Feed Water Heater for Power Plant Market

Feed Water Heater for Power Plant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702826 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Feed Water Heater for Power Plant Market Size

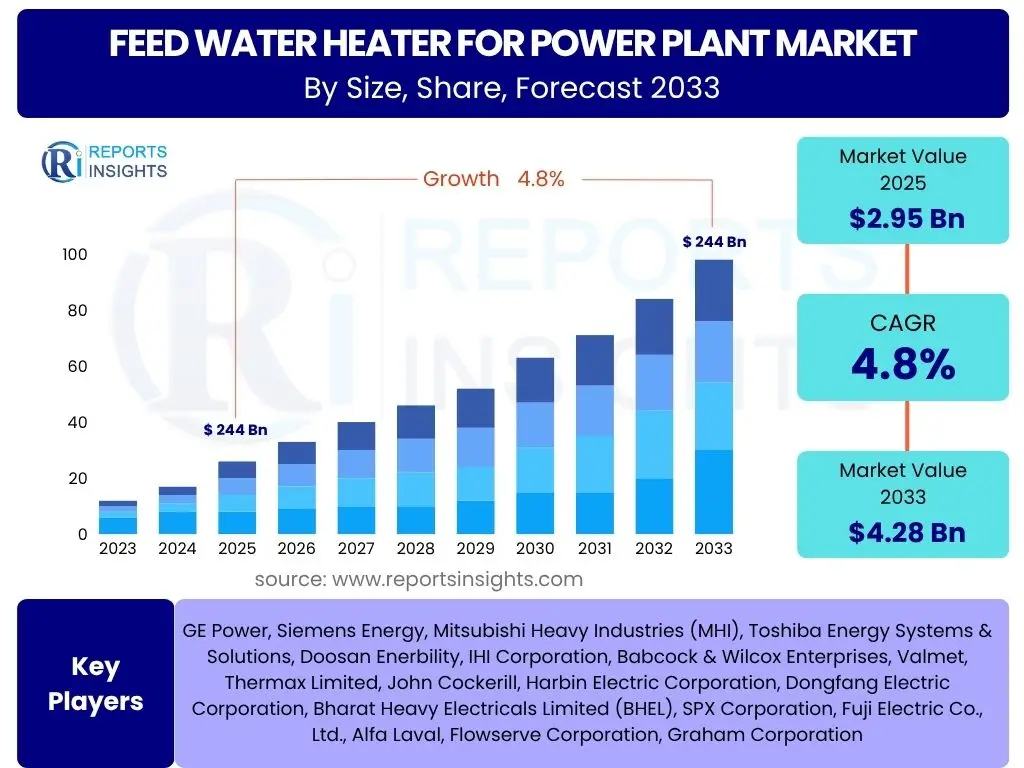

According to Reports Insights Consulting Pvt Ltd, The Feed Water Heater for Power Plant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 2.95 Billion in 2025 and is projected to reach USD 4.28 Billion by the end of the forecast period in 2033.

Key Feed Water Heater for Power Plant Market Trends & Insights

The Feed Water Heater for Power Plant market is currently experiencing significant shifts driven by evolving energy landscapes and technological advancements. A primary trend involves the increasing emphasis on energy efficiency and operational optimization within existing power infrastructure. This includes the adoption of advanced materials and design techniques aimed at enhancing heat transfer efficiency and reducing maintenance requirements, directly impacting the longevity and performance of power plants.

Furthermore, the market is observing a growing demand for customized and modular feed water heater solutions. This trend caters to the diverse needs of various power generation technologies, from conventional thermal plants to burgeoning combined cycle and industrial co-generation facilities. Digitalization and the integration of smart monitoring systems are also becoming prevalent, allowing for real-time performance tracking and predictive maintenance, thereby reducing downtime and extending equipment lifespan.

- Emphasis on high-efficiency designs and advanced materials for improved heat transfer.

- Increased integration of smart monitoring and predictive maintenance technologies.

- Growing demand for modular and customized feed water heater solutions.

- Focus on retrofitting existing power plants to enhance their operational efficiency.

- Shift towards advanced manufacturing techniques for higher durability and performance.

AI Impact Analysis on Feed Water Heater for Power Plant

Artificial intelligence (AI) is poised to significantly transform the Feed Water Heater for Power Plant market by introducing unprecedented levels of operational intelligence and automation. Users are particularly interested in how AI can optimize the performance of these critical components, moving beyond traditional reactive maintenance to predictive and prescriptive approaches. AI algorithms, leveraging vast datasets from sensors and operational history, can accurately forecast potential failures, identify inefficiencies, and recommend optimal operational parameters, leading to substantial reductions in unplanned downtime and operational costs.

The application of AI extends to enhancing the design and manufacturing processes of feed water heaters. Generative design AI can explore thousands of design iterations to create more efficient and robust components, while AI-driven quality control systems can improve manufacturing precision. Furthermore, AI contributes to better energy management within power plants by optimizing the heat exchange processes, leading to improved overall thermal efficiency and reduced fuel consumption. This intelligent integration promises to extend the operational life of assets and ensure peak performance under varying load conditions, addressing critical industry needs for reliability and sustainability.

- Predictive maintenance and anomaly detection for feed water heater systems.

- Optimization of operational parameters to maximize heat transfer efficiency.

- AI-driven design and simulation for enhanced component performance and durability.

- Automated fault diagnosis and root cause analysis for faster issue resolution.

- Improved energy management and thermal efficiency through real-time data analysis.

Key Takeaways Feed Water Heater for Power Plant Market Size & Forecast

The Feed Water Heater for Power Plant market is on a robust growth trajectory, driven by the ongoing need for reliable power generation infrastructure globally. The projected CAGR highlights a sustained demand, underpinned by both the construction of new power plants in emerging economies and the imperative to upgrade and optimize existing facilities in developed regions. A significant takeaway is the increasing investment in energy efficiency technologies, where feed water heaters play a crucial role in improving overall plant thermal performance and reducing fuel consumption.

Furthermore, the market's future growth is intrinsically linked to advancements in material science and digital integration, including AI and IoT, which promise to enhance the operational lifespan and efficiency of these components. Stakeholders are focusing on strategies that not only cater to the immediate power generation demands but also align with long-term sustainability goals, emphasizing lower emissions and reduced operational costs. The continued modernization of power grids and the strategic shift towards more efficient and flexible power sources will be pivotal in shaping the market's direction through 2033.

- Consistent market growth anticipated due to global energy demand and infrastructure modernization.

- Significant opportunities in retrofitting and upgrading existing power generation assets.

- Technological advancements, including smart monitoring and advanced materials, are key enablers.

- Market expansion is influenced by both new plant construction and efficiency improvements in mature markets.

- Sustainability and operational cost reduction are central to investment decisions.

Feed Water Heater for Power Plant Market Drivers Analysis

The global demand for electricity continues to rise steadily, particularly in developing economies, necessitating the construction of new power generation facilities across various fuel types. Feed water heaters are indispensable components in these plants, directly impacting their thermal efficiency and overall operational performance. This pervasive requirement for new capacity, combined with the continuous operation of existing plants, inherently drives the market for these critical components, ensuring their integral role in the power generation value chain.

A significant driver is the global emphasis on improving energy efficiency and reducing carbon emissions from power generation. Feed water heaters contribute significantly to improving the overall thermal efficiency of steam cycles by preheating boiler feedwater using extraction steam, thereby reducing fuel consumption and operational costs. Governments and regulatory bodies worldwide are implementing stricter environmental norms and offering incentives for energy-efficient technologies, compelling power plant operators to invest in modernizing or replacing their existing feed water heater systems to meet these standards and achieve better economic returns.

Furthermore, the aging power infrastructure in many developed countries presents substantial opportunities for market growth. A large proportion of operational power plants globally are reaching or have exceeded their intended design life, necessitating substantial investments in maintenance, upgrades, and replacements of key components, including feed water heaters. This replacement demand, coupled with technological advancements offering more efficient and durable designs, creates a continuous cycle of demand that fuels market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Electricity Demand | +1.5% | Asia Pacific, Middle East & Africa | 2025-2033 |

| Focus on Energy Efficiency & Emission Reduction | +1.2% | Europe, North America, China | 2025-2030 |

| Aging Power Infrastructure & Replacement Needs | +1.0% | North America, Europe | 2025-2033 |

| Industrial Expansion & Co-generation Growth | +0.8% | Developing Economies | 2027-2033 |

Feed Water Heater for Power Plant Market Restraints Analysis

The substantial upfront capital expenditure required for installing or replacing feed water heater systems represents a significant restraint on market growth. These systems involve complex engineering, high-grade materials, and intricate installation processes, leading to considerable initial costs. For power plant operators, particularly those facing budget constraints or uncertain regulatory environments, this high investment can deter modernization projects or lead to delayed replacements, thereby slowing market progression.

Another major restraint stems from the increasing global shift towards renewable energy sources such as solar, wind, and hydropower. As countries commit to decarbonization and transition away from fossil-fuel-based power generation, the rate of new thermal power plant construction, which are the primary consumers of feed water heaters, is declining in many regions. This fundamental shift in energy policy and investment priorities reduces the core market for new feed water heater installations, posing a long-term challenge to the industry's expansion.

Furthermore, the long operational life and replacement cycles of existing feed water heaters contribute to market cyclicality and can act as a restraint. Once installed, these components are designed to function efficiently for several decades, meaning that replacement demand primarily arises from end-of-life failures or significant upgrades rather than routine, short-term cycles. This extended lifespan reduces the frequency of new purchases, leading to periods of stagnant demand and impacting manufacturers' revenue streams and market growth rates.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure | -0.9% | Global | 2025-2033 |

| Shift Towards Renewable Energy Sources | -1.2% | Europe, North America, Japan | 2025-2033 |

| Long Replacement Cycles of Existing Units | -0.7% | Global | 2025-2030 |

| Stringent Environmental Regulations | -0.6% | Developed Countries | 2025-2033 |

Feed Water Heater for Power Plant Market Opportunities Analysis

The widespread existence of aging power plant infrastructure globally presents a significant opportunity for the Feed Water Heater for Power Plant market. Many operational thermal power plants, particularly in developed economies, were constructed decades ago and are in dire need of modernization or component replacement to enhance efficiency, comply with updated environmental regulations, and extend their operational lifespan. This retrofitting and upgrade segment offers a substantial market avenue for advanced, more efficient feed water heaters that can seamlessly integrate into existing systems, boosting plant performance without requiring entirely new construction.

Technological advancements in materials science and manufacturing processes are opening new avenues for innovation and market expansion. The development of corrosion-resistant alloys, improved welding techniques, and more efficient heat transfer designs allows for the production of feed water heaters that are more durable, reliable, and perform better under harsh operating conditions. These innovations not only cater to the replacement market but also attract new investments by promising reduced maintenance costs and enhanced long-term operational efficiency, thereby expanding the competitive landscape and driving product differentiation.

Furthermore, the growth of industrial co-generation and combined heat and power (CHP) plants represents a burgeoning opportunity. These facilities efficiently produce both electricity and useful heat, often utilizing steam cycles where feed water heaters are crucial for optimizing the overall energy conversion process. As industries increasingly seek to reduce their energy costs and carbon footprint, the adoption of CHP solutions is gaining traction, particularly in sectors such as chemicals, paper, and food processing, thereby creating a new demand segment for specialized feed water heater applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Retrofitting & Upgrades of Existing Plants | +1.3% | North America, Europe, China | 2025-2033 |

| Technological Advancements in Materials & Design | +1.0% | Global | 2025-2030 |

| Growth in Industrial Co-generation & CHP Plants | +0.9% | Asia Pacific, Latin America | 2026-2033 |

| Digitalization & Smart Monitoring Solutions | +0.7% | Global | 2025-2033 |

Feed Water Heater for Power Plant Market Challenges Impact Analysis

The Feed Water Heater for Power Plant market faces significant challenges from the volatility in raw material prices. Components of feed water heaters, such as tubes and shells, often require specialized alloys like stainless steel, copper-nickel, and other high-strength metals. Fluctuations in the global prices of these commodities can directly impact manufacturing costs, leading to unpredictable pricing for end-products. This uncertainty can erode profit margins for manufacturers and make project budgeting difficult for power plant operators, potentially delaying or increasing the cost of new installations and replacements.

Another prominent challenge is the increasing intensity of competition within the market. The industry comprises a mix of large, established global players and numerous regional manufacturers, leading to intense price competition and continuous pressure on margins. Furthermore, technological advancements and differentiation can be difficult to achieve sustainably, as innovations are often quickly adopted or reverse-engineered. This competitive landscape necessitates continuous investment in R&D and operational efficiency to maintain market share, which can be particularly challenging for smaller players.

The specialized skill set required for the design, manufacturing, installation, and maintenance of feed water heaters poses a significant challenge in terms of skilled labor availability. A shortage of experienced engineers, technicians, and specialized welders capable of handling these complex systems can lead to project delays, increased labor costs, and compromised quality. This talent gap is particularly acute in regions experiencing rapid industrial growth or where an aging workforce is retiring, creating bottlenecks in project execution and overall market development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% | Global | 2025-2033 |

| Intense Market Competition & Price Pressure | -0.7% | Global | 2025-2033 |

| Shortage of Skilled Labor | -0.6% | Developed & Emerging Economies | 2025-2030 |

| Stringent Quality & Safety Standards | -0.5% | Global | 2025-2033 |

Feed Water Heater for Power Plant Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Feed Water Heater for Power Plant Market, covering historical data, current market conditions, and future projections. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges affecting the industry. The report segments the market by product type, application, and end-use, providing granular insights into each category's performance and future outlook. Furthermore, it includes a thorough regional analysis and profiles of key market players, offering a holistic view for stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.95 Billion |

| Market Forecast in 2033 | USD 4.28 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GE Power, Siemens Energy, Mitsubishi Heavy Industries (MHI), Toshiba Energy Systems & Solutions, Doosan Enerbility, IHI Corporation, Babcock & Wilcox Enterprises, Valmet, Thermax Limited, John Cockerill, Harbin Electric Corporation, Dongfang Electric Corporation, Bharat Heavy Electricals Limited (BHEL), SPX Corporation, Fuji Electric Co., Ltd., Alfa Laval, Flowserve Corporation, Graham Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Feed Water Heater for Power Plant market is comprehensively segmented to provide a detailed understanding of its various facets and dynamics. This segmentation facilitates a granular analysis of market performance across different product categories, applications, and end-use sectors, helping stakeholders identify specific growth opportunities and competitive landscapes. The primary segmentation distinguishes between High Pressure and Low Pressure Feed Water Heaters, reflecting their distinct operational parameters and applications within power generation cycles. High pressure heaters are typically located after the boiler feed pump, while low pressure heaters are upstream, each contributing differently to overall thermal efficiency.

Further segmentation by application highlights the prevalence of feed water heaters across different types of power plants, including coal-fired, nuclear, gas-fired, and combined cycle facilities. Each application has unique requirements regarding design, materials, and operating conditions, influencing demand patterns for specific types of heaters. The industrial power plant segment also forms a crucial part of this analysis, acknowledging the significant role of feed water heaters in industrial co-generation and captive power units.

Lastly, the market is segmented by end-use, encompassing power generation, industrial processes, and marine propulsion systems. While power generation remains the largest segment, the increasing adoption of feed water heaters in various industrial applications for process heating and waste heat recovery, as well as in large marine vessels for propulsion efficiency, indicates diversifying demand streams. This multi-dimensional segmentation provides a robust framework for assessing market trends, competitive positioning, and strategic planning.

- By Type:

- High Pressure Feed Water Heaters

- Low Pressure Feed Water Heaters

- By Application:

- Coal-fired Power Plants

- Nuclear Power Plants

- Gas-fired Power Plants

- Combined Cycle Power Plants

- Industrial Power Plants

- By End-Use:

- Power Generation

- Industrial Processes

- Marine Propulsion Systems

Regional Highlights

- North America: This region is characterized by an aging power infrastructure, leading to significant demand for replacements and upgrades of feed water heater systems to enhance efficiency and comply with environmental regulations. The focus on modernizing existing thermal plants and increasing investments in combined cycle gas turbine (CCGT) plants drives market growth.

- Europe: Driven by strict emission regulations and a strong emphasis on energy efficiency, Europe is a mature market focusing on retrofitting and optimizing existing power plants. While new thermal plant construction is limited due to renewable energy targets, the demand for high-efficiency and low-maintenance feed water heaters for operational sustainability remains robust.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid industrialization, urbanization, and a surging demand for electricity, particularly in emerging economies like China, India, and Southeast Asian countries. Substantial investments in new coal-fired, gas-fired, and nuclear power plant construction are primary drivers for feed water heater adoption in this region.

- Latin America: This region presents considerable growth opportunities, primarily due to increasing industrial activities and the need for reliable power infrastructure development. Countries like Brazil and Mexico are witnessing investments in new thermal power projects and upgrades, contributing to the demand for feed water heaters.

- Middle East and Africa (MEA): The MEA region is experiencing significant power generation capacity expansion, driven by economic diversification and population growth. Investments in new gas-fired power plants and some large-scale industrial projects across the Gulf Cooperation Council (GCC) countries and parts of Africa are propelling the demand for feed water heaters.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Feed Water Heater for Power Plant Market.- GE Power

- Siemens Energy

- Mitsubishi Heavy Industries (MHI)

- Toshiba Energy Systems & Solutions

- Doosan Enerbility

- IHI Corporation

- Babcock & Wilcox Enterprises

- Valmet

- Thermax Limited

- John Cockerill

- Harbin Electric Corporation

- Dongfang Electric Corporation

- Bharat Heavy Electricals Limited (BHEL)

- SPX Corporation

- Fuji Electric Co., Ltd.

- Alfa Laval

- Flowserve Corporation

- Graham Corporation

Frequently Asked Questions

What is a feed water heater in a power plant?

A feed water heater is a heat exchanger used in thermal power plants to preheat boiler feedwater before it enters the boiler. It utilizes extraction steam from various turbine stages, significantly improving the overall thermal efficiency of the steam cycle by recovering waste heat and reducing the amount of fuel required.

Why is a feed water heater important for power plant efficiency?

Feed water heaters are crucial because preheating the feedwater reduces the amount of heat input required from the boiler to convert water into high-pressure steam. This directly translates to lower fuel consumption, improved thermal efficiency of the entire power generation process, and reduced operational costs and emissions.

What are the primary drivers of the Feed Water Heater for Power Plant market?

Key drivers include the global increase in electricity demand, particularly in developing economies, leading to new power plant construction. Additionally, the aging power infrastructure in developed regions necessitates upgrades and replacements, and the universal focus on improving energy efficiency in power generation further propels market growth.

What are the main challenges facing the Feed Water Heater for Power Plant market?

The market faces challenges such as high upfront capital expenditure for installations, the ongoing global shift towards renewable energy sources which reduces demand for new thermal plants, and the long operational life of existing units leading to extended replacement cycles. Volatile raw material prices and intense market competition also pose significant hurdles.

What is the future outlook for the Feed Water Heater for Power Plant market?

The market is projected for steady growth, driven by continued global energy needs and persistent efforts to enhance the efficiency of thermal power generation. Opportunities arise from retrofitting existing plants, technological advancements in materials and digital integration, and growth in industrial co-generation applications. The market will evolve with an increasing emphasis on smart, high-efficiency, and sustainable solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted