Feed Phosphate Market

Feed Phosphate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705960 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Feed Phosphate Market Size

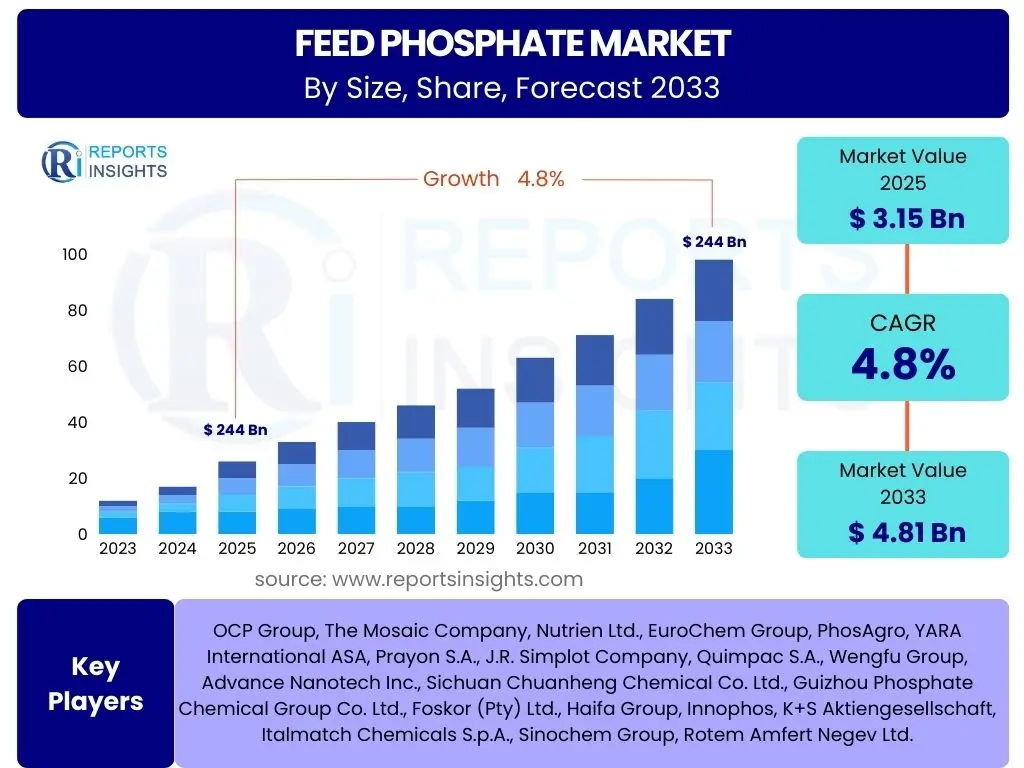

According to Reports Insights Consulting Pvt Ltd, The Feed Phosphate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 3.15 billion in 2025 and is projected to reach USD 4.81 billion by the end of the forecast period in 2033.

Key Feed Phosphate Market Trends & Insights

User queries regarding the Feed Phosphate market frequently center on identifying the primary drivers of growth, emerging applications, and shifts in consumer or livestock industry preferences. Analysis indicates a strong emphasis on sustainability, the adoption of advanced feed formulation techniques, and a growing demand for specialized feed additives that enhance animal health and productivity. The market is also witnessing a gradual shift towards more precise nutritional solutions, driven by improvements in animal husbandry practices and genetic advancements in livestock.

Furthermore, there is increasing interest in regional market dynamics, particularly in emerging economies where livestock production is rapidly expanding. The integration of digital technologies for supply chain optimization and quality control is also a recurring theme. These trends collectively point towards a market that is not only expanding in volume but also evolving in terms of technological sophistication and environmental responsibility, aiming to meet global protein demand while minimizing ecological impact.

- Increasing global meat and aquaculture consumption drives demand.

- Rising focus on animal health, nutrition, and productivity.

- Technological advancements in feed formulation and production.

- Shift towards sustainable and eco-friendly phosphate sources.

- Growing adoption of precision livestock farming techniques.

- Emergence of novel feed additives enhancing nutrient absorption.

- Regional diversification of production and consumption centers.

AI Impact Analysis on Feed Phosphate

User inquiries concerning the impact of Artificial Intelligence (AI) on the Feed Phosphate market often revolve around its potential to optimize feed formulations, enhance supply chain efficiency, and improve animal health monitoring. Stakeholders are particularly interested in how AI can facilitate precision nutrition by analyzing vast datasets related to animal genetics, environmental conditions, and feed ingredient profiles. This predictive capability is expected to minimize nutrient waste, improve feed conversion ratios, and ultimately reduce the overall cost of livestock production, thereby influencing the demand for specific types and quantities of feed phosphates.

Beyond formulation, AI is anticipated to revolutionize the supply chain of feed phosphates, enabling more accurate demand forecasting, inventory management, and logistics optimization. This could lead to more stable pricing and improved availability, reducing market volatility. Furthermore, AI-driven diagnostics and disease prevention in livestock can ensure healthier animals, thereby sustaining the need for optimal nutritional inputs, including feed phosphates. The overall expectation is that AI will foster a more data-driven, efficient, and sustainable feed industry, impacting the entire value chain of feed phosphates from sourcing to consumption.

- Optimized feed formulation through AI algorithms for precise nutrient delivery.

- Enhanced supply chain predictability and efficiency for raw materials and finished products.

- Predictive analytics for animal health management, reducing disease incidence and optimizing growth.

- Automated quality control and ingredient analysis, ensuring consistent product standards.

- Data-driven decision-making for sustainable resource management and waste reduction.

- Development of smart farming systems integrating feed management.

- Personalized nutrition plans for specific animal cohorts, maximizing feed efficacy.

Key Takeaways Feed Phosphate Market Size & Forecast

User questions about the key takeaways from the Feed Phosphate market size and forecast consistently highlight the resilience and steady growth potential of this sector, primarily driven by demographic expansion and evolving dietary patterns. The forecast indicates sustained demand, particularly from the poultry and aquaculture segments, where intensive farming practices necessitate high-quality nutritional inputs. While raw material price volatility and environmental regulations remain considerations, the market demonstrates a robust ability to adapt through innovation and diversified sourcing strategies. The increasing awareness among livestock producers about the critical role of feed phosphates in animal welfare and productivity is a fundamental driver supporting this positive outlook.

Furthermore, the market's trajectory is influenced by significant regional shifts, with Asia Pacific continuing to be a major growth engine due to burgeoning livestock industries and rising disposable incomes. Investments in research and development aimed at creating more bioavailable and environmentally friendly phosphate forms are also key to navigating future challenges and unlocking new opportunities. The long-term outlook emphasizes a balance between meeting growing global protein demand and adhering to stricter environmental and sustainability standards, positioning the Feed Phosphate market for continued, albeit evolving, expansion.

- Consistent market expansion underpinned by global population growth and rising meat consumption.

- Poultry and aquaculture sectors represent primary growth drivers.

- Significant growth opportunities in emerging economies, particularly in Asia Pacific.

- Technological advancements in product formulation and bioavailability are critical for market differentiation.

- Sustainability and environmental compliance are increasingly influencing market strategies.

- Resilience against raw material price fluctuations through diversified supply chains.

- Focus on enhanced animal health and productivity as a core value proposition.

Feed Phosphate Market Drivers Analysis

The Feed Phosphate market is significantly propelled by the increasing global demand for animal protein, driven by a growing population and rising disposable incomes, particularly in developing countries. As dietary preferences shift towards higher meat and dairy consumption, the need for efficient and healthy livestock production intensifies. Feed phosphates are essential minerals for bone development, metabolic functions, and overall growth in animals, directly contributing to improved feed conversion ratios and reduced livestock mortality. This fundamental requirement ensures a continuous and expanding demand for these additives across various livestock sectors.

Furthermore, advancements in animal genetics and nutrition science have led to a greater understanding of precise dietary requirements for optimal animal performance. This scientific progress encourages the use of high-quality feed ingredients, including specific types of feed phosphates that offer superior bioavailability. The global push for enhanced animal welfare and stricter regulations regarding animal health also contributes to the increased adoption of nutrient-rich feed formulations, where feed phosphates play a crucial role in preventing deficiency-related diseases and ensuring robust growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Population & Meat Consumption | +1.5% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Rising Awareness of Animal Health & Nutrition | +1.2% | North America, Europe, China | Mid-term (2025-2029) |

| Expansion of Aquaculture Sector | +1.0% | Southeast Asia, South America, Coastal Regions | Long-term (2025-2033) |

| Industrialization of Livestock Farming | +0.8% | Emerging Economies Globally | Mid to Long-term (2025-2033) |

Feed Phosphate Market Restraints Analysis

Despite robust growth drivers, the Feed Phosphate market faces notable restraints, primarily centered around the volatility of raw material prices and stringent environmental regulations. The primary raw material, phosphate rock, is a finite resource, and its extraction and processing are energy-intensive, making the supply vulnerable to geopolitical events, mining costs, and global demand-supply imbalances. Fluctuations in the prices of phosphorus rock can directly impact the manufacturing costs of feed phosphates, subsequently affecting product pricing and profitability for manufacturers, and potentially leading to a cautious approach from buyers.

Environmental concerns are another significant restraint. Phosphate mining and processing can have substantial ecological footprints, including land degradation, water pollution, and greenhouse gas emissions. Governments worldwide are imposing stricter environmental regulations on phosphate discharge into water bodies and phosphorus content in agricultural runoff, often pushing for reduced usage or more efficient absorption methods in animal feed. These regulations can necessitate costly process upgrades for manufacturers and may encourage the search for alternative, non-phosphate-based feed additives, thereby limiting market expansion for traditional feed phosphates.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Phosphate Rock) | -0.9% | Global, particularly major importing regions | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations | -0.7% | Europe, North America, parts of Asia | Long-term (2025-2033) |

| Development of Phosphate Alternatives | -0.5% | Global, R&D focused regions | Mid to Long-term (2027-2033) |

| Oversupply and Price Erosion in Mature Markets | -0.4% | China, parts of Europe | Short-term (2025-2027) |

Feed Phosphate Market Opportunities Analysis

Significant opportunities in the Feed Phosphate market arise from the expanding aquaculture sector and the continuous pursuit of enhanced product efficacy through innovation. The global growth of fish and shrimp farming, driven by increasing seafood consumption and declining wild fish stocks, presents a substantial new frontier for feed phosphate applications. Aquaculture species have unique nutritional requirements, often demanding highly bioavailable forms of phosphorus for skeletal development and overall health, thus opening avenues for specialized feed phosphate products tailored to this fast-growing industry. Manufacturers who can develop and market such niche solutions stand to gain a competitive advantage.

Moreover, technological advancements in feed processing and the development of novel feed ingredients offer avenues for market growth. This includes the exploration of sustainable and circular economy approaches, such as recovering phosphates from waste streams or developing feed phosphates with improved digestibility and reduced environmental impact. Furthermore, the increasing adoption of precision livestock farming, which involves tailoring nutrition based on individual animal needs and real-time data, creates a demand for sophisticated, high-performance feed phosphates. This focus on efficiency and sustainability aligns with global trends and regulatory pressures, presenting robust opportunities for long-term market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Aquaculture Feed Market | +1.3% | Asia Pacific, Latin America, Europe | Long-term (2025-2033) |

| Development of Enhanced Bioavailability Products | +1.0% | Global, particularly R&D hubs | Mid to Long-term (2026-2033) |

| Focus on Sustainable Sourcing & Production | +0.8% | Europe, North America, Innovating Economies | Long-term (2025-2033) |

| Untapped Potential in Emerging Markets | +0.7% | Africa, parts of Southeast Asia | Long-term (2025-2033) |

Feed Phosphate Market Challenges Impact Analysis

The Feed Phosphate market faces several notable challenges, prominently including the complex and often unpredictable geopolitical landscape, which can significantly disrupt global supply chains. As phosphate rock is concentrated in a few geological locations, geopolitical tensions, trade disputes, or instability in key mining regions can lead to supply shortages, increased shipping costs, and price surges for raw materials. Such disruptions compel manufacturers to seek alternative suppliers or reconfigure logistics, adding layers of complexity and cost to operations. The reliance on specific regions for critical inputs exposes the market to external vulnerabilities that are beyond the direct control of industry players.

Another substantial challenge is the increasing scrutiny from regulatory bodies and public opinion regarding the environmental impact of phosphate use, particularly concerning phosphorus runoff and eutrophication. This pressure often translates into stricter compliance requirements and calls for reduced phosphorus excretion in animal waste, pushing the industry to develop and adopt more environmentally friendly solutions or face potential usage restrictions. Additionally, shifting consumer preferences towards alternative protein sources, such as plant-based or lab-grown meats, could incrementally impact the long-term growth trajectory of traditional livestock farming, indirectly affecting the demand for feed phosphates. Navigating these challenges requires substantial investment in sustainable practices, diversified sourcing, and continuous innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Instability & Supply Chain Disruptions | -0.8% | Global, especially regions dependent on imports | Short to Mid-term (2025-2028) |

| Intensifying Environmental Regulations on Phosphorus Runoff | -0.6% | Europe, North America, China | Mid to Long-term (2026-2033) |

| Competition from Alternative Feed Additives | -0.5% | Global, highly innovative regions | Long-term (2027-2033) |

| Consumer Shifts Towards Plant-based Diets | -0.3% | North America, Europe | Long-term (2028-2033) |

Feed Phosphate Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Feed Phosphate market, offering critical insights into its current size, historical performance, and future projections. The report meticulously details market trends, drivers, restraints, opportunities, and challenges, providing a holistic view of the market dynamics. It further segments the market by various criteria, enabling a granular understanding of different product types, livestock applications, and geographical regions, assisting stakeholders in strategic decision-making and competitive landscape analysis.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.15 Billion |

| Market Forecast in 2033 | USD 4.81 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | OCP Group, The Mosaic Company, Nutrien Ltd., EuroChem Group, PhosAgro, YARA International ASA, Prayon S.A., J.R. Simplot Company, Quimpac S.A., Wengfu Group, Advance Nanotech Inc., Sichuan Chuanheng Chemical Co. Ltd., Guizhou Phosphate Chemical Group Co. Ltd., Foskor (Pty) Ltd., Haifa Group, Innophos, K+S Aktiengesellschaft, Italmatch Chemicals S.p.A., Sinochem Group, Rotem Amfert Negev Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Feed Phosphate market is meticulously segmented to provide a granular view of its diverse components, allowing for detailed analysis of demand patterns and growth avenues across different product types, livestock applications, and physical forms. This comprehensive segmentation highlights the varying requirements of different animal species and farming practices, driving innovation in product development to meet specific nutritional needs. The breakdown also enables a clearer understanding of market saturation points and emerging opportunities in niche applications, allowing market participants to fine-tune their strategies.

Understanding these segments is crucial for identifying key growth areas, assessing competitive landscapes, and forecasting future demand shifts. For instance, the poultry segment typically demands large volumes due to intensive farming, while aquaculture may require specialized, highly bioavailable forms. Similarly, the choice between powder and granular forms often depends on feed manufacturing processes and animal preferences. This detailed analysis ensures that all facets of the market's structure are thoroughly examined, offering actionable insights for investment and market penetration strategies.

- By Type:

- Monocalcium Phosphate (MCP): Preferred for its high phosphorus content and bioavailability, especially in poultry and swine diets.

- Dicalcium Phosphate (DCP): Widely used in various livestock feeds for its balanced calcium and phosphorus content.

- Tricalcium Phosphate (TCP): Utilized for its slow-release properties and as a calcium source.

- Defluorinated Phosphate (DFP): Processed to reduce fluorine, making it suitable for livestock.

- Mono-dicalcium Phosphate (MDCP): Offers a balance between MCP and DCP, providing good bioavailability.

- Others: Includes specialized or blended phosphate types.

- By Livestock:

- Poultry: Largest consumer due to rapid growth rates and high-intensity farming.

- Swine: Significant consumer for bone development and overall health.

- Ruminants (Cattle, Sheep, Goats): Essential for bone integrity, milk production, and fertility.

- Aquaculture (Fish, Shrimp): Critical for skeletal growth and fin development in aquatic species.

- Pet Animals: Used in premium pet foods for bone health.

- Others: Including horses, minor livestock.

- By Form:

- Powder: Commonly used in feed mills for easy mixing.

- Granular: Preferred for its dust-free handling and uniform distribution in some applications.

- By Application:

- Feed Additive: Direct incorporation into compound feed formulations.

- Mineral Premix: Used as a component in vitamin and mineral premixes.

Regional Highlights

The Feed Phosphate market exhibits distinct regional dynamics, influenced by varying livestock production scales, regulatory frameworks, and economic development levels. Asia Pacific stands as the largest and fastest-growing market, primarily driven by robust economic growth, rising disposable incomes, and the consequent surge in meat and aquaculture consumption, particularly in countries like China, India, and Southeast Asian nations. The region's expanding industrial livestock farming sector demands increasing volumes of high-quality feed ingredients, positioning it as a critical growth engine for feed phosphates. Investments in feed production capacities and an increasing focus on animal nutrition are further bolstering this regional market.

North America and Europe represent mature markets characterized by advanced animal husbandry practices, stringent quality standards, and a focus on sustainable production. While growth rates may be more modest compared to Asia Pacific, these regions maintain significant market shares due to established livestock industries and a consistent demand for premium feed formulations. Innovation in these regions often centers on developing more bioavailable and environmentally friendly phosphate solutions. Latin America, with its burgeoning livestock and aquaculture industries (especially in Brazil and Argentina), also presents substantial growth opportunities, driven by increasing protein exports and domestic consumption. The Middle East and Africa (MEA) region, though smaller, is showing promising growth as livestock farming practices modernize and expand, stimulated by government initiatives to enhance food security and reduce reliance on imports. Each region's unique blend of drivers and challenges shapes the global market landscape for feed phosphates.

- Asia Pacific (APAC): Dominates the market due to massive livestock populations, particularly poultry and swine, in countries like China, India, and Indonesia. Rapid economic development and increasing per capita meat consumption are key drivers. Significant expansion in aquaculture also contributes to demand.

- North America: A mature market characterized by large-scale, technologically advanced livestock farming. Focus on efficiency, animal welfare, and high-quality feed formulations. Steady demand driven by established poultry, beef, and dairy industries.

- Europe: Marked by stringent environmental regulations and a strong emphasis on sustainable animal production. Demand is stable, with a growing preference for specialty and eco-friendly feed phosphates. Innovation in feed efficiency and reduced phosphorus excretion is a key trend.

- Latin America: Experiencing substantial growth in livestock and aquaculture sectors, particularly in Brazil, Argentina, and Mexico. Increasing meat exports and domestic consumption are fueling demand for feed phosphates. Abundant agricultural resources support this growth.

- Middle East and Africa (MEA): Emerging market with increasing investments in modern livestock farming to enhance food security. While smaller in scale, the region presents opportunities for growth as traditional practices evolve and per capita meat consumption rises.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Feed Phosphate Market.- OCP Group

- The Mosaic Company

- Nutrien Ltd.

- EuroChem Group

- PhosAgro

- YARA International ASA

- Prayon S.A.

- J.R. Simplot Company

- Quimpac S.A.

- Wengfu Group

- Advance Nanotech Inc.

- Sichuan Chuanheng Chemical Co. Ltd.

- Guizhou Phosphate Chemical Group Co. Ltd.

- Foskor (Pty) Ltd.

- Haifa Group

- Innophos

- K+S Aktiengesellschaft

- Italmatch Chemicals S.p.A.

- Sinochem Group

- Rotem Amfert Negev Ltd.

Frequently Asked Questions

What are Feed Phosphates?

Feed phosphates are essential mineral supplements derived from phosphorus, used in animal feed to provide vital phosphorus and calcium. These minerals are critical for the healthy growth, skeletal development, metabolic functions, and reproductive performance of livestock and aquaculture species.

Why are Feed Phosphates important for animal nutrition?

Feed phosphates are crucial because phosphorus is the second most abundant mineral in an animal's body and plays a key role in energy metabolism, bone formation, cell structure, and enzyme activity. Adequate phosphorus intake through feed phosphates ensures optimal growth, improves feed conversion efficiency, and prevents deficiency-related diseases in animals.

What drives the growth of the Feed Phosphate market?

The primary drivers include the increasing global demand for animal protein due to population growth and rising disposable incomes, the expansion and industrialization of livestock and aquaculture farming, and a growing emphasis on animal health, welfare, and productivity by producers and consumers worldwide.

What are the main types of Feed Phosphates?

The main types include Monocalcium Phosphate (MCP), Dicalcium Phosphate (DCP), Tricalcium Phosphate (TCP), and Mono-dicalcium Phosphate (MDCP). Each type differs in its phosphorus and calcium content, as well as its bioavailability, making them suitable for various animal species and specific nutritional requirements.

What are the key challenges facing the Feed Phosphate market?

Key challenges include the volatility of raw material prices (phosphate rock), stringent environmental regulations concerning phosphorus discharge and sustainability, potential disruptions in global supply chains due to geopolitical factors, and the ongoing development of alternative feed additives that could reduce reliance on traditional phosphates.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted