District Cooling System Market

District Cooling System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705347 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

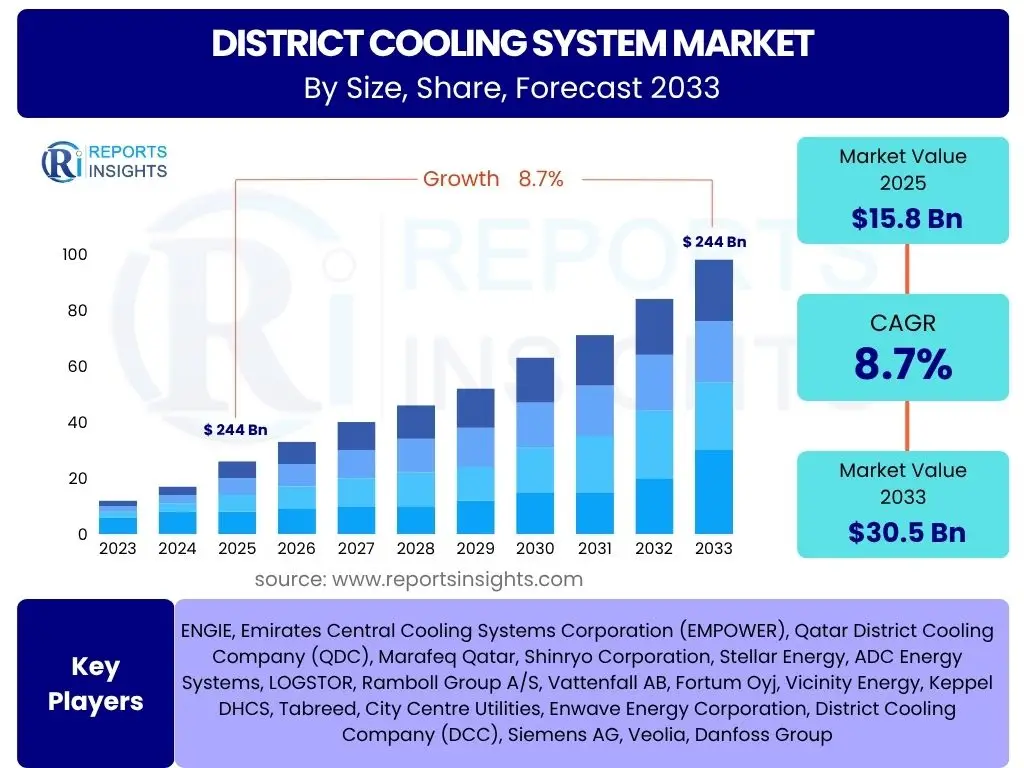

District Cooling System Market Size

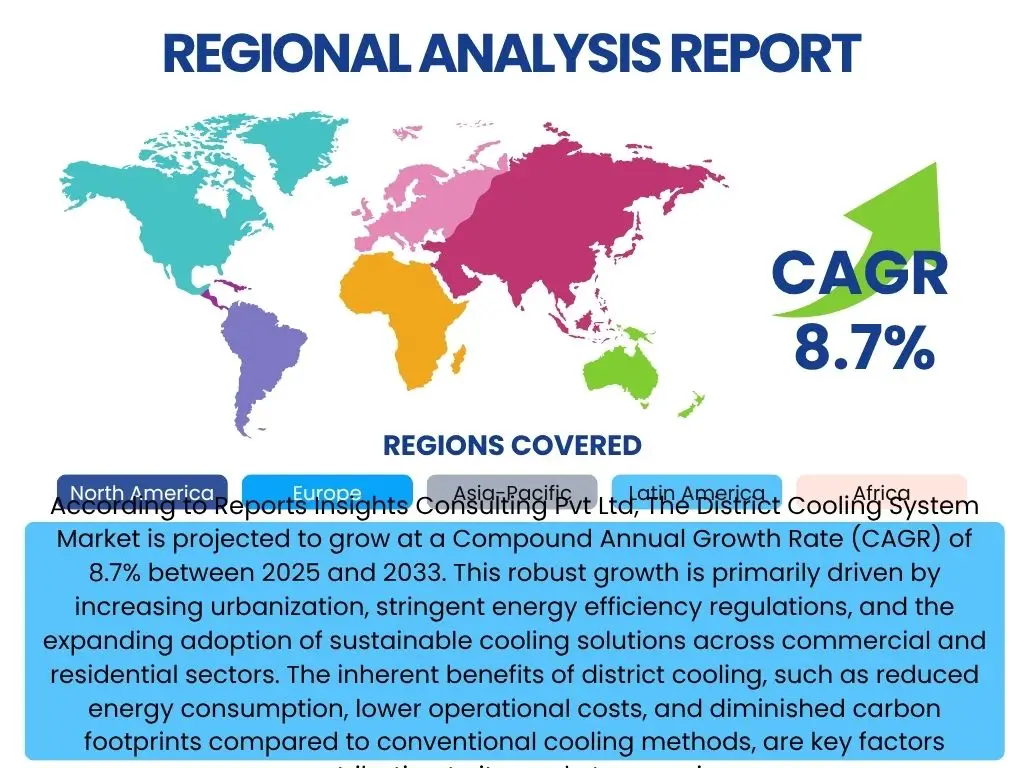

According to Reports Insights Consulting Pvt Ltd, The District Cooling System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. This robust growth is primarily driven by increasing urbanization, stringent energy efficiency regulations, and the expanding adoption of sustainable cooling solutions across commercial and residential sectors. The inherent benefits of district cooling, such as reduced energy consumption, lower operational costs, and diminished carbon footprints compared to conventional cooling methods, are key factors contributing to its market expansion.

The market is estimated at USD 15.8 Billion in 2025 and is projected to reach USD 30.5 Billion by the end of the forecast period in 2033. This significant increase highlights a global shift towards centralized, efficient, and environmentally friendly cooling infrastructure. Developing economies, particularly in Asia Pacific and the Middle East, are expected to be major contributors to this growth due to rapid infrastructure development and supportive government policies promoting green building initiatives.

Key District Cooling System Market Trends & Insights

Common user inquiries concerning trends in the District Cooling System market frequently revolve around sustainability, technological integration, and the evolving regulatory landscape. Users are keen to understand how environmental consciousness and the push for net-zero emissions are shaping the industry, particularly regarding the adoption of renewable energy sources and more efficient cooling technologies. There is also significant interest in the role of smart technologies, such as IoT and advanced control systems, in enhancing the operational efficiency and management of district cooling networks. Furthermore, the impact of governmental policies and international climate agreements on market development and investment opportunities remains a central theme for stakeholders seeking forward-looking insights.

- Growing integration of renewable energy sources such as solar thermal and geothermal for chiller power.

- Increasing adoption of smart district cooling networks leveraging IoT, AI, and big data analytics for optimized energy management and predictive maintenance.

- Expansion of district cooling into mixed-use developments and smart cities to achieve large-scale energy efficiency.

- Enhanced focus on energy storage solutions, including thermal energy storage, to improve grid flexibility and reduce peak load demand.

- Development of hybrid district cooling systems combining traditional and absorption chillers for improved energy performance.

- Rising demand for highly efficient, low-Global Warming Potential (GWP) refrigerants in new installations and retrofits.

AI Impact Analysis on District Cooling System

User queries regarding the impact of Artificial Intelligence (AI) on District Cooling Systems typically focus on its potential to optimize energy consumption, enhance operational efficiency, and facilitate predictive maintenance. Stakeholders are interested in how AI algorithms can analyze vast datasets from sensors and meters to fine-tune cooling production, distribution, and consumption, thereby minimizing energy waste and reducing operating costs. Concerns often include the initial investment required for AI integration, data privacy, and the need for skilled personnel to manage complex AI-driven systems. Nevertheless, there is a strong expectation that AI will play a transformative role in making district cooling networks more autonomous, responsive, and sustainable.

- Predictive maintenance and fault detection in chillers, pumps, and pipelines, reducing downtime and operational costs.

- Optimized energy management through real-time demand forecasting and supply modulation, leading to significant energy savings.

- Enhanced system control and automation, allowing for dynamic adjustments to cooling parameters based on external factors like weather and occupancy.

- Improved anomaly detection and security monitoring within the network, bolstering reliability.

- Facilitation of smart grid integration, enabling district cooling systems to act as flexible loads or energy storage assets.

Key Takeaways District Cooling System Market Size & Forecast

Common user questions about key takeaways from the District Cooling System market size and forecast often center on identifying the most critical growth drivers, the primary regions for investment, and the technological advancements poised to have the greatest impact. Users are keen to understand where future opportunities lie and what strategic considerations are paramount for market participants. There is a strong emphasis on understanding the long-term viability and sustainability aspects of district cooling, given the global push for decarbonization and energy efficiency. Insights are sought on how market dynamics might shift in response to evolving environmental regulations and technological breakthroughs, providing a comprehensive outlook for investors and policymakers alike.

- The market is on a robust growth trajectory, driven by urbanization, sustainability mandates, and infrastructure development.

- Asia Pacific and the Middle East are emerging as significant growth hubs due to rapid construction and supportive policies.

- Technological advancements, including AI, IoT, and thermal energy storage, are pivotal in enhancing system efficiency and attractiveness.

- High initial investment costs remain a notable barrier, though long-term operational savings and environmental benefits offset this.

- Government incentives and public-private partnerships are crucial in accelerating market adoption and project financing.

District Cooling System Market Drivers Analysis

The District Cooling System market is significantly propelled by several macro and microeconomic factors that collectively contribute to its expansion. A primary driver is the accelerating pace of urbanization worldwide, leading to dense population centers and large-scale commercial and residential developments that require efficient and centralized cooling solutions. Additionally, increasing global awareness regarding climate change and the imperative to reduce carbon emissions are compelling governments and organizations to adopt energy-efficient cooling technologies, with district cooling standing out as a viable option. The implementation of stringent energy efficiency regulations and building codes across various regions further mandates the adoption of advanced cooling systems, thereby stimulating market growth.

Furthermore, the inherent advantages of district cooling systems, such as lower operational and maintenance costs, reduced peak electricity demand, and enhanced energy security, are increasingly recognized by developers and end-users. These systems offer significant benefits in terms of space saving, as individual cooling units are replaced by a centralized plant, freeing up valuable building space. The push for smart city initiatives and integrated urban infrastructure also provides a fertile ground for the deployment of district cooling, as it aligns perfectly with the vision of creating sustainable and resource-efficient urban environments. These multifaceted drivers are collectively steering the market towards sustained growth and broader adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Urbanization and Population Density | +2.1% | Asia Pacific, Middle East | 2025-2033 |

| Growing Demand for Energy-Efficient Cooling Solutions | +1.8% | Global | 2025-2033 |

| Supportive Government Regulations and Initiatives | +1.5% | Europe, North America, UAE, China | 2025-2030 |

| Lower Operational Costs and Reduced Carbon Footprint | +1.2% | Global | 2025-2033 |

| Development of Smart Cities and Integrated Infrastructure | +1.0% | Middle East, Southeast Asia | 2028-2033 |

District Cooling System Market Restraints Analysis

Despite its significant growth potential, the District Cooling System market faces several formidable restraints that could impede its expansion. One of the most prominent challenges is the high initial capital investment required for planning, constructing, and deploying the extensive infrastructure, including central cooling plants, distribution networks, and pumping stations. This substantial upfront cost can be a deterrent for potential investors and developers, especially in regions with limited access to financing or where payback periods are perceived as long. Additionally, the complexity involved in securing large land parcels for central plants and laying down elaborate pipe networks can lead to significant logistical and bureaucratic hurdles, particularly in densely populated urban areas where space is at a premium.

Another key restraint is the potential for regulatory complexities and lengthy approval processes, which can delay project implementation and increase overall costs. Obtaining permits from multiple municipal and environmental agencies, along with navigating various zoning laws, often proves to be time-consuming. Furthermore, competition from conventional cooling methods, which may appear more flexible or less capital-intensive for individual building owners in the short term, continues to pose a challenge, particularly in markets where awareness of district cooling's long-term benefits is low. Public perception and resistance to large-scale infrastructure projects, especially if they involve disruption during construction, can also present significant obstacles to market adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.5% | Global, Emerging Economies | 2025-2030 |

| Complexity of Infrastructure Planning and Deployment | -1.0% | Densely Populated Urban Areas | 2025-2033 |

| Regulatory Hurdles and Lengthy Approval Processes | -0.8% | Europe, North America | 2025-2030 |

| Competition from Conventional Cooling Technologies | -0.7% | Global | 2025-2033 |

| Lack of Awareness in Developing Markets | -0.5% | Africa, Parts of Asia Pacific | 2025-2030 |

District Cooling System Market Opportunities Analysis

The District Cooling System market is presented with numerous opportunities that promise to drive substantial growth over the forecast period. A significant opportunity lies in the expanding scope of smart city development projects worldwide, which inherently prioritize integrated and sustainable utility infrastructures. District cooling aligns perfectly with the smart city paradigm by offering centralized, efficient, and interconnected cooling services for large urban areas. This trend, coupled with the increasing adoption of sustainable building practices and green certifications, creates a strong demand for cooling solutions that meet rigorous environmental standards. The integration of district cooling with renewable energy sources, such as solar thermal, geothermal, and waste heat recovery, further enhances its appeal and opens new avenues for energy-efficient and low-carbon operation.

Moreover, the burgeoning demand for cooling in data centers and industrial facilities, which require precise and continuous temperature control, offers a high-growth niche for district cooling systems. These energy-intensive sectors can significantly benefit from the reliability and cost-efficiency provided by centralized cooling. Furthermore, retrofitting existing commercial and residential buildings with district cooling connections presents a vast untapped market, particularly in mature urban centers looking to upgrade their energy infrastructure. The growing emphasis on public-private partnerships (PPPs) and innovative financing models can also de-risk investments and accelerate project deployment, making district cooling more accessible and attractive to a wider range of stakeholders. These opportunities collectively highlight a dynamic landscape for market expansion and innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart City Development Projects | +1.8% | Middle East, Southeast Asia, Europe | 2025-2033 |

| Rising Demand from Data Centers and Industrial Sector | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of Renewable Energy Integration | +1.3% | Global | 2028-2033 |

| Retrofitting of Existing Buildings and Infrastructure | +1.0% | Mature Urban Markets | 2025-2030 |

| Innovative Financing Models and Public-Private Partnerships | +0.9% | Global | 2025-2033 |

District Cooling System Market Challenges Impact Analysis

The District Cooling System market, while promising, is not without its significant challenges that could affect its growth trajectory. One primary challenge is the technical complexity involved in designing, installing, and operating large-scale district cooling networks. This includes ensuring optimal hydraulic balancing across extensive pipeline networks, managing pressure drops, and maintaining consistent cooling capacity across diverse loads. The need for highly specialized engineering expertise and the intricate nature of these systems can lead to increased project costs and potential delays if not managed effectively. Furthermore, ensuring the reliability and redundancy of the central plant and distribution network is critical, as any failure can impact a large number of connected buildings, making system resilience a significant concern for operators and consumers alike.

Another critical challenge stems from environmental concerns, particularly related to water scarcity and the environmental impact of refrigerant leaks. District cooling systems, especially those using evaporative cooling towers, can have significant water consumption, which is a growing concern in water-stressed regions. While efforts are made to use low-GWP refrigerants, potential leaks from large-scale systems still pose an environmental risk. Moreover, the integration of district cooling with existing energy grids can be challenging, requiring careful planning to avoid grid strain, especially during peak demand periods. Overcoming these technical and environmental hurdles, alongside the complexities of large-scale project management, will be crucial for the sustained growth and broader acceptance of district cooling solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Complexities in Design and Operation | -1.2% | Global | 2025-2033 |

| Water Scarcity Concerns for Cooling Towers | -0.9% | Middle East, Arid Regions | 2025-2033 |

| Environmental Impact of Refrigerant Leaks | -0.7% | Global, Europe | 2025-2030 |

| Grid Integration and Peak Load Management | -0.5% | High-Demand Grids | 2025-2033 |

| Land Availability for Central Plants in Urban Areas | -0.4% | Densely Populated Cities | 2025-2030 |

District Cooling System Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the District Cooling System market, offering an exhaustive analysis of its current landscape, historical performance, and future projections. The scope encompasses detailed segmentation across various parameters, including component type, production source, application, end-user, and regional geographical spread, providing a granular view of market trends and opportunities. Furthermore, the report provides an in-depth competitive analysis, profiling key market players and their strategic initiatives, while also assessing the impact of emerging technologies such as Artificial Intelligence and sustainable energy integration on market evolution. The objective is to equip stakeholders with actionable insights for strategic decision-making and investment planning in this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.8 Billion |

| Market Forecast in 2033 | USD 30.5 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ENGIE, Emirates Central Cooling Systems Corporation (EMPOWER), Qatar District Cooling Company (QDC), Marafeq Qatar, Shinryo Corporation, Stellar Energy, ADC Energy Systems, LOGSTOR, Ramboll Group A/S, Vattenfall AB, Fortum Oyj, Vicinity Energy, Keppel DHCS, Tabreed, City Centre Utilities, Enwave Energy Corporation, District Cooling Company (DCC), Siemens AG, Veolia, Danfoss Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The District Cooling System market is analyzed through comprehensive segmentation to provide granular insights into its diverse components, production methods, and end-use applications. This detailed breakdown enables a clear understanding of the market's structure and the performance of various sub-segments. By examining the market through these lenses, stakeholders can identify high-growth areas, assess competitive landscapes, and formulate targeted strategies that align with specific market demands and technological advancements across different sectors.

- By Production Source: Electric Chillers, Absorption Chillers (Steam/Hot Water, Natural Gas Fired, Flue Gas Fired), Heat Pumps, Free Cooling, Hybrid Systems.

- By Component: Chillers (Centrifugal, Screw, Reciprocating, Absorption), Pumps (Circulation Pumps, Condensate Pumps), Pipes (Pre-insulated Pipes, Steel Pipes, HDPE Pipes), Cooling Towers (Open Loop, Closed Loop), Control Systems (BMS, SCADA, IoT), Energy Transfer Stations.

- By Application: Commercial (Office Buildings, Retail & Shopping Malls, Hotels & Resorts, Hospitals & Healthcare, Educational Institutions), Residential (Multi-family Dwellings, Mixed-Use Developments), Industrial (Data Centers, Manufacturing Plants, Pharmaceutical, Food & Beverage), Government & Institutional.

- By End-Use Sector: Utilities, Commercial Real Estate Developers, Industrial Sector, Public Sector.

Regional Highlights

- Middle East and Africa (MEA): This region is a global leader in district cooling adoption, particularly the GCC countries (UAE, Qatar, Saudi Arabia), driven by extreme climatic conditions, rapid infrastructure development, and substantial government investments in smart cities and sustainable initiatives. Dubai and Abu Dhabi, for instance, have some of the largest district cooling networks globally, powered by visionary urban planning.

- Asia Pacific (APAC): Expected to witness the highest growth, propelled by burgeoning urbanization, industrialization, and a rising demand for energy-efficient solutions in countries like China, India, Singapore, and Japan. Government support for green building codes and large-scale urban development projects further fuels market expansion.

- Europe: Characterized by a strong focus on decarbonization and energy efficiency targets, leading to increased adoption of district cooling, especially in Nordic countries (Sweden, Denmark, Finland) where free cooling from natural water bodies is widely utilized. Germany, France, and the UK are also expanding their networks with an emphasis on renewable energy integration.

- North America: The market is mature, with steady growth driven by the need to modernize aging infrastructure, reduce energy costs, and meet stringent environmental regulations. Key cities in the US and Canada are expanding existing systems and investing in new, highly efficient district cooling plants, particularly for commercial and institutional applications.

- Latin America: An emerging market with growing potential, spurred by urbanization and increasing energy demands in countries like Brazil and Mexico. While adoption is slower compared to other regions, growing awareness of energy efficiency and sustainability is expected to drive future investments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the District Cooling System Market.- ENGIE

- Emirates Central Cooling Systems Corporation (EMPOWER)

- Qatar District Cooling Company (QDC)

- Marafeq Qatar

- Shinryo Corporation

- Stellar Energy

- ADC Energy Systems

- LOGSTOR

- Ramboll Group A/S

- Vattenfall AB

- Fortum Oyj

- Vicinity Energy

- Keppel DHCS

- Tabreed

- City Centre Utilities

- Enwave Energy Corporation

- District Cooling Company (DCC)

- Siemens AG

- Veolia

- Danfoss Group

Frequently Asked Questions

Analyze common user questions about the District Cooling System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is District Cooling and how does it work?

District cooling involves the centralized production of chilled water which is then distributed through an underground pipeline network to multiple buildings for air conditioning and process cooling. A central plant generates chilled water using various technologies, which is then pumped to connected buildings, eliminating the need for individual chillers in each structure.

What are the primary benefits of using District Cooling Systems?

District cooling offers numerous benefits including enhanced energy efficiency, reduced operational and maintenance costs, lower carbon emissions, significant space savings within buildings, improved aesthetic appeal of urban landscapes, and increased reliability compared to decentralized cooling methods.

Which regions are leading in District Cooling adoption and why?

The Middle East (especially UAE, Qatar) and parts of Asia Pacific (e.g., Singapore, China) are leading in district cooling adoption due to rapid urbanization, hot climates, significant infrastructure development, and supportive government policies promoting sustainable and energy-efficient building solutions.

What are the main challenges facing the growth of the District Cooling System market?

Key challenges include high initial capital investment for infrastructure, complexities in planning and deploying extensive networks, regulatory hurdles, potential impacts of water scarcity on cooling tower operations, and competition from conventional cooling systems.

How do District Cooling Systems contribute to sustainability and smart cities?

District cooling contributes to sustainability by improving energy efficiency, reducing greenhouse gas emissions, and enabling the integration of renewable energy sources and thermal energy storage. For smart cities, it provides a crucial backbone for integrated, efficient, and resilient urban energy infrastructure, supporting resource optimization and decarbonization goals.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted