Filler Masterbatch Market

Filler Masterbatch Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702734 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

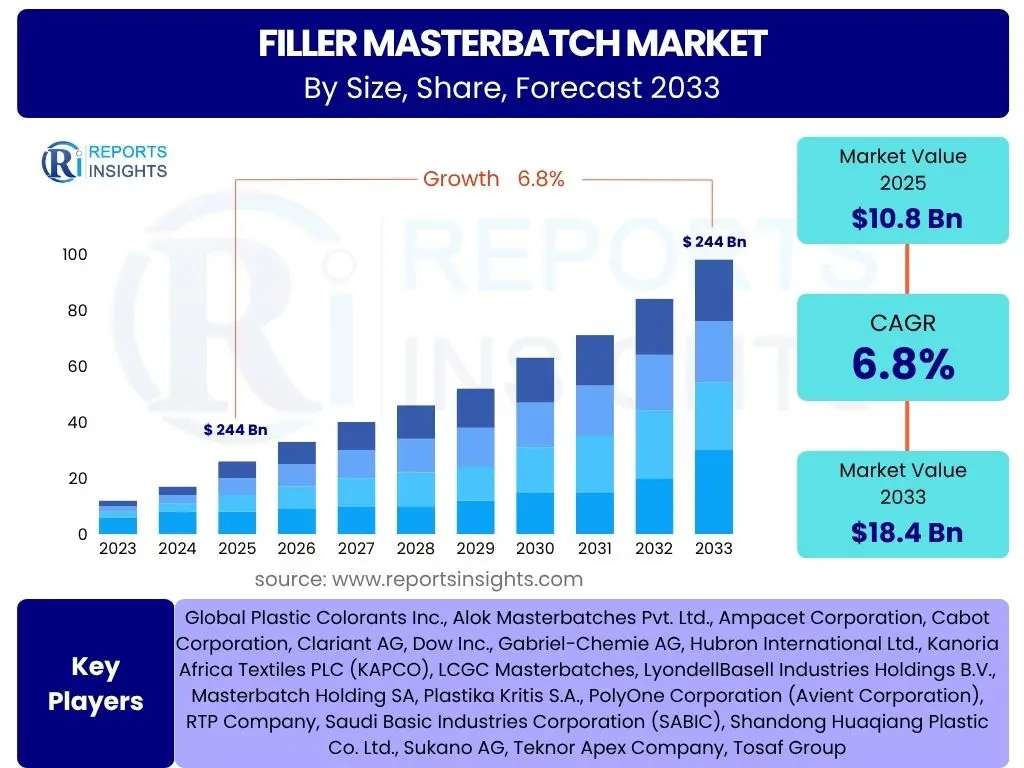

Filler Masterbatch Market Size

According to Reports Insights Consulting Pvt Ltd, The Filler Masterbatch Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 10.8 Billion in 2025 and is projected to reach USD 18.4 Billion by the end of the forecast period in 2033.

Key Filler Masterbatch Market Trends & Insights

The Filler Masterbatch market is experiencing significant evolution driven by several key trends, reflecting the industry's response to demands for sustainability, efficiency, and enhanced product performance. Common inquiries from users often revolve around the adoption of eco-friendly materials, the shift towards lightweighting in various applications, and the increasing demand for cost-effective solutions without compromising quality. These trends highlight a market moving towards innovation in material science and process optimization, aiming to meet both industrial requirements and environmental regulations.

Additionally, insights into the market reveal a strong emphasis on customization and specialty formulations, driven by diverse application needs in packaging, automotive, construction, and consumer goods. Manufacturers are focusing on developing masterbatches that offer specific properties such as improved mechanical strength, better heat resistance, or enhanced UV protection, tailored for specific polymer types and end-use conditions. The integration of advanced manufacturing techniques and the growing importance of regional supply chains also shape the competitive landscape, influencing pricing strategies and market accessibility.

- Increasing adoption of sustainable and recycled content filler masterbatches.

- Growing demand for lightweighting solutions in automotive and packaging industries.

- Technological advancements in nano-fillers and specialty additives.

- Emphasis on cost-effectiveness and process efficiency in manufacturing.

- Expansion of filler masterbatch applications in non-traditional sectors.

- Development of multi-functional filler masterbatches offering combined properties.

- Digitalization and automation in masterbatch production processes.

AI Impact Analysis on Filler Masterbatch

User queries regarding the impact of Artificial Intelligence (AI) on the Filler Masterbatch market frequently touch upon its potential to revolutionize production efficiency, quality control, and supply chain management. The consensus suggests AI could significantly optimize complex manufacturing processes, reduce waste, and enhance product consistency. Concerns often relate to the initial investment required for AI integration and the need for a skilled workforce to manage these advanced systems.

Furthermore, there is keen interest in AI's role in accelerating research and development for new formulations, predicting material performance, and identifying optimal blend ratios, thereby shortening product development cycles. AI-driven predictive maintenance for machinery is also a significant expectation, aiming to minimize downtime and improve operational longevity. While the market is still in the early stages of widespread AI adoption, the overarching expectation is that AI will be a transformative force, leading to more intelligent and adaptive production environments within the filler masterbatch industry.

- Optimization of production parameters and processes for improved yield and quality.

- Enhanced quality control through real-time data analysis and defect prediction.

- Predictive maintenance of machinery, reducing downtime and operational costs.

- Accelerated R&D for new filler masterbatch formulations and material property prediction.

- Supply chain optimization through demand forecasting and logistics management.

- Customization and personalization of masterbatch formulations based on performance data.

Key Takeaways Filler Masterbatch Market Size & Forecast

Common user questions regarding key takeaways from the Filler Masterbatch market size and forecast consistently point to the overall growth trajectory, primary growth drivers, and the most influential market segments. Insights reveal a robust market expansion primarily fueled by the increasing demand for plastics across diverse end-use industries, including packaging, automotive, construction, and consumer goods. The drive for cost efficiency in plastic product manufacturing, coupled with the functional benefits imparted by filler masterbatches such as improved mechanical properties and reduced material usage, underpins this growth.

Furthermore, the forecast indicates a sustained emphasis on innovation in material science, with a growing focus on sustainable and performance-enhancing fillers. Regional growth disparities are also a significant takeaway, with emerging economies in Asia Pacific expected to lead market expansion due to rapid industrialization and urbanization. The competitive landscape is characterized by a mix of established global players and agile regional manufacturers, all striving to offer tailored solutions to meet evolving industry needs and capitalize on market opportunities.

- Significant market growth driven by expanding plastic consumption in diverse sectors.

- Cost reduction and performance enhancement are primary motivations for adoption.

- Asia Pacific is projected to be the fastest-growing region due to industrial expansion.

- Sustainability and bio-based filler masterbatches represent crucial future growth avenues.

- Innovation in functional fillers will differentiate products and capture niche markets.

- The packaging and construction industries remain dominant application areas.

Filler Masterbatch Market Drivers Analysis

The Filler Masterbatch market is significantly driven by the continuous expansion of the plastics processing industry globally, particularly within high-volume sectors such as packaging, automotive, and construction. The inherent ability of filler masterbatches to reduce overall production costs by replacing expensive base polymers with more economical fillers, without significantly compromising product performance, makes them highly attractive. This cost-effectiveness is a major catalyst, especially for manufacturers operating in competitive markets where optimizing material expenses is crucial for profitability.

Moreover, the increasing demand for enhanced material properties in plastic products, such as improved stiffness, dimensional stability, impact strength, and reduced shrinkage, further fuels the adoption of filler masterbatches. These properties are critical for product integrity and performance in diverse applications, from lightweight automotive components to durable construction materials. The ongoing innovation in filler technologies, including the development of specialized and nano-fillers, also contributes to market expansion by enabling new applications and improving existing product characteristics.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Packaging Industry | +1.5% | Global, particularly Asia Pacific & Europe | 2025-2033 |

| Increasing Use in Construction Sector | +1.2% | Asia Pacific, North America | 2025-2033 |

| Cost-Effectiveness & Material Reduction | +1.0% | Global | 2025-2033 |

| Lightweighting Trends in Automotive | +0.8% | Europe, North America, Asia Pacific | 2025-2033 |

Filler Masterbatch Market Restraints Analysis

Despite robust growth drivers, the Filler Masterbatch market faces several notable restraints that could impact its expansion. One significant concern is the volatility in raw material prices, particularly for base polymers and some mineral fillers. Fluctuations in crude oil prices directly affect polymer costs, which in turn influence the pricing and profitability of filler masterbatches, making long-term planning and stable pricing challenging for manufacturers and end-users. This unpredictability can deter new investments and create uncertainties in the supply chain.

Another crucial restraint stems from environmental regulations and increasing public awareness regarding plastic waste and its disposal. Stricter mandates on plastic usage, recycling targets, and the push towards a circular economy can influence the types of fillers permissible and the overall demand for virgin plastic products incorporating masterbatches. While sustainable filler options are emerging, the widespread adoption and regulatory frameworks for their use are still evolving, posing a challenge to conventional filler masterbatch markets. Furthermore, the availability and cost of high-quality recycled polymers as an alternative to virgin plastics can impact the demand for filler masterbatches designed for virgin polymer applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.7% | Global | 2025-2033 |

| Stringent Environmental Regulations | -0.5% | Europe, North America, parts of Asia | 2025-2033 |

| Challenges in Recycling of Filled Plastics | -0.4% | Global | 2025-2033 |

Filler Masterbatch Market Opportunities Analysis

The Filler Masterbatch market is poised for significant opportunities driven by the growing emphasis on sustainability and the increasing demand for specialized, high-performance materials. The development and adoption of bio-based and recycled content filler masterbatches present a major avenue for growth, aligning with global efforts to reduce carbon footprint and promote a circular economy. As consumers and industries increasingly demand eco-friendly products, manufacturers who invest in these sustainable formulations can gain a competitive edge and tap into new market segments, especially in regions with stringent environmental policies.

Furthermore, the continuous innovation in nano-filler technology and the expansion of applications into emerging industries offer lucrative opportunities. Nano-fillers, by virtue of their small particle size, can significantly enhance mechanical, thermal, and barrier properties of plastics at lower loading levels, opening doors for advanced materials in electronics, medical devices, and specialized packaging. The ongoing urbanization and infrastructure development in emerging economies, particularly in Asia Pacific, also create a robust demand for construction and automotive materials, providing fertile ground for market expansion and the introduction of customized filler solutions tailored to regional needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Recycled Filler Masterbatches | +1.1% | Europe, North America, parts of Asia | 2026-2033 |

| Increasing Demand for Nano-fillers & Specialty Formulations | +0.9% | Global, particularly developed markets | 2025-2033 |

| Expansion into Emerging End-use Industries | +0.8% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 |

Filler Masterbatch Market Challenges Impact Analysis

The Filler Masterbatch market faces several challenges that require strategic responses from manufacturers and stakeholders. A primary challenge is the technical complexity associated with achieving consistent dispersion of fillers within the polymer matrix, especially with high loading levels or novel filler types. Poor dispersion can lead to reduced mechanical properties, aesthetic defects, and processing issues, directly impacting product quality and market acceptance. This requires significant investment in advanced compounding technologies and stringent quality control measures, which can be a barrier for smaller players.

Another significant challenge is navigating the evolving regulatory landscape concerning plastics and chemical additives. Governments worldwide are increasingly scrutinizing the environmental impact of plastic products, leading to new regulations on material composition, recyclability, and waste management. Ensuring compliance with these diverse and often region-specific regulations, particularly for masterbatches used in food contact or medical applications, adds considerable complexity and cost to product development and market entry. Furthermore, the integration of filler masterbatches into circular economy models presents a substantial challenge, as traditional fillers can complicate the recycling process of plastic products, necessitating innovation in separable or compatible filler solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Challenges in Filler Dispersion | -0.6% | Global | 2025-2033 |

| Evolving Regulatory Landscape & Compliance | -0.5% | Europe, North America, select Asian countries | 2025-2033 |

| Integration into Circular Economy Models | -0.4% | Global | 2026-2033 |

Filler Masterbatch Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Filler Masterbatch market, offering an updated scope that captures the latest trends, technological advancements, and market shifts. It provides a detailed analysis of market size, growth projections, key drivers, restraints, opportunities, and challenges influencing the industry's trajectory from 2025 to 2033. The report segments the market extensively by various types of fillers, polymer types, applications, and end-use industries, providing a granular view of market performance and potential.

Moreover, the scope includes an in-depth regional analysis, highlighting growth hotspots and market specifics across North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. A dedicated section on the impact of Artificial Intelligence offers forward-looking insights into how digital transformation is shaping the future of masterbatch manufacturing and R&D. The report also profiles leading market players, offering competitive intelligence and a comprehensive understanding of the strategic landscape, making it an invaluable resource for stakeholders seeking actionable market insights.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.8 Billion |

| Market Forecast in 2033 | USD 18.4 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Plastic Colorants Inc., Alok Masterbatches Pvt. Ltd., Ampacet Corporation, Cabot Corporation, Clariant AG, Dow Inc., Gabriel-Chemie AG, Hubron International Ltd., Kanoria Africa Textiles PLC (KAPCO), LCGC Masterbatches, LyondellBasell Industries Holdings B.V., Masterbatch Holding SA, Plastika Kritis S.A., PolyOne Corporation (Avient Corporation), RTP Company, Saudi Basic Industries Corporation (SABIC), Shandong Huaqiang Plastic Co. Ltd., Sukano AG, Teknor Apex Company, Tosaf Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Filler Masterbatch market is meticulously segmented to provide a comprehensive understanding of its diverse components and their respective market dynamics. This segmentation facilitates a granular analysis of product types, their compatibility with various polymers, and their widespread application across different manufacturing processes and end-use industries. Such a detailed breakdown enables stakeholders to identify high-growth areas, understand competitive positioning, and tailor their strategies to specific market niches. The market's complexity is best understood through these specific categories, which highlight both established and emerging product functionalities and applications.

Analyzing these segments reveals that calcium carbonate and talc filler masterbatches dominate the market due to their cost-effectiveness and versatile performance in various plastic products. The packaging and construction industries consistently represent the largest end-use segments, driven by their high volume consumption of plastics. The rise of specialty fillers, such as nano-fillers and those designed for enhanced sustainability, signifies a shift towards value-added products and addresses evolving industry demands for improved material properties and environmental compliance across the identified polymer types and applications.

- By Type: Calcium Carbonate Filler Masterbatch, Talc Filler Masterbatch, Barium Sulfate Filler Masterbatch, Mica Filler Masterbatch, Wollastonite Filler Masterbatch, Glass Fiber Filler Masterbatch, Other Filler Masterbatches

- By Polymer Type: Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), Acrylonitrile Butadiene Styrene (ABS), Polyethylene Terephthalate (PET), Other Polymers

- By Application: Film & Sheet, Injection Molding, Blow Molding, Extrusion, Rotational Molding, Other Applications

- By End-use Industry: Packaging (Flexible Packaging, Rigid Packaging), Automotive, Building & Construction, Consumer Goods, Agriculture, Textile, Electrical & Electronics, Others

Regional Highlights

- Asia Pacific: Expected to be the largest and fastest-growing market, driven by rapid industrialization, urbanization, and a booming manufacturing sector in countries like China, India, and Southeast Asian nations. High demand from packaging, construction, and automotive industries contributes significantly.

- Europe: Characterized by stringent environmental regulations and a strong focus on sustainability. The region shows increasing adoption of recycled and bio-based filler masterbatches. Germany, Italy, and France are key markets, with demand from packaging, automotive, and consumer goods.

- North America: A mature market with steady growth, primarily influenced by the automotive, packaging, and construction sectors. Innovation in advanced materials and lightweighting solutions is a key trend. The United States is the dominant market within this region.

- Latin America: Emerging market with growing potential, influenced by expanding industrial bases and infrastructure development, particularly in Brazil and Mexico. Demand for packaging and construction materials is a major driver.

- Middle East and Africa (MEA): Exhibiting nascent but promising growth, driven by increasing construction activities, packaging industry expansion, and diversification of economies in the GCC countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Filler Masterbatch Market.- Global Plastic Colorants Inc.

- Alok Masterbatches Pvt. Ltd.

- Ampacet Corporation

- Cabot Corporation

- Clariant AG

- Dow Inc.

- Gabriel-Chemie AG

- Hubron International Ltd.

- Kanoria Africa Textiles PLC (KAPCO)

- LCGC Masterbatches

- LyondellBasell Industries Holdings B.V.

- Masterbatch Holding SA

- Plastika Kritis S.A.

- PolyOne Corporation (Avient Corporation)

- RTP Company

- Saudi Basic Industries Corporation (SABIC)

- Shandong Huaqiang Plastic Co. Ltd.

- Sukano AG

- Teknor Apex Company

- Tosaf Group

Frequently Asked Questions

What is filler masterbatch and its primary use?

Filler masterbatch is a concentrated mixture of inorganic fillers like calcium carbonate or talc, dispersed in a polymer carrier. Its primary use is to reduce production costs of plastic products by replacing a portion of the more expensive base polymer, while also enhancing specific properties such as stiffness, dimensional stability, and opacity.

Which industries are the largest consumers of filler masterbatch?

The largest consumers of filler masterbatch are typically the packaging industry, followed by the building and construction, and automotive sectors. These industries extensively use plastics for various applications where cost-efficiency and specific material properties imparted by fillers are crucial.

What are the key drivers for the growth of the filler masterbatch market?

Key drivers include the growing demand for cost-effective plastic solutions, the expansion of the packaging, construction, and automotive industries, and the increasing need for enhanced mechanical properties in plastic products. The trend towards lightweighting and material optimization also contributes significantly.

How do environmental regulations impact the filler masterbatch market?

Environmental regulations increasingly impact the market by encouraging the use of sustainable and recycled content fillers, and by placing pressure on the recyclability of end products. This drives innovation towards more eco-friendly filler masterbatch formulations and can influence the types of fillers permissible in certain applications.

What role does Asia Pacific play in the global filler masterbatch market?

Asia Pacific plays a dominant role and is projected to be the fastest-growing region in the global filler masterbatch market. This is due to rapid industrialization, extensive growth in manufacturing, and increasing demand for plastics in packaging, automotive, and construction sectors across countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted