Endpoint Detection and Response Solution Market

Endpoint Detection and Response Solution Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706659 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

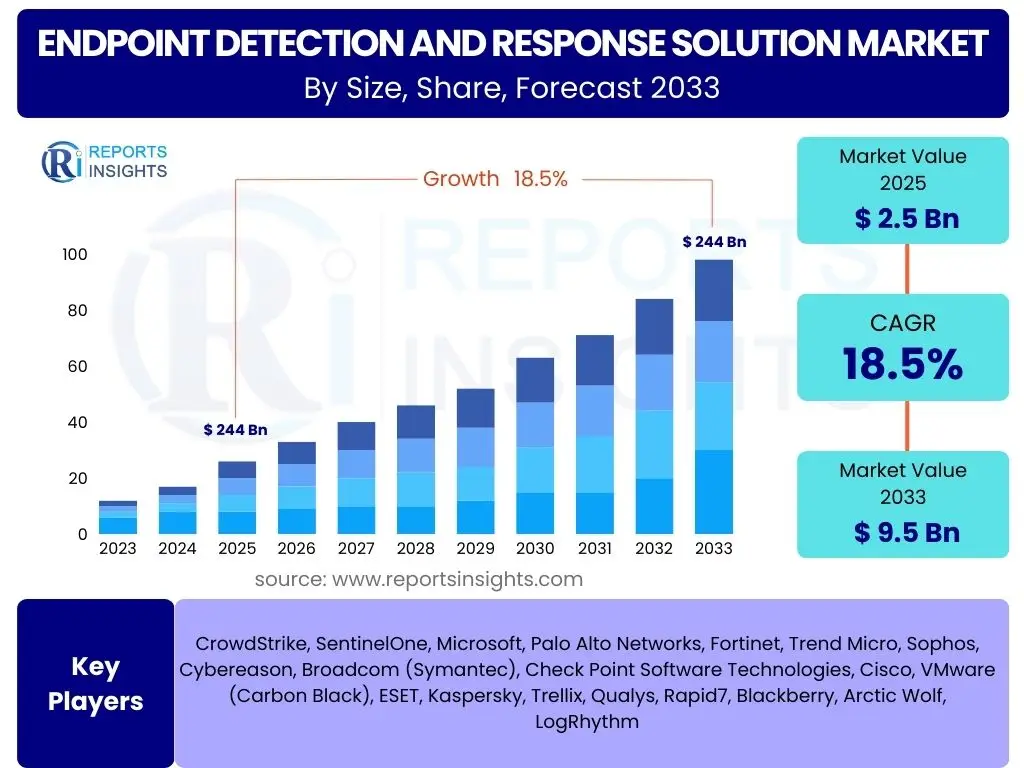

Endpoint Detection and Response Solution Market Size

According to Reports Insights Consulting Pvt Ltd, The Endpoint Detection and Response Solution Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 9.5 Billion by the end of the forecast period in 2033. This significant growth is primarily driven by the escalating sophistication of cyber threats, the increasing adoption of cloud-based solutions, and the critical need for robust security measures across diverse industries. Enterprises globally are recognizing EDR as an indispensable tool for proactive threat hunting and rapid incident response, moving beyond traditional perimeter defenses.

Key Endpoint Detection and Response Solution Market Trends & Insights

The Endpoint Detection and Response (EDR) market is characterized by several dynamic trends reflecting the evolving cybersecurity landscape and advancements in threat detection technologies. A prominent trend is the shift towards cloud-native EDR solutions, offering scalability, flexibility, and reduced infrastructure overhead for organizations of all sizes. This transition facilitates easier deployment and management, alongside providing real-time visibility across distributed environments, which is crucial for modern, remote-first workforces.

Another significant insight is the increasing integration of EDR capabilities within broader Extended Detection and Response (XDR) platforms. This convergence aims to provide a unified security posture by correlating data from endpoints, networks, cloud environments, and applications, offering a more holistic view of threats and enabling coordinated responses. Furthermore, the market is witnessing a surge in the adoption of AI and machine learning for enhanced threat detection, anomaly identification, and automation of response actions, drastically improving the speed and accuracy of cybersecurity operations. The demand for managed EDR (MEDR) services is also on the rise, particularly among small and medium-sized enterprises (SMEs) that may lack the internal resources or expertise to effectively manage complex EDR deployments themselves. This trend allows businesses to leverage expert security operations center (SOC) capabilities without the substantial upfront investment.

- Cloud-native EDR adoption is accelerating for scalability and flexibility.

- Integration with Extended Detection and Response (XDR) platforms for unified security visibility.

- Increased application of Artificial Intelligence (AI) and Machine Learning (ML) for advanced threat detection and automation.

- Growing demand for Managed EDR (MEDR) services among resource-constrained organizations.

- Shift towards proactive threat hunting capabilities to identify emerging threats before they cause significant damage.

AI Impact Analysis on Endpoint Detection and Response Solution

Artificial Intelligence (AI) and Machine Learning (ML) are profoundly transforming the Endpoint Detection and Response (EDR) landscape by enhancing the speed, accuracy, and automation of threat detection and response processes. Users frequently inquire about how AI improves threat identification, reduces false positives, and enables more sophisticated behavioral analysis. AI algorithms are crucial for analyzing vast datasets of endpoint telemetry, identifying subtle patterns indicative of malicious activity that might evade traditional signature-based detection methods. This includes behavioral anomaly detection, which can flag unusual user or process activities, even for zero-day threats.

The application of AI in EDR extends beyond mere detection to predictive threat intelligence and automated remediation. AI-driven EDR solutions can learn from past incidents and evolving threat patterns to anticipate future attacks, proactively fortifying defenses. Furthermore, AI facilitates automated incident response by quickly isolating compromised endpoints, containing outbreaks, and initiating remediation steps without human intervention, thereby significantly reducing the mean time to detect (MTTD) and mean time to respond (MTTR). While AI brings immense benefits in terms of efficiency and effectiveness, user concerns sometimes revolve around the explainability of AI decisions, the potential for adversarial AI attacks, and the need for high-quality data to train robust models. However, the overarching expectation is that AI will continue to be a cornerstone of next-generation EDR, making security operations more intelligent, adaptive, and resilient against sophisticated cyber adversaries.

- Enhanced behavioral anomaly detection to identify unknown threats.

- Reduced false positives through intelligent filtering and correlation.

- Automated threat hunting and incident response capabilities.

- Predictive threat intelligence for proactive defense strategies.

- Improved analysis of large volumes of endpoint data for faster insights.

Key Takeaways Endpoint Detection and Response Solution Market Size & Forecast

The Endpoint Detection and Response (EDR) solution market is poised for substantial expansion, reflecting a critical shift in organizational cybersecurity strategies from prevention-only to a more proactive, detect-and-respond paradigm. Common user questions highlight the importance of understanding the core reasons behind this growth and the strategic implications for businesses and security vendors. A primary takeaway is the non-negotiable imperative for robust endpoint security in an era of escalating and increasingly sophisticated cyberattacks, including ransomware, advanced persistent threats (APTs), and fileless malware. The forecast indicates that EDR is no longer a niche solution but a fundamental component of enterprise security architectures, irrespective of industry or size.

Another crucial insight is the dynamic nature of the market, driven by continuous innovation in threat detection technologies, particularly the integration of Artificial Intelligence, Machine Learning, and behavioral analytics. This evolution empowers EDR solutions to provide deep visibility into endpoint activities, enabling rapid identification and containment of threats before they can propagate across networks. Furthermore, the market's robust Compound Annual Growth Rate (CAGR) underscores the significant investment and adoption across various end-user industries, from finance and healthcare to IT and government, all seeking to bolster their defenses against pervasive digital risks. Stakeholders should note the growing importance of cloud-native and managed EDR offerings, which are democratizing access to advanced endpoint security for organizations with varying levels of internal cybersecurity expertise and resources, thereby broadening the market's reach and growth trajectory.

- The EDR market is experiencing robust growth driven by the escalating sophistication of cyber threats.

- Increased enterprise adoption across all sectors highlights EDR as a foundational security layer.

- Innovation, particularly in AI and behavioral analytics, is a key enabler of market expansion.

- Cloud-native and Managed EDR (MEDR) solutions are democratizing access to advanced endpoint security.

- Proactive threat hunting and rapid incident response are becoming critical capabilities for business continuity.

Endpoint Detection and Response Solution Market Drivers Analysis

The Endpoint Detection and Response (EDR) solution market is propelled by a convergence of critical factors, primarily the dramatic rise in the volume and sophistication of cyberattacks globally. Organizations face a relentless barrage of ransomware, zero-day exploits, fileless malware, and advanced persistent threats (APTs), which traditional antivirus solutions often fail to detect. This escalating threat landscape necessitates advanced tools that can provide deep visibility into endpoint activities, enabling real-time detection and rapid response to complex attacks. The shift towards remote and hybrid work models has further expanded the attack surface, with endpoints becoming the primary gateway for attackers, thereby increasing the urgency for comprehensive EDR deployments across distributed work environments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Sophistication of Cyberattacks | +5.0% | Global | Short to Long-term |

| Rising Adoption of Remote and Hybrid Work Models | +4.5% | North America, Europe, APAC | Short to Mid-term |

| Stringent Regulatory Compliance Requirements | +3.8% | North America, Europe (GDPR), Asia Pacific | Mid-term |

| Growth in Cloud-based Deployments and Digital Transformation | +4.2% | Global | Mid to Long-term |

| Limitations of Traditional Antivirus Solutions | +3.5% | Global | Short to Mid-term |

Endpoint Detection and Response Solution Market Restraints Analysis

Despite its significant growth trajectory, the Endpoint Detection and Response (EDR) solution market faces several notable restraints that could temper its expansion. One primary impediment is the high cost associated with the initial deployment and ongoing management of advanced EDR solutions. This includes not only the licensing fees for sophisticated software but also the substantial investment in hardware, infrastructure, and the highly skilled personnel required to operate and interpret the complex insights generated by EDR platforms. Small and Medium-sized Enterprises (SMEs), in particular, often struggle with these financial and resource burdens, which can deter adoption even when recognizing the critical security benefits.

Another significant restraint is the complexity involved in integrating EDR solutions with existing security infrastructure and legacy systems. Many organizations operate diverse IT environments, and ensuring seamless interoperability between EDR, Security Information and Event Management (SIEM), Security Orchestration, Automation, and Response (SOAR), and other security tools can be a challenging and time-consuming process. This complexity can lead to deployment delays, operational inefficiencies, and a fragmented security posture, reducing the overall effectiveness of the EDR investment. Furthermore, the global shortage of cybersecurity professionals capable of effectively managing and leveraging EDR capabilities poses a considerable barrier. Organizations frequently lack the in-house expertise for threat hunting, incident analysis, and remediation, necessitating reliance on managed security service providers (MSSPs) or extensive training programs, both of which add to the cost and complexity of EDR adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Implementation and Maintenance | -3.0% | Global, particularly SMEs | Short to Mid-term |

| Complexity of Integration with Existing Security Infrastructure | -2.5% | Global | Mid-term |

| Shortage of Skilled Cybersecurity Professionals | -2.8% | Global | Long-term |

| Alert Fatigue and False Positives | -2.0% | Global | Short to Mid-term |

| Data Privacy and Compliance Concerns | -1.5% | Europe, North America | Mid-term |

Endpoint Detection and Response Solution Market Opportunities Analysis

The Endpoint Detection and Response (EDR) solution market is rife with significant opportunities driven by the continuous evolution of cybersecurity threats and technological advancements. One primary opportunity lies in the burgeoning demand for cloud-native EDR solutions, which offer unparalleled scalability, accessibility, and ease of management compared to on-premise deployments. This shift aligns with the broader enterprise trend towards cloud adoption and digital transformation, creating a fertile ground for solutions that seamlessly integrate with cloud environments and distributed workforces. Providers focusing on robust multi-cloud and hybrid cloud EDR capabilities are well-positioned to capitalize on this expanding need, offering flexibility and streamlined operations to a diverse customer base.

Another compelling opportunity emerges from the growing demand for Managed EDR (MEDR) services. Many organizations, especially Small and Medium-sized Enterprises (SMEs), lack the specialized cybersecurity talent and dedicated security operations centers (SOCs) required to effectively implement and manage complex EDR platforms internally. This creates a substantial market for third-party providers offering MEDR, where expert teams provide 24/7 monitoring, threat hunting, incident response, and forensic analysis on behalf of clients. Furthermore, the increasing convergence of EDR with other security technologies, such as network detection and response (NDR) and cloud workload protection platforms (CWPP), into unified Extended Detection and Response (XDR) platforms presents a significant growth avenue. XDR promises a more holistic and automated approach to security, allowing vendors to expand their offerings and provide comprehensive security suites that address the entire attack surface, thereby creating new revenue streams and fostering deeper customer relationships.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Managed EDR (MEDR) Services | +4.0% | Global, particularly SMEs | Short to Mid-term |

| Growing Adoption of Cloud-Native EDR Solutions | +3.5% | Global | Mid to Long-term |

| Convergence with Extended Detection and Response (XDR) | +3.8% | North America, Europe, APAC | Mid to Long-term |

| Increasing Focus on IoT and OT Security | +3.0% | Manufacturing, Critical Infrastructure | Long-term |

| Untapped Market in Emerging Economies | +2.5% | Asia Pacific, Latin America, MEA | Mid to Long-term |

Endpoint Detection and Response Solution Market Challenges Impact Analysis

The Endpoint Detection and Response (EDR) solution market faces several significant challenges that could impede its growth and widespread adoption. A primary challenge is the constantly evolving and increasingly sophisticated nature of the cyber threat landscape. Threat actors are continually developing new evasion techniques, leveraging polymorphic malware, fileless attacks, and advanced social engineering tactics, making it difficult for even the most advanced EDR solutions to provide absolute protection. This perpetual arms race necessitates continuous innovation and updates from EDR vendors, placing considerable pressure on research and development budgets and requiring rapid deployment of new countermeasures to remain effective against emerging threats.

Another significant challenge stems from the overwhelming volume of security alerts and data generated by EDR solutions, often leading to what is known as "alert fatigue" among security analysts. While EDR platforms provide deep visibility, filtering through a deluge of alerts to identify genuine threats from false positives requires substantial human expertise and time, potentially delaying critical response actions. This issue is exacerbated by the existing shortage of skilled cybersecurity professionals globally, making it difficult for organizations to staff security operations centers capable of effectively managing and responding to EDR insights. Furthermore, ensuring seamless interoperability and integration of EDR solutions with diverse existing IT infrastructure and a multitude of other security tools within an organization's ecosystem can be technically complex and resource-intensive, often leading to deployment hurdles and suboptimal performance. Addressing these challenges requires not only technological advancements in automation and AI-driven insights but also strategic investments in talent development and robust integration frameworks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving and Sophisticated Threat Landscape | -3.5% | Global | Ongoing |

| Alert Fatigue and Management of False Positives | -2.8% | Global | Short to Mid-term |

| Integration with Disparate IT Environments | -2.3% | Global | Mid-term |

| Data Privacy and Compliance Complexities | -2.0% | Europe, North America, APAC | Ongoing |

| High Cost of Talent Acquisition and Retention | -1.8% | Global | Long-term |

Endpoint Detection and Response Solution Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Endpoint Detection and Response (EDR) Solution Market, offering critical insights into its current size, historical performance, and future growth projections. It meticulously examines key market trends, significant drivers, formidable restraints, and promising opportunities that shape the industry landscape. The report also includes a detailed assessment of the impact of Artificial Intelligence on EDR solutions, exploring its transformative role in enhancing threat detection and response capabilities. Furthermore, it offers extensive segmentation analysis by component, deployment model, organization size, and end-user industry, along with a thorough regional overview to highlight market dynamics across major geographies. A competitive landscape analysis featuring profiles of top key players is also included to provide a holistic view of the market ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 9.5 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CrowdStrike, SentinelOne, Microsoft, Palo Alto Networks, Fortinet, Trend Micro, Sophos, Cybereason, Broadcom (Symantec), Check Point Software Technologies, Cisco, VMware (Carbon Black), ESET, Kaspersky, Trellix, Qualys, Rapid7, Blackberry, Arctic Wolf, LogRhythm |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Endpoint Detection and Response (EDR) solution market is segmented across several critical dimensions, providing a granular understanding of its various facets and growth opportunities. These segmentations allow for a detailed analysis of market dynamics concerning specific technologies, deployment preferences, organizational requirements, and industry-specific applications. Understanding these segments is crucial for stakeholders to identify key growth areas, tailor solutions to specific customer needs, and develop effective market entry and expansion strategies. The market is broadly categorized by the components that constitute an EDR solution, the different deployment models available, the size of organizations adopting these solutions, and the diverse end-user industries leveraging EDR for enhanced security posture.

The segmentation by component differentiates between the core EDR software solutions, which encompass functionalities like endpoint telemetry collection, behavioral analysis, threat intelligence integration, incident response, and forensic capabilities, and the essential services that support these solutions, including professional services for deployment and customization, and managed services for ongoing security operations. Deployment models distinguish between traditional on-premise installations, increasingly popular cloud-based solutions offering scalability and flexibility, and hybrid approaches that combine both. Furthermore, the market is analyzed based on organization size, recognizing the distinct security needs and resource availability of small and medium-sized enterprises (SMEs) versus large enterprises. Lastly, the end-user segmentation provides insights into the adoption patterns and specific security challenges faced by sectors such as BFSI, IT and Telecommunications, Healthcare, Government, Retail, Manufacturing, and Energy and Utilities, enabling a targeted approach to market penetration.

- By Component: Solutions (Endpoint Telemetry, Behavioral Analysis, Threat Intelligence, Incident Response, Forensics), Services (Professional Services, Managed Services)

- By Deployment Model: On-premise, Cloud-based, Hybrid

- By Organization Size: Small and Medium-sized Enterprises (SMEs), Large Enterprises

- By End-user: BFSI (Banking, Financial Services, and Insurance), IT and Telecommunications, Healthcare, Government and Public Sector, Retail, Manufacturing, Energy and Utilities, Others

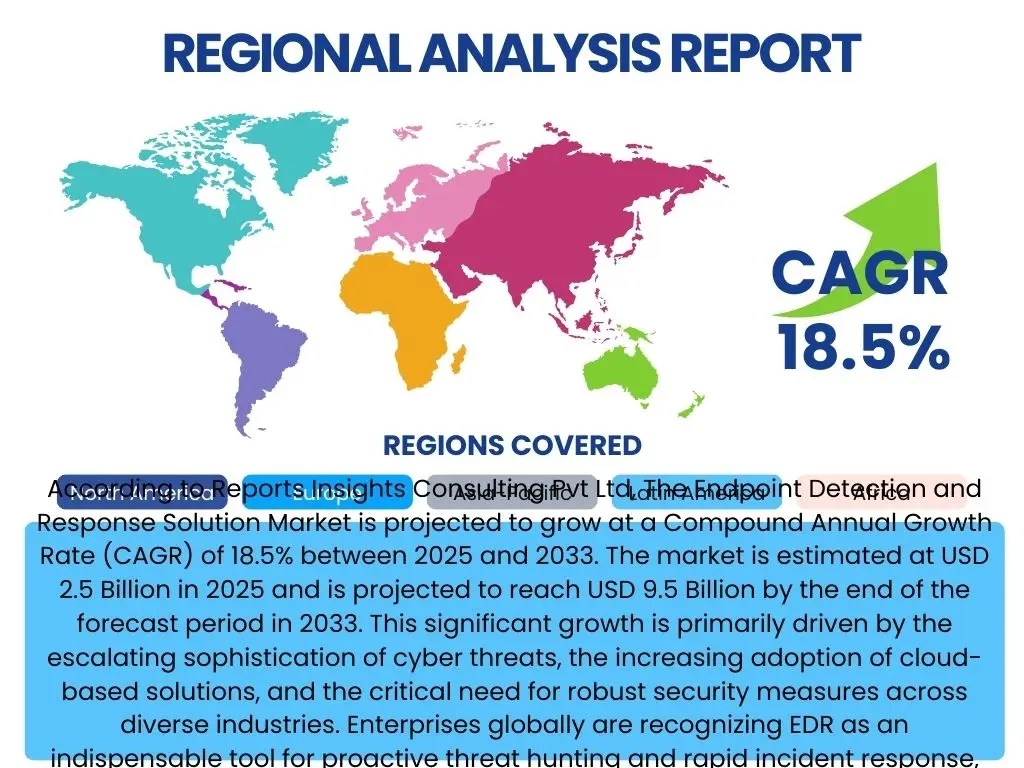

Regional Highlights

- North America: Dominates the EDR market due to early adoption of advanced security technologies, presence of major EDR vendors, and a high incidence of sophisticated cyberattacks. Stringent regulatory frameworks and a robust cybersecurity infrastructure further drive market growth.

- Europe: Exhibits significant growth propelled by increasing awareness of cybersecurity threats, the enforcement of data protection regulations like GDPR, and a growing emphasis on digital transformation across industries. Countries like the UK, Germany, and France are key contributors.

- Asia Pacific (APAC): Emerges as the fastest-growing region, driven by rapid digital transformation initiatives, increasing cloud adoption, and a rising number of cyber incidents in countries such as China, India, Japan, and Australia. Government investments in cybersecurity infrastructure and increasing SME adoption are key factors.

- Latin America: Shows steady growth, fueled by rising internet penetration, growing digital economies, and increasing awareness of cyber risks among enterprises. Brazil and Mexico are leading the adoption of EDR solutions in the region.

- Middle East and Africa (MEA): Experiences nascent but accelerating growth, primarily influenced by governmental efforts to enhance cybersecurity, investments in critical infrastructure protection, and the expansion of IT services. Countries like UAE and Saudi Arabia are at the forefront of adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Endpoint Detection and Response Solution Market.- CrowdStrike

- SentinelOne

- Microsoft

- Palo Alto Networks

- Fortinet

- Trend Micro

- Sophos

- Cybereason

- Broadcom (Symantec)

- Check Point Software Technologies

- Cisco

- VMware (Carbon Black)

- ESET

- Kaspersky

- Trellix

- Qualys

- Rapid7

- Blackberry

- Arctic Wolf

- LogRhythm

Frequently Asked Questions

What is Endpoint Detection and Response (EDR)?

Endpoint Detection and Response (EDR) is a cybersecurity solution that continuously monitors and records all activities on endpoints, such as laptops, servers, and mobile devices. It collects detailed data, analyzes it for suspicious behaviors, and provides security teams with the tools to detect, investigate, and respond to cyber threats in real time, going beyond traditional antivirus capabilities to offer deep visibility and forensic analysis.

How is EDR different from traditional antivirus software?

Traditional antivirus primarily focuses on preventing known malware infections through signature-based detection. EDR, conversely, offers a more proactive and comprehensive approach by continuously monitoring endpoint activity for unknown threats, abnormal behaviors, and advanced attacks that might bypass antivirus. It provides advanced detection, investigation tools, and rapid response capabilities, allowing organizations to detect and contain threats that have already breached initial defenses.

What are the primary benefits of implementing an EDR solution?

Implementing an EDR solution offers several key benefits, including enhanced visibility into endpoint activities, superior detection of advanced persistent threats (APTs), ransomware, and fileless attacks, and improved incident response times. It facilitates proactive threat hunting, reduces the impact of breaches through rapid containment, and provides valuable forensic data for post-incident analysis and continuous security improvement.

What factors should be considered when choosing an EDR solution?

Key factors to consider include the solution's detection capabilities (e.g., AI/ML-driven behavioral analysis), ease of deployment and management, scalability for current and future needs, integration capabilities with existing security tools (like SIEM/SOAR), availability of managed services if internal resources are limited, and the vendor's reputation for threat intelligence and support. Cost-effectiveness and user interface intuitiveness are also important considerations.

How does Artificial Intelligence (AI) enhance EDR capabilities?

AI significantly enhances EDR by enabling advanced behavioral anomaly detection, which identifies malicious activities even without prior knowledge of signatures, drastically reducing false positives. AI algorithms process vast amounts of endpoint data to predict potential threats, automate threat hunting, and orchestrate rapid, automated responses, thereby improving the efficiency and effectiveness of security operations and minimizing manual intervention.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted