Plastic Filler Market

Plastic Filler Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704072 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Plastic Filler Market Size

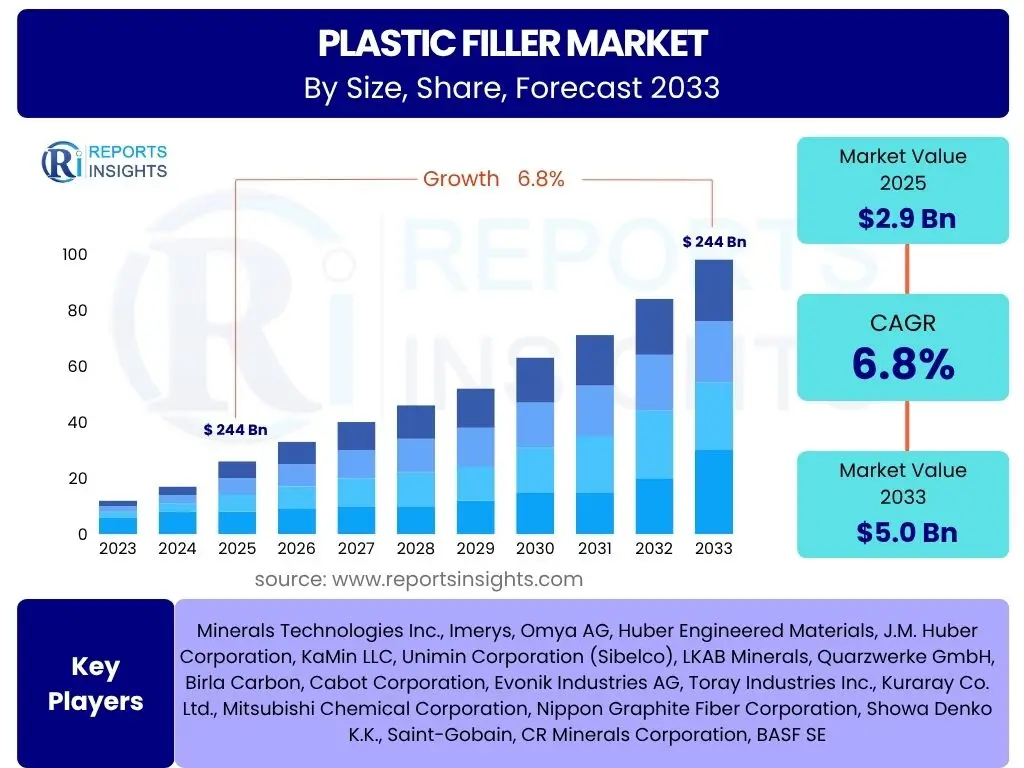

According to Reports Insights Consulting Pvt Ltd, The Plastic Filler Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.9 Billion in 2025 and is projected to reach USD 5.0 Billion by the end of the forecast period in 2033.

Key Plastic Filler Market Trends & Insights

The plastic filler market is undergoing significant transformation, driven by evolving industry demands and a heightened focus on sustainability. Common user inquiries often revolve around the adoption of eco-friendly filler materials, the increasing demand for lightweight and high-performance plastics, and the integration of advanced functional properties. Industry stakeholders are keenly observing how regulations, consumer preferences, and technological advancements are shaping the material landscape, pushing for innovations that balance cost-effectiveness with environmental responsibility and enhanced product attributes.

A prominent trend is the strong emphasis on sustainable solutions, leading to increased research and development in bio-based and recycled fillers. This aligns with global efforts to reduce plastic waste and carbon footprints, offering opportunities for manufacturers to differentiate their products. Furthermore, the automotive and aerospace industries are continuously seeking materials that contribute to vehicle lightweighting, driving the demand for high-strength, low-density fillers. This pursuit of efficiency and performance is not only about fuel economy but also about improving the durability and mechanical properties of plastic components across various applications.

Another significant insight points to the growing demand for multi-functional fillers that can impart properties beyond mere volume reduction, such as flame retardancy, electrical conductivity, or improved thermal stability. This shift reflects a move towards value-added materials that can enhance the overall performance and application range of plastic products. The market is also witnessing a regional divergence in trends, with Asia Pacific leading in consumption due to burgeoning manufacturing, while North America and Europe prioritize innovation and regulatory compliance for advanced and sustainable filler solutions.

- Increased adoption of bio-based and recycled plastic fillers.

- Rising demand for lightweight and high-performance filler solutions in automotive and aerospace sectors.

- Growing focus on multi-functional fillers imparting properties like flame retardancy and electrical conductivity.

- Technological advancements in surface modification and nanoparticle integration for enhanced dispersion.

- Stringent environmental regulations driving the shift towards sustainable and non-toxic filler alternatives.

AI Impact Analysis on Plastic Filler

Common user questions regarding AI's impact on the plastic filler sector frequently explore its potential to revolutionize material discovery, optimize manufacturing processes, and enhance quality control. There is significant interest in how artificial intelligence can accelerate the development of novel filler materials with precise properties, predicting their performance before extensive physical testing. Users also inquire about AI's role in improving the efficiency of existing production lines, from raw material handling to final product extrusion, and its capacity to ensure consistent quality standards throughout the supply chain.

AI is poised to transform the research and development lifecycle for plastic fillers, enabling computational materials design and high-throughput screening. Machine learning algorithms can analyze vast datasets of material properties, processing conditions, and performance outcomes, identifying optimal filler formulations and predicting their behavior under various stresses. This predictive capability significantly reduces the time and cost associated with traditional experimental methods, allowing for faster innovation cycles and the development of custom-tailored filler solutions for specific applications.

Furthermore, within manufacturing, AI-powered systems can optimize real-time process parameters, predict equipment failures through predictive maintenance, and enhance quality assurance through automated defect detection. By analyzing sensor data from production lines, AI can identify subtle deviations that might lead to inconsistencies in material properties, ensuring a higher level of product uniformity and reducing waste. The integration of AI in supply chain management also offers opportunities for improved demand forecasting, inventory optimization, and more efficient logistics, leading to overall operational cost reductions and enhanced market responsiveness for plastic filler manufacturers.

- Accelerated material discovery and design through AI-driven simulations and predictive modeling.

- Optimized manufacturing processes leading to reduced energy consumption and improved yield.

- Enhanced quality control and defect detection via AI-powered vision systems and real-time data analysis.

- Predictive maintenance for production machinery, minimizing downtime and operational costs.

- Improved supply chain efficiency and logistics through AI-driven demand forecasting and inventory management.

Key Takeaways Plastic Filler Market Size & Forecast

Analysis of common user questions regarding the plastic filler market size and forecast reveals a consistent focus on understanding the primary drivers behind its projected growth and the regions poised for the most significant expansion. Users are particularly interested in how macro-economic factors, technological advancements, and evolving regulatory landscapes contribute to the market's trajectory. Insights often highlight the interplay between increasing plastic consumption across diverse industries and the imperative for cost-effective material solutions that also meet performance and sustainability benchmarks.

A key takeaway from the market forecast is the sustained growth driven by the expansion of end-use industries such as packaging, automotive, and construction, particularly in emerging economies. The inherent advantages of plastic fillers, including their ability to reduce material costs, enhance mechanical properties, and improve processing efficiency, continue to make them indispensable components in various plastic formulations. This fundamental utility ensures a steady demand, even amidst shifts in material preferences and environmental scrutiny.

Furthermore, the forecast underscores the pivotal role of Asia Pacific as the leading and fastest-growing region, fueled by rapid industrialization and escalating production capacities. While North America and Europe demonstrate mature markets, their growth is propelled by innovation in specialty and sustainable fillers, adhering to stricter environmental mandates. The overall market trajectory points towards continued innovation in filler types and applications, with a strong emphasis on balancing economic benefits with environmental responsibility, making strategic investments in research and development crucial for long-term success.

- Consistent market expansion driven by sustained demand from packaging, automotive, and construction sectors.

- Asia Pacific remains the dominant and fastest-growing regional market due to industrial development.

- Innovation in specialty and sustainable fillers is crucial for growth in mature markets.

- Cost-effectiveness and performance enhancement remain primary drivers for filler adoption.

- Strategic focus on bio-based and recycled content will be vital for future market positioning.

Plastic Filler Market Drivers Analysis

The plastic filler market is primarily driven by the expanding demand for plastics across various end-use industries, including packaging, automotive, construction, and electronics. Fillers offer a cost-effective solution to modify and enhance the properties of plastics, making them suitable for a broader range of applications while simultaneously reducing overall material costs. This economic advantage, coupled with the functional benefits fillers impart, serves as a fundamental growth catalyst for the market.

The increasing emphasis on lightweighting, particularly in the automotive and aerospace industries, is another significant driver. Fillers such as glass fibers, carbon fibers, and certain mineral fillers can significantly reduce the weight of plastic components without compromising mechanical strength, leading to improved fuel efficiency and reduced emissions. This trend aligns with global sustainability goals and regulatory pressures for cleaner transportation, creating a sustained demand for performance-enhancing fillers.

Moreover, the growing need for improved material performance, such as enhanced stiffness, impact resistance, heat deflection temperature, and dimensional stability, fuels the adoption of various specialized fillers. As product design becomes more complex and demanding, manufacturers rely on fillers to achieve precise material specifications. The versatility of fillers in tailoring plastic properties ensures their continued relevance and integration into new product developments and material advancements across diverse sectors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from End-Use Industries (Packaging, Construction, Automotive) | +2.5% | Global, particularly Asia Pacific (China, India), North America, Europe | Short to Long Term |

| Growing Focus on Lightweighting in Automotive and Aerospace | +1.8% | North America, Europe, Japan, South Korea, China | Mid to Long Term |

| Cost Reduction and Performance Enhancement of Plastics | +1.5% | Global | Short to Mid Term |

| Technological Advancements in Filler Materials | +1.0% | North America, Europe, Japan | Mid to Long Term |

| Rise in Construction Activities and Infrastructure Development | +0.8% | Asia Pacific (Southeast Asia), Middle East & Africa | Short to Mid Term |

Plastic Filler Market Restraints Analysis

The plastic filler market faces significant restraints primarily due to increasingly stringent environmental regulations concerning plastic waste and material sustainability. Governments and regulatory bodies worldwide are implementing policies that restrict the use of certain synthetic materials, promote recycling, and favor bio-based or biodegradable alternatives. This regulatory pressure can limit the growth of conventional plastic fillers and necessitate significant investment in eco-friendly alternatives, posing a challenge for manufacturers.

Volatility in raw material prices, particularly for minerals and chemicals used in filler production, represents another notable restraint. Fluctuations in the cost of energy, mining operations, and transportation can directly impact the production costs of fillers, leading to unstable profit margins for manufacturers and potentially higher prices for end-users. Such unpredictability can deter investment and slow down market expansion, especially in price-sensitive applications.

Furthermore, the availability and growing adoption of alternative materials, such as advanced polymers or composites that might require fewer or different types of fillers, can restrain market growth. While fillers offer benefits, some applications may opt for inherently superior polymers or lightweight designs that circumvent the need for extensive filler incorporation. Technical challenges related to filler dispersion and compatibility with various polymer matrices also exist, which can impact the quality and performance of the final plastic product, leading to adoption barriers in certain specialized applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Policies on Plastic Use | -1.2% | Europe, North America, Japan, China | Mid to Long Term |

| Volatility in Raw Material Prices (Minerals, Chemicals) | -0.8% | Global | Short to Mid Term |

| Availability of Alternative Materials and Technologies | -0.5% | Global | Mid Term |

| Technical Challenges in Filler Dispersion and Polymer Compatibility | -0.3% | Global | Short to Mid Term |

Plastic Filler Market Opportunities Analysis

The plastic filler market is presented with significant opportunities, particularly in the realm of sustainable and bio-based filler materials. With growing environmental consciousness and stringent regulations, there is a surging demand for fillers derived from natural resources or recycled content. This shift provides manufacturers with an avenue to innovate and develop eco-friendly solutions that align with the principles of circular economy, opening new market segments and attracting environmentally conscious consumers and businesses.

Advancements in nanotechnology and the development of specialty fillers offer another substantial opportunity. Nanofillers, such as carbon nanotubes, graphene, and nanoclays, can impart superior mechanical, thermal, and electrical properties to plastics at very low loading levels, creating high-performance composite materials. These advanced fillers enable the creation of lightweight, stronger, and more functional plastics for demanding applications in electronics, medical devices, and aerospace, driving premium market growth.

Furthermore, the rapid industrialization and urbanization in emerging economies, particularly in Asia Pacific, Latin America, and the Middle East, present immense growth opportunities. These regions are experiencing booming construction activities, expanding automotive production, and increasing consumer goods manufacturing, all of which fuel the demand for plastics and, consequently, plastic fillers. Localized production and tailored product offerings for these markets can unlock significant revenue streams and allow companies to capitalize on regional growth dynamics.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Bio-based and Sustainable Fillers | +1.5% | Europe, North America, Asia Pacific | Mid to Long Term |

| Technological Advancements in Nanofillers and Specialty Fillers | +1.2% | North America, Europe, Japan, South Korea | Mid to Long Term |

| Untapped Potential in Emerging Economies and Developing Countries | +1.0% | Asia Pacific (China, India, Southeast Asia), Latin America, MEA | Short to Mid Term |

| Increased Adoption in Electrical & Electronics and Medical Applications | +0.7% | Global | Mid Term |

| Circular Economy Initiatives and Recycling Technologies | +0.5% | Europe, North America | Long Term |

Plastic Filler Market Challenges Impact Analysis

The plastic filler market faces significant challenges due to the increasing stringency of environmental policies and public scrutiny regarding plastic production and disposal. Regulations on plastic additives, microplastics, and overall plastic waste management compel filler manufacturers to invest heavily in research and development for more sustainable and environmentally benign products. Compliance with diverse global and regional environmental standards adds complexity and cost to operations, potentially slowing market expansion in certain segments.

Technical complexities in achieving optimal filler dispersion and compatibility within various polymer matrices also pose a persistent challenge. Poor dispersion can lead to reduced mechanical properties, processing difficulties, and aesthetic issues in the final plastic product. Developing universal or highly adaptable surface modification techniques for fillers across a wide range of polymers is a continuous area of research and represents a hurdle for achieving widespread adoption in high-performance applications without compromising quality.

Furthermore, supply chain disruptions, influenced by geopolitical events, trade barriers, and natural disasters, can significantly impact the availability and cost of raw materials for filler production. The global nature of raw material sourcing means that localized events can have cascading effects on supply chains, leading to price volatility and potential shortages. This unpredictability necessitates robust supply chain management strategies and diversification of sourcing, adding another layer of complexity for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Landscape and Environmental Concerns | -1.0% | Global, particularly Europe, North America | Mid to Long Term |

| Technical Difficulties in Achieving Optimal Filler Dispersion | -0.7% | Global | Short to Mid Term |

| Volatility of Raw Material Costs and Supply Chain Disruptions | -0.6% | Global | Short Term |

| Competition from Alternative Materials or Design Solutions | -0.4% | Global | Mid Term |

Plastic Filler Market - Updated Report Scope

This market research report offers an in-depth analysis of the plastic filler market, providing a comprehensive overview of its current state, historical performance, and future growth projections. The scope encompasses detailed segmentation by filler type, polymer type, and end-use industry, along with a thorough regional analysis. It aims to provide stakeholders with actionable insights into market dynamics, including drivers, restraints, opportunities, and challenges, enabling informed strategic decision-making and identification of key investment areas within the plastic filler value chain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.9 Billion |

| Market Forecast in 2033 | USD 5.0 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Minerals Technologies Inc., Imerys, Omya AG, Huber Engineered Materials, J.M. Huber Corporation, KaMin LLC, Unimin Corporation (Sibelco), LKAB Minerals, Quarzwerke GmbH, Birla Carbon, Cabot Corporation, Evonik Industries AG, Toray Industries Inc., Kuraray Co. Ltd., Mitsubishi Chemical Corporation, Nippon Graphite Fiber Corporation, Showa Denko K.K., Saint-Gobain, CR Minerals Corporation, BASF SE |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The plastic filler market is meticulously segmented to provide a granular understanding of its diverse applications and material compositions. This segmentation is crucial for identifying specific growth pockets, understanding competitive landscapes within niches, and tailoring product development strategies. The market is primarily analyzed across various dimensions including filler type, polymer type, end-use industry, and form, each offering unique insights into market dynamics and consumer preferences.

The segmentation by filler type differentiates between traditional mineral-based fillers such as calcium carbonate, talc, and kaolin, and more advanced materials like glass fibers, carbon fibers, and specialty fillers designed for specific performance enhancements. Each filler type offers distinct properties and cost profiles, influencing their adoption in various plastic formulations. Similarly, segmenting by polymer type, including polypropylene, polyethylene, PVC, and engineering plastics, highlights the specific compatibility and processing requirements of fillers, reflecting the broad range of plastic materials utilized across industries.

Furthermore, segmenting by end-use industry provides a clear picture of the major demand drivers, with packaging, automotive, and building & construction consistently being the largest consumers. This breakdown helps in understanding industry-specific requirements for performance, durability, and cost-efficiency. Finally, the segmentation by form, distinguishing between powder, granules, and fibers, provides insights into processing preferences and the physical characteristics required for effective integration into plastic compounds, enabling a comprehensive market view.

- By Filler Type: Calcium Carbonate, Talc, Kaolin, Mica, Wollastonite, Wood Flour, Glass Fibers, Carbon Fibers, Specialty Fillers, Others.

- By Polymer Type: Polypropylene (PP), Polyethylene (PE), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Polyamide (PA), Engineering Plastics, Others.

- By End-Use Industry: Packaging, Automotive, Building & Construction, Electrical & Electronics, Consumer Goods, Marine, Aerospace, Others.

- By Form: Powder, Granules, Fibers, Others.

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market for plastic fillers, driven by extensive manufacturing capabilities, rapid industrialization, and significant growth in end-use industries like automotive, construction, and packaging, especially in countries such as China, India, and Southeast Asian nations. The region benefits from abundant raw material availability and lower production costs.

- Europe: A mature market characterized by stringent environmental regulations and a strong emphasis on sustainability and circular economy principles. Growth is fueled by the adoption of advanced and bio-based fillers, alongside innovation in high-performance applications in the automotive and electrical and electronics sectors, particularly in Germany, France, and the UK.

- North America: A key market for innovation and specialized plastic fillers, driven by robust automotive, construction, and packaging industries. The region focuses on lightweighting, enhanced performance, and the development of sustainable filler solutions, with significant research and development activities across the United States and Canada.

- Latin America: An emerging market experiencing steady growth due to increasing industrialization, urbanization, and expanding construction and automotive sectors. Brazil and Mexico are leading contributors, presenting opportunities for both conventional and specialty filler adoption as their manufacturing bases develop.

- Middle East and Africa (MEA): Showing nascent but significant growth, primarily driven by infrastructure development, construction boom, and expansion of the packaging industry. The region's rich oil and gas resources also support the petrochemical industry, creating demand for plastic fillers in various applications, particularly in Saudi Arabia, UAE, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Plastic Filler Market.- Minerals Technologies Inc.

- Imerys

- Omya AG

- Huber Engineered Materials

- J.M. Huber Corporation

- KaMin LLC

- Unimin Corporation (Sibelco)

- LKAB Minerals

- Quarzwerke GmbH

- Birla Carbon

- Cabot Corporation

- Evonik Industries AG

- Toray Industries Inc.

- Kuraray Co. Ltd.

- Mitsubishi Chemical Corporation

- Nippon Graphite Fiber Corporation

- Showa Denko K.K.

- Saint-Gobain

- CR Minerals Corporation

- BASF SE

Frequently Asked Questions

What is the current market size of the Plastic Filler Market?

The Plastic Filler Market is estimated at USD 2.9 Billion in 2025.

What is the projected growth rate for the Plastic Filler Market?

The Plastic Filler Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033.

Which factors are primarily driving the Plastic Filler Market?

Key drivers include increasing demand from packaging, automotive, and construction industries, along with the need for cost reduction and performance enhancement in plastic products.

What are the significant trends in the Plastic Filler Market?

Major trends include the rising adoption of sustainable and bio-based fillers, increasing demand for lightweight solutions, and advancements in multifunctional and specialty filler technologies.

Which region holds the largest share in the Plastic Filler Market?

Asia Pacific (APAC) currently holds the largest market share and is projected to be the fastest-growing region, driven by robust industrial and manufacturing growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted