Epoxy Phenol Novolac Market

Epoxy Phenol Novolac Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700240 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

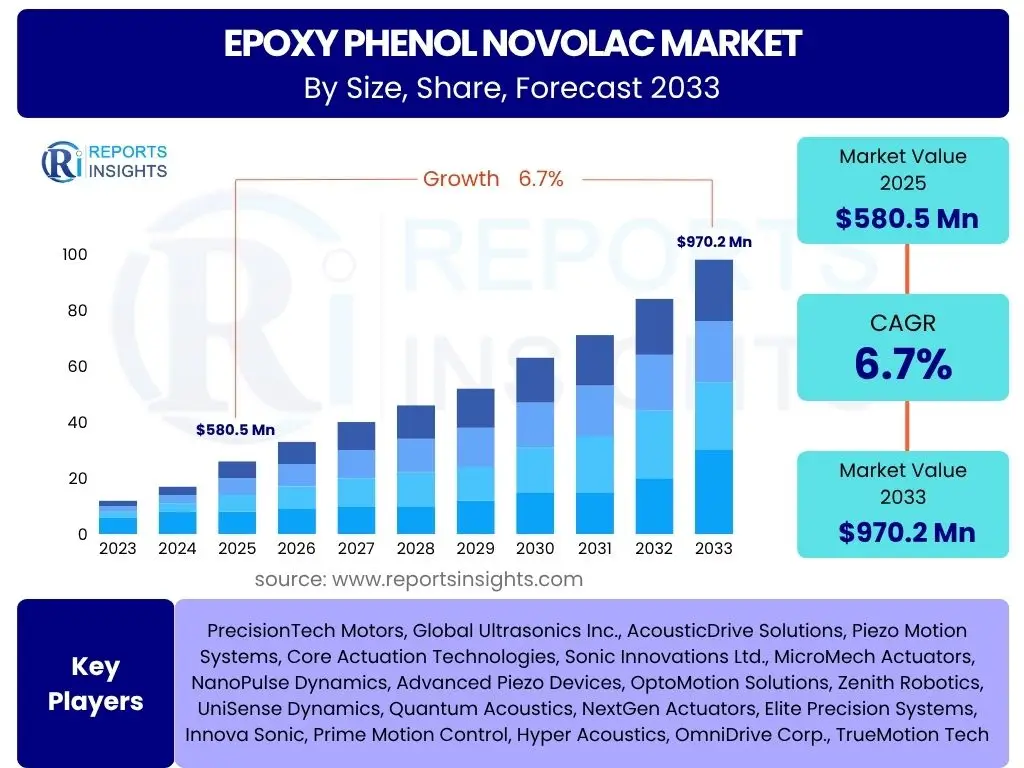

Epoxy Phenol Novolac Market is projected to grow at a Compound annual growth rate (CAGR) of 6.7% between 2025 and 2033, current valued at USD 580.5 Million in 2025 and is projected to grow by USD 970.2 Million by 2033, the end of the forecast period.

Key Epoxy Phenol Novolac Market Trends & Insights

The Epoxy Phenol Novolac market is currently witnessing a confluence of trends shaping its growth trajectory. Significant advancements in material science are leading to the development of enhanced novolac resins with superior thermal stability, chemical resistance, and adhesive properties, broadening their application scope. Furthermore, the increasing focus on miniaturization and high-performance requirements in the electronics industry is driving the demand for epoxy phenol novolacs in encapsulants and printed circuit board laminates. Environmental considerations are also influencing market dynamics, pushing manufacturers towards more sustainable and low-VOC formulations, aligning with global regulatory shifts and consumer preferences for greener solutions.

- Advancements in high-performance resin formulations.

- Rising demand from the electronics sector for encapsulation and PCB manufacturing.

- Growing adoption in lightweighting applications within automotive and aerospace.

- Increased focus on sustainable and eco-friendly novolac variants.

- Expansion of applications in industrial coatings and composites.

AI Impact Analysis on Epoxy Phenol Novolac

Artificial intelligence (AI) is poised to revolutionize various facets of the Epoxy Phenol Novolac market, from research and development to production and supply chain management. AI-driven predictive modeling can accelerate the discovery and optimization of new resin formulations, reducing development cycles and costs. In manufacturing, AI algorithms can enhance process control, optimize reaction conditions, and improve product consistency and quality, leading to higher yields and reduced waste. Furthermore, AI's analytical capabilities can provide deeper insights into market demand forecasting, supply chain vulnerabilities, and competitive landscapes, enabling more agile and informed strategic decisions for market players.

- Accelerated R&D for novel epoxy phenol novolac formulations through AI-driven simulations.

- Enhanced predictive maintenance and quality control in manufacturing processes.

- Optimized supply chain management and demand forecasting using AI analytics.

- Improved material property prediction and performance analysis for specific applications.

- Potential for autonomous process optimization in resin synthesis.

Key Takeaways Epoxy Phenol Novolac Market Size & Forecast

- The Epoxy Phenol Novolac market is set for robust growth, driven primarily by increasing demand across high-performance end-use industries like electronics, automotive, and industrial coatings.

- The market's expansion is notably influenced by technological advancements leading to superior material properties and broader application versatility.

- Despite potential challenges such as raw material price volatility and environmental regulations, innovation in sustainable formulations is expected to unlock new growth avenues.

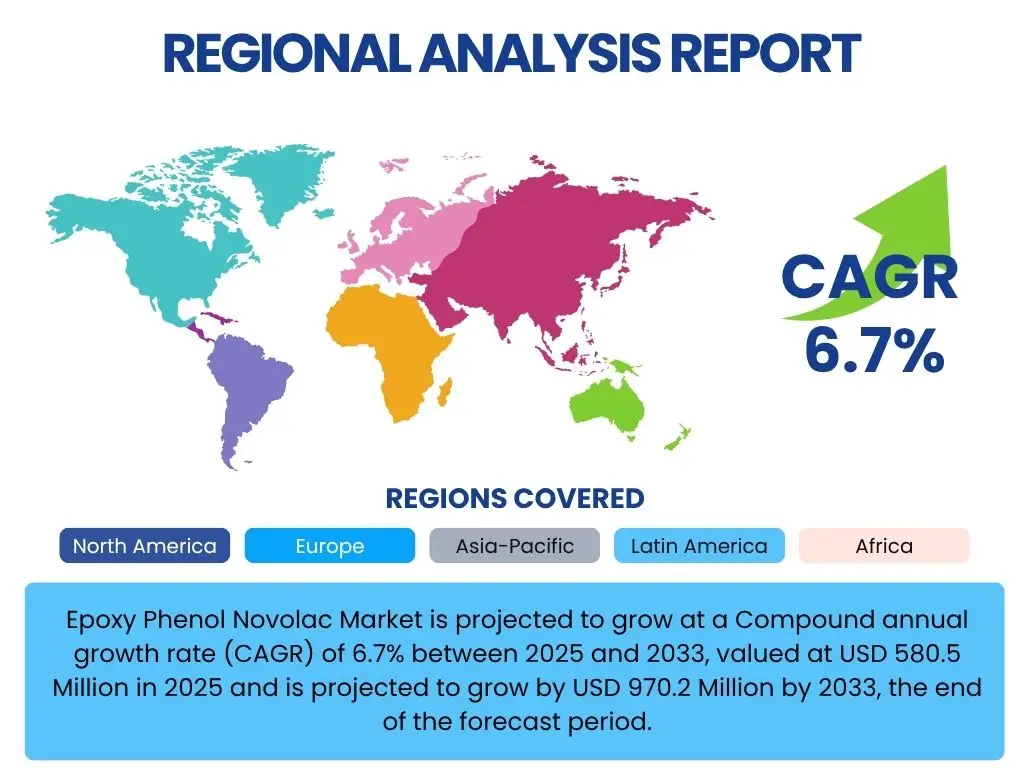

- Asia Pacific is anticipated to remain the dominant region, fueled by rapid industrialization and the booming electronics manufacturing sector.

- Strategic partnerships, mergers, and acquisitions, along with a strong focus on research and development, are key competitive factors influencing market share and positioning.

Epoxy Phenol Novolac Market Drivers Analysis

The Epoxy Phenol Novolac market is significantly propelled by the burgeoning demand from the electronics industry, where these resins are indispensable for encapsulating semiconductor components and fabricating high-performance printed circuit boards. Their excellent thermal stability, low coefficient of thermal expansion, and superior electrical insulation properties make them ideal for protecting delicate electronic devices from environmental factors and mechanical stress. The continuous evolution of electronic gadgets, miniaturization trends, and the pervasive adoption of advanced computing technologies further stimulate the consumption of epoxy phenol novolacs. This sustained growth in the electronics sector creates a foundational demand that underpins the overall market expansion.

Another crucial driver is the increasing adoption of epoxy phenol novolacs in the automotive sector, particularly for lightweighting initiatives and enhanced corrosion protection. As manufacturers strive to improve fuel efficiency and reduce emissions, the use of advanced composites and high-performance coatings becomes paramount. Epoxy phenol novolacs contribute to the structural integrity of composite materials used in vehicle components and provide durable, chemically resistant coatings for critical parts, extending their lifespan. The global automotive industry's consistent investment in advanced materials, coupled with stringent environmental regulations, ensures a steady uptake of these specialized resins. This trend is not limited to traditional vehicles but extends to electric vehicles, where thermal management and robust material performance are even more critical.

Furthermore, the expansion of industrial coatings, adhesives, and composite applications contributes substantially to market growth. Epoxy phenol novolacs are highly valued for their exceptional resistance to aggressive chemicals, high temperatures, and abrasive conditions, making them suitable for heavy-duty protective coatings in industrial infrastructure, chemical processing plants, and marine environments. Their superior bonding strength also makes them preferred choice in high-performance adhesives for various industrial assembly processes. The increasing investment in infrastructure development, coupled with the need for long-lasting and resilient materials in diverse industrial settings, creates a robust demand for epoxy phenol novolacs, driving innovation and market penetration across multiple sectors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Electronics Industry | +2.1% | Asia Pacific, North America, Europe | Short to Mid-term |

| Increasing Automotive Applications | +1.8% | Europe, North America, Asia Pacific | Mid to Long-term |

| Expanding Industrial Coatings & Adhesives | +1.5% | Global, particularly Emerging Economies | Mid-term |

| Advancements in Composite Materials | +0.8% | North America, Europe, Asia Pacific | Long-term |

| Focus on High-Performance Materials | +0.5% | Global | Ongoing |

Epoxy Phenol Novolac Market Restraints Analysis

The Epoxy Phenol Novolac market faces significant restraints primarily due to the volatility of raw material prices. Phenol and formaldehyde, the key precursors for novolac resins, are petrochemical derivatives, making their prices highly susceptible to fluctuations in crude oil markets, geopolitical instabilities, and supply-demand imbalances. Unpredictable shifts in these costs directly impact the production expenses of epoxy phenol novolacs, leading to unstable profit margins for manufacturers and potentially higher end-product prices for consumers. This price volatility can deter investment in new production capacities and compel end-users to seek more cost-stable alternative materials, thus impeding market growth and creating uncertainty across the value chain.

Another notable restraint is the increasing stringency of environmental regulations concerning the production and use of chemicals, including those involved in epoxy phenol novolac manufacturing. Regulations pertaining to volatile organic compound (VOC) emissions, hazardous waste disposal, and worker safety are becoming more stringent globally. Compliance often requires significant investment in new technologies, process modifications, and permits, which increases operational costs for manufacturers. These regulations can also limit the permissible uses of certain formulations or necessitate the development of more eco-friendly, yet potentially more expensive, alternatives. The challenge of navigating diverse and evolving regulatory landscapes across different regions adds complexity and cost, acting as a brake on market expansion.

Furthermore, the presence of alternative resin systems poses a competitive restraint to the Epoxy Phenol Novolac market. While epoxy phenol novolacs offer unique properties, other high-performance resins like bisphenol A epoxies, acrylics, polyurethanes, and silicones can sometimes offer comparable performance in certain applications at potentially lower costs or with different processing advantages. Manufacturers and end-users continuously evaluate these alternatives based on performance requirements, cost-effectiveness, ease of processing, and regulatory compliance. The availability and ongoing development of these competitive resins compel epoxy phenol novolac producers to constantly innovate and differentiate their products to maintain market share, creating a challenging environment for sustained growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices | -1.2% | Global | Short to Mid-term |

| Stringent Environmental Regulations | -0.9% | Europe, North America, parts of Asia Pacific | Mid to Long-term |

| Competition from Alternative Resins | -0.7% | Global | Ongoing |

| High Initial Investment for Production | -0.4% | Emerging Markets | Long-term |

| Supply Chain Disruptions | -0.3% | Global | Short-term (Event-driven) |

Epoxy Phenol Novolac Market Opportunities Analysis

Significant opportunities for the Epoxy Phenol Novolac market stem from the emergence of high-performance and specialized applications across various sectors. Industries such as aerospace, defense, and advanced industrial manufacturing are continuously seeking materials that can withstand extreme conditions, including high temperatures, aggressive chemicals, and significant mechanical stress. Epoxy phenol novolacs, with their superior thermal stability and chemical resistance, are ideal for these demanding environments. Their use in lightweight composite structures for aircraft components, protective coatings for military equipment, and high-temperature adhesives in industrial machinery opens up new, high-value market segments. The growing investment in these advanced industries provides a fertile ground for market expansion, driven by the need for enhanced material performance and durability.

The burgeoning trend towards sustainable chemistry and the development of bio-based materials presents another substantial opportunity for the Epoxy Phenol Novolac market. With increasing environmental consciousness and regulatory pressures, there is a rising demand for products derived from renewable resources and those with a lower environmental footprint. Research and development efforts focused on incorporating bio-derived feedstocks into novolac resin synthesis, or developing processes that reduce energy consumption and waste, can significantly enhance the market's appeal. Companies that successfully innovate in this area will not only meet evolving market preferences but also gain a competitive edge by aligning with global sustainability goals. This shift towards greener alternatives can unlock new partnerships and market niches.

Furthermore, the expansion into emerging economies offers vast untapped potential for the Epoxy Phenol Novolac market. Rapid industrialization, urbanization, and growing manufacturing capabilities in regions like Asia Pacific, Latin America, and parts of Africa are driving increased demand for advanced materials in electronics, automotive, construction, and industrial sectors. As these economies mature and their technological infrastructure develops, the need for high-performance resins like epoxy phenol novolacs for critical applications will escalate. Companies that strategically invest in establishing production facilities, distribution networks, and localized sales channels in these regions can capitalize on their high growth rates and burgeoning industrial output. This geographic expansion represents a long-term growth trajectory for the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of High-Performance Applications | +1.5% | Global, especially Developed Economies | Mid to Long-term |

| Development of Bio-based Novolac Resins | +1.0% | Europe, North America, Asia Pacific | Long-term |

| Expansion in Emerging Economies | +0.8% | Asia Pacific, Latin America, MEA | Mid to Long-term |

| Technological Advancements in Synthesis | +0.6% | Global | Ongoing |

| Increasing Demand for Smart Electronics | +0.5% | Asia Pacific, North America | Short to Mid-term |

Epoxy Phenol Novolac Market Challenges Impact Analysis

The Epoxy Phenol Novolac market is confronted by significant challenges, notably the stringent regulatory compliance required across various jurisdictions. The chemicals used in the production and formulation of epoxy phenol novolacs, as well as the finished products themselves, are subject to a complex web of environmental, health, and safety regulations. These include rules on chemical registration (like REACH in Europe), restrictions on hazardous substances, occupational safety standards, and waste management guidelines. Meeting these diverse and often evolving regulatory requirements demands substantial investment in research, testing, and process adjustments, increasing operational costs and potentially delaying market entry for new products or formulations. Non-compliance can result in hefty fines, production halts, and reputational damage, posing a continuous hurdle for market participants.

Another critical challenge is the inherent difficulty and cost associated with the disposal and recycling of thermoset resins like epoxy phenol novolacs. Unlike thermoplastics, thermosets undergo irreversible chemical changes upon curing, making them difficult to melt and reform. This property, while beneficial for their end-use performance, presents a significant environmental and economic challenge at the end of their lifecycle. Current recycling methods for thermosets are often energy-intensive and produce lower-value materials, or simply lead to incineration or landfill disposal. As sustainability mandates become more pervasive, the industry faces increasing pressure to develop viable, cost-effective recycling solutions or alternative end-of-life strategies, which requires substantial R&D investment and collaborative efforts across the value chain. This challenge could limit market growth if sustainable disposal methods are not adequately addressed.

Furthermore, the market faces challenges related to intellectual property (IP) protection and the potential for counterfeiting, particularly in developing regions. Innovations in epoxy phenol novolac formulations, synthesis processes, and application techniques are crucial for maintaining a competitive edge. However, the risk of unauthorized replication of patented technologies or the production of counterfeit products can undermine investments in R&D and erode market share for legitimate manufacturers. Protecting proprietary formulations and processes across diverse legal frameworks globally is a complex and costly endeavor. This challenge not only impacts the profitability of innovators but can also lead to the proliferation of inferior products that may compromise safety and performance standards, thereby harming the market's overall reputation and potentially stifling further innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Compliance | -1.0% | Global, particularly Europe and North America | Ongoing |

| Disposal and Recycling Issues | -0.7% | Global | Mid to Long-term |

| Intellectual Property Protection | -0.5% | Asia Pacific, Emerging Markets | Ongoing |

| Skilled Labor Shortage | -0.3% | Developed Economies | Mid-term |

| Economic Slowdowns Affecting End-Use | -0.2% | Global | Short-term (Cyclical) |

Epoxy Phenol Novolac Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Epoxy Phenol Novolac market, offering critical insights into its current state and future growth trajectory. The report encompasses historical data, current market dynamics, and robust forecasts, enabling stakeholders to make informed strategic decisions. It delves into key market trends, significant drivers, restraining factors, emerging opportunities, and potential challenges that are shaping the industry landscape. Furthermore, the report offers a detailed segmentation analysis, regional breakdowns, and profiles of leading market players, providing a holistic view of the market's competitive structure and growth potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 580.5 Million |

| Market Forecast in 2033 | USD 970.2 Million |

| Growth Rate | 6.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Resins Solutions, Advanced Polymer Innovations, Chemical Synthetics Group, Industrial Coatings Dynamics, ElectroMaterials Co., Precision Adhesives Corp., Novolac Technologies Inc., Sustainable Chemical Products, High-Performance Polymers Ltd., Specialty Resins International, Universal Composites Alliance, Integrated Materials Group, FutureChem Industries, Vertex Chemical Solutions, OmniPolymer Systems, Phoenix Resins & Coatings, Synergy Chemical Corp., Apex Advanced Materials, InnovateChem Solutions, MegaResin Global |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

:The Epoxy Phenol Novolac market is meticulously segmented to provide a granular understanding of its diverse applications and product variations, enabling precise market analysis and strategic planning. These segmentations allow for a detailed examination of market dynamics within specific product types, application areas, and end-use industries, highlighting growth pockets and opportunities. Understanding these distinct segments is crucial for identifying targeted marketing strategies, product development priorities, and competitive positioning within the complex chemical industry landscape. Each segment contributes uniquely to the overall market growth, driven by specific industry needs and technological advancements.

The market is primarily segmented by Type, which includes Liquid Epoxy Phenol Novolac, Solid Epoxy Phenol Novolac, and Solution-based Epoxy Phenol Novolac. Liquid forms are often favored for coatings and adhesives due to their ease of processing, while solid variants are critical for electrical laminates and molding compounds where higher thermal stability is required. Solution-based products offer versatility in application and can be tailored for specific industrial processes. Each type possesses distinct properties that dictate its suitability for various applications, directly impacting their demand across different sectors. This breakdown helps in analyzing the supply-side capabilities and technological advancements across different forms of the resin.

Further segmentation is based on Application, encompassing Adhesives, Coatings, Composites, Encapsulation, Electrical Laminates (PCBs), Casting and Tooling, and Other Applications. The Composites segment further subdivides into Aerospace Composites, Automotive Composites, and Industrial Composites, reflecting the growing adoption of lightweight, high-strength materials in these demanding sectors. Encapsulation in electronics and electrical laminates for printed circuit boards represent significant high-value applications due to the superior electrical and thermal properties of these resins. These application segments highlight the versatility and critical role of epoxy phenol novolacs in diverse manufacturing processes, with each application driving demand based on specific performance requirements and end-product innovation.

The End-Use Industry segmentation is vital for understanding demand origins, categorizing the market into Electronics & Electrical, Automotive & Transportation, Aerospace & Defense, Marine, Industrial Manufacturing, Construction, Oil & Gas, Chemical Processing, and Other End-Use Industries. The Electronics & Electrical sector remains a dominant consumer, driven by continuous innovation and increasing demand for reliable, high-performance components. Automotive & Transportation, along with Aerospace & Defense, are growing rapidly due to the focus on lightweighting and enhanced durability. The Industrial Manufacturing, Construction, Oil & Gas, and Chemical Processing sectors rely on epoxy phenol novolacs for their exceptional chemical and corrosion resistance, ensuring longevity and safety in harsh environments. Analyzing these end-use industries provides a clear picture of the primary revenue streams and emerging opportunities for market players.

- By Type:

- Liquid Epoxy Phenol Novolac: Predominantly used in liquid formulations for coatings, flooring, and casting.

- Solid Epoxy Phenol Novolac: Preferred for molding compounds, powder coatings, and electrical laminates due to their higher molecular weight and thermal performance.

- Solution-based Epoxy Phenol Novolac: Utilized in specialized applications where specific solvent characteristics are required for processing.

- By Application:

- Adhesives: For high-strength, chemical-resistant bonding in various industrial applications.

- Coatings: Protective layers in industrial, marine, andchemical processing environments.

- Composites: Reinforcing materials for lightweight structures requiring high strength and temperature resistance.

- Aerospace Composites: For aircraft components, interiors, and structures.

- Automotive Composites: For vehicle body parts, chassis, and under-hood components.

- Industrial Composites: For pipes, tanks, and structural elements in harsh industrial settings.

- Encapsulation: Protecting electronic components, semiconductors, and integrated circuits.

- Electrical Laminates (PCBs): As critical binders for printed circuit boards, offering excellent dielectric properties.

- Casting and Tooling: For molds, patterns, and prototypes requiring high dimensional stability and heat resistance.

- Other Applications: Including sealants, putties, and specialized industrial uses.

- By End-Use Industry:

- Electronics & Electrical: Essential for semiconductors, PCBs, and electrical insulation.

- Automotive & Transportation: Used in vehicle structures, coatings, and adhesives for durability and lightweighting.

- Aerospace & Defense: For high-performance composites, structural components, and protective coatings.

- Marine: Anti-corrosion coatings and structural components for boats and ships.

- Industrial Manufacturing: Protective coatings for machinery, flooring, and chemical equipment.

- Construction: Heavy-duty flooring, protective coatings, and structural adhesives.

- Oil & Gas: Pipeline coatings, tanks, and equipment for corrosion resistance in harsh conditions.

- Chemical Processing: Linings for reaction vessels, storage tanks, and pipes due to excellent chemical resistance.

- Other End-Use Industries: Includes wind energy, sports equipment, and consumer goods.

- By Region:

- North America: Mature market with strong R&D and high-value applications.

- Europe: Driven by stringent regulations and emphasis on sustainable solutions.

- Asia Pacific (APAC): Largest and fastest-growing market due to manufacturing hubs and industrialization.

- Latin America: Emerging market with growing industrial base and infrastructure development.

- Middle East & Africa (MEA): Driven by oil & gas, construction, and infrastructure projects.

Regional Highlights

The global Epoxy Phenol Novolac market exhibits distinct regional dynamics, influenced by varying industrial landscapes, regulatory environments, and technological advancements. Asia Pacific stands out as the leading region, and is also projected to be the fastest-growing market throughout the forecast period. This dominance is primarily attributed to the region's robust manufacturing sector, particularly in electronics, automotive, and industrial production, especially in countries like China, Japan, South Korea, and India. The sheer scale of electronic component manufacturing and the expanding automotive industry in these nations create a substantial and continuous demand for high-performance epoxy phenol novolacs for encapsulation, PCB fabrication, and lightweight composite applications. Furthermore, rapid urbanization and industrial infrastructure development in emerging economies within APAC are significantly boosting the consumption of these resins in coatings and adhesives.

North America and Europe represent mature markets for Epoxy Phenol Novolac, characterized by a strong emphasis on advanced research and development, stringent regulatory frameworks, and a focus on high-value, specialized applications. In North America, the demand is largely driven by the aerospace and defense industries, sophisticated electronics manufacturing, and the automotive sector's continuous innovation in electric vehicles and lightweight materials. The region also exhibits a high adoption rate of advanced industrial coatings and composites. Europe, similarly, benefits from a well-established industrial base, particularly in automotive, chemical processing, and wind energy. The region's proactive approach to environmental regulations is also fostering innovation in sustainable and low-VOC epoxy phenol novolac formulations, pushing manufacturers towards greener solutions and ensuring long-term market stability.

Latin America, and the Middle East and Africa (MEA) are emerging markets for Epoxy Phenol Novolac, showing promising growth prospects driven by increasing industrialization, infrastructure development, and diversification of economies. In Latin America, the expanding automotive and construction sectors, coupled with growing electronics assembly, are fueling demand. The MEA region is witnessing significant investments in oil and gas infrastructure, chemical processing plants, and construction projects, all of which require high-performance coatings and structural materials that can withstand harsh environmental conditions. While these regions currently hold smaller market shares compared to APAC, North America, and Europe, their ongoing industrial expansion and growing appetite for advanced materials are expected to contribute significantly to the global market's growth in the mid to long term, offering new opportunities for market players to establish a foothold and expand their operations.

- Asia Pacific (APAC): Dominant market share and fastest growth attributed to robust electronics manufacturing, rapid industrialization in China, South Korea, and Japan, and increasing automotive production.

- North America: Significant market driven by advanced electronics, aerospace & defense industries, and high-performance automotive applications, coupled with strong R&D investments.

- Europe: Mature market with demand from automotive, chemical processing, and renewable energy sectors, alongside a strong focus on regulatory compliance and sustainable product development.

- Latin America: Growing market fueled by increasing industrialization, infrastructure development, and expanding automotive manufacturing capabilities.

- Middle East & Africa (MEA): Emerging demand primarily from the oil & gas industry, construction sector, and infrastructure projects requiring durable and corrosion-resistant materials.

Top Key Players:

The market research report covers the analysis of key stake holders of the Epoxy Phenol Novolac Market. Some of the leading players profiled in the report include -:- Global Resins Solutions

- Advanced Polymer Innovations

- Chemical Synthetics Group

- Industrial Coatings Dynamics

- ElectroMaterials Co.

- Precision Adhesives Corp.

- Novolac Technologies Inc.

- Sustainable Chemical Products

- High-Performance Polymers Ltd.

- Specialty Resins International

- Universal Composites Alliance

- Integrated Materials Group

- FutureChem Industries

- Vertex Chemical Solutions

- OmniPolymer Systems

- Phoenix Resins & Coatings

- Synergy Chemical Corp.

- Apex Advanced Materials

- InnovateChem Solutions

- MegaResin Global

Frequently Asked Questions:

What is Epoxy Phenol Novolac?

Epoxy Phenol Novolac is a high-performance thermosetting resin synthesized from phenol and formaldehyde, cured with epoxy resins. It is valued for its exceptional thermal stability, chemical resistance, mechanical strength, and electrical insulation properties, making it indispensable in demanding applications.What are the primary applications of Epoxy Phenol Novolac?

The primary applications of Epoxy Phenol Novolac include electrical laminates for printed circuit boards (PCBs), semiconductor encapsulation, high-performance protective coatings, industrial adhesives, and advanced composite materials for aerospace and automotive industries.How is the Epoxy Phenol Novolac market growing?

The Epoxy Phenol Novolac market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033, driven by increasing demand from the electronics, automotive, and industrial sectors, alongside advancements in material science.What drives the growth of the Epoxy Phenol Novolac market?

Key drivers of the Epoxy Phenol Novolac market include the expanding electronics industry, increasing adoption in automotive for lightweighting and corrosion protection, and growing demand for high-performance protective coatings and advanced composite materials in various industrial applications.What are the key challenges facing the Epoxy Phenol Novolac market?

Major challenges for the Epoxy Phenol Novolac market include the volatility of raw material prices, stringent environmental regulations regarding chemical production and emissions, difficulties in the disposal and recycling of thermoset resins, and intense competition from alternative resin systems.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted