Superconducting Cable Market

Superconducting Cable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704383 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

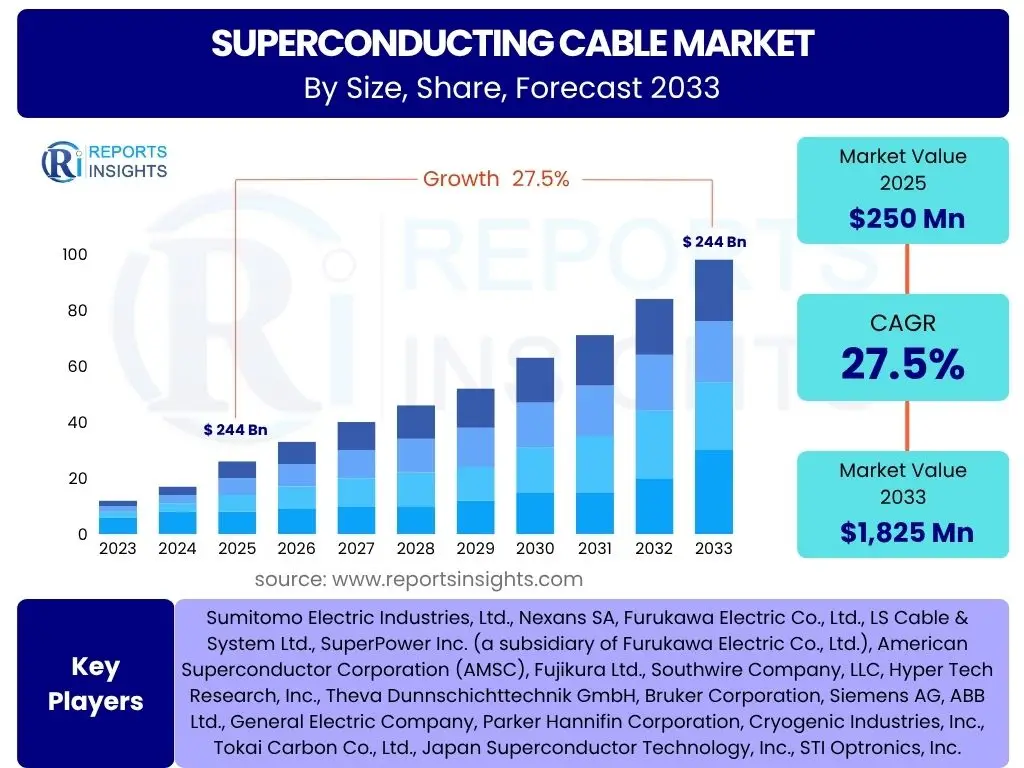

Superconducting Cable Market Size

According to Reports Insights Consulting Pvt Ltd, The Superconducting Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 27.5% between 2025 and 2033. The market is estimated at USD 250 million in 2025 and is projected to reach USD 1,825 million by the end of the forecast period in 2033.

Key Superconducting Cable Market Trends & Insights

User inquiries frequently focus on the emergent trends shaping the superconducting cable market, seeking to understand the underlying drivers and technological advancements. Key questions revolve around the push for enhanced energy efficiency, the integration of renewable energy sources into existing grids, and the modernization of power infrastructure. The market is increasingly influenced by the global imperative to reduce transmission losses and bolster grid resilience, leading to significant investments in research and development aimed at improving superconducting materials and their applications. This includes advancements in high-temperature superconductor (HTS) technology, which promises more practical and cost-effective solutions for widespread adoption.

Furthermore, there is considerable interest in how superconducting cables can facilitate the development of smart cities and advanced industrial applications, moving beyond traditional utility uses. The trends indicate a shift towards higher power density, reduced environmental footprint, and the potential for these cables to revolutionize areas such as data centers, electric transportation infrastructure, and specialized industrial processes. The strategic importance of superconducting technology in achieving national energy security and sustainability goals is also a recurring theme, highlighting governmental and institutional support as a critical market driver.

- Growing demand for energy efficient power transmission and distribution.

- Increased integration of renewable energy sources requiring high-capacity grid connections.

- Rapid advancements in high-temperature superconductor (HTS) materials and cooling technologies.

- Modernization of aging power grids and development of smart grid infrastructure.

- Expanding applications beyond utilities, including industrial, commercial, and defense sectors.

- Emphasis on reducing transmission losses and enhancing grid resilience.

AI Impact Analysis on Superconducting Cable

User queries regarding the impact of Artificial Intelligence (AI) on the Superconducting Cable market often center on how AI can optimize the design, manufacturing, and operational phases of these advanced cables. There is a strong expectation that AI will play a pivotal role in accelerating material discovery and characterization, enabling the identification of novel superconducting compounds with improved properties. Furthermore, users are keen to understand how AI-driven simulations and predictive modeling can refine cable design, minimizing energy losses and enhancing overall performance even before physical prototypes are developed, thereby reducing R&D costs and time-to-market.

From an operational standpoint, AI's influence is anticipated in intelligent grid management systems that integrate superconducting cables. This includes real-time fault detection, predictive maintenance schedules for cryogenic systems, and optimizing power flow for maximum efficiency and stability across complex networks. Concerns often revolve around data privacy and the complexity of integrating sophisticated AI algorithms with existing infrastructure, but the overarching expectation is that AI will significantly enhance the reliability, efficiency, and economic viability of superconducting cable deployments, making them more attractive for widespread adoption in smart grid initiatives and other high-power applications.

- AI for accelerated discovery and optimization of new superconducting materials.

- Enhanced design and simulation through AI, improving cable performance and reducing R&D cycles.

- Predictive maintenance and fault detection in superconducting grid systems using AI algorithms.

- Optimized power flow and grid stability management facilitated by AI integration.

- AI-driven manufacturing process optimization, leading to improved quality and reduced production costs.

- Advanced data analysis for monitoring cryogenic systems and ensuring operational efficiency.

Key Takeaways Superconducting Cable Market Size & Forecast

User inquiries often seek concise summaries of the market's trajectory and what critical implications can be drawn from its projected growth. The primary takeaway is the significant expansion anticipated for the superconducting cable market, driven by its unparalleled energy efficiency and high power density capabilities, which address the escalating global demand for sustainable and resilient energy infrastructure. The substantial Compound Annual Growth Rate (CAGR) underscores the technology's readiness for broader adoption, moving from niche applications to becoming a more integral component of future power networks.

Another key insight is the increasing commercial viability, spurred by ongoing advancements in materials and cooling technologies that are steadily reducing the overall cost and complexity of deployment. This forecast highlights the strategic shift towards more efficient power transmission and distribution, emphasizing that superconducting cables are not merely an incremental improvement but a transformative technology poised to redefine grid capabilities. The market's growth signals a strong confidence in its ability to meet the challenges of integrating large-scale renewable energy, modernizing urban grids, and supporting the power requirements of advanced industrial and data center applications.

- The superconducting cable market is poised for robust expansion, reflecting its growing strategic importance in global energy infrastructure.

- Significant CAGR indicates increasing commercial viability and readiness for broader adoption of the technology.

- Advancements in high-temperature superconductors and cryogenic systems are key enablers for market growth.

- The technology offers unparalleled benefits in energy efficiency, reduced transmission losses, and increased power density.

- Key applications in grid modernization, renewable energy integration, and high-power density environments are driving demand.

Superconducting Cable Market Drivers Analysis

The superconducting cable market is propelled by a confluence of critical factors, primarily the global imperative for enhanced energy efficiency and the modernization of aging power grids. As conventional transmission and distribution systems face increasing strain from rising electricity demand and the integration of intermittent renewable sources, the superior characteristics of superconducting cables—namely, near-zero resistive losses and high power density—become exceptionally attractive. This capability to transmit significantly more power over smaller cross-sections with minimal energy waste aligns perfectly with environmental goals and the economic drive to reduce operational costs for utilities and large industrial consumers.

Moreover, the accelerating adoption of renewable energy technologies, such as large-scale wind and solar farms, often situated far from major consumption centers, necessitates efficient long-distance power transfer. Superconducting cables offer a highly efficient solution for connecting these remote generation sites to urban load centers, minimizing energy loss during transmission. Furthermore, the development of smart grid initiatives worldwide, aimed at creating more resilient, flexible, and responsive power networks, inherently relies on advanced infrastructure. Superconducting cables, with their capacity for enhanced fault current limitation and efficient power delivery in constrained urban environments, are becoming a cornerstone technology for these next-generation grids.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for energy efficiency and reduced transmission losses | +8.5% | Global, particularly developed economies (North America, Europe, East Asia) | 2025-2033 (Long-term) |

| Increasing integration of renewable energy into grid infrastructure | +7.0% | Europe, North America, Asia Pacific (China, India, Japan) | 2025-2033 (Mid to Long-term) |

| Modernization and expansion of smart grid initiatives | +6.5% | North America, Europe, Asia Pacific (South Korea, China) | 2025-2030 (Mid-term) |

| Rising power consumption and urbanization globally | +5.5% | Asia Pacific (China, India), Latin America, Africa | 2025-2033 (Long-term) |

Superconducting Cable Market Restraints Analysis

Despite the inherent advantages of superconducting cables, several significant restraints impede their widespread adoption and market growth. The most prominent challenge is the substantially high initial cost of deployment compared to conventional copper or aluminum cables. This high capital expenditure covers not only the advanced superconducting materials but also the complex cryogenic cooling systems and specialized installation procedures required to maintain the ultra-low operating temperatures. Such significant upfront investment can deter utilities and industrial operators, particularly in regions with limited budgets or where the economic benefits of energy savings are not immediately apparent over the long term.

Furthermore, the operational complexity and the need for continuous cryogenic cooling present considerable logistical and maintenance challenges. Maintaining temperatures near absolute zero, or even at higher cryogenic temperatures for HTS cables, requires reliable and energy-intensive refrigeration systems. Any failure in these systems can lead to a loss of superconductivity, rendering the cable ineffective. This necessitates specialized technical expertise for installation, monitoring, and ongoing maintenance, which is not widely available globally. The relatively nascent stage of the technology, coupled with a lack of extensive long-term operational experience at scale, also contributes to a cautious approach from potential adopters, who often prefer proven and standardized solutions over innovative but complex alternatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial installation and capital expenditure costs | -4.0% | Global, particularly developing regions (Latin America, MEA) | 2025-2030 (Mid-term) |

| Complexity of cryogenic cooling systems and operational maintenance | -3.5% | Global, affecting project viability | 2025-2033 (Long-term) |

| Lack of standardized infrastructure and regulatory frameworks | -2.5% | Global, more pronounced in less regulated markets | 2025-2028 (Short to Mid-term) |

| Limited long-term operational experience and public perception barriers | -2.0% | Global, influencing adoption rates | 2025-2033 (Long-term) |

Superconducting Cable Market Opportunities Analysis

The superconducting cable market is presented with significant growth opportunities stemming from ongoing technological breakthroughs, particularly in high-temperature superconductor (HTS) materials. The development of HTS materials, capable of operating at relatively higher temperatures (e.g., liquid nitrogen temperature), drastically reduces the complexity and cost associated with cryogenic cooling compared to traditional low-temperature superconductors (LTS) that require liquid helium. This advancement broadens the applicability of superconducting cables, making them more commercially viable for a wider range of projects and facilitating easier integration into existing infrastructure. Continued research in this domain promises even higher operating temperatures and simplified cooling, further enhancing market potential.

Furthermore, substantial government funding and policy initiatives globally, aimed at grid modernization, renewable energy integration, and climate change mitigation, create a fertile ground for superconducting cable deployment. These policies often include incentives for energy-efficient technologies and investments in advanced infrastructure, providing crucial financial and regulatory support for high-cost, high-impact solutions like superconducting cables. Additionally, the expansion of superconducting cable applications beyond traditional utility transmission into new sectors, such as data centers requiring high power density in confined spaces, electric vehicle charging infrastructure, specialized industrial processes, and defense applications, represents a significant market diversification opportunity, unlocking previously untapped revenue streams and accelerating adoption.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in High-Temperature Superconductor (HTS) technology | +7.5% | Global, particularly R&D hubs (USA, Japan, Germany, China) | 2025-2033 (Long-term) |

| Government funding and policies supporting grid modernization and green energy | +6.0% | Europe (EU Green Deal), North America (Infrastructure Bill), Asia Pacific (China's 5-year plans) | 2025-2030 (Mid-term) |

| Expansion into new applications like data centers, EVs, and industrial motors | +5.0% | Global, high-density urban areas, industrial zones | 2028-2033 (Mid to Long-term) |

| Potential for retrofitting and upgrading existing power infrastructure | +4.0% | Developed economies with aging grids (USA, Europe) | 2025-2033 (Long-term) |

Superconducting Cable Market Challenges Impact Analysis

The superconducting cable market faces several distinct challenges that could temper its growth trajectory and adoption rate. A primary concern revolves around the technical complexity and scalability of manufacturing long lengths of superconducting wire with consistent quality. The fabrication process for HTS materials is intricate, requiring precise control over material composition and crystalline structure, which can be difficult to replicate reliably at industrial scales. Ensuring uniformity over kilometers of cable length is essential for performance and reliability, yet remains a significant hurdle, potentially limiting the volume of deployment and increasing production costs.

Furthermore, the maintenance and repair of superconducting cable systems present unique challenges. Unlike conventional cables, superconducting systems involve cryogenic components that require specialized equipment and highly trained personnel for any intervention. Fault localization, diagnosis, and repair in a cryogenic environment are complex and time-consuming processes, potentially leading to extended downtime and higher operational expenses. Overcoming these technical and logistical barriers requires substantial investment in training, infrastructure, and advanced diagnostic tools. Additionally, the relatively higher cost of superconducting cables compared to traditional alternatives continues to be a barrier, especially for projects where the long-term energy savings do not immediately offset the higher initial capital outlay, leading to a slower return on investment and a preference for established, lower-cost solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Manufacturing scalability and consistency of superconducting materials | -3.0% | Global, affecting production capacity | 2025-2030 (Mid-term) |

| Complex maintenance and repair procedures requiring specialized expertise | -2.5% | Global, impacting operational costs | 2025-2033 (Long-term) |

| High installation costs and competition from mature conventional technologies | -2.0% | Global, especially in cost-sensitive markets | 2025-2028 (Short to Mid-term) |

| Public and stakeholder skepticism regarding new, complex power technologies | -1.5% | Global, affecting adoption rates in conservative sectors | 2025-2033 (Long-term) |

Superconducting Cable Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Superconducting Cable Market, encompassing historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The scope extends to a detailed examination of technological advancements, particularly in High-Temperature Superconductors (HTS), and their impact on market evolution. Furthermore, the report profiles key industry players, offering an understanding of the competitive landscape and strategic developments shaping the global market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 250 million |

| Market Forecast in 2033 | USD 1,825 million |

| Growth Rate | 27.5% |

| Number of Pages | 267 |

| Key Trends | >|

| Segments Covered | >|

| Key Companies Covered | Sumitomo Electric Industries, Ltd., Nexans SA, Furukawa Electric Co., Ltd., LS Cable & System Ltd., SuperPower Inc. (a subsidiary of Furukawa Electric Co., Ltd.), American Superconductor Corporation (AMSC), Fujikura Ltd., Southwire Company, LLC, Hyper Tech Research, Inc., Theva Dunnschichttechnik GmbH, Bruker Corporation, Siemens AG, ABB Ltd., General Electric Company, Parker Hannifin Corporation, Cryogenic Industries, Inc., Tokai Carbon Co., Ltd., Japan Superconductor Technology, Inc., STI Optronics, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Superconducting Cable Market is comprehensively segmented to provide a nuanced understanding of its various facets, enabling stakeholders to identify specific growth areas and market dynamics. These segmentations are crucial for analyzing product adoption rates, technological preferences, and demand patterns across different applications and end-user industries. The market is primarily divided by type, distinguishing between Low Temperature Superconductors (LTS) and High Temperature Superconductors (HTS), reflecting the evolution of material science and their respective operational requirements and cost implications. LTS cables, while offering superior performance, demand more complex and expensive cooling, whereas HTS cables are gaining traction due to their more manageable cryogenic requirements.

Further segmentation by application highlights the diverse utility of superconducting cables across the power infrastructure. Key applications include high-capacity power transmission over long distances, efficient power distribution within urban grids, and the critical role of Fault Current Limiters (FCLs) in enhancing grid stability and protecting equipment from surge currents. Beyond traditional utilities, the market is also segmented by end-use industry, encompassing industrial sectors requiring high-power density solutions, commercial establishments like data centers, and the burgeoning field of research and development. Voltage level segmentation further refines the market view, categorizing cables into low, medium, and high voltage applications, which directly correlates with their suitability for different parts of the power grid and specialized industrial needs.

- By Type: Low Temperature Superconductors (LTS), High Temperature Superconductors (HTS)

- By Application: Power Transmission, Power Distribution, Fault Current Limiters (FCLs), Transformers, Motors and Generators, Others (e.g., Industrial, Medical, Defense)

- By End-Use Industry: Utilities, Industrial (e.g., Manufacturing, Heavy Industry), Commercial (e.g., Data Centers, Hospitals), Research and Development

- By Voltage Level: Low Voltage (Below 1 kV), Medium Voltage (1 kV to 36 kV), High Voltage (Above 36 kV)

Regional Highlights

- North America: A leading region driven by substantial investments in grid modernization, smart grid initiatives, and the integration of large-scale renewable energy projects. Government support and a strong research and development ecosystem contribute significantly to market growth. The focus is on enhancing grid resilience and efficiency in dense urban areas and remote generation sites.

- Europe: Characterized by ambitious green energy targets and widespread adoption of smart grid technologies under initiatives like the EU Green Deal. European countries are at the forefront of demonstrating superconducting cable projects for urban power distribution and inter-country grid connections, emphasizing energy efficiency and carbon footprint reduction.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid industrialization, urbanization, and increasing electricity demand, particularly in China, Japan, and South Korea. Significant government investments in advanced power infrastructure and smart cities, coupled with growing domestic research and manufacturing capabilities, are propelling the market forward.

- Latin America: An emerging market with growing awareness and potential for superconducting cable adoption, primarily driven by increasing energy demand, infrastructure development, and a push for more efficient power networks in developing economies.

- Middle East and Africa (MEA): Represents a nascent but promising market, spurred by large-scale infrastructure projects, diversification from fossil fuels, and investments in renewable energy. Opportunities exist for developing new, highly efficient power grids from the ground up.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Superconducting Cable Market.- Sumitomo Electric Industries, Ltd.

- Nexans SA

- Furukawa Electric Co., Ltd.

- LS Cable & System Ltd.

- SuperPower Inc. (a subsidiary of Furukawa Electric Co., Ltd.)

- American Superconductor Corporation (AMSC)

- Fujikura Ltd.

- Southwire Company, LLC

- Hyper Tech Research, Inc.

- Theva Dunnschichttechnik GmbH

- Bruker Corporation

- Siemens AG

- ABB Ltd.

- General Electric Company

- Parker Hannifin Corporation

- Cryogenic Industries, Inc.

- Tokai Carbon Co., Ltd.

- Japan Superconductor Technology, Inc.

- STI Optronics, Inc.

Frequently Asked Questions

Analyze common user questions about the Superconducting Cable market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are superconducting cables?

Superconducting cables are advanced electrical cables that can transmit electricity with virtually no energy loss when cooled to extremely low temperatures. They utilize superconducting materials that exhibit zero electrical resistance below a critical temperature, offering superior power transmission capacity and efficiency compared to conventional copper or aluminum cables.

How do superconducting cables improve energy efficiency?

By eliminating electrical resistance, superconducting cables drastically reduce energy losses during transmission and distribution, which can be as high as 6-8% in traditional grids. This leads to substantial energy savings, lower operational costs for utilities, and a reduced carbon footprint, making them highly efficient for modern power networks.

What are the main applications of superconducting cables?

Superconducting cables are primarily used in power transmission and distribution for grid modernization, integrating renewable energy sources, and urban power delivery where space is limited. They also find applications in Fault Current Limiters (FCLs) for grid stability, high-power industrial applications, data centers, and specialized defense or research projects.

What are the primary challenges in adopting superconducting cables?

Key challenges include the high initial capital expenditure compared to conventional cables, the complexity and cost of maintaining cryogenic cooling systems, and the need for specialized expertise for installation and maintenance. Additionally, scalability in manufacturing long lengths of high-quality superconducting wire and a lack of widespread standardization are ongoing hurdles.

What is the future outlook for the superconducting cable market?

The outlook is highly positive, with significant growth projected due to continuous advancements in high-temperature superconductor (HTS) materials, increasing global demand for energy efficiency, and substantial investments in smart grid infrastructure and renewable energy integration. As costs decrease and technology matures, superconducting cables are poised for broader adoption in diverse applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted