Engineered Gearbox and Drive Market

Engineered Gearbox and Drive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701960 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Engineered Gearbox and Drive Market Size

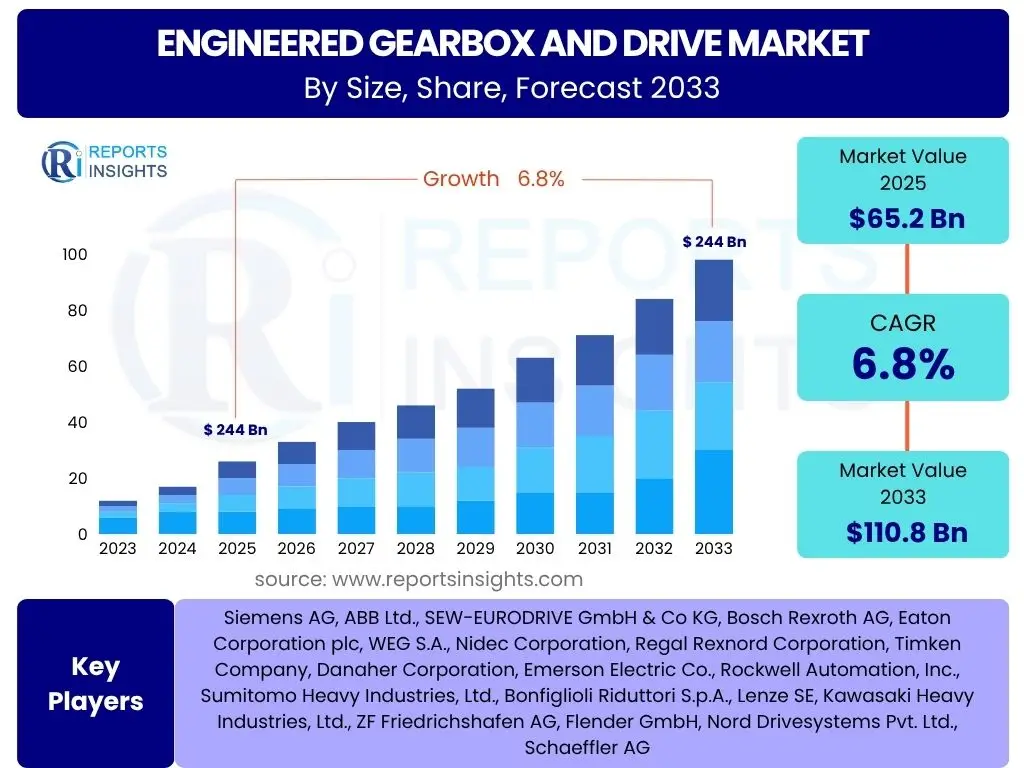

According to Reports Insights Consulting Pvt Ltd, The Engineered Gearbox and Drive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 65.2 Billion in 2025 and is projected to reach USD 110.8 Billion by the end of the forecast period in 2033.

Key Engineered Gearbox and Drive Market Trends & Insights

The Engineered Gearbox and Drive market is currently experiencing significant transformative trends driven by the escalating demand for industrial automation, energy efficiency, and the integration of advanced digital technologies. A predominant trend involves the increasing adoption of smart gearboxes and drives equipped with sensors and IoT capabilities, enabling predictive maintenance and remote monitoring. This shift is critical for optimizing operational uptime and reducing maintenance costs across various industrial sectors.

Furthermore, the market is witnessing a strong push towards customization and modularity to meet the diverse and evolving requirements of end-use industries, from heavy machinery to precision robotics. Manufacturers are focusing on developing compact, lightweight, and high-performance solutions that offer greater flexibility and easier integration into complex systems. The emphasis on sustainable solutions, including the design of more energy-efficient components and the use of eco-friendly materials, is also gaining traction, aligning with global environmental regulations and corporate sustainability goals.

Another crucial insight is the growing influence of electrification across different industries, particularly in the automotive and renewable energy sectors. This trend is driving the development of specialized gearboxes and drives optimized for electric powertrains and wind turbine applications, demanding higher power density, efficiency, and reliability. The convergence of mechanical engineering with advanced electronics and software is therefore reshaping product development and competitive strategies within the market.

- Shift towards smart and connected drive systems with IoT integration.

- Rising demand for energy-efficient and high-performance solutions.

- Increased focus on customized and modular gearbox and drive designs.

- Proliferation of electrification in industrial and mobility applications.

- Adoption of advanced materials for lightweight and durable components.

- Integration of predictive maintenance and condition monitoring capabilities.

- Emphasis on sustainability and reduced environmental footprint.

AI Impact Analysis on Engineered Gearbox and Drive

The integration of Artificial intelligence (AI) is set to profoundly transform the Engineered Gearbox and Drive market, moving beyond traditional mechanical functionalities to intelligent, self-optimizing systems. Users are increasingly concerned with how AI can enhance the reliability, efficiency, and longevity of these critical components. The primary expectation is that AI algorithms, particularly machine learning, will enable advanced predictive maintenance, allowing for the early detection of anomalies and potential failures in gearboxes and drives. This proactive approach aims to minimize downtime, reduce maintenance costs, and extend the operational lifespan of industrial machinery.

Beyond maintenance, AI's influence is anticipated in optimizing operational parameters and energy consumption. By analyzing vast amounts of real-time operational data—such as temperature, vibration, torque, and speed—AI can dynamically adjust drive settings to achieve optimal performance and energy efficiency under varying load conditions. This capability is highly sought after by industries aiming to reduce their carbon footprint and achieve significant energy savings. Furthermore, AI is expected to revolutionize design and manufacturing processes, enabling generative design for optimized gearbox geometries and automated quality control through computer vision.

The market also foresees AI playing a pivotal role in facilitating autonomous operations and enhancing human-machine collaboration within industrial environments. AI-powered drives can integrate seamlessly into broader automation systems, communicating with other smart components to orchestrate complex tasks with precision and efficiency. While the benefits are clear, user concerns revolve around data security, the complexity of AI implementation, and the need for specialized skills to manage and interpret AI-driven insights, underscoring the importance of user-friendly interfaces and robust cybersecurity measures in future AI-integrated solutions.

- Enhanced predictive maintenance and fault diagnosis through machine learning.

- Real-time operational optimization for energy efficiency and performance.

- AI-driven design and simulation for lighter, stronger components.

- Automated quality control and defect detection in manufacturing.

- Improved human-machine interface and autonomous system integration.

- Supply chain optimization and demand forecasting for components.

- Development of self-learning and adaptive drive control systems.

Key Takeaways Engineered Gearbox and Drive Market Size & Forecast

The Engineered Gearbox and Drive market is poised for robust growth, driven by an accelerating pace of industrial automation, global infrastructure development, and the increasing adoption of renewable energy sources. A key takeaway from the market size and forecast is the sustained demand across diverse end-use sectors, including manufacturing, material handling, and power generation, which are continually seeking more reliable and efficient power transmission solutions. The projected growth underscores the essential role these components play in the backbone of modern industrial operations, with significant investment continuing in technological advancements to meet evolving performance requirements.

Moreover, the forecast highlights a clear trend towards technologically advanced and integrated solutions. There is a strong emphasis on smart, connected, and energy-efficient systems that can seamlessly integrate into Industry 4.0 environments. This shift indicates that future market leadership will likely belong to companies that can offer comprehensive solutions combining mechanical excellence with digital capabilities, such as real-time monitoring, predictive analytics, and remote control. The premium placed on efficiency and sustainability is not merely a regulatory compliance issue but a fundamental driver of innovation and market competitiveness.

Finally, regional dynamics will play a crucial role in shaping market opportunities. Emerging economies in Asia Pacific and Latin America are expected to contribute significantly to market expansion due to rapid industrialization, urbanization, and government initiatives promoting manufacturing and renewable energy. Meanwhile, mature markets in North America and Europe will focus on replacement demand, technological upgrades, and the adoption of high-value, specialized solutions. Understanding these regional nuances is essential for market participants to tailor their strategies and capitalize on distinct growth pockets, ensuring a balanced and resilient market presence.

- Significant growth projected, driven by automation and industrial expansion.

- Strong demand across diverse end-use industries globally.

- Increasing adoption of smart, connected, and energy-efficient drive systems.

- Technological innovation is key to competitive advantage and market share.

- Asia Pacific and emerging economies are primary growth engines.

- Focus on predictive maintenance and operational optimization solutions.

- Sustainability and energy efficiency mandates influencing product development.

Engineered Gearbox and Drive Market Drivers Analysis

The Engineered Gearbox and Drive market is significantly propelled by the global surge in industrial automation and the widespread adoption of Industry 4.0 principles. Industries worldwide are investing heavily in automated machinery, robotics, and integrated manufacturing systems to enhance productivity, reduce labor costs, and improve operational safety. Gearboxes and drives are foundational components in these automated systems, providing the necessary power transmission and motion control for various applications, from assembly lines to material handling, thereby driving consistent demand for advanced and reliable solutions.

Another powerful driver is the growing focus on energy efficiency and sustainability across all sectors. Governments and industries are implementing stringent energy consumption regulations and sustainability targets, pushing manufacturers to develop and adopt more energy-efficient gearboxes and drives. High-efficiency components not only reduce operational costs but also contribute to a smaller carbon footprint, making them highly attractive to environmentally conscious businesses. This demand fuels innovation in design, materials, and control technologies aimed at minimizing energy losses and maximizing performance.

Furthermore, the rapid expansion of the renewable energy sector, particularly wind power generation, represents a substantial growth impetus. Wind turbines, both onshore and offshore, rely heavily on large, high-precision gearboxes to convert low-speed turbine rotation into high-speed generator input. As global investments in renewable energy infrastructure continue to escalate to meet climate goals, the demand for specialized, robust, and durable gearboxes designed for these demanding applications is experiencing a significant uptick. This specific vertical market segment contributes substantially to the overall market's expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation & Industry 4.0 Adoption | +1.5% | Global, particularly APAC, Europe, North America | 2025-2033 (Long-term) |

| Growing Demand for Energy-Efficient Solutions | +1.2% | Global, driven by regulatory mandates (EU, US) | 2025-2033 (Mid to Long-term) |

| Expansion of Renewable Energy Sector (Wind Power) | +1.0% | Europe, North America, China, India | 2025-2033 (Long-term) |

| Rise in Infrastructure Development & Construction Activities | +0.8% | Emerging Economies (APAC, Latin America, MEA) | 2025-2030 (Mid-term) |

| Technological Advancements in Material Science & Manufacturing | +0.7% | Global, focused on R&D hubs | 2025-2033 (Continuous) |

Engineered Gearbox and Drive Market Restraints Analysis

The Engineered Gearbox and Drive market faces significant restraints, primarily stemming from the high initial capital investment required for advanced systems. Precision-engineered gearboxes and sophisticated drive systems, especially those designed for high-performance, heavy-duty, or specialized applications, involve considerable upfront costs. This can be a deterrent for small and medium-sized enterprises (SMEs) or industries with limited capital budgets, leading them to opt for less advanced or refurbished equipment, thereby impacting market expansion and the adoption of cutting-edge technologies.

Another critical restraint is the volatility in raw material prices, particularly for metals such as steel, aluminum, and copper, which are essential components in gearbox and drive manufacturing. Fluctuations in commodity markets directly impact production costs, squeezing profit margins for manufacturers and potentially leading to price increases for end products. This unpredictability in material costs can hinder long-term planning, investment in R&D, and lead to supply chain instabilities, making it challenging for companies to maintain stable pricing strategies and competitive market positions.

Furthermore, the long replacement cycles characteristic of industrial machinery pose a significant challenge. Unlike consumer goods, industrial gearboxes and drives are built for durability and extended operational life, often spanning decades. This inherent longevity means that the market for new installations is limited, with a substantial portion of demand coming from replacement cycles or new project developments. This extended product lifespan limits the frequency of new purchases, slowing down market growth and making market penetration contingent on large-scale industrial expansions or significant technological obsolescence that necessitates upgrades.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.9% | Global, impacting SMEs & developing regions | 2025-2033 (Long-term) |

| Volatility in Raw Material Prices | -0.7% | Global, impacting manufacturing costs | 2025-2028 (Short to Mid-term) |

| Long Product Replacement Cycles | -0.6% | Mature Industrial Economies (Europe, North America) | 2025-2033 (Long-term) |

| Intense Competition from Local & Unorganized Players | -0.5% | Asia Pacific, Latin America | 2025-2033 (Continuous) |

| Economic Downturns & Geopolitical Instabilities | -0.4% | Global, varying by specific event | Event-dependent (Short to Mid-term) |

Engineered Gearbox and Drive Market Opportunities Analysis

Significant opportunities in the Engineered Gearbox and Drive market are emerging from the increasing global adoption of Industry 4.0 and smart manufacturing initiatives. As industries transition towards fully connected and intelligent factories, there is a growing demand for gearboxes and drives that are not only efficient but also capable of seamless integration with IoT platforms, cloud computing, and advanced analytics. This creates a fertile ground for manufacturers to innovate by embedding sensors, connectivity modules, and AI capabilities into their products, offering value-added services like predictive maintenance, remote diagnostics, and performance optimization, thereby opening up new revenue streams beyond traditional hardware sales.

The burgeoning demand for specialized and customized solutions across diverse industrial applications presents another lucrative opportunity. Standardized products may not always meet the unique requirements of emerging sectors such as robotics, aerospace, electric vehicles, and high-precision automation. This encourages manufacturers to invest in flexible production capabilities and advanced engineering expertise to deliver bespoke gearboxes and drives tailored to specific performance, size, and environmental parameters. Customization caters to niche markets with high-profit margins and fosters stronger client relationships by addressing specific operational challenges.

Furthermore, the vast untapped potential in emerging markets, particularly in Asia Pacific, Latin America, and the Middle East & Africa, offers substantial growth opportunities. These regions are undergoing rapid industrialization, urbanization, and infrastructure development, leading to increased investment in manufacturing, construction, and power generation sectors. As these economies expand and modernize their industrial base, the demand for reliable and efficient power transmission solutions will surge. Companies that can strategically establish distribution networks, offer competitive pricing, and provide localized support will be well-positioned to capture a significant share of these developing markets, driving overall market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Adoption of Smart Manufacturing & IoT Integration | +1.3% | Global, particularly developed markets | 2025-2033 (Long-term) |

| Growth in Customization & Niche Applications | +1.1% | Global, high-value industries | 2025-2033 (Continuous) |

| Untapped Potential in Emerging Economies | +1.0% | Asia Pacific, Latin America, MEA | 2025-2033 (Long-term) |

| Development of Lightweight & Compact Solutions | +0.9% | Global, particularly robotics, aerospace, EV sectors | 2025-2030 (Mid-term) |

| Aftermarket Services & Retrofit Opportunities | +0.8% | Mature Industrial Economies | 2025-2033 (Continuous) |

Engineered Gearbox and Drive Market Challenges Impact Analysis

The Engineered Gearbox and Drive market faces a significant challenge in the form of a persistent shortage of skilled labor and technical expertise. Modern gearboxes and drives are increasingly complex, incorporating advanced electronics, software, and precision mechanics. This complexity demands highly skilled engineers, technicians, and maintenance personnel for design, manufacturing, installation, and servicing. The lack of adequately trained professionals, particularly in developing regions, can impede market growth, lead to inefficiencies in production, and impact the effective deployment and maintenance of sophisticated systems, thereby increasing operational risks for end-users.

Supply chain disruptions represent another critical challenge for the market. The globalized nature of manufacturing means that components for gearboxes and drives often originate from various countries. Geopolitical tensions, trade disputes, natural disasters, and global health crises can severely disrupt the flow of raw materials, electronic components, and finished goods. Such disruptions lead to increased lead times, higher logistics costs, and production delays, directly impacting manufacturers' ability to meet demand and maintain competitive pricing, thereby creating instability within the market.

Furthermore, the rapid pace of technological obsolescence poses a continuous challenge. As innovations in material science, additive manufacturing, AI, and IoT continue to advance, older models of gearboxes and drives quickly become less efficient or incompatible with new industrial standards. This forces manufacturers to constantly invest in research and development to remain competitive, but also creates pressure on end-users to upgrade their machinery more frequently, which can be a significant capital expenditure. Managing this balance between innovation and economic viability, while ensuring compatibility and long-term support for legacy systems, is a complex task for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled Labor & Technical Expertise | -0.8% | Global, impacting industrial productivity | 2025-2033 (Long-term) |

| Supply Chain Disruptions & Volatility | -0.7% | Global, impacting manufacturing & delivery | 2025-2028 (Short to Mid-term) |

| Rapid Technological Obsolescence | -0.6% | Developed Markets, high-tech sectors | 2025-2033 (Continuous) |

| Increasing Cybersecurity Risks in Connected Systems | -0.5% | Global, particularly critical infrastructure | 2025-2033 (Emerging) |

| Compliance with Evolving Environmental Regulations | -0.4% | Europe, North America, requiring R&D investment | 2025-2030 (Mid-term) |

Engineered Gearbox and Drive Market - Updated Report Scope

This report provides a comprehensive analysis of the global Engineered Gearbox and Drive market, delving into market size estimations, growth forecasts, key trends, and a detailed examination of market drivers, restraints, opportunities, and challenges. It segments the market by product type, end-use industry, application, and torque range, offering regional insights across major geographies. The scope includes an in-depth competitive landscape, profiling leading companies and their strategic initiatives, alongside an impact assessment of AI integration and sustainability factors shaping the industry's future trajectory. The report serves as an essential resource for stakeholders seeking strategic insights into market dynamics and growth prospects.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.2 Billion |

| Market Forecast in 2033 | USD 110.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, ABB Ltd., SEW-EURODRIVE GmbH & Co KG, Bosch Rexroth AG, Eaton Corporation plc, WEG S.A., Nidec Corporation, Regal Rexnord Corporation, Timken Company, Danaher Corporation, Emerson Electric Co., Rockwell Automation, Inc., Sumitomo Heavy Industries, Ltd., Bonfiglioli Riduttori S.p.A., Lenze SE, Kawasaki Heavy Industries, Ltd., ZF Friedrichshafen AG, Flender GmbH, Nord Drivesystems Pvt. Ltd., Schaeffler AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Engineered Gearbox and Drive market is meticulously segmented to provide a granular understanding of its diverse components and their respective market dynamics. This segmentation facilitates in-depth analysis of specific product types, their applications across various industries, and their performance characteristics based on torque ranges. Understanding these segments is crucial for manufacturers to tailor their product offerings, for end-users to select appropriate solutions, and for investors to identify high-growth areas within the broader market. Each segment responds differently to market drivers, restraints, opportunities, and technological advancements, necessitating a segmented approach for strategic decision-making.

- By Product Type:

- Gearboxes: Comprising Planetary, Helical, Worm, Bevel, Spur, Hypoid, and Harmonic gearboxes, each designed for specific power transmission and motion control requirements across various industrial applications, from high-torque to high-precision uses.

- Drives: Including Variable Frequency Drives (VFDs), Servo Drives, DC Drives, and AC Drives, which control the speed and torque of electric motors, enhancing energy efficiency and process control in machinery.

- By End-Use Industry:

- Industrial: Encompasses a wide range of sub-sectors such as Manufacturing, Material Handling, Food & Beverage, Automotive, Mining, and Construction, representing significant demand for robust and reliable gearbox and drive systems.

- Power Generation: Primarily driven by the burgeoning Wind Power sector, alongside Hydro Power and Thermal Power plants, requiring specialized high-capacity and durable gearboxes and drives.

- Agriculture: For machinery used in farming, irrigation, and harvesting.

- Marine: Applications in shipbuilding, propulsion systems, and offshore equipment.

- Defense: Critical for military vehicles, naval vessels, and specialized equipment.

- Healthcare: Used in medical devices, diagnostic equipment, and rehabilitation robotics.

- By Application:

- Conveyors: For material transport systems in various industries.

- Pumps: Essential for fluid transfer in industrial and municipal applications.

- Fans: For ventilation and air circulation systems.

- Compressors: Used in industrial processes requiring compressed air or gases.

- Extruders: For plastic, food, and other material processing.

- Mixers: For blending and agitation in diverse manufacturing processes.

- Robotics: Precision motion control in industrial and collaborative robots.

- By Torque Range:

- Low Torque: Typically for smaller machines and precision instruments.

- Medium Torque: Common in general industrial machinery and automation.

- High Torque: Essential for heavy machinery, mining equipment, and wind turbines.

Regional Highlights

Regional dynamics play a pivotal role in shaping the demand and supply landscape of the Engineered Gearbox and Drive market. Each region presents a unique set of opportunities and challenges influenced by industrialization rates, government policies, technological adoption, and economic development. Understanding these regional variations is crucial for manufacturers to tailor their market strategies, optimize supply chains, and invest in localized production or distribution capabilities to effectively penetrate specific markets.

North America and Europe represent mature markets characterized by high adoption of advanced automation, Industry 4.0 initiatives, and a strong emphasis on energy efficiency and predictive maintenance. While new installations are driven by technological upgrades and modernization of existing infrastructure, the demand for high-performance, precision, and customized solutions remains strong. These regions are also at the forefront of renewable energy adoption, particularly wind power, driving demand for specialized heavy-duty gearboxes and drives.

Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by rapid industrialization, burgeoning manufacturing sectors, significant infrastructure development, and increasing investments in automation and renewable energy, especially in China, India, Japan, and South Korea. This region offers immense potential for market expansion, with a growing number of new industrial projects and a rising demand for both standard and technologically advanced gearbox and drive solutions. Latin America and the Middle East & Africa (MEA) are also emerging as significant markets, driven by mining activities, oil and gas, and developing manufacturing bases, indicating diverse growth opportunities across the global landscape.

- North America: Strong emphasis on automation, smart manufacturing, and replacement demand; significant investment in renewable energy.

- Europe: Leading in energy efficiency regulations, Industry 4.0 adoption, and advanced industrial machinery; substantial market for high-precision components.

- Asia Pacific (APAC): Fastest-growing market due to rapid industrialization, infrastructure development, and expanding manufacturing base, especially in China and India.

- Latin America: Growth driven by mining, agriculture, and increasing industrial investments, with a rising demand for robust solutions.

- Middle East and Africa (MEA): Emerging market driven by oil & gas, construction, and diversification of economies; increasing adoption of industrial solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Engineered Gearbox and Drive Market.- Siemens AG

- ABB Ltd.

- SEW-EURODRIVE GmbH & Co KG

- Bosch Rexroth AG

- Eaton Corporation plc

- WEG S.A.

- Nidec Corporation

- Regal Rexnord Corporation

- Timken Company

- Danaher Corporation

- Emerson Electric Co.

- Rockwell Automation, Inc.

- Sumitomo Heavy Industries, Ltd.

- Bonfiglioli Riduttori S.p.A.

- Lenze SE

- Kawasaki Heavy Industries, Ltd.

- ZF Friedrichshafen AG

- Flender GmbH

- Nord Drivesystems Pvt. Ltd.

- Schaeffler AG

Frequently Asked Questions

What is an engineered gearbox and drive?

An engineered gearbox is a mechanical system designed to transmit and modify torque and speed from a prime mover to an output device, often for specific industrial applications requiring precise control or significant power changes. An engineered drive, typically an electric drive (like a Variable Frequency Drive or Servo Drive), controls the speed, torque, and direction of electric motors, optimizing performance and energy consumption within a mechanical system. Together, they form critical power transmission and motion control solutions in industrial machinery.

What are the primary drivers of the Engineered Gearbox and Drive market growth?

The primary drivers include the accelerating global trend towards industrial automation and Industry 4.0 adoption, increasing demand for energy-efficient solutions to reduce operational costs and carbon footprint, and the rapid expansion of the renewable energy sector, particularly wind power, which relies heavily on specialized high-capacity gearboxes.

How is Artificial Intelligence (AI) impacting the Engineered Gearbox and Drive market?

AI is transforming the market by enabling advanced predictive maintenance through real-time data analysis, optimizing operational parameters for enhanced energy efficiency, and improving design and manufacturing processes through generative design and automated quality control. It also facilitates smarter integration into autonomous industrial systems.

Which end-use industries are major consumers of engineered gearboxes and drives?

Major end-use industries include general industrial sectors (manufacturing, material handling, automotive, mining, construction), power generation (especially wind turbines), agriculture, marine, and defense. These sectors rely on engineered gearboxes and drives for efficient power transmission and precise motion control in their machinery and equipment.

What are the key challenges facing the Engineered Gearbox and Drive market?

Key challenges include the high initial capital investment required for advanced systems, volatility in raw material prices, long product replacement cycles that limit new sales, and a persistent shortage of skilled labor and technical expertise needed for complex system design, installation, and maintenance. Supply chain disruptions and rapid technological obsolescence also pose significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted