FC BGA Substrate Market

FC BGA Substrate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701963 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

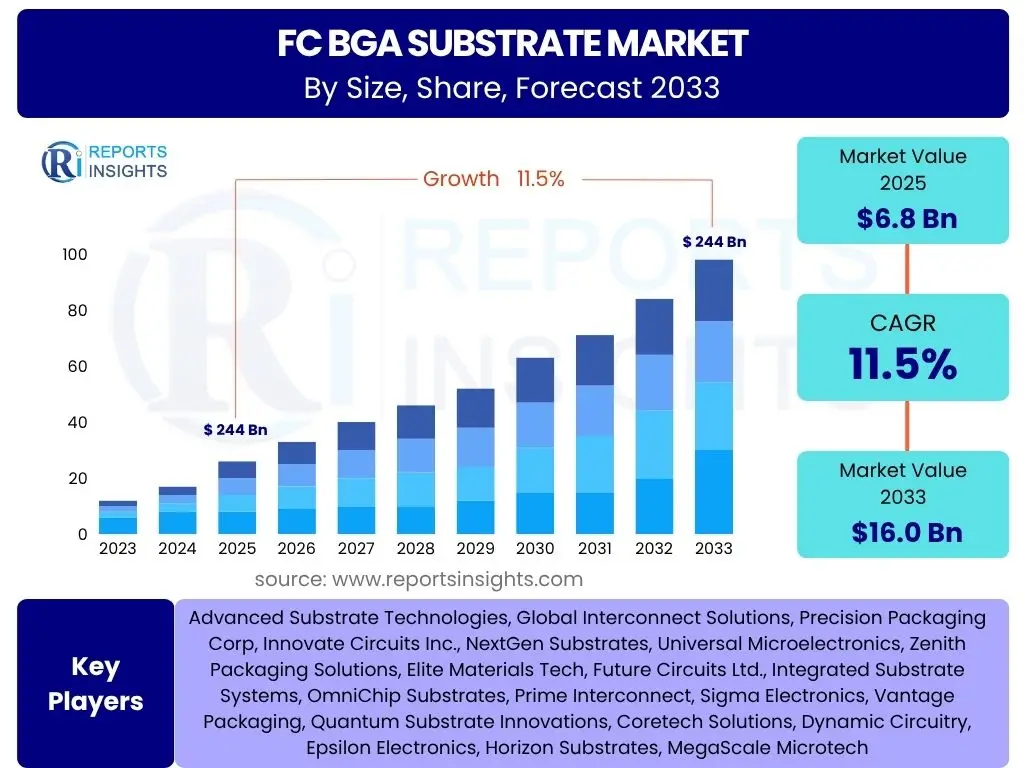

FC BGA Substrate Market Size

According to Reports Insights Consulting Pvt Ltd, The FC BGA Substrate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 6.8 Billion in 2025 and is projected to reach USD 16.0 Billion by the end of the forecast period in 2033.

Key FC BGA Substrate Market Trends & Insights

The FC BGA (Flip Chip Ball Grid Array) Substrate market is currently shaped by several transformative trends, primarily driven by the escalating demand for high-performance computing (HPC), artificial intelligence (AI), and advanced connectivity solutions. Miniaturization continues to be a paramount focus, pushing the boundaries of substrate design and manufacturing to accommodate increasingly complex integrated circuits within smaller form factors. This drives innovation in fine-pitch technology and multi-layer substrate structures.

Another significant trend is the growing adoption of advanced packaging technologies such as 2.5D and 3D integration. These technologies heavily rely on high-density FC BGA substrates to facilitate vertical stacking and interconnections, offering superior performance, power efficiency, and reduced latency. The shift towards higher data rates and increased bandwidth in applications like data centers, 5G infrastructure, and automotive electronics further accelerates the demand for robust and reliable FC BGA substrates capable of handling such rigorous requirements. Furthermore, sustainability and supply chain resilience are emerging as critical considerations, influencing material choices and manufacturing processes.

Innovation in substrate materials, including low-loss and high-thermal-conductivity materials, is also a key trend, addressing the challenges posed by increased power dissipation and signal integrity in advanced chip designs. The interplay of these trends highlights a dynamic market environment where technological advancements are continuously reshaping the landscape of electronic packaging and semiconductor manufacturing.

- Miniaturization and increasing I/O counts in advanced semiconductors.

- Rising adoption of advanced packaging technologies (2.5D, 3D ICs).

- Growing demand from high-performance computing (HPC), AI, and data centers.

- Expansion of 5G infrastructure and IoT devices requiring higher bandwidth.

- Developments in substrate materials for enhanced thermal management and electrical performance.

- Emphasis on supply chain diversification and regional manufacturing resilience.

AI Impact Analysis on FC BGA Substrate

The proliferation of Artificial Intelligence (AI) and machine learning (ML) across various industries profoundly impacts the FC BGA Substrate market. AI workloads, characterized by their immense computational requirements, necessitate processors with higher core counts, faster clock speeds, and significantly increased data throughput. This directly translates to a demand for FC BGA substrates capable of supporting more power, denser interconnections, and superior thermal dissipation, as these substrates are the foundational interface between the high-performance AI chips and the rest of the system board.

As AI applications become more sophisticated, integrating AI accelerators, GPUs, and specialized ASICs into compact packages becomes crucial. FC BGA substrates are essential for these complex heterogeneous integrations, enabling high-bandwidth memory (HBM) integration and multi-die chiplets. Users are concerned with whether current substrate technologies can keep pace with the exponential growth in AI computational power without compromising reliability or cost-effectiveness. Expectations are high for innovations in materials and manufacturing processes to meet these escalating performance demands.

The relentless pursuit of energy efficiency in AI systems also drives innovation in FC BGA substrates, as power delivery network (PDN) integrity and signal integrity become paramount. AI's push for edge computing further necessitates smaller, more power-efficient, yet high-performance, packaging solutions, solidifying the critical role of advanced FC BGA substrates in the evolving AI ecosystem. The market anticipates continued investment in R&D to optimize substrate performance for future AI generations.

- Increased demand for high-performance FC BGA substrates to support AI processors (GPUs, ASICs).

- Requirement for enhanced thermal management capabilities due to AI chip power density.

- Driving force for advanced packaging techniques (e.g., 2.5D, 3D) enabled by FC BGA.

- Emphasis on high-density interconnections and signal integrity for AI data throughput.

- Innovation in substrate materials and design for power delivery networks to support AI.

Key Takeaways FC BGA Substrate Market Size & Forecast

The FC BGA Substrate market is poised for robust growth, driven primarily by the insatiable demand for advanced electronics that power high-performance computing, artificial intelligence, and sophisticated communication networks. The significant projected Compound Annual Growth Rate (CAGR) reflects the critical role these substrates play in enabling the next generation of semiconductors, forming the backbone for everything from data centers to automotive electronics. This growth trajectory underscores the ongoing trend of increasing complexity and integration in microelectronics, which directly translates to a need for more advanced and high-density packaging solutions.

The estimated market valuation in 2025, reaching a substantial figure by 2033, indicates a sustained and accelerated expansion. This expansion is not merely quantitative but also qualitative, involving continuous innovation in substrate materials, design, and manufacturing processes to meet stringent performance, power, and thermal requirements. The market's future is intrinsically linked to advancements in chip architecture and packaging, making FC BGA substrates a pivotal component in the semiconductor value chain.

Furthermore, the forecast highlights the market's resilience and adaptability in the face of evolving technological landscapes. As industries increasingly adopt digital transformation and embrace data-intensive applications, the foundational role of FC BGA substrates will continue to solidify, ensuring their sustained relevance and commanding a significant share of the semiconductor packaging market. The investment in R&D and manufacturing capacity by key players will be crucial in realizing this projected growth.

- Strong double-digit CAGR indicates significant market expansion through 2033.

- Market growth is directly tied to the proliferation of high-performance computing and AI.

- Increasing integration of semiconductors necessitates advanced FC BGA substrates.

- Substantial market valuation projected, highlighting the critical role of these components.

- Continuous innovation in materials and manufacturing is essential for sustaining growth.

FC BGA Substrate Market Drivers Analysis

The FC BGA Substrate market is experiencing significant tailwinds from several key drivers, primarily stemming from the pervasive demand for high-performance computing and advanced connectivity. The relentless drive for miniaturization in electronic devices, coupled with the need for enhanced functionality within smaller footprints, compels manufacturers to adopt sophisticated packaging solutions that utilize FC BGA substrates. These substrates are crucial for integrating complex chips with high input/output (I/O) counts, facilitating superior electrical performance and thermal management, which are paramount for modern processors and memory units.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Performance Computing (HPC) and AI Accelerators | +3.5% | Global, particularly North America, APAC (China, Taiwan, South Korea) | Short to Long-term (2025-2033) |

| Proliferation of 5G Technology and Data Centers | +2.8% | Global, with strong growth in APAC, North America, Europe | Medium to Long-term (2026-2033) |

| Advancements in Advanced Packaging Technologies (2.5D/3D ICs) | +2.5% | Global, led by major semiconductor manufacturing hubs | Short to Long-term (2025-2033) |

| Growth in Automotive Electronics and IoT Devices | +1.7% | Europe, APAC (Japan, China), North America | Medium to Long-term (2027-2033) |

FC BGA Substrate Market Restraints Analysis

Despite the robust growth prospects, the FC BGA Substrate market faces several formidable restraints that could temper its expansion. One primary challenge is the escalating manufacturing costs associated with producing increasingly complex and high-density substrates. The need for advanced materials, sophisticated fabrication processes, and stringent quality control measures drives up production expenses, which can impact profit margins and potentially limit broader adoption in cost-sensitive applications. Furthermore, the inherent complexity of these substrates also contributes to lower manufacturing yields, adding to the overall cost burden.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Capital Expenditure | -1.2% | Global, affecting smaller players and new entrants | Short to Medium-term (2025-2028) |

| Technological Complexity and Yield Management Challenges | -1.0% | Global, particularly in leading-edge technology nodes | Short to Medium-term (2025-2028) |

| Geopolitical Tensions and Supply Chain Volatility | -0.8% | Global, with higher impact on regions dependent on specific suppliers | Short-term (2025-2026) |

| Rapid Technological Obsolescence and R&D Investment | -0.7% | Global, affecting companies without strong R&D pipelines | Medium to Long-term (2027-2033) |

FC BGA Substrate Market Opportunities Analysis

The FC BGA Substrate market is ripe with numerous opportunities for growth and innovation, driven by evolving technological landscapes and expanding application areas. The continuous evolution of semiconductor technology, particularly in the realm of advanced packaging, presents a significant avenue for substrate manufacturers. As chip designs become more intricate, requiring higher levels of integration and performance, the demand for sophisticated FC BGA substrates capable of supporting these next-generation architectures will continue to surge. This includes the development of substrates for chiplet-based designs and heterogeneous integration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Chiplet Architectures and Heterogeneous Integration | +3.0% | Global, with strong momentum in semiconductor innovation hubs | Medium to Long-term (2026-2033) |

| Increasing Investment in AI and Data Center Infrastructure | +2.7% | North America, APAC (China, Singapore, Japan), Europe | Short to Long-term (2025-2033) |

| Development of Advanced Materials for Improved Performance and Thermal Management | +2.2% | Global, driven by R&D focused regions | Medium to Long-term (2027-2033) |

| Expansion into New End-use Applications (e.g., Metaverse, Quantum Computing) | +1.5% | Global, early adopters in technologically advanced regions | Long-term (2029-2033) |

FC BGA Substrate Market Challenges Impact Analysis

The FC BGA Substrate market faces several critical challenges that demand strategic responses from industry players. One major challenge is the inherent complexity in manufacturing these highly intricate components. As chip designs push the boundaries of miniaturization and integration, the precision required in substrate fabrication increases exponentially. This leads to higher defect rates and lower manufacturing yields, which directly impact production costs and the overall supply chain efficiency. Managing these yield challenges while scaling up production for burgeoning demand remains a persistent hurdle.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining High Manufacturing Yields Amid Increasing Complexity | -1.5% | Global, impacting all major manufacturers | Short to Medium-term (2025-2028) |

| Talent Shortage in Skilled Engineering and Manufacturing Roles | -1.0% | North America, Europe, parts of APAC | Medium to Long-term (2027-2033) |

| Intense R&D Investment Required for Next-Gen Technologies | -0.9% | Global, particularly for companies seeking market leadership | Short to Long-term (2025-2033) |

| Environmental Regulations and Sustainable Manufacturing Practices | -0.7% | Europe, North America, increasingly in APAC | Medium to Long-term (2027-2033) |

FC BGA Substrate Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global FC BGA Substrate market, offering crucial insights into its size, growth trajectory, key trends, and future outlook. It meticulously dissects market dynamics by examining drivers, restraints, opportunities, and challenges that shape the industry landscape. The report also includes a detailed segmentation analysis, covering various substrate types, applications, and regional market performances, ensuring a holistic understanding for stakeholders. Furthermore, it profiles key industry players, offering strategic competitive intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 16.0 Billion |

| Growth Rate | 11.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Substrate Technologies, Global Interconnect Solutions, Precision Packaging Corp, Innovate Circuits Inc., NextGen Substrates, Universal Microelectronics, Zenith Packaging Solutions, Elite Materials Tech, Future Circuits Ltd., Integrated Substrate Systems, OmniChip Substrates, Prime Interconnect, Sigma Electronics, Vantage Packaging, Quantum Substrate Innovations, Coretech Solutions, Dynamic Circuitry, Epsilon Electronics, Horizon Substrates, MegaScale Microtech |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The FC BGA Substrate market is comprehensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market growth. This segmentation is crucial for identifying specific growth pockets, understanding technological preferences, and tailoring market strategies. The primary segmentation categories include substrate type, material used, and various end-use applications, each driven by unique market dynamics and technological requirements. This layered analysis allows for a precise evaluation of market performance across different product categories and industry verticals.

- By Type:

- Standard Substrates: Traditional FC BGA substrates catering to mainstream applications.

- High-Density Substrates: Designed for chips with higher I/O counts and performance demands.

- Ultra-High-Density Substrates: For leading-edge processors, AI accelerators, and advanced packaging, featuring extremely fine pitches and multi-layer structures.

- By Material:

- BT Resin (Bismaleimide Triazine Resin): Widely used due to its excellent electrical properties and cost-effectiveness.

- ABF (Ajinomoto Build-up Film): Preferred for high-performance processors and advanced packaging due to superior electrical properties and fine-line capabilities.

- Ceramic: Utilized in high-reliability and high-temperature applications.

- Others: Includes emerging materials like glass and advanced polymers being explored for next-generation substrates.

- By Application:

- Computing & Networking: Encompasses applications in data centers, servers, laptops, PCs, and networking equipment, representing a significant demand segment for high-performance FC BGA substrates.

- Consumer Electronics: Includes smartphones, tablets, wearables, and gaming consoles, driving demand for miniaturized and cost-effective solutions.

- Automotive: Growing segment driven by ADAS, infotainment systems, and electric vehicle power electronics.

- Industrial: Applications in automation, robotics, and industrial control systems requiring robust and reliable substrates.

- Telecommunications: Critical for 5G base stations, network routers, and other communication infrastructure.

- Aerospace & Defense: Demands high-reliability and ruggedized substrates for extreme environments.

- Medical Devices: Requires highly reliable and often miniaturized substrates for various diagnostic and therapeutic devices.

Regional Highlights

- Asia Pacific (APAC): Dominates the FC BGA Substrate market due to the presence of major semiconductor manufacturing hubs in Taiwan, South Korea, Japan, and China. The region benefits from robust electronics production, strong government support for semiconductor industries, and high demand from consumer electronics, automotive, and data center sectors. Continued investment in advanced packaging and AI infrastructure further cements its leading position.

- North America: A significant market driven by innovation in high-performance computing, artificial intelligence, and cloud services. The region hosts leading fabless semiconductor companies and major data center operators, fueling demand for cutting-edge FC BGA substrates. Emphasis on research and development, coupled with investments in domestic manufacturing, contributes to its growth.

- Europe: Exhibits steady growth, primarily influenced by the expanding automotive electronics sector, industrial automation, and telecommunications infrastructure (5G rollout). Countries like Germany and France are key contributors, focusing on high-reliability and niche applications, alongside increasing efforts to strengthen regional semiconductor supply chains.

- Latin America & Middle East and Africa (MEA): These regions are emerging markets with growing potential, driven by increasing digitalization, expanding IT infrastructure, and rising adoption of consumer electronics. While smaller in market share, they represent future growth opportunities as local manufacturing capabilities develop and connectivity expands.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the FC BGA Substrate Market.- Advanced Substrate Technologies

- Global Interconnect Solutions

- Precision Packaging Corp

- Innovate Circuits Inc.

- NextGen Substrates

- Universal Microelectronics

- Zenith Packaging Solutions

- Elite Materials Tech

- Future Circuits Ltd.

- Integrated Substrate Systems

- OmniChip Substrates

- Prime Interconnect

- Sigma Electronics

- Vantage Packaging

- Quantum Substrate Innovations

- Coretech Solutions

- Dynamic Circuitry

- Epsilon Electronics

- Horizon Substrates

- MegaScale Microtech

Frequently Asked Questions

What is the projected growth rate of the FC BGA Substrate market?

The FC BGA Substrate market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033.

What are the primary drivers of the FC BGA Substrate market?

Key drivers include the increasing demand for high-performance computing (HPC) and AI accelerators, the proliferation of 5G technology and data centers, advancements in advanced packaging technologies (2.5D/3D ICs), and growth in automotive electronics and IoT devices.

How does AI impact the FC BGA Substrate market?

AI significantly impacts the market by driving demand for higher performance, better thermal management, and denser interconnections in FC BGA substrates to support powerful AI processors and advanced packaging solutions.

Which region holds the largest market share for FC BGA Substrates?

Asia Pacific (APAC) currently holds the largest market share, driven by its robust semiconductor manufacturing ecosystem and strong demand from various electronics sectors.

What are the key materials used in FC BGA Substrates?

The primary materials used include BT Resin (Bismaleimide Triazine Resin) and ABF (Ajinomoto Build-up Film), with ceramic and other advanced polymers also being utilized for specific applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted