Cycloaliphatic Epoxy Resin Market

Cycloaliphatic Epoxy Resin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701610 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

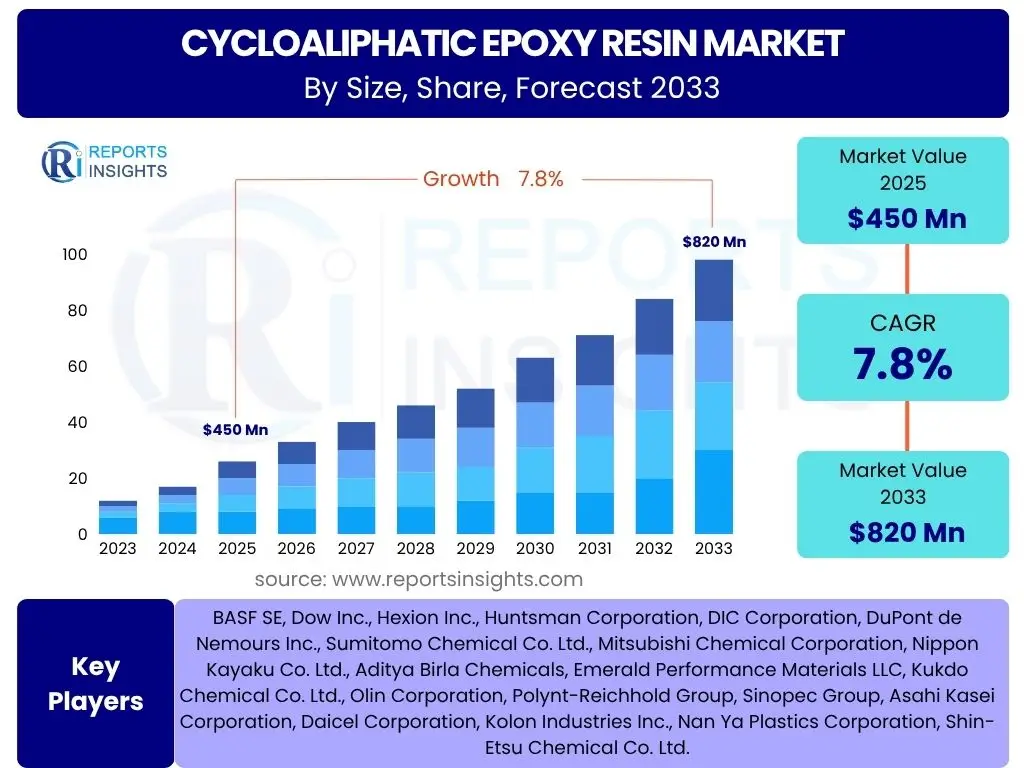

Cycloaliphatic Epoxy Resin Market Size

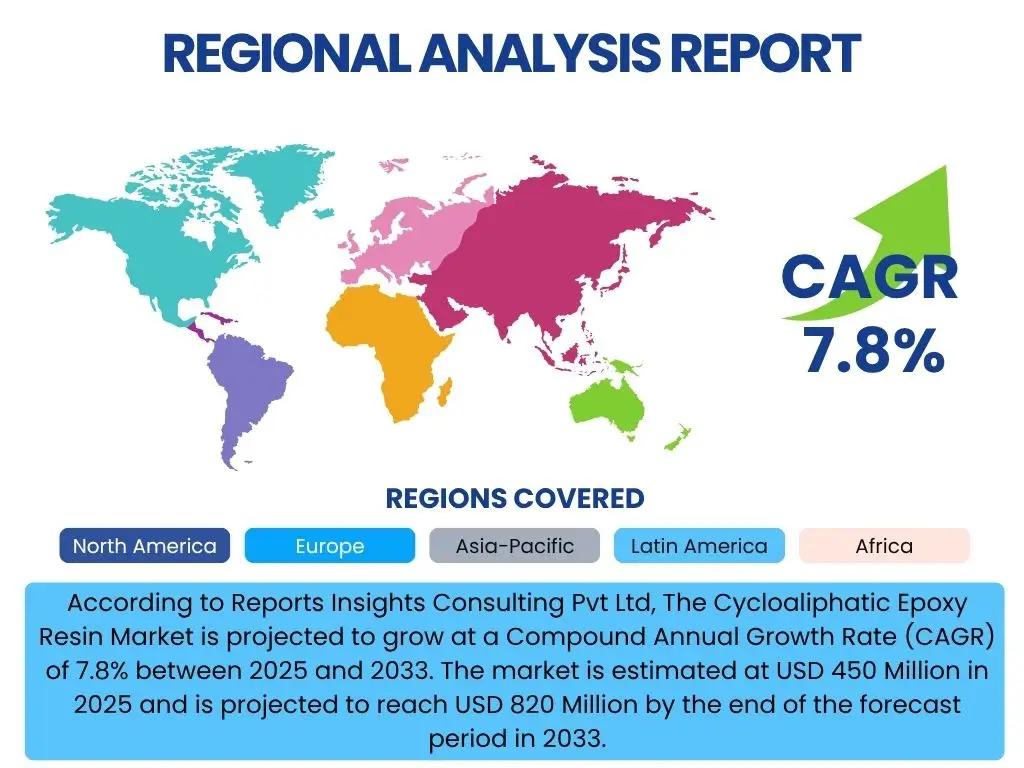

According to Reports Insights Consulting Pvt Ltd, The Cycloaliphatic Epoxy Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 820 Million by the end of the forecast period in 2033.

Key Cycloaliphatic Epoxy Resin Market Trends & Insights

The cycloaliphatic epoxy resin market is experiencing dynamic shifts driven by escalating demand for high-performance materials across diverse industrial applications. Users frequently inquire about the leading technological advancements and sustainability initiatives shaping the industry. A significant trend involves the increasing adoption of these resins in specialized electrical and electronic components, where their superior dielectric properties, thermal stability, and low shrinkage are highly valued. Furthermore, the market is witnessing a strong push towards developing environmentally friendly solutions, including bio-based formulations and more efficient curing systems, addressing both regulatory pressures and consumer preferences for sustainable products.

Another prominent trend observed is the growing integration of cycloaliphatic epoxy resins in outdoor electrical insulation systems, particularly in harsh environmental conditions. This is fueled by expanding renewable energy infrastructure, such as solar power installations and wind turbines, which require materials capable of withstanding extreme temperatures, UV radiation, and moisture without degradation. The miniaturization of electronic devices and the advent of 5G technology are also creating new opportunities, demanding resins with enhanced purity, faster curing times, and improved optical clarity for sophisticated applications like LED encapsulants and advanced optical lenses. This continuous innovation in material science is pivotal to meeting the evolving technical requirements of end-use industries.

- Increasing demand from electrical and electronics industries for high-performance insulation and encapsulation.

- Growing adoption in LED encapsulants and optical components due to superior transparency and UV stability.

- Shift towards high-performance materials in outdoor electrical insulation, driven by renewable energy expansion.

- Rising focus on sustainable and bio-based epoxy resin formulations to meet environmental regulations.

- Technological advancements in curing agents and additives for improved processing and performance characteristics.

AI Impact Analysis on Cycloaliphatic Epoxy Resin

User inquiries regarding the impact of Artificial Intelligence (AI) on the cycloaliphatic epoxy resin market primarily revolve around process optimization, new material development, and supply chain efficiency. AI is poised to revolutionize manufacturing processes by enabling predictive maintenance, optimizing reaction parameters for synthesis, and enhancing quality control. Machine learning algorithms can analyze vast datasets from production lines to identify anomalies, predict equipment failures, and fine-tune operating conditions, leading to significant reductions in waste, energy consumption, and production costs. This analytical capability ensures a higher yield of high-purity resins, crucial for sensitive applications.

Beyond manufacturing, AI is significantly accelerating research and development efforts in cycloaliphatic epoxy resin formulations. AI-driven computational chemistry and materials informatics can predict the properties of novel resin compositions, simulate their performance under various conditions, and identify optimal molecular structures with desired characteristics. This reduces the need for extensive physical experimentation, dramatically shortening the product development cycle and fostering innovation in areas like improved thermal resistance, dielectric strength, or bio-degradability. The ability of AI to sift through complex chemical interactions allows for the rapid exploration of a wider design space, leading to breakthroughs in new applications.

Furthermore, AI plays a critical role in enhancing supply chain resilience and transparency for cycloaliphatic epoxy resins. By analyzing global demand patterns, raw material availability, and logistics networks, AI can optimize inventory management, predict potential disruptions, and recommend alternative sourcing strategies. This proactive approach minimizes lead times, ensures a stable supply of critical raw materials, and helps manufacturers navigate volatile market conditions more effectively. The integration of AI tools across the value chain will lead to a more efficient, responsive, and robust cycloaliphatic epoxy resin market.

- Process Optimization: AI-driven predictive maintenance and real-time parameter adjustments in manufacturing, leading to enhanced efficiency and reduced waste.

- New Material Design: Acceleration of R&D through AI-powered computational chemistry for predicting and optimizing novel resin properties.

- Supply Chain Optimization: Improved inventory management, demand forecasting, and risk mitigation through AI analytics.

- Quality Control: Enhanced anomaly detection and consistency assurance in resin production using machine learning algorithms.

Key Takeaways Cycloaliphatic Epoxy Resin Market Size & Forecast

User queries regarding key takeaways from the cycloaliphatic epoxy resin market size and forecast consistently highlight the pivotal role of specific end-use industries and geographical regions in shaping its future trajectory. A primary insight is the sustained and robust growth anticipated from the electrical and electronics sector, which remains the largest consumer due to the resins' indispensable properties in insulation, encapsulation, and component protection. The rapid evolution of technologies like 5G, advanced computing, and electric vehicles is set to further solidify this demand, driving innovation in resin purity and performance characteristics.

Another significant takeaway underscores the unparalleled growth opportunities in the Asia Pacific region. This dominance is attributed to burgeoning manufacturing bases, increasing foreign direct investment, and a rapidly expanding electronics industry in countries such as China, Japan, South Korea, and India. The region's commitment to developing smart cities and renewable energy infrastructure also fuels the demand for high-performance insulation and protective coatings, making it a critical hub for market expansion. This geographical concentration of demand emphasizes the strategic importance of localized production and distribution networks.

Finally, the market forecast indicates that innovation in material science, particularly towards sustainable and application-specific formulations, will be a crucial differentiator for market players. The growing emphasis on environmental regulations and corporate sustainability targets is pushing manufacturers to invest in bio-based resins, lower VOC (Volatile Organic Compounds) formulations, and energy-efficient curing processes. Companies that successfully adapt to these evolving demands, offering tailored solutions with enhanced environmental profiles, are poised to capture significant market share and ensure long-term competitiveness.

- Dominant growth in the Asia Pacific region, driven by expanding electronics manufacturing and infrastructure development.

- Electrical and electronics sectors remain the primary and most significant application segment, fueled by technological advancements.

- Innovation in UV-curable, high-purity, and high-performance formulations is crucial for meeting evolving industry standards.

- Increasing focus on sustainability and bio-based alternatives presents new avenues for product development and market penetration.

- Strategic partnerships and localized production are essential for navigating regional market dynamics and supply chain complexities.

Cycloaliphatic Epoxy Resin Market Drivers Analysis

The cycloaliphatic epoxy resin market is experiencing robust growth propelled by several key drivers, primarily stemming from the increasing demand for high-performance materials across critical industries. The expanding global electronics and electrical sectors are a significant impetus, necessitating materials with superior dielectric strength, thermal stability, and resistance to environmental degradation. Cycloaliphatic epoxy resins excel in these properties, making them indispensable for applications such as electrical insulation, transformers, circuit boards, and various electronic components where reliability and longevity are paramount.

The burgeoning LED lighting industry also represents a strong growth catalyst. As LED technology advances and becomes more ubiquitous, the demand for high-transparency encapsulants that can withstand UV exposure without yellowing or cracking increases. Cycloaliphatic epoxy resins, with their excellent optical clarity and UV resistance, are ideally suited for LED encapsulation, ensuring optimal light output and extended product lifespan. This trend is further amplified by global initiatives promoting energy-efficient lighting solutions, leading to widespread adoption of LED technology in both commercial and residential settings.

Moreover, the global push towards renewable energy infrastructure, including solar power generation and wind turbines, significantly contributes to market expansion. These critical energy systems require robust outdoor electrical insulation materials that can endure harsh environmental conditions, including extreme temperatures, moisture, and UV radiation, for prolonged periods. Cycloaliphatic epoxy resins provide the necessary durability and performance, ensuring the reliable operation and longevity of components in renewable energy installations, thereby driving their demand in this high-growth sector.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electrical and Electronics Industry | +1.2% | Global, particularly Asia Pacific (China, South Korea) | 2025-2033 (Long-term) |

| Increasing Demand for LED Encapsulants | +0.8% | Global, particularly Asia Pacific, North America | 2025-2033 (Mid to Long-term) |

| Expansion of Renewable Energy Infrastructure | +0.7% | Europe, North America, Asia Pacific (China, India) | 2025-2033 (Long-term) |

| Advancements in Outdoor Electrical Insulation | +0.5% | Global, particularly developing economies | 2025-2030 (Mid-term) |

Cycloaliphatic Epoxy Resin Market Restraints Analysis

Despite the promising growth trajectory, the cycloaliphatic epoxy resin market faces several significant restraints that could impede its full potential. A primary challenge is the relatively high production cost associated with these specialized resins compared to conventional epoxy resins. The complex synthesis processes and the need for high-purity raw materials contribute to higher manufacturing expenses, which can limit their adoption in cost-sensitive applications or regions where budget constraints are more stringent. This cost disadvantage often drives manufacturers in some sectors to opt for more economical, albeit less performant, alternative materials, thereby restricting market expansion.

Another crucial restraint is the volatility of raw material prices. The synthesis of cycloaliphatic epoxy resins relies on petroleum-derived intermediates, making them susceptible to fluctuations in global crude oil prices and the supply chain dynamics of these petrochemicals. Unpredictable price swings can significantly impact manufacturing costs, profit margins, and the overall financial planning for producers. Such instability makes it challenging for manufacturers to offer competitive and stable pricing to their end-users, potentially hindering long-term contract agreements and market consistency.

Furthermore, stringent environmental regulations regarding the use and disposal of certain chemical compounds, as well as the increasing scrutiny over industrial emissions, pose a significant restraint. While cycloaliphatic epoxy resins generally offer better performance in specific applications, their manufacturing processes and potential end-of-life disposal can come under regulatory pressure. Compliance with evolving environmental standards often necessitates additional investments in R&D for greener formulations and advanced waste management systems, adding to the operational burden for market players and potentially slowing innovation if not adequately addressed.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Cost | -0.6% | Global, particularly developing regions | 2025-2033 (Long-term) |

| Volatility of Raw Material Prices | -0.4% | Global, especially regions reliant on imported raw materials | 2025-2030 (Mid-term) |

| Competition from Alternative Materials | -0.3% | Global, in non-critical applications | 2025-2033 (Long-term) |

| Environmental Regulations and Disposal Concerns | -0.2% | Europe, North America, rapidly industrializing APAC countries | 2025-2033 (Long-term) |

Cycloaliphatic Epoxy Resin Market Opportunities Analysis

Significant opportunities are emerging for the cycloaliphatic epoxy resin market, primarily driven by rapid technological advancements and increasing demand for high-performance materials in cutting-edge applications. The advent of 5G technology and the ongoing trend towards miniaturization in electronics present a vast untapped potential. These innovations require extremely reliable, compact, and high-purity insulating and encapsulating materials that can operate effectively in high-frequency environments. Cycloaliphatic epoxy resins, with their superior dielectric properties, low loss factors, and excellent thermal management capabilities, are uniquely positioned to meet these stringent requirements, enabling new product designs and functionalities in communication infrastructure and portable devices.

Another compelling opportunity lies in the development and commercialization of bio-based cycloaliphatic epoxy resins. As industries increasingly prioritize sustainability and reduce their carbon footprint, the demand for environmentally friendly alternatives to petroleum-derived chemicals is growing rapidly. Investing in research and development for bio-based feedstock and sustainable synthesis routes can unlock new market segments and attract eco-conscious consumers and industries. This aligns with global regulatory trends and corporate sustainability goals, providing a significant competitive advantage and opening doors to partnerships with companies committed to green initiatives.

Furthermore, the expanding automotive and aerospace sectors, particularly with the rise of electric vehicles (EVs) and advanced avionics, offer lucrative growth avenues. These industries require lightweight, high-strength composites and robust encapsulation materials for critical electronic components, battery systems, and structural applications that can withstand extreme operational conditions. Cycloaliphatic epoxy resins contribute to enhancing the durability, safety, and efficiency of these next-generation vehicles and aircraft. Strategic collaborations with key players in these sectors can facilitate market penetration and establish these resins as standard materials for future mobility solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of 5G Technology and Miniaturization | +1.0% | Global, particularly North America, Asia Pacific (China, South Korea) | 2025-2030 (Mid-term) |

| Development of Bio-based Cycloaliphatic Epoxy Resins | +0.9% | Europe, North America | 2027-2033 (Long-term) |

| Untapped Potential in Emerging Economies (Ex-China/India) | +0.7% | Southeast Asia, Latin America, Africa | 2028-2033 (Long-term) |

| Demand for High-Performance Coatings and Adhesives | +0.6% | Global, particularly industrial and automotive sectors | 2025-2033 (Long-term) |

Cycloaliphatic Epoxy Resin Market Challenges Impact Analysis

The cycloaliphatic epoxy resin market faces several intrinsic and external challenges that could potentially hinder its growth. One significant challenge pertains to the complex synthesis and processing requirements of these specialized resins. Achieving the desired purity, molecular weight, and specific functionalities often involves intricate chemical reactions and precise control over manufacturing conditions. This complexity translates into higher production costs, requires specialized equipment, and demands a highly skilled workforce, limiting the number of manufacturers capable of producing high-quality cycloaliphatic epoxy resins consistently. These barriers to entry can slow down market expansion and innovation by deterring new players.

Another prominent challenge is the intense competitive landscape, particularly from conventional epoxy resins and other alternative materials. While cycloaliphatic epoxy resins offer superior properties in specific applications, their higher cost and niche performance characteristics mean they must continually demonstrate clear value propositions over more commoditized alternatives. Manufacturers must invest significantly in R&D to maintain their technological edge and differentiate their products based on performance, purity, and application-specific advantages. Without continuous innovation and clear market positioning, these resins risk being substituted in less demanding or cost-sensitive applications.

Furthermore, global supply chain disruptions pose a persistent challenge to the cycloaliphatic epoxy resin market. Dependence on a limited number of raw material suppliers or specific production regions can make the supply chain vulnerable to geopolitical events, natural disasters, or logistical bottlenecks. Such disruptions can lead to raw material shortages, price spikes, and delays in product delivery, impacting manufacturing schedules and profitability. Ensuring supply chain resilience through diversification of sourcing and strategic inventory management is crucial for mitigating these risks and maintaining market stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Synthesis and Processing | -0.5% | Global, particularly smaller manufacturers | 2025-2033 (Long-term) |

| Intense Competitive Landscape | -0.3% | Global, in all application segments | 2025-2033 (Long-term) |

| Limited Awareness in Niche Applications | -0.2% | Emerging markets, new application areas | 2025-2030 (Mid-term) |

| Supply Chain Disruptions | -0.4% | Global, particularly for specialized raw materials | 2025-2028 (Short to Mid-term) |

Cycloaliphatic Epoxy Resin Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global cycloaliphatic epoxy resin market, covering historical performance, current market dynamics, and future projections. It delivers crucial insights into market size, growth drivers, restraints, opportunities, and challenges, offering a detailed segmentation by type, application, and end-use industry. The report also includes a thorough regional analysis and profiles of key market players to provide a holistic view of the competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 820 Million |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Dow Inc., Hexion Inc., Huntsman Corporation, DIC Corporation, DuPont de Nemours Inc., Sumitomo Chemical Co. Ltd., Mitsubishi Chemical Corporation, Nippon Kayaku Co. Ltd., Aditya Birla Chemicals, Emerald Performance Materials LLC, Kukdo Chemical Co. Ltd., Olin Corporation, Polynt-Reichhold Group, Sinopec Group, Asahi Kasei Corporation, Daicel Corporation, Kolon Industries Inc., Nan Ya Plastics Corporation, Shin-Etsu Chemical Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The cycloaliphatic epoxy resin market is broadly segmented based on various critical factors, including type, application, and end-use industry. This granular segmentation provides a comprehensive view of the market's dynamics, highlighting the specific areas of growth and demand. The 'By Type' segment differentiates between high-purity resins, essential for sensitive electronic and optical applications requiring superior clarity and minimal impurities, and general-purpose resins, which cater to a broader range of industrial uses where cost-effectiveness and good overall performance are key. Understanding these distinctions is vital for manufacturers to tailor their product offerings and for consumers to select the appropriate resin for their specific requirements.

The 'By Application' segment details the diverse uses of cycloaliphatic epoxy resins across various sectors. Electrical insulation remains a cornerstone application due to the resins' excellent dielectric properties, crucial for high-voltage components and power transmission. LED encapsulation leverages their high transparency and UV stability, ensuring long-term performance of light-emitting diodes. Additionally, their use in optical components, high-performance coatings, and advanced composites underscores their versatility and growing adoption in demanding environments where traditional materials fall short. This wide array of applications highlights the material's adaptability and critical role in modern industrial processes.

Furthermore, the 'By End-Use Industry' segment provides insight into the primary sectors driving market demand. The electronics industry leads consumption, driven by continuous innovation in devices and components. The automotive and aerospace & defense sectors are increasingly adopting these resins for lightweighting, structural integrity, and electronic component protection. Energy & power, construction, and medical industries also represent significant segments, utilizing these resins for robust insulation, durable coatings, and specialized medical devices, respectively. This diversified end-use landscape ensures a stable and growing demand base for cycloaliphatic epoxy resins across global markets.

- By Type:

- High Purity Cycloaliphatic Epoxy Resins

- General Purpose Cycloaliphatic Epoxy Resins

- By Application:

- Electrical Insulation

- LED Encapsulation

- Optical Components

- Coating & Adhesives

- Composites

- Other Applications

- By End-Use Industry:

- Electronics

- Automotive

- Aerospace & Defense

- Energy & Power

- Construction

- Medical

- Others

Regional Highlights

The global cycloaliphatic epoxy resin market exhibits distinct regional dynamics, influenced by varying industrial landscapes, technological advancements, and regulatory frameworks. Asia Pacific consistently stands as the dominant and fastest-growing region, primarily driven by its robust manufacturing base, particularly in the electronics and electrical industries. Countries such as China, Japan, South Korea, and Taiwan are at the forefront of electronic component production and LED manufacturing, fueling a significant demand for high-purity cycloaliphatic epoxy resins. Rapid urbanization, infrastructural development, and increasing investments in renewable energy projects further solidify the region's market leadership. The competitive landscape within APAC is vibrant, with both global players and strong regional manufacturers vying for market share.

North America and Europe also represent significant markets, characterized by advanced industrial economies and a strong emphasis on high-performance applications and sustainable solutions. In North America, the demand is largely propelled by the aerospace and defense sectors, specialized electronics, and the expanding automotive industry, particularly with the growth of electric vehicles that require advanced insulation and encapsulation materials. European markets are driven by stringent environmental regulations, fostering innovation in bio-based resins and highly efficient formulations, alongside steady demand from the electrical and power transmission sectors. Both regions prioritize technological innovation and high-quality standards, influencing product development and market trends globally.

Latin America, the Middle East, and Africa (MEA) are emerging regions that present long-term growth opportunities, albeit from a smaller base. Growth in these areas is often linked to increasing industrialization, infrastructure development, and foreign investments in manufacturing capabilities. Countries in Latin America are seeing growth in automotive and construction sectors, while MEA is experiencing development in energy infrastructure and diversifying economies that could gradually increase demand for specialized materials like cycloaliphatic epoxy resins. However, market penetration in these regions may be slower due to economic volatility, less developed industrial ecosystems, and varying regulatory environments, requiring tailored market entry strategies from global players.

- Asia Pacific (APAC): Dominant market due to extensive electronics manufacturing, increasing LED production, and significant investments in electrical infrastructure, particularly in China, Japan, South Korea, and Taiwan.

- North America: Strong demand from the aerospace & defense, specialized electronics, and automotive industries, coupled with a focus on advanced materials and technological innovation.

- Europe: Driven by stringent environmental regulations promoting sustainable resin development, robust electrical and power sectors, and demand from high-tech industries.

- Latin America: Emerging market with growth potential in automotive and construction sectors, supported by industrial expansion and foreign investments.

- Middle East and Africa (MEA): Gradually increasing demand driven by infrastructure development, energy sector investments, and industrial diversification efforts.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cycloaliphatic Epoxy Resin Market. These companies are actively involved in the production, distribution, and innovation of cycloaliphatic epoxy resins, driving market growth and shaping the competitive landscape through strategic initiatives and product development.

- BASF SE

- Dow Inc.

- Hexion Inc.

- Huntsman Corporation

- DIC Corporation

- DuPont de Nemours Inc.

- Sumitomo Chemical Co. Ltd.

- Mitsubishi Chemical Corporation

- Nippon Kayaku Co. Ltd.

- Aditya Birla Chemicals

- Emerald Performance Materials LLC

- Kukdo Chemical Co. Ltd.

- Olin Corporation

- Polynt-Reichhold Group

- Sinopec Group

- Asahi Kasei Corporation

- Daicel Corporation

- Kolon Industries Inc.

- Nan Ya Plastics Corporation

- Shin-Etsu Chemical Co. Ltd.

Frequently Asked Questions

What are cycloaliphatic epoxy resins primarily used for?

Cycloaliphatic epoxy resins are primarily used in high-performance applications such as electrical insulation, LED encapsulation, optical components, and durable coatings. Their superior properties like excellent dielectric strength, UV stability, and transparency make them ideal for sensitive electronic and outdoor electrical applications where reliability and longevity are crucial.

How is the market for these resins expected to grow by 2033?

The Cycloaliphatic Epoxy Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. It is estimated to reach USD 820 Million by the end of 2033, driven by increasing demand from electrical, electronics, and renewable energy sectors globally.

What key factors are driving the demand for cycloaliphatic epoxy resins?

Key drivers include the burgeoning electrical and electronics industries, particularly for insulation and component protection; the rapid growth of the LED lighting sector requiring high-transparency encapsulants; and the expansion of renewable energy infrastructure demanding robust outdoor electrical insulation materials.

Which regions are major contributors to the cycloaliphatic epoxy resin market?

The Asia Pacific region is the dominant and fastest-growing market, primarily due to its extensive electronics manufacturing base. North America and Europe are also significant contributors, driven by advanced industrial applications, R&D in high-performance materials, and focus on sustainable solutions.

What are the main challenges faced by the cycloaliphatic epoxy resin market?

The main challenges include the relatively high production cost compared to conventional resins, volatility in raw material prices, intense competition from alternative materials, and complex synthesis processes. Additionally, stringent environmental regulations and potential supply chain disruptions can impact market stability and growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted