Extreme Ultraviolet Lithography Market

Extreme Ultraviolet Lithography Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710067 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

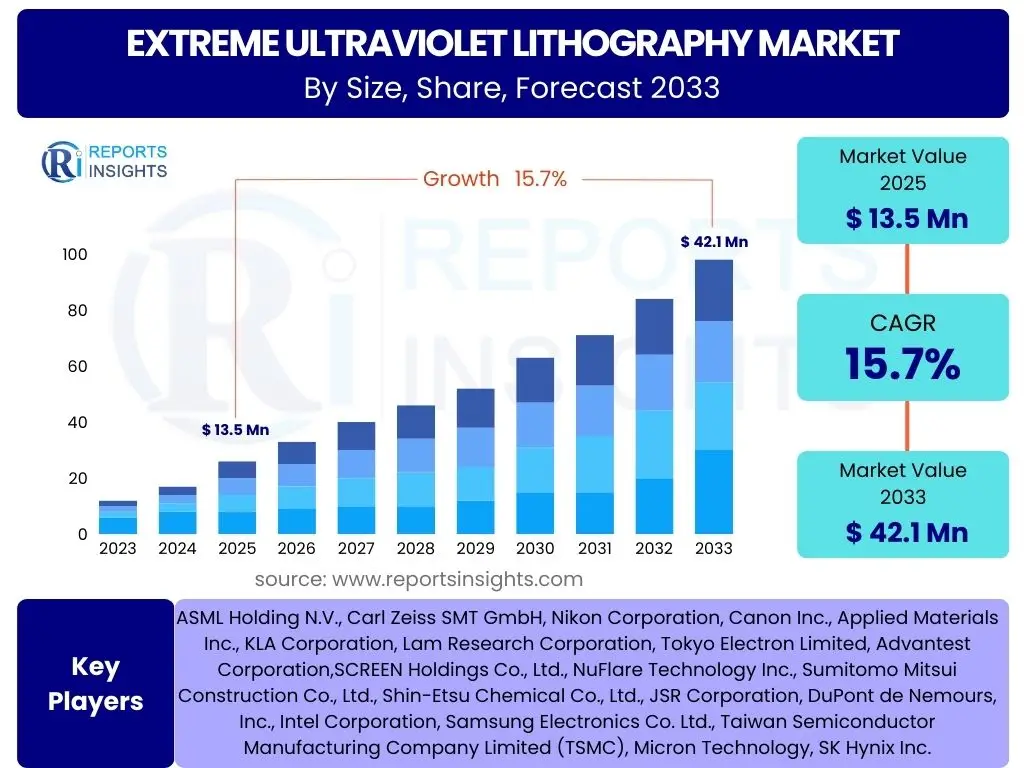

Extreme Ultraviolet Lithography Market Size

According to Reports Insights Consulting Pvt Ltd, The Extreme Ultraviolet Lithography Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.7% between 2025 and 2033. The market is estimated at USD 13.5 Billion in 2025 and is projected to reach USD 42.1 Billion by the end of the forecast period in 2033.

Key Extreme Ultraviolet Lithography Market Trends & Insights

User queries regarding the Extreme Ultraviolet Lithography (EUVL) market consistently highlight several pivotal trends shaping its evolution. There is a strong interest in the ongoing miniaturization of semiconductor devices and the relentless pursuit of higher transistor density, which directly necessitates advanced lithography techniques like EUVL. Furthermore, the market is characterized by significant research and development investments aimed at improving throughput, yield, and overall cost-effectiveness of EUV systems, driven by the increasing complexity of chip designs.

Another prominent area of interest revolves around the expansion of EUVL applications beyond logic chips to memory manufacturing, signaling a broader adoption across different semiconductor segments. The integration of advanced computational lithography techniques and artificial intelligence for process optimization and defect inspection also stands out as a critical trend. This technological progression is essential for maintaining the high precision and efficiency required for next-generation chip production, addressing the complex challenges associated with patterning at nanometer scales.

- Continued miniaturization of semiconductor devices driving demand for advanced patterning.

- Intensified R&D investments focusing on improving EUV system throughput and yield.

- Expansion of EUVL application into memory manufacturing, broadening market scope.

- Increasing adoption of computational lithography and AI for process optimization and defect reduction.

- Development of advanced pellicles and resist materials enhancing EUV efficiency and defectivity.

- Growing strategic collaborations among foundries, IDMs, and equipment manufacturers to accelerate technology adoption.

- Focus on energy efficiency and sustainable manufacturing practices within EUV ecosystem.

AI Impact Analysis on Extreme Ultraviolet Lithography

Common user questions regarding AI's impact on Extreme Ultraviolet Lithography frequently center on its potential to revolutionize various stages of the manufacturing process, from design to defect inspection. Users are keen to understand how artificial intelligence can address the inherent complexities of EUV technology, particularly in enhancing resolution, reducing stochastic defects, and optimizing the overall manufacturing yield. The expectation is that AI will provide solutions for challenges that are difficult to overcome with traditional physics-based models, offering new avenues for process control and efficiency.

Furthermore, there is significant interest in AI's role in predictive maintenance for highly complex EUV equipment, minimizing downtime, and extending the operational lifespan of expensive machinery. Questions also arise about the application of machine learning in design for manufacturability (DFM) and computational lithography, where AI can accelerate pattern optimization and simulate complex light interactions with masks and resists. This indicates a strong belief that AI will be a critical enabler for the future advancements and broader adoption of EUV technology, moving beyond incremental improvements to transformative changes in semiconductor fabrication.

- AI algorithms significantly enhance computational lithography, optimizing mask designs and pattern fidelity.

- Machine learning improves defect detection and classification in EUV manufacturing, leading to higher yields.

- Predictive maintenance for EUV scanners and components is enabled by AI, reducing downtime and operational costs.

- AI assists in optimizing process parameters (e.g., dose, focus) for improved patterning performance and stability.

- Advanced AI models analyze large datasets to identify subtle patterns and correlations, driving continuous process improvement.

- Automated design for manufacturability (DFM) solutions leverage AI to ensure designs are EUV-compatible.

- AI-powered simulation tools accelerate R&D by predicting outcomes of new materials or process changes without extensive physical testing.

Key Takeaways Extreme Ultraviolet Lithography Market Size & Forecast

An analysis of common user questions concerning the Extreme Ultraviolet Lithography (EUVL) market size and forecast reveals a strong interest in the factors driving its substantial growth and the long-term sustainability of this advanced technology. Users are primarily concerned with understanding the market's projected financial trajectory, the key technological milestones expected, and the economic implications for semiconductor manufacturers. There is a clear emphasis on identifying the core drivers behind the anticipated CAGR and the specific applications that will fuel market expansion, such as advanced computing and artificial intelligence hardware.

Moreover, inquiries often focus on the critical role EUVL plays in enabling the next generation of semiconductors, particularly for nodes below 7nm, and its indispensability for maintaining competitive advantage in the global microelectronics industry. The overall sentiment reflects a recognition of EUVL as a foundational technology for future digital innovation, with its market growth being directly tied to the increasing demand for high-performance and energy-efficient electronic devices. The forecast underscores EUVL's transition from an emerging technology to a mainstream, high-growth segment within the semiconductor equipment market.

- The EUVL market is poised for robust double-digit growth, driven by sustained demand for advanced node semiconductors.

- Significant capital expenditures by leading foundries and memory manufacturers will fuel market expansion through 2033.

- EUVL's critical role in enabling chips below 7nm, essential for AI, HPC, and 5G/6G, ensures its market centrality.

- Technological advancements in throughput, uptime, and cost-of-ownership are key to market sustainability and broader adoption.

- Geopolitical considerations and regional manufacturing initiatives are increasingly influencing the geographical distribution of EUVL investments.

- The long-term forecast indicates continued market dominance due to lack of viable, economically competitive alternatives for advanced patterning.

Extreme Ultraviolet Lithography Market Drivers Analysis

The primary driver for the Extreme Ultraviolet Lithography market is the relentless demand for higher transistor density and smaller feature sizes in advanced semiconductor manufacturing. As the industry pushes beyond 7nm and into 5nm, 3nm, and even 2nm process nodes, conventional optical lithography methods face fundamental physical limitations due to light wavelength. EUVL, with its shorter 13.5nm wavelength, offers the precision necessary to pattern these incredibly small features, making it indispensable for producing cutting-edge microprocessors, memory chips, and other complex integrated circuits.

Furthermore, the explosive growth in data-intensive applications such as artificial intelligence, machine learning, high-performance computing (HPC), 5G/6G communications, and autonomous driving systems significantly contributes to the demand for advanced chips. These applications require immense processing power and energy efficiency, which can only be achieved through advanced semiconductor architectures enabled by EUVL. The continuous innovation in these high-growth sectors directly translates into increased investment and adoption of EUVL technology by leading chip manufacturers worldwide.

The economic imperative for chip manufacturers to achieve higher yields and lower per-chip costs for advanced nodes also acts as a crucial driver. While initial EUV system costs are high, the ability to simplify multi-patterning processes and improve overall throughput for complex designs makes EUVL a more cost-effective solution in the long run for high-volume production of state-of-the-art semiconductors. This combination of technological necessity and economic efficiency propels the market forward.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Advanced Node Semiconductors (7nm, 5nm, 3nm) | +4.0% | Global, particularly APAC (South Korea, Taiwan), North America, Europe | 2025-2033 |

| Proliferation of AI, HPC, and 5G/6G Technologies | +3.5% | Global, especially North America, APAC (China, South Korea) | 2025-2033 |

| Increased Focus on Miniaturization and High-Performance Devices | +2.5% | Global | 2025-2033 |

| Cost-Efficiency for High-Volume Manufacturing of Complex Chips | +2.0% | Global, particularly major foundry regions | 2025-2033 |

Extreme Ultraviolet Lithography Market Restraints Analysis

One of the most significant restraints for the Extreme Ultraviolet Lithography market is the extraordinarily high capital expenditure required for EUV systems and associated infrastructure. A single EUV scanner can cost hundreds of millions of dollars, and setting up an EUV-capable fab involves substantial investments in cleanroom facilities, specialized mask infrastructure, and sophisticated defect inspection tools. This prohibitive cost creates a significant barrier to entry, limiting the number of companies that can afford to adopt EUV technology, primarily to a few global leaders in semiconductor manufacturing.

Another critical restraint is the inherent complexity and technical challenges associated with EUV technology. Achieving stable and reliable operation requires overcoming issues related to source power, mask defectivity, resist performance, and vacuum environments. The learning curve for optimizing EUV processes is steep, demanding highly specialized expertise and extensive R&D efforts. Any setbacks or delays in resolving these technical hurdles can impact the adoption rate and production timelines, thereby hindering market growth.

Furthermore, the EUV supply chain is highly concentrated, with a single dominant supplier for the core lithography tools and a limited number of suppliers for critical components like mirrors, light sources, and pellicles. This concentration creates potential vulnerabilities regarding supply chain disruptions, geopolitical factors, and the pace of technological innovation. Any issues within this narrow supply chain can have cascading effects across the entire EUV ecosystem, posing a significant restraint on the market's overall expansion and stability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for EUV Systems and Infrastructure | -3.0% | Global, particularly new entrants or smaller players | 2025-2033 |

| Technical Complexities and Steep Learning Curve | -2.5% | Global | 2025-2030 |

| Highly Concentrated and Fragile Supply Chain | -2.0% | Global, especially regions reliant on imports | 2025-2033 |

| Limited Alternative Advanced Lithography Options | -1.5% | Global | 2025-2033 |

Extreme Ultraviolet Lithography Market Opportunities Analysis

A significant opportunity in the Extreme Ultraviolet Lithography market lies in the continuous miniaturization of semiconductor devices and the relentless pursuit of Moore's Law. As chip manufacturers push to 2nm and beyond, the intrinsic capabilities of EUV become even more critical, making it the only viable solution for high-volume manufacturing of these advanced nodes. This technological imperative creates a sustained demand for improved EUV systems, including next-generation High-NA EUV, which promises even finer resolution, opening up new frontiers in chip design and performance for the coming decades.

The expansion of EUVL applications beyond logic manufacturing into memory fabrication presents another substantial growth opportunity. While initially focused on logic chips, the increasing density requirements for advanced DRAM and NAND flash memory are creating a compelling case for EUV adoption in this segment. This broader application base significantly expands the total addressable market for EUV equipment and services, diversifying revenue streams and strengthening the overall market's resilience against fluctuations in any single segment.

Furthermore, the global emphasis on building robust domestic semiconductor manufacturing capabilities, driven by geopolitical considerations and supply chain resilience, creates new opportunities for EUV market expansion. Countries and regions are investing heavily in establishing or expanding local foundries and IDMs, which often include plans for advanced process nodes that necessitate EUV technology. This localized investment trend, supported by government incentives and strategic alliances, can accelerate the deployment of EUV tools in new geographic areas and bolster long-term market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of High-NA EUV for Sub-2nm Nodes | +3.5% | Global | 2028-2033 |

| Expansion of EUV into Advanced Memory (DRAM, NAND) Manufacturing | +3.0% | APAC (South Korea, Japan), North America | 2025-2033 |

| Increased Government and Industry Investment in Domestic Semiconductor Fabs | +2.5% | North America, Europe, APAC (China, Japan) | 2025-2033 |

| Development of Advanced Materials (Resists, Pellicles) Improving EUV Performance | +2.0% | Global | 2025-2033 |

Extreme Ultraviolet Lithography Market Challenges Impact Analysis

One of the persistent challenges facing the Extreme Ultraviolet Lithography market is the high cost of ownership associated with EUV systems, extending beyond the initial capital expenditure. This includes the significant operational expenses related to maintaining the complex vacuum environment, sourcing high-power laser-produced plasma (LPP) light, and regularly replacing expensive components like pellicles and mirrors. These ongoing costs can strain the financial resources of even large semiconductor manufacturers, potentially limiting the scalability and widespread adoption of EUV technology across all foundries and process nodes, particularly for those with lower-volume production requirements.

Another critical challenge is the inherent defectivity associated with EUV masks and the lithography process itself. Even minute particles or imperfections on the mask can lead to critical defects on the wafer, impacting yield. While significant progress has been made in mask inspection and repair, achieving "zero defect" masks remains an elusive goal. Furthermore, stochastic defects, which are random variations in resist patterns at the nanometer scale, pose a fundamental challenge that requires continuous innovation in resist materials and process control, demanding substantial R&D investment and expertise.

The specialized skill set required to operate and maintain EUV equipment, coupled with the highly complex R&D cycles, presents a significant human capital challenge. There is a global shortage of engineers and scientists with expertise in EUV technology, optics, vacuum systems, and plasma physics. This talent gap can hinder faster deployment, effective troubleshooting, and future innovation, potentially slowing down the overall progress and market penetration of EUV technology. Addressing this requires long-term investments in education and industry-academic collaborations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Ownership and Operational Expenses | -2.8% | Global | 2025-2033 |

| EUV Mask Defectivity and Stochastic Printing Challenges | -2.2% | Global | 2025-2030 |

| Talent Shortage and Specialized Skill Requirements | -1.8% | Global | 2025-2033 |

| Intense R&D Investment and Long Development Cycles | -1.5% | Global | 2025-2033 |

Extreme Ultraviolet Lithography Market - Updated Report Scope

This report provides an in-depth analysis of the Extreme Ultraviolet Lithography (EUVL) market, offering comprehensive insights into its current landscape, key trends, and future growth trajectories. It encompasses a detailed examination of market size, segmentation by component, application, and end-use, alongside a thorough regional assessment. The report also addresses the impact of emerging technologies like AI and High-NA EUV, providing a strategic outlook for stakeholders navigating this highly complex and rapidly evolving industry. The scope aims to equip readers with critical market intelligence essential for informed decision-making and strategic planning within the advanced semiconductor manufacturing ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.5 Billion |

| Market Forecast in 2033 | USD 42.1 Billion |

| Growth Rate | 15.7% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASML Holding N.V., Carl Zeiss SMT GmbH, Nikon Corporation, Canon Inc., Applied Materials Inc., KLA Corporation, Lam Research Corporation, Tokyo Electron Limited, Advantest Corporation,SCREEN Holdings Co., Ltd., NuFlare Technology Inc., Sumitomo Mitsui Construction Co., Ltd., Shin-Etsu Chemical Co., Ltd., JSR Corporation, DuPont de Nemours, Inc., Intel Corporation, Samsung Electronics Co. Ltd., Taiwan Semiconductor Manufacturing Company Limited (TSMC), Micron Technology, SK Hynix Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Extreme Ultraviolet Lithography market is intricately segmented across various dimensions, reflecting the complex ecosystem of advanced semiconductor manufacturing. This segmentation allows for a granular understanding of market dynamics, identifying specific areas of growth, technological advancements, and end-use applications. Key segments include components that form the EUV system, types of equipment utilized, diverse applications in chip fabrication, and the end-use industries driving demand for EUV-enabled semiconductors. Analyzing these segments provides a comprehensive view of how different parts of the EUV value chain contribute to overall market growth and evolution.

The component segment encompasses the highly specialized parts integral to an EUV scanner, each representing a critical area of innovation and investment. Equipment types differentiate between the core scanner units and the essential metrology and inspection tools that ensure quality and yield. Application segmentation highlights the primary manufacturing processes benefiting from EUV, while end-use industries delineate the sectors ultimately consuming these high-performance chips, thereby providing insights into the overarching market drivers. This detailed breakdown is vital for stakeholders to identify strategic opportunities and address specific market needs.

- By Component:

- Light Sources (e.g., Laser-Produced Plasma, Droplet Generators)

- Mirrors (e.g., Multi-Layer Reflective Optics)

- Optical Systems (e.g., Projection Optics, Illumination Optics)

- Masks & Pellicles (e.g., EUV Reticles, Protective Pellicles)

- Resists (e.g., Chemically Amplified Resists, Metal-Oxide Resists)

- Other Components (e.g., Vacuum Systems, Contamination Control)

- By Equipment Type:

- EUV Scanners (e.g., Low-NA, High-NA)

- EUV Metrology Tools (e.g., CD-SEM, Overlay Metrology)

- EUV Inspection Tools (e.g., Mask Inspection, Wafer Inspection)

- By Application:

- Logic Manufacturing (e.g., Microprocessors, GPUs)

- Memory Manufacturing (DRAM, NAND Flash)

- Foundries (Contract Chip Manufacturing)

- Integrated Device Manufacturers (IDMs)

- Research & Development (Academic, Industrial Labs)

- By End-Use Industry:

- Consumer Electronics (e.g., Smartphones, Laptops)

- Automotive (e.g., ADAS, Infotainment)

- Healthcare (e.g., Medical Devices, Diagnostics)

- Industrial (e.g., Automation, Robotics)

- Telecommunications (e.g., 5G/6G Infrastructure)

- Others (e.g., Aerospace & Defense, Data Centers)

Regional Highlights

- Asia Pacific (APAC): Dominates the EUVL market due to the presence of major semiconductor foundries and IDMs in Taiwan, South Korea, China, and Japan. These countries are at the forefront of advanced node manufacturing and massive investments in new fab construction drive significant EUV demand. Government initiatives supporting domestic chip production further bolster market growth.

- North America: A key region for EUVL technology, driven by leading design companies and a renewed focus on establishing advanced manufacturing capabilities. Significant R&D investments and the presence of major equipment manufacturers and material suppliers contribute to its strong market position.

- Europe: A critical hub for EUVL innovation, primarily due to the headquarters of the dominant EUV equipment supplier and its extensive research ecosystem. While manufacturing presence is less concentrated than APAC, European contributions in core technology development and component supply are indispensable.

- Latin America: Expected to show nascent growth, primarily through partnerships and indirect demand from global supply chains. Direct EUV fab investment is currently limited but potential for future development exists.

- Middle East and Africa (MEA): Currently a smaller market for direct EUV adoption, but increasing investments in digital infrastructure and potential for future semiconductor manufacturing diversification could drive demand in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Extreme Ultraviolet Lithography Market.- ASML Holding N.V.

- Carl Zeiss SMT GmbH

- Nikon Corporation

- Canon Inc.

- Applied Materials Inc.

- KLA Corporation

- Lam Research Corporation

- Tokyo Electron Limited

- Advantest Corporation

- SCREEN Holdings Co., Ltd.

- NuFlare Technology Inc.

- Sumitomo Mitsui Construction Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- JSR Corporation

- DuPont de Nemours, Inc.

- Intel Corporation

- Samsung Electronics Co. Ltd.

- Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- Micron Technology

- SK Hynix Inc.

Frequently Asked Questions

What is Extreme Ultraviolet Lithography (EUVL)?

Extreme Ultraviolet Lithography (EUVL) is an advanced optical lithography technology used in semiconductor manufacturing to create the extremely small patterns required for next-generation microprocessors and memory chips. It utilizes extreme ultraviolet light with a wavelength of 13.5 nanometers, significantly shorter than conventional optical lithography, enabling the patterning of features at 7nm, 5nm, and smaller nodes.

Why is EUVL crucial for advanced semiconductor manufacturing?

EUVL is crucial because it provides the resolution necessary to pattern the increasingly tiny features on advanced semiconductors, enabling higher transistor density and improved performance for devices. Without EUVL, manufacturing chips at process nodes below 7nm would be significantly more complex, costly, or even impossible with conventional optical lithography techniques, hindering the progress of Moore's Law.

What are the primary challenges in EUVL adoption?

The primary challenges include the extremely high capital cost of EUV systems, the technical complexities associated with maintaining stable light sources and defect-free masks, and the intensive research and development required for new materials like resists and pellicles. Additionally, the highly concentrated supply chain and the shortage of specialized talent pose significant hurdles.

How does AI impact the Extreme Ultraviolet Lithography market?

AI significantly impacts the EUVL market by enhancing computational lithography for optimized mask designs, improving defect detection and classification, enabling predictive maintenance for complex equipment, and refining process parameters for higher yields. AI-driven simulations also accelerate R&D, contributing to overall efficiency and performance improvements in EUV manufacturing.

Which regions are leading in EUVL market adoption and investment?

Asia Pacific (APAC), particularly South Korea, Taiwan, China, and Japan, leads in EUVL market adoption and investment due to the presence of major foundries and IDMs driving advanced node production. North America also holds a strong position with significant R&D and manufacturing capabilities, while Europe contributes substantially through core technology development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted