JXTG Nippon Oil & Energy Corporation

- Pertamina

Frequently Asked Questions

What are finished lubricants?

Finished lubricants are oil-based or synthetic fluids specifically formulated with base oils and performance additives to reduce friction, prevent wear, cool components, and protect against corrosion in machinery and engines. They are essential for the smooth and efficient operation of various automotive and industrial equipment.

What drives the finished lubricant market?

Key drivers include global industrialization and manufacturing growth, increasing automotive production, the rising demand for high-performance and specialty lubricants, and stringent environmental regulations promoting fuel efficiency and lower emissions. Technological advancements in machinery also necessitate advanced lubricant solutions.

How do electric vehicles (EVs) impact the lubricant market?

EVs significantly reduce the demand for traditional engine oils used in internal combustion engines. However, they create new opportunities for specialized e-fluids, including thermal management fluids, transmission fluids, and greases tailored for electric drivetrains, battery systems, and electric motors.

What are the key trends in lubricant formulations?

Major trends in lubricant formulations involve a shift towards synthetic and semi-synthetic oils for enhanced performance and extended drain intervals, increasing development of bio-based and biodegradable lubricants for sustainability, and specialized formulations like e-fluids for emerging automotive technologies. Additive technology is also advancing for specific performance enhancements.

Which regions are key for the finished lubricant market?

Asia Pacific is the largest and fastest-growing region due to rapid industrial and automotive expansion. North America and Europe are mature markets focused on high-performance and sustainable lubricants. Latin America and the Middle East & Africa are emerging regions showing strong growth driven by economic development and industrialization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted