Field Erected Cooling Tower Market

Field Erected Cooling Tower Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705899 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

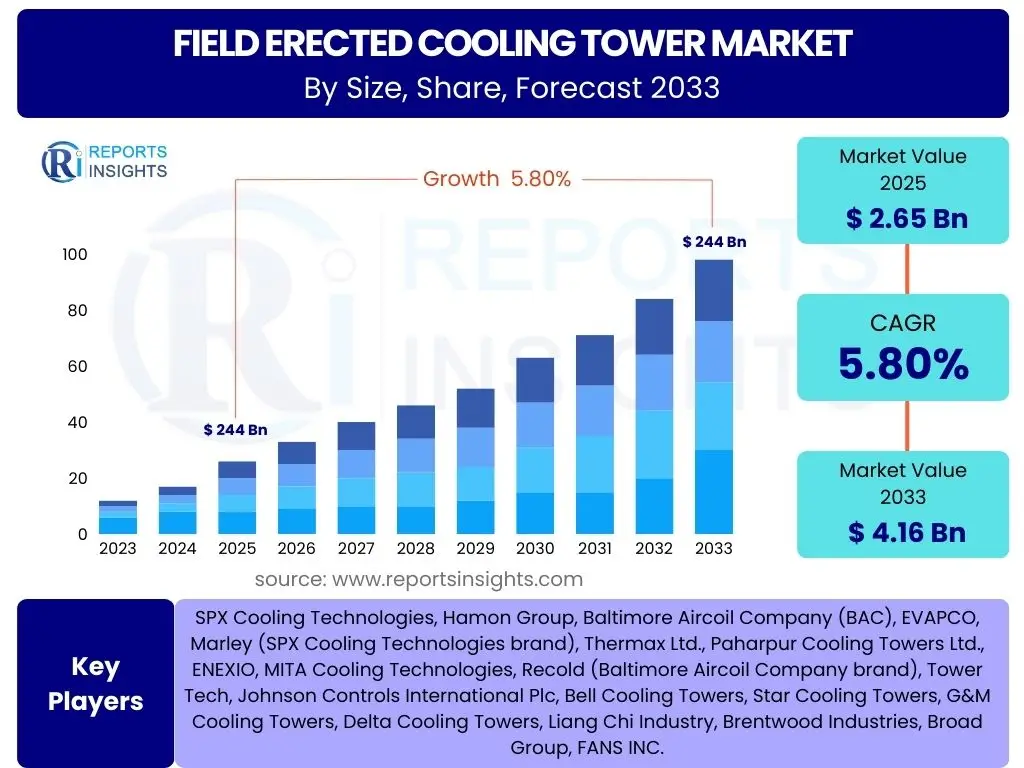

Field Erected Cooling Tower Market Size

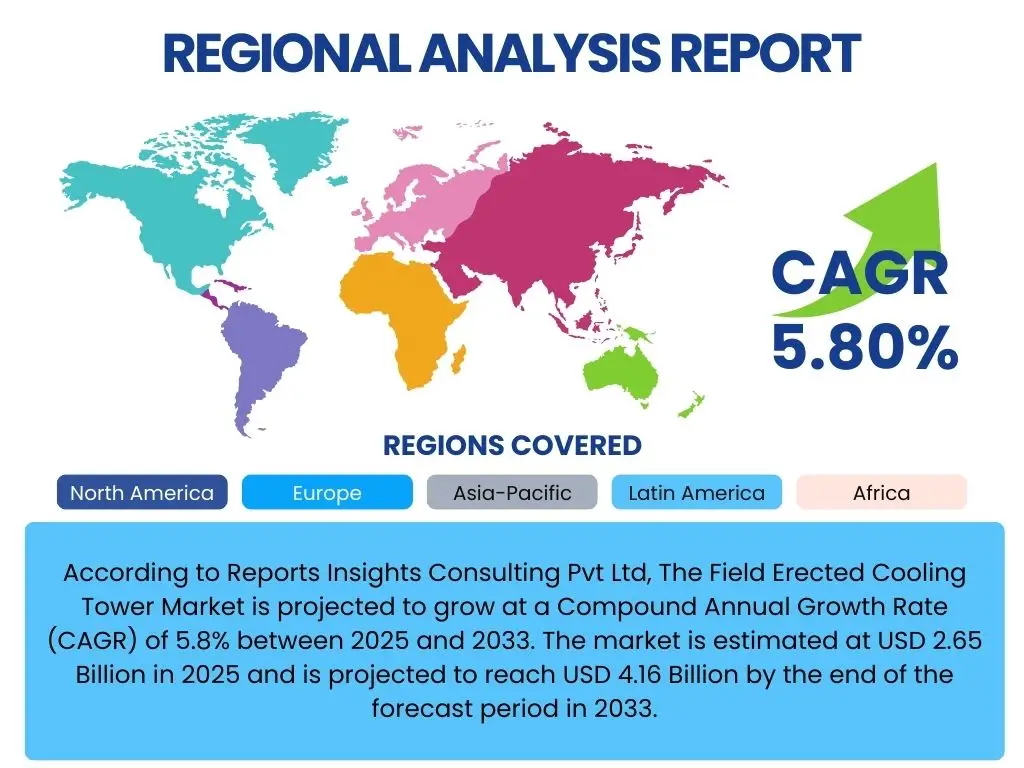

According to Reports Insights Consulting Pvt Ltd, The Field Erected Cooling Tower Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 2.65 Billion in 2025 and is projected to reach USD 4.16 Billion by the end of the forecast period in 2033.

Key Field Erected Cooling Tower Market Trends & Insights

The Field Erected Cooling Tower market is experiencing transformative shifts driven by global sustainability imperatives, technological advancements, and evolving industrial demands. A prominent trend involves the increasing adoption of energy-efficient designs and materials, responding to stricter environmental regulations and rising energy costs. Furthermore, the integration of smart technologies, such as IoT sensors and AI-powered analytics, is gaining momentum, enabling predictive maintenance, optimized performance, and real-time monitoring capabilities. This shift enhances operational efficiency and extends equipment lifespan, reflecting a broader industry move towards digitalization.

Another significant insight pertains to the growing emphasis on water conservation and re-use technologies. As water scarcity becomes a critical global concern, industries are seeking cooling solutions that minimize water consumption through advanced drift eliminators, efficient water treatment systems, and closed-loop designs. The market is also witnessing a surge in demand for hybrid cooling towers that offer flexibility in operation, adapting to varying ambient conditions and load requirements to optimize both water and energy usage. These trends collectively underscore the industry's commitment to environmental responsibility and operational excellence, influencing design, material selection, and overall market dynamics.

- Increased focus on energy efficiency and sustainable designs to reduce operational costs and environmental impact.

- Rising adoption of smart cooling towers with IoT, AI, and data analytics for predictive maintenance and optimized performance.

- Growing demand for water-saving technologies, including advanced drift eliminators and efficient water treatment systems.

- Shift towards modular and hybrid cooling tower designs for enhanced flexibility, easier installation, and reduced downtime.

- Stricter environmental regulations compelling industries to invest in compliant and eco-friendly cooling solutions.

AI Impact Analysis on Field Erected Cooling Tower

The integration of Artificial Intelligence (AI) into Field Erected Cooling Tower operations is a rapidly evolving area, with users keenly interested in its potential to revolutionize efficiency, maintenance, and resource management. Common inquiries revolve around how AI can enhance predictive capabilities, optimize energy consumption, and identify potential failures before they occur. The primary expectation is that AI will move cooling tower management from reactive to proactive, significantly reducing operational costs and unplanned downtime. Users are also concerned with the practicalities of implementation, including data security, integration with existing infrastructure, and the need for specialized skills.

AI's influence is primarily manifested in predictive analytics for equipment health, optimization of fan speeds and water flow based on real-time environmental data, and sophisticated fault detection. By analyzing vast datasets from sensors, AI algorithms can learn operational patterns, detect anomalies indicative of wear or malfunction, and even suggest optimal control parameters to minimize energy and water usage. This not only improves the longevity and reliability of the cooling towers but also contributes significantly to environmental sustainability efforts. While the initial investment and data management challenges are noted, the long-term benefits of enhanced performance, reduced operational expenditure, and improved resource efficiency are driving increasing adoption and research into AI applications in this domain.

- Predictive Maintenance: AI algorithms analyze sensor data (vibration, temperature, flow rates) to predict equipment failure, enabling proactive maintenance and reducing unscheduled downtime.

- Operational Optimization: AI adjusts fan speeds, water flow, and other parameters in real-time based on environmental conditions and load requirements, minimizing energy and water consumption.

- Enhanced Fault Detection: AI systems can quickly identify subtle anomalies that indicate impending issues, allowing for early intervention and preventing major malfunctions.

- Resource Management: AI contributes to more efficient water usage by optimizing blowdown cycles and identifying leakage, promoting sustainability.

- Improved Safety: By providing early warnings of critical issues, AI can help prevent hazardous conditions and improve overall operational safety.

- Reduced Human Intervention: Automation driven by AI can decrease the need for manual monitoring and adjustments, freeing up personnel for more complex tasks.

Key Takeaways Field Erected Cooling Tower Market Size & Forecast

The Field Erected Cooling Tower market is poised for robust growth, driven by an expanding industrial landscape and the increasing global demand for efficient cooling solutions. A key takeaway is the consistent upward trajectory in market size, underscored by significant investments in power generation, chemical processing, and data center infrastructure worldwide. This growth is not merely volumetric but also qualitative, reflecting a strong market inclination towards high-performance, durable, and environmentally compliant cooling systems. The forecast period highlights a sustained demand, particularly from emerging economies, where rapid industrialization and urbanization are fueling new project developments.

Furthermore, technological innovation stands as a pivotal accelerant for this market, with advancements in material science, digital monitoring, and water-saving technologies being crucial. The market is increasingly characterized by a focus on Total Cost of Ownership (TCO) rather than just initial capital expenditure, prompting end-users to seek towers that offer superior energy efficiency and lower maintenance requirements over their lifecycle. The influence of stringent environmental regulations on emissions and water discharge is also a dominant factor, compelling manufacturers to innovate and offer solutions that align with global sustainability goals, thereby shaping the competitive landscape and product development strategies.

- The Field Erected Cooling Tower market demonstrates consistent growth, projected to exceed USD 4 billion by 2033, driven by industrial expansion.

- Significant investments in power generation, HVAC systems, and data centers are primary demand drivers.

- Technological advancements, including smart monitoring and water-saving features, are critical for market competitiveness.

- Emphasis on energy efficiency and reduced operational costs is influencing purchasing decisions and product development.

- Stringent environmental regulations are compelling innovations in sustainable and compliant cooling tower designs.

- Asia Pacific is expected to remain a dominant growth region due to rapid industrialization and infrastructure development.

Field Erected Cooling Tower Market Drivers Analysis

The expansion of the Field Erected Cooling Tower market is fundamentally driven by several interconnected factors that create sustained demand across various industrial sectors. A primary driver is the continuous growth in industrial and commercial sectors globally, necessitating efficient thermal management solutions for manufacturing processes, power generation, and commercial HVAC systems. As economies develop and expand, particularly in emerging markets, new industrial facilities and infrastructure projects inherently require large-scale cooling capabilities, which field erected towers are ideally suited to provide due to their customizable nature and high capacity.

Moreover, the increasing global demand for energy, especially electricity, continues to fuel the construction and expansion of power plants, including thermal, nuclear, and renewable energy facilities, all of which rely heavily on cooling towers for heat dissipation. Concurrently, the burgeoning data center industry, driven by rapid digitalization and cloud computing adoption, represents a significant growth area, as data centers require massive and uninterrupted cooling to maintain optimal operating temperatures for servers. Finally, evolving environmental regulations, while sometimes posing challenges, also act as a driver by compelling industries to upgrade to more efficient, water-conserving, and environmentally compliant cooling technologies, thereby stimulating demand for modern field erected cooling towers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Industrialization & Infrastructure Development | +1.2% | Asia Pacific, Middle East & Africa | Mid-to-Long Term (2025-2033) |

| Rising Global Energy Demand & Power Generation Expansion | +1.0% | Global, particularly APAC and North America | Mid-to-Long Term (2025-2033) |

| Increasing Demand from HVAC & Commercial Sectors | +0.8% | North America, Europe, Asia Pacific | Short-to-Mid Term (2025-2029) |

| Expansion of Data Centers & IT Infrastructure | +0.9% | North America, Europe, Asia Pacific | Short-to-Long Term (2025-2033) |

| Aging Infrastructure & Need for Replacements | +0.7% | Developed Economies (North America, Europe) | Mid-to-Long Term (2027-2033) |

| Stricter Environmental Regulations (Water & Energy Efficiency) | +0.6% | Global | Ongoing |

Field Erected Cooling Tower Market Restraints Analysis

While the Field Erected Cooling Tower market exhibits strong growth potential, it is also subject to several significant restraints that can impede its expansion. One major deterrent is the substantial initial capital investment required for the design, construction, and installation of these large-scale systems. This high upfront cost can be a barrier for smaller enterprises or projects with limited budgets, prompting them to consider alternative, less costly cooling methods or pre-assembled cooling units, even if less efficient for large applications. The complexity and duration of the construction process, involving significant site work and specialized labor, also contribute to this high entry barrier.

Another crucial restraint is the increasing concern over water scarcity and the associated stringent water usage regulations in many regions. Cooling towers, particularly open-circuit designs, consume considerable amounts of water through evaporation, drift, and blowdown. As water resources become scarcer and environmental regulations tighten, industries face pressure to reduce water consumption, which can limit the adoption of traditional cooling tower designs. Furthermore, the operational and maintenance costs, including water treatment, energy consumption for fans and pumps, and periodic inspections/repairs, represent ongoing expenses that can be a disincentive for potential buyers. Finally, the volatile prices of raw materials such as steel, concrete, and FRP, coupled with supply chain disruptions, can lead to increased manufacturing costs and project delays, impacting overall market profitability and project feasibility.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment & Installation Costs | -0.8% | Global | Short-to-Mid Term (2025-2029) |

| Increasing Water Scarcity & Stringent Water Usage Regulations | -0.7% | Arid Regions, Heavily Regulated Countries (e.g., California, parts of Europe) | Mid-to-Long Term (2027-2033) |

| High Operational & Maintenance Costs (Energy, Water Treatment) | -0.6% | Global | Ongoing |

| Long Project Lead Times & Construction Complexity | -0.5% | Global | Short-to-Mid Term (2025-2029) |

| Volatility in Raw Material Prices & Supply Chain Disruptions | -0.4% | Global | Short-to-Mid Term (2025-2028) |

Field Erected Cooling Tower Market Opportunities Analysis

Despite existing restraints, the Field Erected Cooling Tower market is rich with significant opportunities for innovation and growth, driven by evolving industrial needs and environmental consciousness. One prominent opportunity lies in the extensive market for retrofitting and upgrading existing cooling towers. As many older industrial facilities seek to improve energy efficiency, reduce water consumption, and comply with updated environmental standards, replacing or modernizing outdated cooling systems presents a substantial demand segment. This allows manufacturers to offer advanced components, smart controls, and sustainable solutions without the need for entirely new construction, providing a cost-effective pathway to enhanced performance for end-users.

Furthermore, the increasing integration of smart technologies, such as the Internet of Things (IoT), artificial intelligence (AI), and advanced sensor systems, offers lucrative avenues for market expansion. These technologies enable real-time monitoring, predictive maintenance, and optimized operational control, leading to significant reductions in energy and water usage, and improved system reliability. The growing adoption of sustainable water management practices, including zero liquid discharge (ZLD) and advanced water treatment systems, also creates new niches for cooling tower designs that minimize environmental impact. Lastly, the rapid industrialization in emerging economies across Asia Pacific, Latin America, and Africa continues to present greenfield opportunities for new installations, driven by robust investments in power, petrochemical, manufacturing, and data center sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Retrofit & Modernization of Existing Towers | +1.0% | Developed Economies (North America, Europe, Japan) | Mid-to-Long Term (2027-2033) |

| Integration of Smart Technologies (IoT, AI, Automation) | +0.9% | Global | Short-to-Mid Term (2025-2029) |

| Growing Demand for Water-Efficient & Sustainable Solutions | +0.8% | Global, particularly Water-Stressed Regions | Mid-to-Long Term (2027-2033) |

| Expansion into Emerging Markets & Greenfield Projects | +1.1% | Asia Pacific, Latin America, Middle East & Africa | Short-to-Long Term (2025-2033) |

| Development of Hybrid Cooling Solutions (Wet-Dry) | +0.7% | Global | Mid-to-Long Term (2027-2033) |

Field Erected Cooling Tower Market Challenges Impact Analysis

The Field Erected Cooling Tower market faces several inherent challenges that demand strategic responses from manufacturers and service providers. One significant challenge is the intense competition within the market, driven by a fragmented landscape of established global players and numerous regional and local manufacturers. This competitive pressure often leads to price wars, impacting profit margins and necessitating continuous innovation to differentiate products and services. Companies must constantly invest in R&D to offer superior performance, energy efficiency, and cost-effectiveness to maintain their market position, which can strain resources.

Another critical challenge involves the fluctuations in raw material prices, particularly for steel, concrete, and fiberglass, which are primary components in field erected cooling tower construction. These price volatilities can significantly impact manufacturing costs and project quotations, making long-term planning and fixed-price contracts difficult. Furthermore, securing a skilled workforce for specialized tasks such as design, fabrication, and on-site assembly presents a continuous challenge. The lack of experienced engineers, welders, and technicians can lead to project delays, quality control issues, and increased labor costs. Adapting to diverse and evolving regional regulations concerning emissions, water discharge, and noise pollution also adds complexity, requiring manufacturers to develop region-specific compliance solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Price Pressure | -0.6% | Global | Ongoing |

| Volatility of Raw Material Prices | -0.5% | Global | Short-to-Mid Term (2025-2028) |

| Skilled Labor Shortage for Installation & Maintenance | -0.4% | Global, particularly Developed Economies | Mid-to-Long Term (2027-2033) |

| Complex Regulatory & Environmental Compliance | -0.3% | Global, Varies by Region | Ongoing |

| Energy Price Fluctuations Affecting Operational Costs | -0.2% | Global | Ongoing |

Field Erected Cooling Tower Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Field Erected Cooling Tower market, offering a detailed understanding of its current size, historical trends, and future growth projections. The scope encompasses a meticulous examination of key market dynamics, including drivers, restraints, opportunities, and challenges that shape the industry landscape. Furthermore, the report delves into extensive segmentation analysis across various parameters such as type, design, end-use industry, material, and capacity, providing granular insights into market opportunities. It also highlights regional market performance, identifies key players, and assesses the competitive environment, ensuring stakeholders receive actionable intelligence for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.65 Billion |

| Market Forecast in 2033 | USD 4.16 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SPX Cooling Technologies, Hamon Group, Baltimore Aircoil Company (BAC), EVAPCO, Marley (SPX Cooling Technologies brand), Thermax Ltd., Paharpur Cooling Towers Ltd., ENEXIO, MITA Cooling Technologies, Recold (Baltimore Aircoil Company brand), Tower Tech, Johnson Controls International Plc, Bell Cooling Towers, Star Cooling Towers, G&M Cooling Towers, Delta Cooling Towers, Liang Chi Industry, Brentwood Industries, Broad Group, FANS INC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Field Erected Cooling Tower market is comprehensively segmented to provide a granular view of its diverse components and understand varied market dynamics across different applications and designs. This detailed segmentation allows for the identification of specific growth pockets, emerging preferences, and technological shifts within the industry. By breaking down the market based on various parameters such as cooling tower type, design, material of construction, end-use industry, and capacity, the analysis offers valuable insights into how different segments contribute to the overall market size and growth trajectory. This structured approach helps stakeholders to pinpoint high-potential areas and tailor their strategies effectively.

Understanding these segments is crucial for manufacturers in product development and market positioning, as each segment often has distinct requirements concerning efficiency, durability, footprint, and cost. For instance, power generation facilities typically demand very large capacity towers, often concrete structures, while commercial HVAC applications might prefer smaller, modular FRP or steel units. The ongoing innovation in materials and smart technologies is also creating new sub-segments and cross-segment opportunities, particularly in areas like hybrid designs and advanced water treatment. This multi-faceted segmentation analysis underpins a robust understanding of market structure and competitive dynamics, enabling precise forecasting and strategic decision-making.

- By Type:

- Crossflow: Water flows horizontally across the fill as air flows vertically. Known for ease of maintenance and lower pumping head.

- Counterflow: Water flows vertically down the fill as air flows vertically up, optimizing heat transfer efficiency and requiring less floor space.

- By Design:

- Natural Draft: Relies on buoyancy of heated air for natural air circulation; typically very large concrete hyperbolic structures, common in large power plants.

- Mechanical Draft: Uses fans to force or induce air movement; offers better control over airflow and cooling performance.

- Forced Draft: Fans at the air inlet push air through the tower.

- Induced Draft: Fans at the air outlet pull air through the tower.

- By End-Use Industry:

- Power Generation: Crucial for thermal, nuclear, and concentrated solar power plants to dissipate waste heat.

- HVAC: Used in large commercial buildings, hospitals, and educational institutions for air conditioning and refrigeration.

- Chemical & Petrochemical: Essential for process cooling in refineries, chemical manufacturing, and pharmaceutical plants.

- Food & Beverage: Utilized for cooling processes in breweries, dairies, and other food processing facilities.

- Manufacturing: Supports cooling in various industrial processes, including automotive, metal processing, and textiles.

- Data Centers: Critical for maintaining optimal temperatures for server equipment to prevent overheating.

- Others: Includes applications in pulp & paper, metallurgy, and other heavy industries.

- By Material:

- Concrete: Offers high durability, long lifespan, and resistance to harsh environments, suitable for large industrial applications.

- Fiberglass Reinforced Plastic (FRP): Lightweight, corrosion-resistant, and relatively easy to install, often used in medium to large applications.

- Wood: Traditionally used, cost-effective but requires more maintenance and is susceptible to decay.

- Steel: (Galvanized Steel, Stainless Steel): Durable and fire-resistant, but susceptible to corrosion if not properly treated, commonly used in various industrial settings.

- By Capacity:

- Small: Typically for smaller industrial processes or light commercial applications.

- Medium: Caters to a broader range of industrial and commercial cooling needs.

- Large: Designed for heavy industrial use, such as power plants and large chemical facilities, requiring significant heat rejection.

Regional Highlights

- North America: This region is characterized by a mature industrial base and significant investments in data centers and infrastructure upgrades. Demand is driven by the need for energy-efficient replacements and technological advancements in cooling solutions. The presence of stringent environmental regulations also fosters innovation and adoption of compliant systems.

- Europe: Similar to North America, Europe's market is influenced by strict environmental policies and a focus on sustainability. The demand for retrofitting existing facilities and the adoption of advanced, eco-friendly cooling technologies are key drivers. Investment in renewable energy and green data centers also contributes to market growth.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market due to rapid industrialization, urbanization, and significant investments in manufacturing, power generation, and commercial infrastructure, particularly in countries like China, India, and Southeast Asian nations. The growing population and economic development are propelling the need for new cooling tower installations.

- Latin America: This region presents emerging opportunities driven by increasing industrial activity, particularly in mining, oil & gas, and manufacturing sectors. Infrastructure development and a growing energy demand are contributing to a steady rise in the adoption of field erected cooling towers.

- Middle East and Africa (MEA): MEA is witnessing substantial growth fueled by large-scale infrastructure projects, expansion of the petrochemical industry, and power generation initiatives. The region's hot climate necessitates robust and efficient cooling solutions, creating a strong demand for field erected towers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Field Erected Cooling Tower Market.- SPX Cooling Technologies

- Hamon Group

- Baltimore Aircoil Company (BAC)

- EVAPCO

- Marley (SPX Cooling Technologies brand)

- Thermax Ltd.

- Paharpur Cooling Towers Ltd.

- ENEXIO

- MITA Cooling Technologies

- Recold (Baltimore Aircoil Company brand)

- Tower Tech

- Johnson Controls International Plc

- Bell Cooling Towers

- Star Cooling Towers

- G&M Cooling Towers

- Delta Cooling Towers

- Liang Chi Industry

- Brentwood Industries

- Broad Group

- FANS INC.

Frequently Asked Questions

What is a field erected cooling tower?

A field erected cooling tower is a large-scale heat rejection device, custom-built on-site from individual components, designed to dissipate waste heat from industrial processes or HVAC systems by cooling water. Unlike factory-assembled units, these towers are highly customizable in terms of size, capacity, and materials, making them suitable for extensive industrial and power generation applications.

What are the primary benefits of field erected cooling towers?

The main benefits include their ability to handle very large heat loads, customizability to fit specific site requirements and operational demands, superior energy efficiency compared to smaller units for large applications, and a long service life due to robust construction and durable materials. They offer significant operational flexibility for complex industrial processes.

Which industries primarily use field erected cooling towers?

Field erected cooling towers are predominantly used in industries requiring substantial heat rejection. Key sectors include power generation (thermal, nuclear, and some renewable plants), chemical and petrochemical processing, oil & gas refineries, large manufacturing facilities, and extensive HVAC systems for commercial and institutional complexes. They are also increasingly vital for hyper-scale data centers.

How do environmental regulations impact the market?

Environmental regulations significantly influence the market by driving demand for more efficient and sustainable cooling solutions. Strict rules regarding water consumption (e.g., evaporation and blowdown), drift emissions, and noise pollution compel manufacturers to innovate and develop advanced designs, such as hybrid towers and intelligent water management systems, which comply with or exceed regulatory standards.

What new technologies are being integrated into field erected cooling towers?

New technologies include the integration of IoT sensors for real-time monitoring and data collection, AI-powered analytics for predictive maintenance and operational optimization, variable frequency drives (VFDs) for fan motor efficiency, advanced drift eliminators for water conservation, and specialized fills for enhanced heat transfer. These innovations aim to improve performance, reduce operational costs, and promote sustainability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted