Ferro Titanium Market

Ferro Titanium Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704165 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Ferro Titanium Market Size

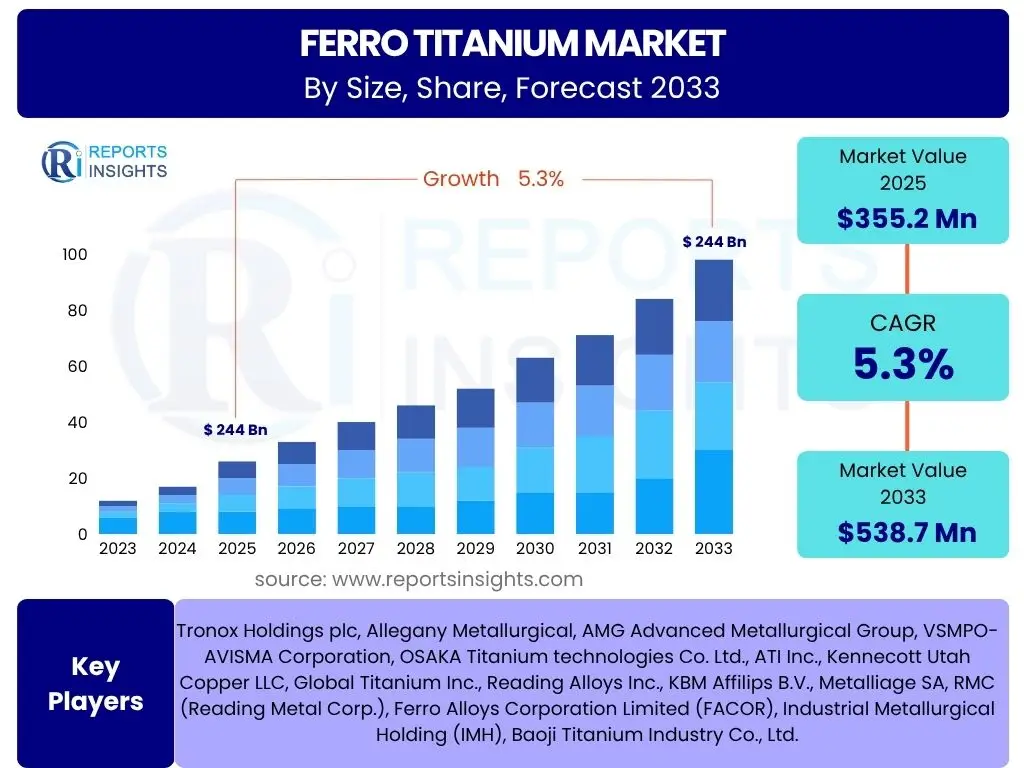

According to Reports Insights Consulting Pvt Ltd, The Ferro Titanium Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.3% between 2025 and 2033. The market is estimated at USD 355.2 Million in 2025 and is projected to reach USD 538.7 Million by the end of the forecast period in 2033. This growth is primarily driven by the increasing demand from the steel industry, particularly for high-strength low-alloy (HSLA) steels and stainless steels, where ferro titanium acts as a crucial deoxidizer, denitrifier, and grain refiner. The expansion of end-use industries such as aerospace, automotive, and chemical processing also contributes significantly to this projected market expansion.

The market's trajectory is also influenced by global industrial output and infrastructure development projects. As economies worldwide recover and invest in new construction, transportation, and manufacturing capacities, the need for advanced metallurgical products, including ferro titanium, is expected to rise. Furthermore, the growing focus on lightweight and high-performance materials in critical applications will sustain demand, fostering consistent growth throughout the forecast period. The strategic importance of ferro titanium in improving material properties and manufacturing efficiency underscores its stable position in the industrial materials market.

Key Ferro Titanium Market Trends & Insights

The Ferro Titanium market is currently shaped by several significant trends reflecting evolving industrial demands and technological advancements. A primary trend is the escalating adoption of ferro titanium in high-performance alloy production, driven by the aerospace, defense, and automotive sectors' continuous need for lighter, stronger, and more corrosion-resistant materials. This push for advanced materials directly influences demand for ferro titanium as a critical additive. Additionally, there is a noticeable shift towards sustainable and efficient production methods within the steel and alloy manufacturing industries, prompting companies to optimize their material inputs, including ferro titanium, for better resource utilization and reduced environmental impact. The global emphasis on decarbonization and circular economy principles is encouraging innovations in ferro titanium production and recycling, further shaping market dynamics.

Another crucial insight points to the increasing geographical diversification of manufacturing hubs. While traditional industrial powerhouses in North America and Europe remain significant consumers, emerging economies in Asia Pacific, particularly China and India, are demonstrating robust growth in steel production and associated industries, becoming major demand centers for ferro titanium. This regional shift impacts supply chain strategies and investment patterns within the market. Furthermore, advancements in additive manufacturing (3D printing) are slowly beginning to explore novel applications for titanium and its alloys, which could indirectly influence the long-term demand for ferro titanium as a precursor or alloying element, albeit still in nascent stages.

- Growing demand from high-performance alloy sectors (aerospace, defense, automotive).

- Increased focus on sustainable and efficient material production in metallurgy.

- Geographical diversification of demand, with significant growth in Asia Pacific.

- Exploration of ferro titanium in advanced manufacturing techniques like additive manufacturing.

- Rising adoption in specialty steel grades for improved material properties.

AI Impact Analysis on Ferro Titanium

Artificial intelligence (AI) is poised to exert a transformative influence across various facets of the Ferro Titanium market, primarily by enhancing operational efficiencies, optimizing supply chain management, and accelerating research and development. Users commonly inquire about how AI can mitigate the volatility in raw material prices or improve production predictability. AI-powered predictive analytics can forecast demand and supply fluctuations with greater accuracy, allowing manufacturers to optimize inventory levels, negotiate better raw material procurement deals, and minimize waste. Furthermore, machine learning algorithms can analyze vast datasets from production lines to identify anomalies, predict equipment failures, and suggest optimal process parameters, leading to reduced downtime and improved energy efficiency in ferro titanium smelting and alloy manufacturing.

Beyond operational improvements, AI also holds significant potential for innovation in material science relevant to ferro titanium. Researchers are exploring AI and machine learning to design novel alloys with specific properties, predict material behaviors under different conditions, and streamline the discovery of new applications for titanium and its ferroalloys. This capability could shorten development cycles for new products and enhance the competitive edge of market players. While direct AI integration into ferro titanium production remains in its early stages for many smaller players, the overarching trend toward digitalization across the industrial sector implies that AI will increasingly become a tool for strategic decision-making, quality control, and market analysis, thereby indirectly but significantly impacting the Ferro Titanium market's efficiency and growth potential.

- Supply chain optimization through AI-driven demand forecasting and logistics.

- Enhanced production efficiency and quality control via predictive maintenance and process optimization.

- Accelerated R&D for new ferro titanium alloys and applications.

- Improved raw material procurement strategies and cost management.

- Data-driven decision-making for market trend analysis and strategic planning.

Key Takeaways Ferro Titanium Market Size & Forecast

The Ferro Titanium market is on a robust growth trajectory, driven by its indispensable role in enhancing the properties of various steel grades and high-performance alloys. A key takeaway is the sustained demand from the steel manufacturing sector, particularly for stainless steel, high-strength low-alloy (HSLA) steels, and other specialty steels that require improved strength, ductility, and corrosion resistance. The forecast indicates that this foundational demand will continue to be the primary growth engine, underscoring ferro titanium's critical function in modern metallurgy. The market's resilience is also attributed to its diverse application base, extending beyond traditional steelmaking to include aerospace, automotive, and chemical processing industries, all of which are undergoing periods of innovation and expansion.

Another significant insight derived from the market size and forecast is the strategic importance of regional industrial growth, especially in emerging economies. Asia Pacific, led by China and India, is expected to remain a dominant force in terms of both production and consumption, reflecting its rapid industrialization and burgeoning manufacturing capabilities. This geographical shift necessitates flexible supply chain strategies and localized market approaches for key players. Furthermore, the increasing global emphasis on lightweighting and performance enhancement in end-user products means that ferro titanium will continue to be a material of choice for engineers and manufacturers aiming to meet stringent performance and efficiency standards. The long-term outlook for the ferro titanium market remains positive, underpinned by continuous technological advancements and expanding industrial applications worldwide.

- Consistent growth driven by steel manufacturing, especially specialty and high-strength steels.

- Diversified application base in aerospace, automotive, and chemical sectors ensuring market stability.

- Asia Pacific emerging as a significant growth engine due to rapid industrialization.

- Ferro titanium's critical role in lightweighting and performance enhancement materials.

- Positive long-term outlook supported by ongoing technological advancements and industrial expansion.

Ferro Titanium Market Drivers Analysis

The Ferro Titanium market is propelled by a confluence of factors, primarily the increasing global demand for high-performance and specialty steels. Ferro titanium is a vital additive in steelmaking, enhancing properties such as grain refinement, deoxidation, and nitrogen stabilization, which are crucial for producing advanced steel grades used in critical applications. The rapid expansion of industries like aerospace, where lightweight and strong materials are paramount for fuel efficiency and structural integrity, significantly contributes to this demand. Similarly, the automotive sector's continuous drive for lighter vehicles to meet stringent emission standards and improve fuel economy directly translates into a higher consumption of ferro titanium for high-strength steel components.

Beyond these key industrial applications, the growing investment in infrastructure projects worldwide, including bridges, buildings, and transportation networks, fuels the demand for durable and corrosion-resistant steel, indirectly boosting the ferro titanium market. Emerging economies are particularly active in this area, creating new avenues for market expansion. Furthermore, technological advancements in metallurgy continually seek to refine material properties, making ferro titanium an indispensable component in the development of new alloys and improving the efficiency of existing production processes. This ongoing innovation ensures a sustained demand for ferro titanium as manufacturers strive for superior product quality and operational excellence.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Strength Low-Alloy (HSLA) Steels | +1.8% | Global, particularly Asia Pacific & North America | 2025-2033 |

| Growth in Aerospace & Defense Industry | +1.5% | North America, Europe, China | 2025-2033 |

| Expansion of Automotive Sector and Lightweighting Trends | +1.2% | Global, with emphasis on Germany, Japan, US, China | 2025-2033 |

| Rising Infrastructure Development Projects | +0.8% | Asia Pacific, Latin America, Middle East | 2025-2033 |

| Technological Advancements in Metallurgy | +0.5% | Global | 2025-2033 |

Ferro Titanium Market Restraints Analysis

Despite its robust growth potential, the Ferro Titanium market faces certain restraints that could temper its expansion. One of the primary challenges is the volatility of raw material prices, particularly titanium ore (ilmenite and rutile) and ferroalloys. Fluctuations in the cost of these essential inputs can significantly impact the production costs of ferro titanium, leading to unpredictable pricing for end-users and potentially affecting demand stability. Geopolitical tensions and trade policies can further exacerbate these price swings, disrupting global supply chains and creating uncertainty for market participants. Manufacturers must navigate these external factors carefully to maintain profitability and competitive pricing.

Another significant restraint is the high energy consumption associated with the production of ferro titanium. The smelting process is energy-intensive, making production costs highly susceptible to changes in energy prices. This not only affects the economic viability of production but also raises environmental concerns regarding carbon emissions. Strict environmental regulations in various regions are compelling manufacturers to invest in cleaner technologies and more efficient processes, adding to operational expenditures. Furthermore, the availability of substitute materials, though limited for some specific applications, could pose a long-term challenge if alternative alloying elements emerge that offer comparable performance at lower costs or with easier processing. The market must also contend with the cyclical nature of the steel industry, which is the largest consumer of ferro titanium, as economic downturns can lead to reduced steel production and, consequently, lower demand for ferro titanium.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Titanium Ore) | -1.2% | Global | 2025-2033 |

| High Energy Consumption in Production | -0.9% | Global, particularly Europe & Asia | 2025-2033 |

| Environmental Regulations and Compliance Costs | -0.7% | Europe, North America, China | 2025-2033 |

| Economic Downturns Affecting Steel Industry | -0.5% | Global | Short to Medium-Term (2025-2028) |

| Availability of Substitute Materials (limited) | -0.3% | Global | Long-Term (2029-2033) |

Ferro Titanium Market Opportunities Analysis

The Ferro Titanium market is presented with several promising opportunities that could accelerate its growth beyond current projections. A significant opportunity lies in the expanding applications of titanium-containing alloys in emerging fields such as additive manufacturing (3D printing). As industries increasingly adopt 3D printing for complex components, the demand for high-quality metal powders and precursors, including those derived from ferro titanium, is expected to grow. This technological shift opens new avenues for ferro titanium producers to diversify their product portfolios and target niche, high-value markets. Furthermore, the global push towards decarbonization and sustainable manufacturing practices creates an opportunity for ferro titanium producers to innovate in greener production methods, potentially attracting environmentally conscious customers and investors.

Another key opportunity stems from the growing focus on circular economy principles, particularly the recycling of titanium-containing scrap. Developing more efficient and economically viable methods for recovering titanium from end-of-life products could create a sustainable source of raw material, reducing reliance on virgin ore and mitigating price volatility. This also aligns with corporate sustainability goals and government regulations promoting resource efficiency. Additionally, the continuous research and development into new material composites and advanced metallurgical processes could unlock novel applications for ferro titanium in unforeseen industries, broadening its market reach. Partnerships and collaborations across the value chain, from raw material suppliers to end-use manufacturers, can also foster innovation and create synergistic growth opportunities, particularly in developing customized ferro titanium grades for specialized applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Additive Manufacturing (3D Printing) | +1.5% | North America, Europe, Asia Pacific | 2027-2033 |

| Advancements in Recycling and Circular Economy Initiatives | +1.0% | Global, particularly Europe & Japan | 2026-2033 |

| Development of New Alloys and Composite Materials | +0.8% | Global Research Hubs | 2025-2033 |

| Increasing Demand for High-Purity Ferro Titanium Grades | +0.6% | Global | 2025-2033 |

| Expansion in Non-Traditional Industrial Uses | +0.5% | Emerging Markets | 2028-2033 |

Ferro Titanium Market Challenges Impact Analysis

The Ferro Titanium market faces a number of challenges that could impede its growth and operational stability. Intense competition among existing players, coupled with the potential entry of new market participants, can lead to price wars and reduced profit margins. This competitive landscape necessitates continuous innovation and differentiation to maintain market share. Furthermore, the industry is vulnerable to disruptions in the global supply chain, often triggered by geopolitical events, natural disasters, or pandemics. Such disruptions can affect the availability of raw materials, delay shipments, and increase logistics costs, directly impacting production schedules and profitability for manufacturers of ferro titanium.

Another significant challenge is the capital-intensive nature of ferro titanium production. Establishing and maintaining production facilities requires substantial investment in infrastructure, equipment, and technology, posing a barrier to entry for new players and a significant operational cost for existing ones. Additionally, stringent quality control standards are essential, especially for aerospace and defense applications, which demand high purity and precise chemical compositions. Meeting these rigorous specifications requires advanced testing facilities and highly skilled personnel, adding to operational complexities and costs. The fluctuating demand from end-user industries, particularly the cyclical steel market, also presents a challenge, requiring manufacturers to maintain flexible production capacities and inventory management strategies to adapt to varying market conditions effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressures | -1.0% | Global | 2025-2033 |

| Supply Chain Disruptions and Geopolitical Risks | -0.8% | Global | Short to Medium-Term (2025-2028) |

| High Capital Expenditure and Operational Costs | -0.7% | Global | 2025-2033 |

| Stringent Quality Control and Certification Requirements | -0.5% | North America, Europe, Japan | 2025-2033 |

| Fluctuating Demand from End-User Industries | -0.4% | Global | 2025-2033 |

Ferro Titanium Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Ferro Titanium market, offering detailed insights into its size, trends, drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of market dynamics across various segments, including type, application, and end-use industry, alongside a robust regional analysis. The report aims to furnish stakeholders with actionable intelligence to make informed strategic decisions, identify key growth avenues, and understand the competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 355.2 Million |

| Market Forecast in 2033 | USD 538.7 Million |

| Growth Rate | 5.3% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Tronox Holdings plc, Allegany Metallurgical, AMG Advanced Metallurgical Group, VSMPO-AVISMA Corporation, OSAKA Titanium technologies Co. Ltd., ATI Inc., Kennecott Utah Copper LLC, Global Titanium Inc., Reading Alloys Inc., KBM Affilips B.V., Metalliage SA, RMC (Reading Metal Corp.), Ferro Alloys Corporation Limited (FACOR), Industrial Metallurgical Holding (IMH), Baoji Titanium Industry Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ferro Titanium market is comprehensively segmented to provide a detailed understanding of its dynamics across various dimensions, reflecting the diverse forms and applications of this crucial alloy. Segmentation by type differentiates between High Carbon Ferro Titanium, Low Carbon Ferro Titanium, and Medium Carbon Ferro Titanium, each offering distinct properties that cater to specific metallurgical requirements. High Carbon grades are typically used where a higher carbon content is acceptable or desirable in the final alloy, while Low Carbon grades are preferred for applications demanding precise carbon control, often in stainless steels.

Further segmentation by application highlights the primary end-uses of ferro titanium. Steel manufacturing dominates this segment, with sub-categories including stainless steel, high-strength low-alloy (HSLA) steel, and tool steel production, where ferro titanium acts as a deoxidizer, denitrifier, and grain refiner. Beyond steel, significant applications exist in the aerospace and defense industries for high-performance alloys, the automotive sector for lightweighting, and the chemical processing industry for corrosion resistance. The segmentation by end-use industry then categorizes the broader sectors consuming ferro titanium, such as metallurgy, aerospace, automotive, marine, construction, and chemicals, offering a holistic view of the market's reach and impact across the global industrial landscape.

- By Type:

- High Carbon Ferro Titanium

- Low Carbon Ferro Titanium

- Medium Carbon Ferro Titanium

- Other Grades (e.g., Vacuum Grade)

- By Application:

- Steel Manufacturing

- Stainless Steel

- High Strength Low Alloy Steel

- Tool Steel

- Other Steel Grades

- Aerospace & Defense

- Automotive Industry

- Chemical Processing

- Marine Applications

- Brazing & Welding Consumables

- Others

- Steel Manufacturing

- By End-Use Industry:

- Metallurgy

- Chemicals

- Aerospace

- Automotive

- Marine

- Construction

- Medical

- Consumer Goods

Regional Highlights

The global Ferro Titanium market exhibits distinct regional dynamics, with certain geographies playing a pivotal role in both production and consumption. Asia Pacific stands as the largest and fastest-growing market, primarily driven by rapid industrialization, burgeoning steel production, and significant infrastructure development in countries like China and India. China, in particular, is a dominant force due to its vast manufacturing base and continuous expansion in steel and alloy production, while India's rising automotive and construction sectors contribute substantially to regional demand. The region's increasing focus on advanced manufacturing and economic growth further cements its leading position in the ferro titanium market.

North America and Europe also hold substantial market shares, characterized by mature industrial sectors and a strong emphasis on high-performance materials. In North America, the robust aerospace and defense industries, coupled with a resurgent automotive sector, are key drivers for ferro titanium demand. The United States, with its extensive manufacturing capabilities and ongoing investments in advanced materials, remains a critical market. Similarly, Europe, with countries like Germany and France at the forefront of automotive and aerospace manufacturing, maintains a steady demand for ferro titanium. The region's stringent environmental regulations also foster innovation in cleaner production processes and high-efficiency material applications. Latin America and the Middle East & Africa are emerging markets, displaying gradual growth spurred by infrastructure development and nascent industrial expansion, contributing to the diversified global consumption landscape for ferro titanium.

- Asia Pacific: Dominant market, driven by China and India's extensive steel production, automotive, and construction sectors. High growth due to rapid industrialization.

- North America: Significant market share, propelled by robust aerospace, defense, and automotive industries. Strong emphasis on high-performance alloys in the United States and Canada.

- Europe: Mature market with steady demand from Germany, France, and the UK, supported by advanced manufacturing in automotive, aerospace, and specialty steel.

- Latin America: Emerging market with growth tied to infrastructure development and industrial expansion in countries like Brazil and Mexico.

- Middle East & Africa (MEA): Gradually growing market influenced by industrialization efforts, particularly in the construction and oil & gas sectors in countries like Saudi Arabia and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ferro Titanium Market.- Tronox Holdings plc

- Allegany Metallurgical

- AMG Advanced Metallurgical Group

- VSMPO-AVISMA Corporation

- OSAKA Titanium technologies Co. Ltd.

- ATI Inc.

- Kennecott Utah Copper LLC

- Global Titanium Inc.

- Reading Alloys Inc.

- KBM Affilips B.V.

- Metalliage SA

- RMC (Reading Metal Corp.)

- Ferro Alloys Corporation Limited (FACOR)

- Industrial Metallurgical Holding (IMH)

- Baoji Titanium Industry Co., Ltd.

- Rusal

- GfE Metalle und Materialien GmbH

- C. Steinweg (S.A.) (Pty) Ltd.

- W. R. Grace & Co.

- American Elements

Frequently Asked Questions

Analyze common user questions about the Ferro Titanium market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Ferro Titanium primarily used for?

Ferro Titanium is primarily used as an alloying agent and deoxidizer in steel manufacturing, especially for producing stainless steel, high-strength low-alloy (HSLA) steels, and other specialty steels, where it enhances strength, ductility, and corrosion resistance. It also finds applications in aerospace, automotive, and chemical processing industries.

What are the main types of Ferro Titanium available in the market?

The main types of Ferro Titanium available are High Carbon Ferro Titanium, Low Carbon Ferro Titanium, and Medium Carbon Ferro Titanium, distinguished by their carbon content which influences their specific applications in metallurgy.

Which regions are leading the demand for Ferro Titanium?

Asia Pacific, particularly China and India, is currently the largest and fastest-growing region for Ferro Titanium demand due to extensive steel production and rapid industrialization. North America and Europe also maintain significant demand from their advanced manufacturing sectors.

How do raw material prices affect the Ferro Titanium market?

Raw material prices, especially for titanium ore, are a significant restraint on the Ferro Titanium market. Volatility in these prices directly impacts production costs, influencing market pricing and potentially affecting demand stability and profitability for manufacturers.

What impact does AI have on the Ferro Titanium industry?

AI impacts the Ferro Titanium industry by enhancing supply chain optimization through predictive analytics, improving production efficiency via predictive maintenance, and accelerating research and development for new alloys. It primarily contributes to operational improvements and strategic decision-making.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted