Fill Finish Manufacturing Market

Fill Finish Manufacturing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704282 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Fill Finish Manufacturing Market Size

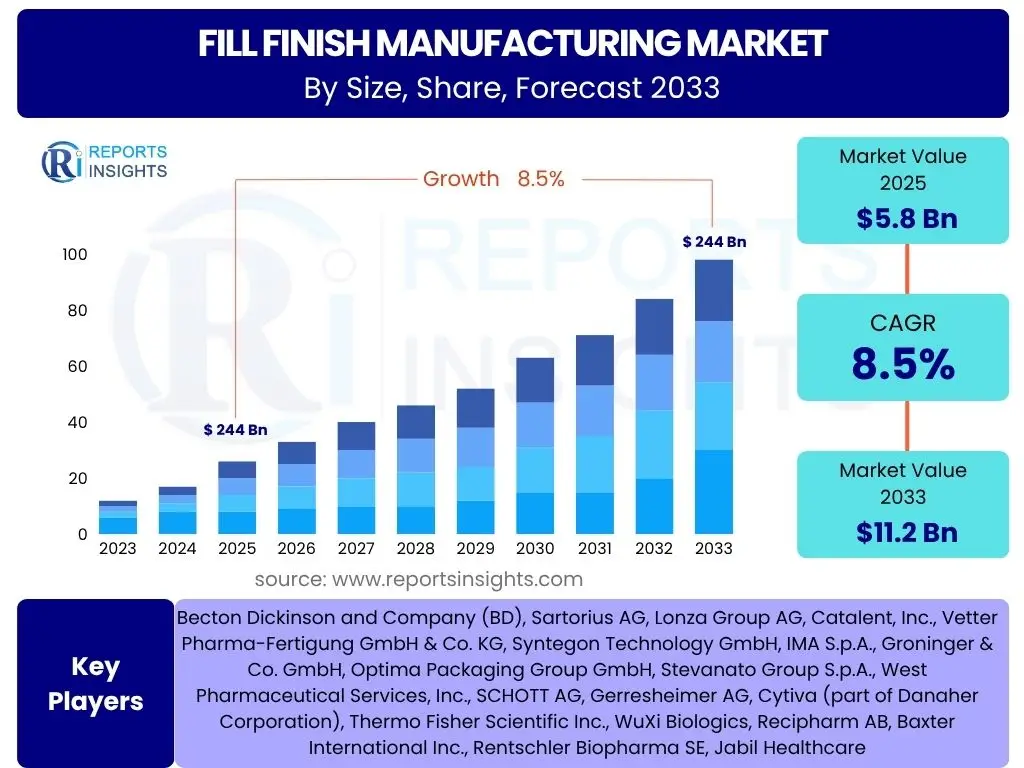

According to Reports Insights Consulting Pvt Ltd, The Fill Finish Manufacturing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 11.2 Billion by the end of the forecast period in 2033.

Key Fill Finish Manufacturing Market Trends & Insights

The Fill Finish Manufacturing market is undergoing significant transformation, driven by an evolving pharmaceutical landscape and advancements in manufacturing technologies. Users frequently inquire about the emerging trends shaping this sector, particularly those related to drug delivery innovation, manufacturing efficiency, and quality assurance. A primary trend observed is the increasing demand for ready-to-use parenteral drug formats, such as pre-filled syringes and cartridges, which offer convenience for both healthcare providers and patients, while also enhancing drug safety by minimizing handling and potential contamination.

Another pivotal trend is the widespread adoption of automation and robotic technologies within fill-finish lines. This shift is aimed at improving throughput, reducing human error, and ensuring higher levels of sterility and precision, especially crucial for sensitive biologic drugs. Furthermore, the market is witnessing a strong emphasis on integrating advanced analytical tools and digitalization to achieve real-time process monitoring and data-driven decision-making, moving towards a more predictive and less reactive manufacturing paradigm. Cold chain management also remains a critical area of focus, especially with the proliferation of temperature-sensitive biologics and vaccines requiring stringent storage conditions.

Beyond technological advancements, sustainability initiatives are gaining traction. Companies are increasingly exploring eco-friendly packaging materials and energy-efficient manufacturing processes to reduce their environmental footprint. The rise of personalized medicine and gene therapies also introduces new complexities and opportunities, necessitating flexible and scalable fill-finish solutions capable of handling smaller batch sizes with high potency products, often requiring specialized aseptic processing capabilities.

- Increased demand for pre-filled syringes and ready-to-use drug formats.

- Rising adoption of automation, robotics, and advanced aseptic processing technologies.

- Integration of digitalization, Industry 4.0 principles, and real-time process monitoring.

- Growing focus on cold chain management for temperature-sensitive biologics.

- Emphasis on sustainable manufacturing practices and eco-friendly packaging solutions.

- Development of flexible and scalable solutions for personalized medicine and smaller batch sizes.

AI Impact Analysis on Fill Finish Manufacturing

Common user questions regarding AI's impact on Fill Finish Manufacturing revolve around its practical applications, benefits in terms of efficiency and quality, and the challenges associated with its implementation. Users are particularly interested in how AI can enhance precision, minimize waste, and improve regulatory compliance. AI's role is increasingly critical in optimizing complex fill-finish processes, offering capabilities that traditional automation alone cannot achieve. It facilitates predictive maintenance for equipment, anticipating failures before they occur and minimizing downtime, a significant concern in high-volume production environments.

Furthermore, AI algorithms are being deployed for advanced quality control, enabling real-time inspection of drug products and packaging components with unprecedented accuracy. This capability helps in detecting minute defects, ensuring product integrity, and reducing costly recalls. AI also plays a vital role in data analysis, transforming vast amounts of operational data into actionable insights for process optimization, batch consistency, and yield improvement. This data-driven approach allows manufacturers to fine-tune their operations, leading to higher efficiency and reduced operational costs.

The integration of AI in fill-finish operations extends to supply chain management, where it can optimize material flow, predict demand fluctuations, and enhance traceability. While the initial investment and the need for specialized skills present implementation challenges, the long-term benefits in terms of enhanced productivity, superior quality, and improved decision-making are compelling. AI is not just an incremental improvement but a transformative technology poised to redefine the standards of sterile manufacturing excellence.

- Optimization of manufacturing processes and equipment parameters.

- Predictive maintenance for fill-finish machinery, reducing downtime.

- Enhanced quality control and real-time defect detection through image recognition.

- Data-driven insights for process improvement and yield optimization.

- Streamlined supply chain management and inventory forecasting.

- Support for regulatory compliance and audit readiness through data integrity.

Key Takeaways Fill Finish Manufacturing Market Size & Forecast

User inquiries about key takeaways from the Fill Finish Manufacturing market size and forecast often focus on the overall growth potential, the primary drivers of this expansion, and the most promising segments for investment or strategic development. The market is positioned for robust growth, underpinned by fundamental shifts in the global pharmaceutical and biopharmaceutical industries. The increasing pipeline of biologics, vaccines, and advanced therapeutic medicinal products (ATMPs) directly correlates with the rising demand for sophisticated fill-finish solutions capable of handling these sensitive and high-value drugs with precision and sterility.

Technological advancements, particularly in automation, robotics, and digitalization, are not merely supporting but actively driving market expansion. These innovations are enabling higher throughput, superior quality, and greater flexibility in manufacturing processes, addressing the evolving needs of drug developers and manufacturers. The trend towards outsourcing fill-finish operations to specialized Contract Development and Manufacturing Organizations (CDMOs) is also a significant factor, as these partners offer expertise, specialized equipment, and economies of scale, allowing pharmaceutical companies to focus on core drug discovery and development.

Geographically, while established markets in North America and Europe continue to innovate and demand high-end solutions, emerging markets in Asia Pacific are demonstrating accelerated growth due to expanding healthcare infrastructure, increasing pharmaceutical production, and a growing patient base. This global demand, combined with an imperative for sterile, safe, and efficient drug delivery, ensures a sustained upward trajectory for the fill-finish manufacturing market throughout the forecast period, presenting considerable opportunities for technology providers, service providers, and drug manufacturers alike.

- The market exhibits strong and sustained growth driven by biopharmaceutical innovation.

- Technological advancements in automation and digitalization are critical growth enablers.

- Outsourcing to CDMOs is a key strategy for market players, enhancing capacity and expertise.

- Increasing demand for pre-filled syringes and other ready-to-use formats fuels segment growth.

- Emerging economies in Asia Pacific are significant contributors to market expansion.

- Focus on aseptic processing and containment solutions for high-potency and sterile drugs.

Fill Finish Manufacturing Market Drivers Analysis

The Fill Finish Manufacturing market is significantly propelled by several intertwined factors that collectively foster its expansion. A primary driver is the accelerating growth of the biopharmaceutical industry, characterized by a burgeoning pipeline of biologics, vaccines, and cell and gene therapies. These complex drug products often require precise aseptic handling and specialized packaging solutions like pre-filled syringes or vials, driving demand for advanced fill-finish technologies that can maintain product integrity and sterility. The inherent sensitivity of these biologics necessitates high-precision filling and robust containment solutions, pushing manufacturers to invest in cutting-edge equipment and processes.

Another crucial driver is the rising global prevalence of chronic and infectious diseases, which continuously increases the demand for effective and safe pharmaceutical treatments. This demographic and epidemiological shift mandates higher production volumes of diverse drug products, necessitating efficient and scalable fill-finish capabilities. Furthermore, the growing preference for self-administration of drugs and the emphasis on patient convenience have fueled the demand for user-friendly drug delivery systems, particularly pre-filled syringes and auto-injectors, which simplify medication adherence and reduce the risk of dosing errors, thereby directly impacting fill-finish requirements.

Technological advancements also play a pivotal role. Innovations in automation, robotics, and smart manufacturing (Industry 4.0) are revolutionizing fill-finish lines, enabling higher throughput, superior accuracy, and reduced human intervention, which minimizes contamination risks. The imperative for enhanced product quality, reduced waste, and adherence to stringent global regulatory standards further encourages the adoption of sophisticated and automated fill-finish solutions. This continuous innovation, coupled with the increasing need for sterile and safe parenteral drug products, ensures a robust growth trajectory for the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Biologics & Biosimilars Market | +2.5% | Global | Long-term |

| Increasing Prevalence of Chronic Diseases | +1.8% | Global | Long-term |

| Advancements in Automation & Robotics | +1.5% | North America, Europe, Asia Pacific | Mid-term |

| Rising Demand for Pre-filled Syringes & Auto-injectors | +1.2% | Global | Mid-term |

| Growing Adoption of Contract Manufacturing Services | +1.0% | Global | Mid-to-Long term |

Fill Finish Manufacturing Market Restraints Analysis

Despite its significant growth potential, the Fill Finish Manufacturing market faces several notable restraints that can impede its expansion. One of the primary challenges is the substantial capital investment required for establishing and upgrading advanced fill-finish lines. High-speed, automated, and aseptic manufacturing facilities demand sophisticated equipment, specialized cleanroom environments, and complex validation processes, translating into significant upfront costs that can be prohibitive for smaller companies or new entrants. This barrier to entry can limit market competition and slow the adoption of the latest technologies across the industry.

Another significant restraint involves the stringent and continuously evolving regulatory landscape. Fill-finish operations are subject to rigorous regulations by bodies such as the FDA, EMA, and other national health authorities, particularly concerning aseptic processing, quality control, and data integrity. Compliance requires substantial ongoing investment in quality management systems, validation, and personnel training, adding complexity and cost to manufacturing processes. Any non-compliance can lead to severe penalties, production halts, and reputational damage, making risk management a critical concern.

Furthermore, the inherent complexity of handling various drug products, especially high-potency APIs, biologics, and cell and gene therapies, presents considerable technical challenges. These products often require highly specialized containment solutions, precise temperature control, and minimal product loss during the filling process. The risk of product contamination, degradation, or interaction with primary packaging materials necessitates meticulous process design and validation, often leading to slower adoption rates for new technologies and higher operational expenditures. Supply chain vulnerabilities, especially for specialized components and raw materials, can also pose a restraint, impacting production schedules and costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment for Advanced Lines | -1.5% | Global | Short-to-Mid term |

| Stringent Regulatory Compliance Requirements | -1.2% | Global | Ongoing | Complexity of Aseptic Processing & Product Handling | -1.0% | Global | Ongoing |

| Risk of Product Loss & Container-Closure Integrity Issues | -0.8% | Global | Ongoing |

| Skilled Workforce Shortage for Specialized Operations | -0.7% | Global | Long-term |

Fill Finish Manufacturing Market Opportunities Analysis

The Fill Finish Manufacturing market is poised for significant opportunities driven by several transformative trends within the pharmaceutical and biotechnology sectors. A paramount opportunity lies in the burgeoning pipeline of innovative biologics, including monoclonal antibodies, gene therapies, and cell therapies. These advanced therapeutic products typically require highly specialized aseptic fill-finish capabilities, often in smaller batch sizes, creating a niche for manufacturers capable of handling high-value, sensitive materials with precision and minimal loss. The increasing complexity and potency of these drugs necessitate next-generation fill-finish solutions that can integrate advanced containment and isolation technologies, offering a lucrative avenue for market participants.

Another compelling opportunity emerges from the growing trend of pharmaceutical companies outsourcing their manufacturing operations to Contract Development and Manufacturing Organizations (CDMOs). As drug development becomes more specialized and capital-intensive, many pharmaceutical firms opt to leverage the expertise, advanced infrastructure, and flexibility offered by CDMOs for their fill-finish needs. This strategic shift allows companies to focus on core R&D while offloading manufacturing complexities, thus presenting substantial growth prospects for CDMOs capable of providing comprehensive and high-quality fill-finish services, particularly those investing in scalable and adaptable technologies.

Furthermore, technological innovation continually opens new avenues. The adoption of single-use systems (SUS) within fill-finish operations offers benefits such as reduced cleaning and sterilization times, minimized cross-contamination risks, and increased flexibility, particularly for multi-product facilities. The integration of advanced analytics, artificial intelligence (AI), and machine learning (ML) for process optimization, predictive maintenance, and enhanced quality control represents a significant opportunity to drive efficiency and reduce operational costs. The expansion into emerging markets, where healthcare infrastructure and pharmaceutical consumption are rapidly growing, also provides untapped potential for companies to establish new manufacturing facilities or partnerships, capitalizing on increasing demand and potentially lower operational costs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Biologics & Advanced Therapies Pipeline | +2.0% | Global | Long-term |

| Increasing Outsourcing to CDMOs | +1.5% | Global | Mid-to-Long term |

| Technological Advancements (AI, Robotics, SUS) | +1.3% | Developed Regions, Emerging APAC | Mid-term |

| Growth in Emerging Pharmaceutical Markets | +1.0% | Asia Pacific, Latin America, MEA | Long-term |

| Demand for Patient-Centric Drug Delivery Systems | +0.8% | Global | Mid-term |

Fill Finish Manufacturing Market Challenges Impact Analysis

The Fill Finish Manufacturing market faces several intricate challenges that demand continuous innovation and strategic adaptation from market participants. A critical challenge revolves around maintaining absolute sterility throughout the filling process, particularly for highly sensitive sterile injectables and biologics. Ensuring aseptic conditions in cleanrooms, preventing microbial contamination, and validating sterilization procedures are complex and resource-intensive tasks. Any breach in sterility can lead to product recalls, significant financial losses, and severe reputational damage, underscoring the constant need for vigilance and advanced aseptic technologies.

Another significant challenge is minimizing product loss and maximizing yield, especially when dealing with high-value or scarce drug substances like gene and cell therapies. The very small batch sizes, coupled with the high cost of these products, make even minor volumetric errors or spills financially impactful. Manufacturers must invest in ultra-precise filling technologies and robust container-closure integrity systems to ensure that every drop of the drug product is effectively utilized and securely contained. This focus on efficiency and waste reduction is paramount for economic viability in an increasingly competitive landscape.

Furthermore, the rapid pace of technological advancements, while an opportunity, also presents a challenge in terms of integration and workforce readiness. Implementing state-of-the-art robotic systems, advanced sensors, and AI-driven analytics requires significant capital investment, specialized technical expertise, and continuous training for personnel. Adapting existing facilities to incorporate these new technologies, ensuring interoperability, and managing the cultural shift towards data-driven manufacturing can be daunting. The global shortage of skilled professionals capable of operating and maintaining these sophisticated systems further exacerbates this challenge, potentially slowing down the adoption of innovative solutions and impacting operational efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Aseptic Conditions & Sterility Assurance | -1.8% | Global | Ongoing |

| Minimizing Product Loss & Maximizing Yield | -1.0% | Global | Ongoing |

| Managing Regulatory Complexity & Compliance | -0.9% | Global | Ongoing |

| Integration of New Technologies & Digitalization | -0.7% | Developed Regions | Mid-term |

| Supply Chain Disruptions for Components & Materials | -0.5% | Global | Short-to-Mid term |

Fill Finish Manufacturing Market - Updated Report Scope

This report provides an in-depth analysis of the Fill Finish Manufacturing market, offering a comprehensive overview of its size, trends, drivers, restraints, opportunities, and challenges. It delves into key market dynamics, technological advancements, and strategic insights to assist stakeholders in making informed decisions. The scope covers various product types, applications, and end-users across key geographical regions, alongside a detailed competitive landscape analysis of leading market players.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 11.2 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Becton Dickinson and Company (BD), Sartorius AG, Lonza Group AG, Catalent, Inc., Vetter Pharma-Fertigung GmbH & Co. KG, Syntegon Technology GmbH, IMA S.p.A., Groninger & Co. GmbH, Optima Packaging Group GmbH, Stevanato Group S.p.A., West Pharmaceutical Services, Inc., SCHOTT AG, Gerresheimer AG, Cytiva (part of Danaher Corporation), Thermo Fisher Scientific Inc., WuXi Biologics, Recipharm AB, Baxter International Inc., Rentschler Biopharma SE, Jabil Healthcare |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fill Finish Manufacturing market is comprehensively segmented to provide granular insights into its diverse components and growth drivers. This segmentation allows for a detailed analysis of market dynamics across different product types, the specific applications they serve, and the various end-user industries that rely on these critical manufacturing services. Understanding these distinct segments is crucial for identifying key growth areas, assessing competitive landscapes, and formulating effective market strategies tailored to specific industry needs and technological requirements.

The segmentation by product type reflects the evolving preferences for drug delivery formats, with pre-filled syringes and cartridges gaining prominence due to convenience and safety benefits, while vials remain essential for multi-dose applications and specific drug formulations. Application-based segmentation highlights the increasing demand driven by the robust pipeline of biologics and advanced therapies, which require specialized handling compared to traditional small molecules. Furthermore, the end-user segmentation differentiates between in-house manufacturing capabilities of pharmaceutical companies and the growing reliance on specialized contract manufacturing organizations (CMOs/CDMOs) for expertise and capacity.

Moreover, the report dissects the market by workflow and service, distinguishing between aseptic and non-aseptic processes, and specialized services like lyophilization, which is critical for stabilizing sensitive biological drugs. The technology/automation level segment provides insights into the adoption rates of manual, semi-automated, automated, and robotic systems, reflecting the industry's drive towards higher efficiency, precision, and reduced human intervention. Each of these segments contributes uniquely to the market's overall growth and innovation trajectory, providing a multi-faceted view of the industry's landscape.

- By Product: Vials, Syringes (Prefilled, Conventional), Cartridges, Bags, Bottles, Ampoules.

- By Application: Vaccines, Monoclonal Antibodies (mAbs), Gene and Cell Therapies, Insulin, Oncology, Pain Management, Anticoagulants, Other Biologics, Small Molecules.

- By End-User: Pharmaceutical and Biopharmaceutical Companies, Contract Manufacturing Organizations (CMOs) / Contract Development and Manufacturing Organizations (CDMOs), Research and Academic Institutes.

- By Workflow/Service: Aseptic Fill Finish, Non-Aseptic Fill Finish, Lyophilization, Liquid Fill Finish.

- By Technology/Automation Level: Manual, Semi-Automated, Automated, Robotic.

Regional Highlights

The Fill Finish Manufacturing market exhibits distinct regional dynamics, influenced by varying levels of pharmaceutical R&D, manufacturing infrastructure, regulatory environments, and healthcare expenditures. North America continues to dominate the market, largely due to its robust biopharmaceutical industry, significant investments in advanced drug delivery systems, and a strong presence of key market players and research institutions. The region benefits from early adoption of cutting-edge technologies like robotics and AI in manufacturing, coupled with a high demand for complex biologics and personalized medicines.

Europe represents another significant market, driven by a well-established pharmaceutical sector, stringent regulatory standards, and a focus on innovative drug development, particularly in countries like Germany, France, and Switzerland. The region is characterized by a strong emphasis on quality and precision in fill-finish operations, with a growing trend towards outsourcing to specialized CDMOs. Continuous investment in upgrading manufacturing facilities to comply with evolving Good Manufacturing Practices (GMP) also fuels market growth here.

Asia Pacific is projected to be the fastest-growing region in the forecast period. This growth is attributable to expanding healthcare infrastructure, increasing pharmaceutical manufacturing capabilities, and a rising prevalence of chronic diseases. Countries like China and India are emerging as major manufacturing hubs, attracting foreign investment and expanding their domestic biopharmaceutical production. Furthermore, improving economic conditions and increasing access to healthcare services in these regions are driving the demand for pharmaceutical products, consequently boosting the fill-finish market. Latin America, the Middle East, and Africa are also showing nascent growth, driven by increasing healthcare spending and efforts to enhance local pharmaceutical production capabilities, although they lag behind more developed regions in terms of technological adoption and market maturity.

- North America: Dominant market share due to robust biopharmaceutical R&D, high adoption of advanced technologies, and significant demand for biologics and specialty drugs.

- Europe: Strong market position driven by established pharmaceutical companies, stringent regulatory frameworks, and increasing investments in advanced manufacturing capabilities.

- Asia Pacific (APAC): Fastest-growing region, fueled by expanding healthcare infrastructure, rising pharmaceutical production, growing patient populations, and increasing outsourcing activities.

- Latin America, Middle East, and Africa (MEA): Emerging markets with growing healthcare expenditure, increasing focus on local drug production, and developing pharmaceutical infrastructure, offering future growth potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fill Finish Manufacturing Market.- Becton Dickinson and Company (BD)

- Sartorius AG

- Lonza Group AG

- Catalent, Inc.

- Vetter Pharma-Fertigung GmbH & Co. KG

- Syntegon Technology GmbH

- IMA S.p.A.

- Groninger & Co. GmbH

- Optima Packaging Group GmbH

- Stevanato Group S.p.A.

- West Pharmaceutical Services, Inc.

- SCHOTT AG

- Gerresheimer AG

- Cytiva (part of Danaher Corporation)

- Thermo Fisher Scientific Inc.

- WuXi Biologics

- Recipharm AB

- Baxter International Inc.

- Rentschler Biopharma SE

- Jabil Healthcare

Frequently Asked Questions

Analyze common user questions about the Fill Finish Manufacturing market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is fill-finish manufacturing?

Fill-finish manufacturing is the final stage in pharmaceutical production where drug products are filled into their primary containers (such as vials, syringes, or cartridges) and then finished (e.g., capped, labeled, inspected) for distribution. This critical process ensures the sterile, safe, and accurate packaging of therapeutic agents.

What are the key drivers of the fill-finish market?

The primary drivers include the expanding pipeline of biologics and biosimilars, increasing prevalence of chronic diseases demanding more pharmaceutical products, rising adoption of pre-filled syringes for patient convenience, and continuous technological advancements in automation and aseptic processing.

How is AI impacting fill-finish operations?

AI is transforming fill-finish operations by enabling predictive maintenance for machinery, enhancing real-time quality control through advanced defect detection, optimizing processes based on data analysis, and improving overall efficiency and consistency in sterile drug manufacturing.

What challenges does the fill-finish market face?

Key challenges include the high capital investment required for advanced facilities, stringent and evolving regulatory compliance, the inherent complexity of maintaining absolute sterility for sensitive drugs, minimizing product loss of high-value compounds, and a shortage of skilled personnel.

What are the main types of fill-finish products?

The main types of fill-finish products encompass vials (for single or multi-dose applications), pre-filled syringes (for convenience and self-administration), cartridges (often used with pen injectors), ampoules, and specialized bags for intravenous solutions or cell therapies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted