Ferro Chrome Market

Ferro Chrome Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702820 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Ferro Chrome Market Size

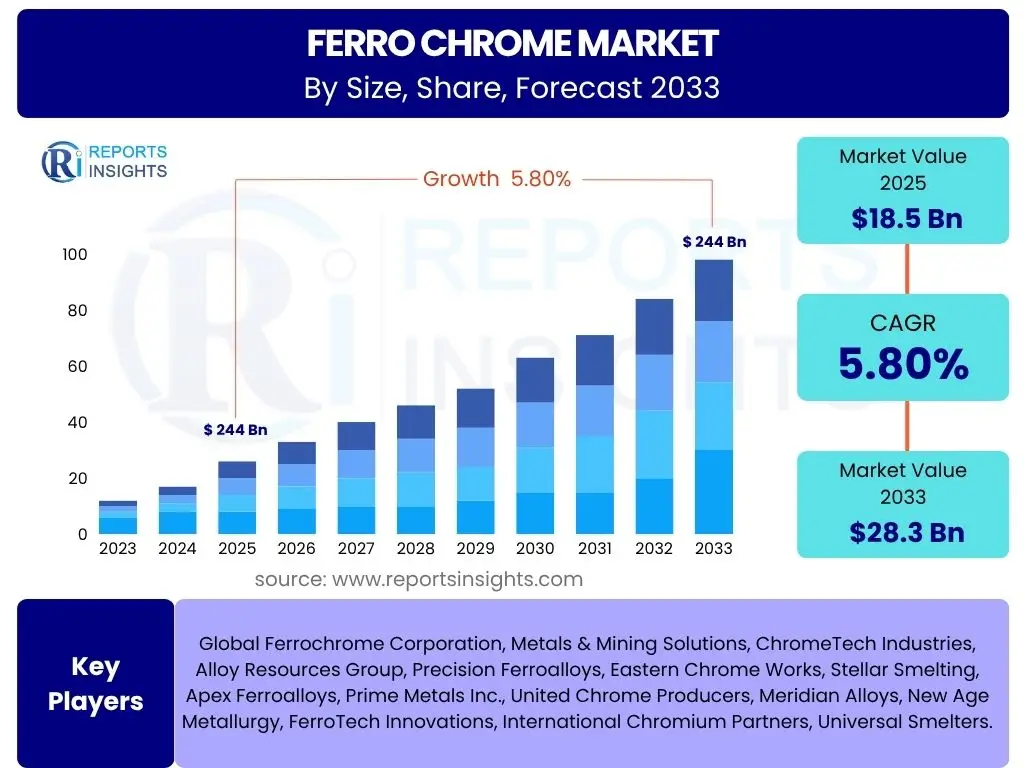

According to Reports Insights Consulting Pvt Ltd, The Ferro Chrome Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 18.5 billion in 2025 and is projected to reach USD 28.3 billion by the end of the forecast period in 2033.

Key Ferro Chrome Market Trends & Insights

The Ferro Chrome market is significantly shaped by the evolving dynamics of the global stainless steel industry, which accounts for the vast majority of ferro chrome consumption. A prominent trend observed is the increasing demand for high-performance and specialty stainless steel grades, driven by sectors such as automotive, construction, and infrastructure development. This shift necessitates higher quality and specific types of ferro chrome, pushing producers towards more advanced manufacturing processes and product diversification. Furthermore, the market is experiencing a growing emphasis on energy efficiency and sustainable production practices, as environmental regulations become stricter and industries strive to reduce their carbon footprint.

Another crucial insight is the impact of urbanization and industrialization in emerging economies, particularly in Asia Pacific, which continues to be the largest consumer and producer of ferro chrome. The rapid expansion of manufacturing capabilities and infrastructure projects in countries like China and India fuels a consistent demand for steel and, consequently, ferro chrome. Geopolitical factors and trade policies also play a significant role, influencing supply chains and pricing stability. Producers are increasingly investing in backward integration, securing raw material supplies, and optimizing logistics to mitigate these external risks and maintain competitive advantages.

Technological advancements in ferro chrome production, such as improved smelting processes and raw material beneficiation, are contributing to enhanced operational efficiency and reduced production costs. There is also a growing interest in circular economy principles, leading to research and development into recycling ferro chrome from waste streams, which could alleviate pressure on primary resources and offer new revenue streams. These trends collectively underscore a market that is dynamic, responsive to global economic shifts, and increasingly focused on sustainable and efficient production methods.

- Growing demand for stainless steel, especially in emerging economies.

- Increasing adoption of energy-efficient and sustainable production methods.

- Emphasis on high-performance and specialty ferro chrome grades.

- Impact of geopolitical factors and trade policies on supply chains.

- Advancements in smelting technologies and raw material processing.

- Rising focus on recycling and circular economy principles.

AI Impact Analysis on Ferro Chrome

Artificial Intelligence (AI) is beginning to exert a transformative influence on the ferro chrome industry, primarily through its application in optimizing operational efficiency and decision-making processes. Users frequently inquire about AI's potential to enhance various stages of the ferro chrome production lifecycle, from raw material sourcing and quality control to smelting operations and supply chain management. The core expectation is that AI can lead to significant cost reductions, improved product quality, and greater resource utilization. For instance, predictive analytics powered by AI can forecast equipment failures, enabling proactive maintenance and minimizing costly downtime in smelting plants. This capability is particularly appealing in an industry where capital expenditure on machinery is substantial and operational continuity is critical.

Beyond operational improvements, AI's role in supply chain optimization is a major area of interest. Users are keen on understanding how AI algorithms can analyze vast datasets to predict demand fluctuations, optimize inventory levels, and manage logistics more effectively. This allows for better alignment of production with market needs, reducing waste and improving responsiveness to customer orders. Furthermore, AI-driven data analysis can provide deeper insights into market trends, enabling more informed strategic planning and risk management for ferro chrome producers. The ability of AI to process and interpret complex data sets far beyond human capacity offers a distinct advantage in navigating the volatile commodity markets.

The impact of AI also extends to sustainability efforts within the ferro chrome industry. AI can be deployed to monitor and optimize energy consumption in energy-intensive smelting processes, leading to reduced greenhouse gas emissions and lower operational costs. Moreover, AI-powered quality control systems can precisely analyze raw material composition and final product purity, ensuring consistent quality and reducing off-spec production. While the adoption of AI in this traditional industry is still nascent, the anticipated benefits in efficiency, cost reduction, quality improvement, and environmental performance are driving increasing investment and research into its applications, addressing a wide range of user concerns regarding future competitiveness and operational excellence.

- Enhanced operational efficiency through predictive maintenance.

- Optimized raw material sourcing and quality control.

- Improved smelting process control and energy efficiency.

- Advanced supply chain management and demand forecasting.

- Data-driven decision-making for market strategy and risk assessment.

- Reduction in production waste and improvement in product consistency.

Key Takeaways Ferro Chrome Market Size & Forecast

Users frequently seek a concise summary of the most critical insights from the Ferro Chrome market size and forecast, aiming to grasp the overarching narrative of market health and future direction. A primary takeaway is the consistent and robust growth projected for the market, indicating underlying stability and increasing demand from its primary end-use sectors, particularly stainless steel. The anticipated expansion from USD 18.5 billion in 2025 to USD 28.3 billion by 2033, at a CAGR of 5.8%, signifies a healthy market trajectory driven by global industrialization, infrastructure development, and automotive sector advancements. This growth underscores ferro chrome's indispensable role in modern industrial applications, cementing its position as a vital alloy in high-performance materials.

Another key insight revolves around the regional dynamics shaping this growth. While global demand remains strong, the Asia Pacific region is expected to lead this expansion, fueled by continued urbanization and manufacturing growth in economies like China and India. This regional dominance necessitates strategic focus for market participants on supply chain resilience and localized production capabilities. Furthermore, the market's future will be heavily influenced by technological adoption, especially in areas like AI and automation, which promise to enhance efficiency and sustainability, thus mitigating some of the traditional challenges associated with energy-intensive production processes and volatile raw material prices.

Finally, the forecast highlights the increasing importance of environmental, social, and governance (ESG) factors. Industry stakeholders are increasingly prioritizing sustainable sourcing, energy-efficient production, and waste reduction. Companies that strategically integrate these considerations into their operations are better positioned for long-term growth and market acceptance. The market's resilience, coupled with strategic shifts towards efficiency and sustainability, suggests a mature yet evolving landscape where innovation and responsible practices will be crucial for sustained success and navigating future uncertainties.

- The Ferro Chrome market is poised for steady growth, driven by sustained demand from the stainless steel industry and global industrial expansion.

- Asia Pacific remains the dominant growth engine, propelled by infrastructure and manufacturing developments.

- Technological advancements, including AI, are crucial for enhancing operational efficiency and sustainability within the industry.

- Sustainability and ESG factors are increasingly influencing production methods and investment decisions.

- Market participants must focus on supply chain resilience and adapting to evolving regulatory landscapes.

Ferro Chrome Market Drivers Analysis

The global Ferro Chrome market is primarily driven by the robust and continuous demand from the stainless steel industry, which relies heavily on chromium for its corrosion resistance and aesthetic properties. As global population grows and urbanization accelerates, the need for new infrastructure, commercial buildings, and residential complexes increases, directly boosting the consumption of stainless steel in construction. Moreover, the automotive sector's evolving landscape, particularly the growing adoption of lightweight and high-strength steels to improve fuel efficiency and meet emissions standards, also contributes significantly to the demand for ferro chrome-containing alloys. This sustained consumption across diverse end-use sectors ensures a consistent baseline demand for ferro chrome, acting as a foundational growth driver.

Beyond traditional applications, the expansion of various manufacturing industries globally, including machinery and equipment, consumer goods, and energy sectors, further bolsters the market. These industries utilize stainless and alloy steels for components requiring durability, strength, and resistance to extreme conditions. Developing economies, in particular, are witnessing rapid industrialization and infrastructure projects, such as railway networks, bridges, and power plants, which are highly material-intensive and consequently drive up the demand for steel and its alloying elements like ferro chrome. The improving global economic outlook in many regions supports increased industrial activity, thereby creating a favorable environment for market expansion.

Furthermore, technological advancements in steel production and the increasing focus on specialty alloys for niche applications contribute to market growth. The development of advanced high-strength steels (AHSS) and other high-performance alloys for aerospace, defense, and renewable energy sectors requires precise compositions of ferro chrome, often in higher grades. Innovations in mining and smelting processes that make ferro chrome production more efficient and cost-effective also act as an indirect driver, enabling competitive pricing and broader market accessibility. These combined factors highlight a multifaceted driver landscape, underpinning the positive market outlook.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Stainless Steel Production | +2.5% | Global, especially APAC (China, India) | Long-term (2025-2033) |

| Infrastructure Development & Urbanization | +1.8% | Emerging Economies (ASEAN, India, Africa) | Medium to Long-term (2025-2033) |

| Increasing Automotive Production & Light-weighting Trends | +0.9% | North America, Europe, China | Medium-term (2025-2030) |

| Demand from Specialty Alloys & Foundries | +0.6% | Global | Long-term (2025-2033) |

Ferro Chrome Market Restraints Analysis

The Ferro Chrome market faces significant restraints, primarily stemming from the inherent volatility of raw material prices, particularly chrome ore and energy. Chrome ore, being a finite resource, is subject to supply disruptions, geopolitical tensions in major mining regions (like South Africa), and fluctuating demand from key consuming nations. Energy costs, especially electricity, constitute a substantial portion of ferro chrome production expenses, and their unpredictable nature can severely impact profitability and discourage new investments. These price fluctuations create an unstable operating environment, making long-term planning and consistent pricing strategies challenging for manufacturers, which can dampen overall market growth.

Environmental regulations and escalating concerns over the carbon footprint of industrial operations represent another major restraint. Ferro chrome production is energy-intensive and can generate significant greenhouse gas emissions, leading to increasing pressure from governments and environmental agencies to adopt cleaner technologies and reduce pollution. Compliance with stringent emission standards and waste disposal regulations often requires substantial capital investments in new equipment and processes, which can raise production costs and limit output for manufacturers, especially smaller players. Failure to comply can result in heavy fines or operational shutdowns, posing considerable risks to market participants.

Furthermore, trade barriers and protectionist policies implemented by various countries can disrupt global supply chains and restrict market access. Import tariffs, quotas, and anti-dumping duties can distort prices, reduce the competitiveness of imported ferro chrome, and lead to localized oversupply or undersupply. Geopolitical instability in key producing or consuming regions also poses a significant risk, potentially disrupting mining operations, transportation routes, and market stability. Such external factors introduce uncertainty and complexity into the global ferro chrome market, acting as formidable impediments to its unconstrained growth potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material & Energy Prices | -1.5% | Global | Long-term (2025-2033) |

| Stringent Environmental Regulations & Carbon Taxes | -1.2% | Europe, North America, China | Medium to Long-term (2025-2033) |

| Geopolitical Instability & Trade Protectionism | -0.8% | Global, specific trade blocs | Short to Medium-term (2025-2028) |

| High Capital Expenditure for New Production Facilities | -0.5% | Global | Long-term (2025-2033) |

Ferro Chrome Market Opportunities Analysis

The Ferro Chrome market is presented with significant opportunities, particularly from the burgeoning demand for specialized alloys in new and evolving industries. The rapid growth of the electric vehicle (EV) sector, for instance, requires advanced materials with superior strength-to-weight ratios and corrosion resistance for battery casings, structural components, and various automotive parts. These specialized alloys often contain higher proportions of chromium, creating a niche but high-value demand for ferro chrome. Similarly, the expansion of renewable energy infrastructure, including wind turbines and solar panel frameworks, necessitates durable and weather-resistant materials, further opening avenues for ferro chrome applications beyond traditional stainless steel.

Another substantial opportunity lies in the circular economy and the increasing focus on recycling. As industries strive for greater sustainability and resource efficiency, the recycling of stainless steel and other chromium-containing scraps offers a viable alternative to primary production. Innovations in recycling technologies that allow for efficient recovery of ferro chrome from end-of-life products can reduce dependence on virgin chrome ore, mitigate environmental impact, and potentially offer a more stable and cost-effective supply source. Companies investing in advanced recycling processes are positioned to capitalize on this growing trend, aligning with global sustainability objectives and potentially gaining a competitive edge.

Furthermore, the continued industrialization and urbanization in emerging economies present long-term growth opportunities. Regions such as Southeast Asia, Africa, and parts of Latin America are undergoing significant infrastructure development, construction booms, and expansion of their manufacturing bases. While China and India remain dominant, these burgeoning markets represent untapped potential for increased ferro chrome consumption as their industrial capabilities mature. Market players who strategically invest in these regions, by establishing local supply chains or partnerships, can secure future demand and diversify their revenue streams, harnessing the momentum of global economic shifts.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Specialty Alloys (EV, Renewable Energy) | +1.3% | Global | Long-term (2025-2033) |

| Advancements in Recycling & Circular Economy Initiatives | +1.0% | Europe, North America, Asia Pacific | Medium to Long-term (2025-2033) |

| Industrialization in Emerging Markets (beyond China/India) | +0.7% | Southeast Asia, Africa, Latin America | Long-term (2028-2033) |

| Technological Innovation in Production Processes | +0.5% | Global | Medium-term (2025-2030) |

Ferro Chrome Market Challenges Impact Analysis

The Ferro Chrome market faces significant challenges, primarily centered around ensuring the stability and security of its supply chain amidst geopolitical uncertainties and logistics complexities. The primary source of chrome ore, crucial for ferro chrome production, is highly concentrated in a few regions, making the supply chain vulnerable to political instability, labor disputes, or policy changes in these areas. Disruptions to mining operations or transportation networks can lead to severe raw material shortages and price spikes, impacting global production capabilities. Managing these supply chain risks requires extensive strategic planning and diversification efforts, which can be costly and time-consuming for market participants, adding a layer of operational complexity.

Another prominent challenge is the increasing pressure to reduce the carbon footprint and enhance energy efficiency in ferro chrome production. As an energy-intensive industry, producers are under scrutiny to adopt cleaner technologies and processes to meet increasingly stringent global climate targets. This necessitates significant capital investment in advanced furnaces, waste heat recovery systems, and potentially carbon capture technologies, which can inflate production costs and impact competitiveness, especially for older facilities. The transition to more sustainable production methods is not only a regulatory imperative but also a market expectation, requiring continuous innovation and substantial financial commitment.

Furthermore, the market grapples with the inherent cyclical nature of the steel industry, which directly influences ferro chrome demand. Economic downturns or slowdowns in key end-use sectors like construction and automotive can lead to a sudden decrease in demand, resulting in oversupply and downward pressure on prices. This cyclicality makes long-term investment planning challenging and can result in periods of reduced profitability for manufacturers. Companies must develop robust risk management strategies and maintain financial resilience to navigate these demand fluctuations and ensure sustainable operations in a highly sensitive commodity market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Risks & Supply Chain Disruptions | -1.0% | Global, particularly major producing regions | Short to Medium-term (2025-2028) |

| High Energy Consumption & Decarbonization Pressures | -0.9% | Europe, China, North America | Long-term (2025-2033) |

| Price Volatility & Market Cyclicality | -0.7% | Global | Short to Medium-term (2025-2029) |

| Intense Competition & Oversupply Concerns | -0.4% | Global | Medium-term (2025-2030) |

Ferro Chrome Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Ferro Chrome market, encompassing its historical performance, current dynamics, and future projections. The report offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It aims to equip stakeholders with actionable insights to navigate the evolving market landscape and make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 billion |

| Market Forecast in 2033 | USD 28.3 billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Ferrochrome Corporation, Metals & Mining Solutions, ChromeTech Industries, Alloy Resources Group, Precision Ferroalloys, Eastern Chrome Works, Stellar Smelting, Apex Ferroalloys, Prime Metals Inc., United Chrome Producers, Meridian Alloys, New Age Metallurgy, FerroTech Innovations, International Chromium Partners, Universal Smelters. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ferro Chrome market is comprehensively segmented to provide a granular understanding of its diverse components and drivers. These segmentations allow for a detailed analysis of consumption patterns, technological preferences, and end-use industry specific demands, offering critical insights for strategic market positioning. Understanding these distinct categories is essential for producers, suppliers, and investors to identify lucrative opportunities and tailor their offerings to specific market needs. The differentiation across types, applications, and end-use industries highlights the varying quality requirements and performance criteria for ferro chrome across its broad spectrum of uses.

- By Type:

- High Carbon Ferro Chrome: Primarily used in stainless steel production for its cost-effectiveness and high carbon content.

- Medium Carbon Ferro Chrome: Utilized when lower carbon content is desired, often in specialty steels.

- Low Carbon Ferro Chrome: Essential for producing super alloys and special steels where very low carbon content is critical to prevent carbide formation.

- Super Low Carbon Ferro Chrome: Employed in the most demanding applications requiring ultra-low carbon levels, such as aerospace and medical-grade alloys.

- By Application:

- Stainless Steel Production: The largest application, dominating consumption due to chromium's role in corrosion resistance and aesthetics.

- Alloy Steel Production: Used to enhance strength, hardness, and wear resistance in various alloy steels.

- Carbon Steel Production: Applied to improve certain properties of carbon steels, though in smaller quantities compared to stainless steel.

- Others (e.g., Foundry, Chemicals): Includes use in specialized castings, hardfacing applications, and chemical compounds.

- By End-Use Industry:

- Automotive: For lightweight, corrosion-resistant components and structural parts.

- Building & Construction: Extensive use in structural elements, facades, and interior fittings requiring durability and low maintenance.

- Machinery & Equipment: For manufacturing industrial machinery components, tools, and heavy equipment.

- Consumer Goods: Applied in appliances, kitchenware, and various consumer products for durability and aesthetic appeal.

- Energy: Utilized in power generation facilities, including components for renewable energy systems and traditional power plants.

- Other Manufacturing: Diverse applications across sectors like aerospace, defense, marine, and medical devices.

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market for Ferro Chrome, primarily driven by rapid industrialization, urbanization, and robust growth in the construction, automotive, and manufacturing sectors. China and India are the leading consumers and producers, fueled by massive infrastructure projects and expanding stainless steel industries. Significant investments in manufacturing capabilities across Southeast Asia further contribute to regional dominance.

- Europe: A mature market characterized by stringent environmental regulations and a focus on high-quality, specialty steel production. Demand is driven by the automotive, machinery, and energy sectors, with a strong emphasis on efficiency and sustainability in ferro chrome production processes. The region also plays a crucial role in research and development for advanced alloys.

- North America: Exhibits stable demand, primarily from the automotive, construction, and oil & gas industries. The region focuses on technological advancements in steel manufacturing and specialty alloy production, contributing to a consistent, albeit slower, growth rate compared to APAC. Environmental compliance and recycling initiatives are increasingly important factors.

- Latin America: An emerging market with significant potential, driven by developing infrastructure, mining, and automotive sectors in countries like Brazil and Mexico. The region offers opportunities for both consumption and potential raw material sourcing, though political and economic stability can influence market dynamics.

- Middle East and Africa (MEA): A region with substantial chrome ore reserves, particularly South Africa, making it a critical hub for ferro chrome production. While consumption within MEA is growing due to developing industries and construction, a significant portion of the production is geared towards exports. Economic diversification efforts and infrastructure projects are key drivers for internal demand growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ferro Chrome Market.- Global Ferrochrome Corporation

- Metals & Mining Solutions

- ChromeTech Industries

- Alloy Resources Group

- Precision Ferroalloys

- Eastern Chrome Works

- Stellar Smelting

- Apex Ferroalloys

- Prime Metals Inc.

- United Chrome Producers

- Meridian Alloys

- New Age Metallurgy

- FerroTech Innovations

- International Chromium Partners

- Universal Smelters

Frequently Asked Questions

What is Ferro Chrome and its primary use?

Ferro Chrome is an alloy of chromium and iron, produced by electric arc furnace reduction of chromite. Its primary use is as an alloying agent in the production of stainless steel, imparting corrosion resistance, strength, and durability.

What are the main types of Ferro Chrome?

The main types of Ferro Chrome include High Carbon Ferro Chrome (HCFC), Medium Carbon Ferro Chrome (MCFC), Low Carbon Ferro Chrome (LCFC), and Super Low Carbon Ferro Chrome (SLCFC), distinguished by their carbon content and suitability for various steel grades.

Which region dominates the Ferro Chrome market?

The Asia Pacific region, particularly China and India, dominates the Ferro Chrome market due to their extensive stainless steel production, rapid industrialization, and significant infrastructure development projects.

What are the key drivers for Ferro Chrome market growth?

Key drivers include the expanding global stainless steel industry, increasing demand from the automotive and construction sectors, urbanization trends, and the growing need for specialty alloys in new applications like electric vehicles.

What challenges does the Ferro Chrome market face?

Major challenges include the volatility of raw material and energy prices, stringent environmental regulations requiring significant investments in cleaner production, geopolitical risks affecting supply chains, and the inherent cyclical nature of the global steel industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted