Fiber optic Cable Market

Fiber optic Cable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702243 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

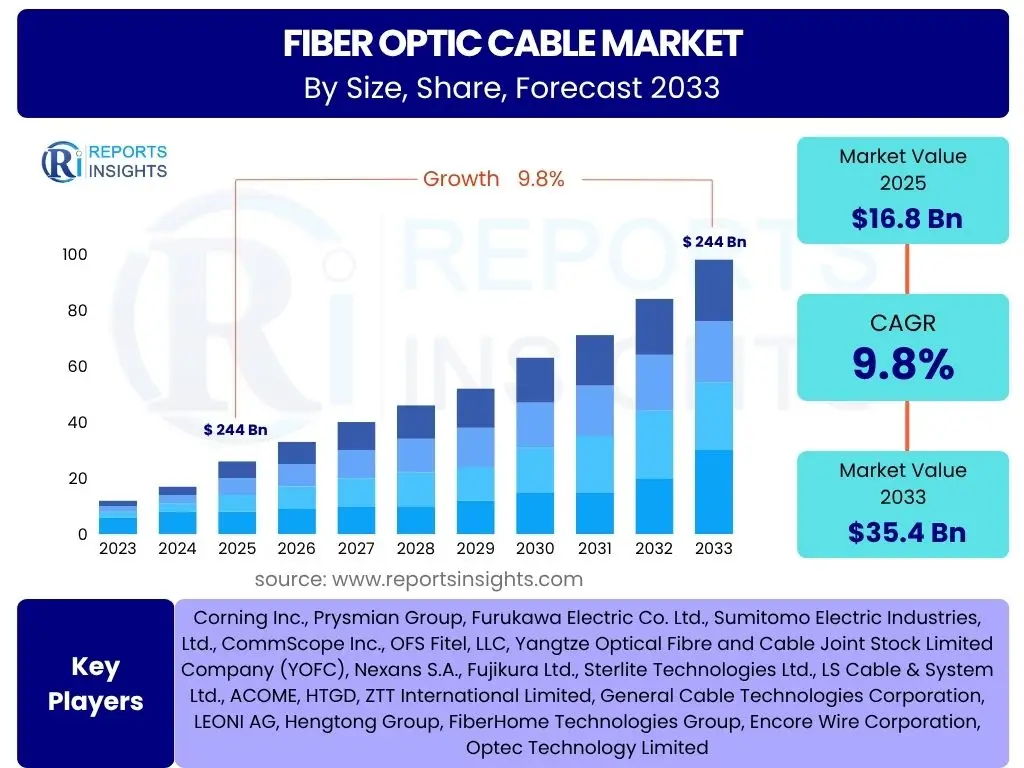

Fiber optic Cable Market Size

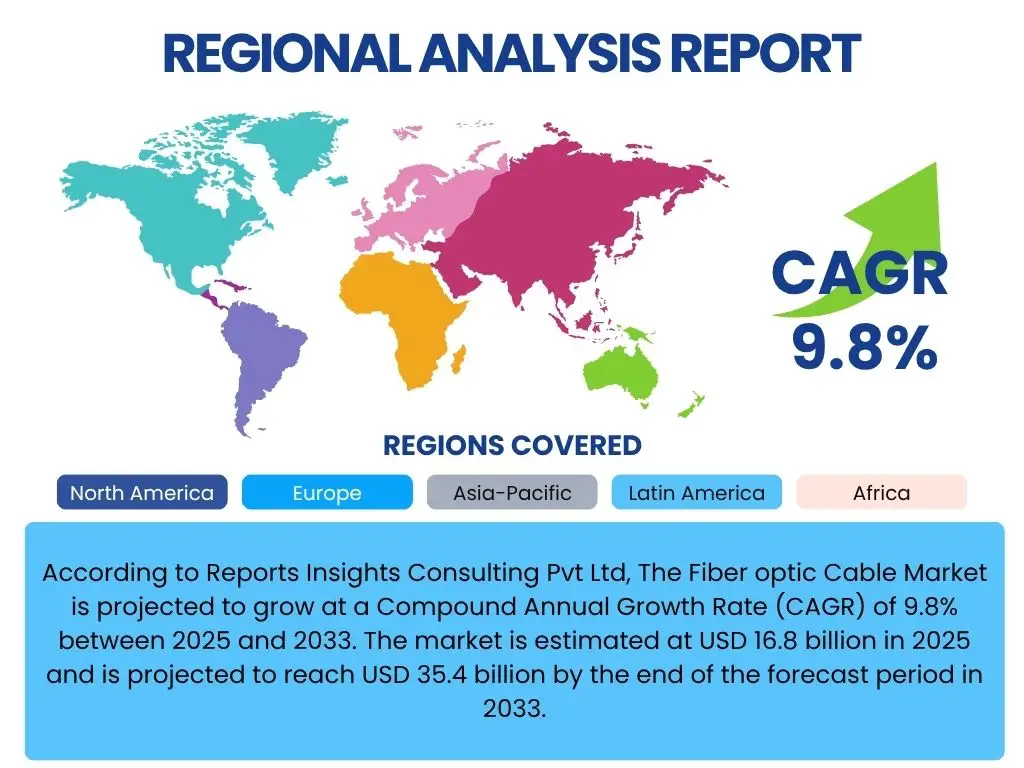

According to Reports Insights Consulting Pvt Ltd, The Fiber optic Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 16.8 billion in 2025 and is projected to reach USD 35.4 billion by the end of the forecast period in 2033.

Key Fiber optic Cable Market Trends & Insights

User inquiries frequently highlight the accelerating pace of digital transformation and infrastructure development as central to the fiber optic cable market. The pervasive demand for high-speed internet connectivity, driven by escalating data consumption and the global rollout of next-generation wireless technologies, is creating an unprecedented need for advanced fiber optic networks. Trends indicate a significant shift towards fiber-to-the-X (FTTx) deployments, particularly fiber-to-the-home (FTTH), as well as the critical role of fiber in enabling 5G networks and supporting hyperscale data centers. Innovations in cable design, such as higher fiber count cables and bend-insensitive fibers, are also noted as essential for efficient deployment and enhanced performance in increasingly complex network architectures.

- Exponential growth in global data traffic and internet penetration.

- Aggressive expansion of Fiber-to-the-X (FTTx) deployments, especially FTTH.

- Widespread rollout of 5G networks, necessitating extensive fiber backhaul infrastructure.

- Boom in hyperscale data centers and cloud computing demanding high-bandwidth interconnectivity.

- Emergence of smart cities and IoT ecosystems requiring robust wired communication backbones.

- Technological advancements in fiber optic cable design, including higher density and bend-insensitive fibers.

- Increasing demand for submarine cables for intercontinental data transmission.

- Focus on sustainable and environmentally friendly manufacturing practices within the industry.

AI Impact Analysis on Fiber optic Cable

Common user questions regarding AI's impact on fiber optic cables often revolve around how artificial intelligence can optimize network performance, manage complex infrastructures, and predict potential failures. AI's influence is predominantly seen in enhancing the operational efficiency and reliability of fiber optic networks rather than directly affecting the physical cable manufacturing process. AI-driven analytics are being applied to vast datasets generated by network traffic, allowing for real-time optimization of data routing, bandwidth allocation, and fault detection. This capability significantly reduces downtime, improves service quality, and enables more proactive maintenance strategies, thereby maximizing the lifespan and performance of fiber optic assets.

Furthermore, AI is instrumental in the evolution of autonomous networks, where self-healing and self-optimizing functionalities are paramount. Through machine learning algorithms, network operators can identify anomalies, predict congestion points, and automate responses, ensuring seamless data flow across fiber infrastructure. This extends to security aspects, where AI can detect unusual patterns indicative of cyber threats or physical tampering with fiber lines. While AI does not replace fiber optic cables, it critically augments their utility and management, making complex, high-capacity networks more manageable, resilient, and cost-effective to operate. The synergistic relationship between AI and fiber optics is set to define the next generation of digital infrastructure.

- Enhanced network optimization and traffic management through AI algorithms.

- Predictive maintenance and fault detection, improving network reliability and uptime.

- Automation of network operations and resource allocation, leading to increased efficiency.

- Improved security monitoring and threat detection for fiber optic infrastructure.

- Data analytics for network planning and capacity expansion, driven by AI insights.

Key Takeaways Fiber optic Cable Market Size & Forecast

An analysis of user queries regarding the fiber optic cable market size and forecast consistently points to an industry poised for substantial and sustained growth. The overriding insight is that fiber optics remain the indispensable backbone of the modern digital economy, with demand being fundamentally driven by the relentless increase in global data traffic and the widespread deployment of advanced communication technologies. The market is not merely growing but expanding in scope, incorporating new applications and deepening its penetration into previously underserved areas, such as rural broadband initiatives. The forecast indicates that despite potential challenges, the strategic importance of fiber connectivity will continue to propel significant investment and innovation in the sector, solidifying its role as the foundational infrastructure for future digital ecosystems.

The market's trajectory is robustly supported by macro trends including widespread urbanization, the proliferation of smart devices, and the continuous evolution of cloud-based services. Furthermore, governmental initiatives worldwide aimed at digital inclusion and infrastructure modernization are providing significant impetus, ensuring a steady demand pipeline. The integration of cutting-edge technologies like 5G, IoT, and AI necessitates fiber optic's unparalleled bandwidth and low latency capabilities, making it a critical enabler rather than just a component. Therefore, the long-term outlook for the fiber optic cable market is exceedingly positive, characterized by consistent growth and diversification into new and emerging application areas.

- The fiber optic cable market is set for robust, long-term growth, driven by fundamental shifts in global data consumption and digital transformation.

- Investment in fiber infrastructure is critical for the rollout of 5G networks, contributing significantly to market expansion.

- FTTx deployments, especially FTTH, represent a major growth vector, bridging the digital divide and enabling high-speed connectivity.

- Technological advancements in cable design and manufacturing are enhancing efficiency and capacity, meeting evolving network demands.

- Government support for digital infrastructure projects globally is a key accelerator for market development.

- Despite initial investment hurdles, the long-term benefits and strategic necessity of fiber optics ensure continued market ascendancy.

Fiber optic Cable Market Drivers Analysis

The proliferation of high-speed internet demand stands as a paramount driver for the fiber optic cable market. With the escalating reliance on digital services, remote work, online education, and entertainment streaming, the need for robust, low-latency, and high-bandwidth connectivity has surged globally. Fiber optic cables, owing to their superior data transmission capabilities over long distances with minimal signal loss, are the foundational infrastructure for meeting this burgeoning demand. This fundamental shift in consumer and enterprise behavior necessitates extensive deployment of fiber infrastructure, particularly in urban and increasingly, rural areas, to support current and future data traffic volumes.

Furthermore, the global rollout of 5G networks is intrinsically linked to the expansion of fiber optic infrastructure. 5G technology, promising ultra-low latency and unprecedented speeds, requires a dense network of fiber backhaul to connect its base stations and ensure optimal performance. Each 5G cell site, whether macro or small cell, needs fiber connectivity to handle the immense data throughput. This symbiotic relationship ensures that as 5G deployments accelerate, so too does the demand for a comprehensive fiber optic network, positioning it as a critical enabler for the next generation of wireless communication. Complementing this, the rapid growth of cloud computing and hyperscale data centers also fuels demand, as these facilities require vast amounts of fiber for internal connections and external interconnections to process and distribute massive data volumes efficiently.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Speed Internet | +1.5% | Global | Long-term |

| Global Rollout of 5G Networks | +1.2% | North America, Asia Pacific, Europe | Mid-term |

| Growth of Cloud Computing and Data Centers | +1.0% | Global, particularly North America, Europe, Asia Pacific | Mid-term to Long-term |

| Government Initiatives and Investments in Digital Infrastructure | +0.8% | Emerging Economies, Europe, Asia Pacific | Mid-term |

| Rising Adoption of FTTH/FTTx Deployments | +1.1% | Asia Pacific, Europe, North America | Mid-term to Long-term |

| Expansion of IoT and Smart City Projects | +0.7% | Global, especially developed urban areas | Long-term |

Fiber optic Cable Market Restraints Analysis

Despite the robust growth drivers, the fiber optic cable market faces several significant restraints, primarily stemming from the substantial initial investment required for deployment. The capital expenditure involved in laying down extensive fiber networks, including civil works, trenching, and labor costs, is exceptionally high. This cost barrier can deter smaller service providers or limit the pace of infrastructure development, particularly in developing regions or economically challenged areas. Additionally, the complexity of installation, which often involves navigating diverse terrains, existing underground utilities, and obtaining multiple permits, further adds to both cost and deployment timelines, slowing market expansion.

Another prominent restraint is the intense competition from wireless communication technologies. While fiber optics is the backbone for wireless networks like 5G, the ongoing advancements in satellite internet, fixed wireless access (FWA), and next-generation Wi-Fi standards present alternatives for last-mile connectivity. These wireless solutions may offer quicker deployment and lower upfront costs in certain scenarios, potentially diverting investments from fiber optic infrastructure in specific applications or geographical niches. Furthermore, the market can be impacted by geopolitical tensions and supply chain disruptions. Reliance on specific regions for raw materials or manufacturing can lead to price volatility and delays, affecting the overall stability and growth trajectory of the fiber optic cable market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Deployment Costs | -0.8% | Global, particularly Emerging Markets | Mid-term |

| Complexity of Installation and Right-of-Way Issues | -0.6% | Global | Mid-term |

| Competition from Wireless Technologies (e.g., Satellite, FWA) | -0.5% | Rural Areas, Specific Verticals | Short-term to Mid-term |

| Skilled Labor Shortage for Installation and Maintenance | -0.4% | Developed Economies | Mid-term |

| Geopolitical Tensions and Supply Chain Disruptions | -0.7% | Global | Short-term |

Fiber optic Cable Market Opportunities Analysis

The global drive for enhanced digital connectivity presents a significant opportunity for the fiber optic cable market through increased rural broadband deployment. Many remote and underserved areas still lack access to high-speed internet, creating a vast untapped market. Government initiatives and public-private partnerships focused on bridging the digital divide are actively promoting and funding the expansion of fiber infrastructure into these regions. This not only opens new revenue streams for fiber optic cable manufacturers and deployers but also stimulates economic growth and improves quality of life in these communities, making it a critical area for market expansion over the coming years.

Another substantial opportunity lies in the continuous upgrade and expansion of submarine cable networks. These indispensable underwater conduits form the backbone of intercontinental communication, carrying the vast majority of global internet traffic. As data demands continue to surge, the need for new, higher-capacity submarine cables and the maintenance/upgrade of existing ones will remain constant. Furthermore, the advent of smart cities and the Internet of Things (IoT) provides immense opportunities, as these require ubiquitous, high-bandwidth, and low-latency connectivity that only fiber can reliably provide. Specialty fiber applications in sectors like medical, defense, and industrial automation also represent niche but high-value growth areas, leveraging fiber's unique properties beyond traditional telecommunications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rural Broadband and Underserved Area Deployments | +1.3% | Global, particularly Asia Pacific, Africa, Latin America | Long-term |

| Expansion and Upgrade of Submarine Cable Networks | +1.0% | Coastal Regions, Global Interconnections | Mid-term to Long-term |

| Growth of Smart Cities and IoT Infrastructure | +0.9% | Developed Urban Areas Globally | Mid-term to Long-term |

| Demand for Specialty Fiber Optic Cables in Niche Applications | +0.7% | North America, Europe, Asia Pacific | Mid-term |

| Development of Sustainable and Green Fiber Solutions | +0.6% | Global | Long-term |

Fiber optic Cable Market Challenges Impact Analysis

The fiber optic cable market faces significant challenges related to supply chain disruptions and volatility in raw material prices. The production of fiber optic cables relies on specific high-purity glass, plastics, and other components, often sourced from a concentrated number of suppliers globally. Geopolitical events, trade disputes, and natural disasters can disrupt these intricate supply chains, leading to shortages of critical materials and increased lead times. This directly impacts manufacturing capacities, delays project deployments, and can inflate production costs, subsequently affecting market stability and profitability across the value chain. Ensuring a resilient and diversified supply chain remains a critical concern for industry stakeholders.

Another formidable challenge is the complex regulatory landscape and the need for numerous permits and approvals. Deploying fiber optic infrastructure, especially underground or across public lands, involves navigating a patchwork of local, regional, and national regulations, environmental assessments, and right-of-way negotiations. These processes can be time-consuming, costly, and subject to frequent changes, leading to significant project delays and increased administrative burdens for network operators and cable manufacturers. Furthermore, technological obsolescence, while less immediate than in other tech sectors, poses a long-term challenge. As new transmission technologies emerge or as network demands push beyond current fiber capacities, existing infrastructure may require costly upgrades or replacements, requiring continuous innovation and investment in research and development to maintain competitive edge and future-proof deployments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Raw Material Price Volatility | -0.7% | Global | Short-term to Mid-term |

| Complex Regulatory Environment and Permitting Issues | -0.5% | Regional Specific (e.g., Europe, North America) | Mid-term |

| Ensuring Network Security and Preventing Physical Damage | -0.4% | Global | Ongoing |

| Environmental Concerns and Waste Management | -0.3% | Developed Economies | Long-term |

| Technological Obsolescence and Need for Continuous Innovation | -0.2% | Global | Long-term |

Fiber optic Cable Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Fiber optic Cable Market, encompassing market sizing, growth forecasts, key trends, and a detailed examination of market drivers, restraints, opportunities, and challenges. It segments the market by various types, applications, and end-use industries, providing a granular view of market dynamics across key geographical regions. The report also offers competitive landscape insights, profiling leading market participants and their strategic initiatives, to deliver actionable intelligence for stakeholders navigating this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 16.8 billion |

| Market Forecast in 2033 | USD 35.4 billion |

| Growth Rate | 9.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Corning Inc., Prysmian Group, Furukawa Electric Co. Ltd., Sumitomo Electric Industries, Ltd., CommScope Inc., OFS Fitel, LLC, Yangtze Optical Fibre and Cable Joint Stock Limited Company (YOFC), Nexans S.A., Fujikura Ltd., Sterlite Technologies Ltd., LS Cable & System Ltd., ACOME, HTGD, ZTT International Limited, General Cable Technologies Corporation, LEONI AG, Hengtong Group, FiberHome Technologies Group, Encore Wire Corporation, Optec Technology Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fiber optic Cable Market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market growth. This comprehensive segmentation allows for detailed analysis of various product types, applications, and end-use industries, enabling stakeholders to identify specific growth areas and emerging trends. The market is primarily divided by fiber type, highlighting the prevalence and specific use cases of single-mode versus multi-mode fibers. Further breakdowns by application underscore the varying demands from FTTx deployments, long-haul communication, data centers, and specialized industrial uses. The end-use industry segmentation provides insights into the primary sectors driving adoption, such as telecommunications, oil and gas, and defense, reflecting the broad applicability of fiber optic technology across the global economy.

- By Type:

- Single-mode Fiber: Predominantly used for long-distance communication and high-bandwidth applications due to its ability to carry a single light ray.

- Multi-mode Fiber: Utilized for shorter distances, typically within buildings or campuses, offering cost-effective solutions for less demanding applications.

- By Application:

- FTTx (Fiber-to-the-Home/Building/Curb/Node): Driving residential and commercial high-speed internet connectivity.

- Long-Haul Communication: Essential for backbone networks connecting cities and countries.

- Submarine Communication: Forming the bedrock of intercontinental data transmission.

- Data Center Interconnect: Providing high-speed links within and between data centers.

- Enterprise Networks: Supporting robust internal communication infrastructures for businesses.

- Industrial Control Systems: Enabling reliable data transfer in industrial automation and smart manufacturing.

- Defense and Aerospace: Critical for secure and high-performance communication in military and avionics.

- Healthcare: Used for medical imaging, patient monitoring, and high-bandwidth data needs in hospitals.

- Broadcast and CATV: Facilitating high-quality video and television signal distribution.

- Smart Cities and IoT: Providing the foundational network for urban smart services and IoT device connectivity.

- By End-Use Industry:

- Telecommunications: The largest segment, driven by mobile network backhaul, internet infrastructure, and fixed-line services.

- Oil & Gas: Used for seismic exploration, well monitoring, and communication in harsh environments.

- Energy & Utilities: Essential for smart grids, power transmission monitoring, and utility communication.

- Medical: For high-resolution imaging, endoscopic equipment, and data-intensive medical applications.

- Defense: For secure communication, surveillance, and critical mission applications.

- Industrial: Enabling automation, process control, and data acquisition in manufacturing and industrial facilities.

- Government: For secure internal networks and public service infrastructure.

- Residential: Directly linked to FTTH deployments for consumer broadband.

- Commercial: For business parks, offices, and commercial establishments requiring high-speed connectivity.

- By Material:

- Glass Optical Fiber: The dominant material due to its superior performance characteristics.

- Plastic Optical Fiber (POF): Used in shorter distance, less demanding applications due to flexibility and ease of installation.

- By Deployment:

- Aerial: Cables suspended on poles.

- Direct-Buried: Cables laid directly underground.

- Duct: Cables installed within protective conduits.

- Submarine: Cables laid on the ocean floor for international connectivity.

- Indoor: Cables used within buildings and data centers.

Regional Highlights

- North America: This region is characterized by robust investments in 5G infrastructure, continuous upgrades to existing broadband networks, and the expansion of data centers. The presence of major technology companies and a high rate of digital adoption drive sustained demand for high-capacity fiber optic cables. Government initiatives and private sector funding for rural broadband also contribute significantly to market growth.

- Europe: Europe is focused on achieving widespread gigabit connectivity, propelled by national broadband plans and the Digital Agenda for Europe. The region sees strong deployment of FTTx, particularly FTTH, and significant investments in smart city projects that rely heavily on fiber infrastructure. Regulatory support and increasing demand for ultra-fast internet across industries fuel market expansion.

- Asia Pacific (APAC): APAC is anticipated to be the fastest-growing region, primarily driven by large-scale FTTH deployments in countries like China, India, and Japan. Rapid urbanization, increasing smartphone penetration, and massive investments in 5G network rollouts are key growth catalysts. The region also boasts a significant manufacturing base for fiber optic cables, contributing to competitive pricing and extensive supply.

- Latin America: This region is experiencing significant growth in internet penetration and digital transformation initiatives. Countries are increasingly investing in expanding their broadband infrastructure, including national fiber backbone networks and last-mile connectivity. The demand is fueled by a rising middle class and governmental efforts to bridge the digital divide, creating substantial opportunities for market players.

- Middle East and Africa (MEA): The MEA region is witnessing substantial investments in telecommunication infrastructure, driven by economic diversification efforts, smart city developments (e.g., in UAE and Saudi Arabia), and increasing internet access for a young and growing population. Governments are actively promoting digital connectivity, leading to new fiber optic cable deployments for both domestic and international connectivity, including submarine cable projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fiber optic Cable Market.- Corning Inc.

- Prysmian Group

- Furukawa Electric Co. Ltd.

- Sumitomo Electric Industries, Ltd.

- CommScope Inc.

- OFS Fitel, LLC

- Yangtze Optical Fibre and Cable Joint Stock Limited Company (YOFC)

- Nexans S.A.

- Fujikura Ltd.

- Sterlite Technologies Ltd.

- LS Cable & System Ltd.

- ACOME

- HTGD

- ZTT International Limited

- General Cable Technologies Corporation

- LEONI AG

- Hengtong Group

- FiberHome Technologies Group

- Encore Wire Corporation

- Optec Technology Limited

Frequently Asked Questions

Analyze common user questions about the Fiber optic Cable market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary driver of fiber optic cable market growth?

The primary driver is the exponentially increasing demand for high-speed internet, driven by data consumption from streaming, cloud services, and 5G network rollouts, necessitating robust and high-bandwidth infrastructure.

How does 5G deployment impact the fiber optic cable market?

5G deployment significantly boosts the fiber optic cable market as 5G networks require extensive fiber backhaul for their dense network of cell sites to ensure ultra-low latency and high data throughput, making fiber indispensable.

What are the main challenges facing the fiber optic cable market?

Key challenges include the high initial investment costs for deployment, complex installation processes, skilled labor shortages, and potential supply chain disruptions affecting raw material availability and pricing.

What role does AI play in the fiber optic cable industry?

AI primarily enhances the fiber optic industry through network optimization, predictive maintenance, and autonomous management systems, improving network efficiency, reliability, and reducing operational costs. It complements, not replaces, fiber infrastructure.

Which region is expected to lead the fiber optic cable market growth?

Asia Pacific is anticipated to lead market growth due to rapid FTTx deployments, extensive 5G infrastructure development, and increasing internet penetration in densely populated countries across the region.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted