Electronic Design Automation Market

Electronic Design Automation Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704578 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Electronic Design Automation Market Size

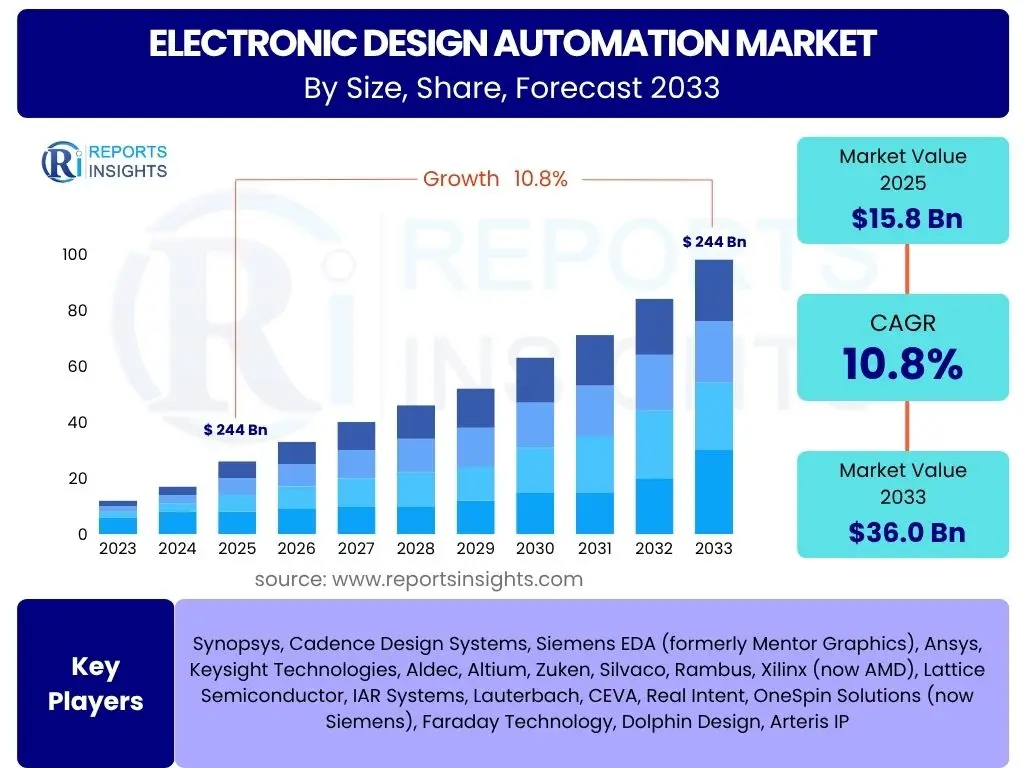

According to Reports Insights Consulting Pvt Ltd, The Electronic Design Automation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 15.8 Billion in 2025 and is projected to reach USD 36.0 Billion by the end of the forecast period in 2033.

Key Electronic Design Automation Market Trends & Insights

The Electronic Design Automation (EDA) market is currently undergoing a significant transformation, driven by an escalating demand for highly integrated and functionally complex semiconductor designs. Key user inquiries frequently center on the disruptive influence of artificial intelligence and machine learning, the imperative for advanced verification methodologies, and the shift towards specialized design architectures like chiplets. These trends reflect the industry's continuous effort to overcome design bottlenecks, reduce time-to-market, and manage the exponential growth in design data, while also addressing critical concerns regarding power efficiency and cost reduction across various applications. The market is adapting rapidly to facilitate innovation in areas such as high-performance computing, artificial intelligence, and sophisticated communication systems.

Furthermore, the increasing adoption of cloud-based EDA solutions is a prominent theme, offering enhanced scalability, collaboration capabilities, and cost efficiencies for design teams globally. Users are also keen to understand how EDA tools are evolving to support the burgeoning fields of automotive electronics, the Internet of Things (IoT), and 5G communication, which demand highly reliable and efficient chip designs. The focus remains on improving design productivity, ensuring design integrity, and enabling rapid iteration cycles to meet the aggressive timelines set by competitive global markets. This collective push is shaping the development of next-generation EDA platforms that are more intelligent, automated, and interconnected.

- Growing adoption of Artificial Intelligence (AI) and Machine Learning (ML) for design optimization and verification.

- Increasing complexity of System-on-Chip (SoC) designs and advanced node technologies (7nm, 5nm, 3nm and beyond).

- Shift towards specialized architectures like chiplets and multi-die integration for enhanced performance and power efficiency.

- Rising demand for cloud-based EDA solutions offering scalability, flexibility, and collaborative design environments.

- Intensified focus on advanced verification methodologies, including formal verification and emulation, to ensure design correctness.

- Expansion of EDA tool usage in emerging application areas such as automotive electronics, IoT, and 5G/6G communication.

- Emphasis on Design for Manufacturability (DFM) and yield optimization to reduce production costs and improve reliability.

AI Impact Analysis on Electronic Design Automation

User queries regarding the impact of Artificial Intelligence (AI) on Electronic Design Automation (EDA) consistently highlight its potential to revolutionize every stage of the chip design flow. There is significant interest in how AI can automate complex tasks, optimize design parameters, and accelerate the traditionally time-consuming verification process. Users anticipate AI's role in enabling faster design cycles, managing the increasing complexity of modern ICs, and overcoming the limitations of conventional rule-based approaches, ultimately leading to more efficient, higher-performance, and lower-power designs. Concerns often revolve around the data requirements for training AI models, the interpretability of AI-driven design decisions, and the integration of AI tools within existing EDA ecosystems.

The integration of AI into EDA is expected to introduce a paradigm shift, moving towards more predictive and adaptive design methodologies. Specific expectations include AI-powered synthesis, automated layout generation, intelligent power optimization, and more effective bug detection in verification. The general sentiment is that AI will augment human designers, allowing them to focus on higher-level architectural challenges while routine or highly iterative tasks are managed by AI. This fusion is critical for pushing the boundaries of silicon innovation, making it possible to design chips that were previously unfeasible due to complexity and time constraints, particularly in specialized domains like AI accelerators and quantum computing interfacing.

- AI-driven design optimization for improved power, performance, and area (PPA).

- Accelerated verification cycles through AI-powered anomaly detection and test pattern generation.

- Automated layout and routing, reducing manual effort and design iterations.

- Enhanced predictive capabilities for design manufacturability and yield analysis.

- Intelligent IP integration and system-level design optimization.

- Facilitation of complex design exploration and architectural trade-off analysis.

Key Takeaways Electronic Design Automation Market Size & Forecast

The Electronic Design Automation (EDA) market is poised for robust expansion, driven primarily by the relentless pursuit of advanced semiconductor technologies and the escalating complexity of integrated circuit designs. The projected growth signifies the indispensable role of EDA tools in enabling innovation across a multitude of high-tech industries, from consumer electronics to automotive and artificial intelligence. Stakeholders frequently inquire about the sustainability of this growth, the primary factors contributing to it, and the strategic implications for investment and technological development. The forecast underscores a critical reliance on sophisticated design methodologies to meet accelerating demand for higher performance, lower power consumption, and reduced time-to-market in a fiercely competitive global landscape.

A significant takeaway is the market's resilience and adaptability in navigating technological shifts, particularly the transformative impact of artificial intelligence and cloud computing. The sustained double-digit CAGR indicates a healthy market environment, propelled by continuous investment in research and development, a growing global semiconductor ecosystem, and the imperative for companies to innovate rapidly. This trajectory highlights the strategic importance of EDA as a foundational technology for digital transformation, enabling the creation of next-generation electronic systems that power an increasingly connected and intelligent world. It also signals a heightened focus on talent acquisition and skill development within the EDA sector to sustain this growth momentum.

- Significant market expansion expected due to increasing IC design complexity and technological advancements.

- Artificial Intelligence and cloud adoption are pivotal growth catalysts for the EDA sector.

- Strong demand across diverse end-use industries, including automotive, IoT, and high-performance computing, fuels market growth.

- Continuous innovation in design methodologies and tools is critical for market leadership and competitiveness.

- The market's robust growth trajectory reinforces EDA's foundational role in the global semiconductor ecosystem.

Electronic Design Automation Market Drivers Analysis

The Electronic Design Automation (EDA) market is significantly propelled by several key drivers, reflecting the dynamic nature of the semiconductor industry. The unrelenting demand for increasingly complex and miniature integrated circuits (ICs) necessitates sophisticated EDA tools capable of managing billions of transistors while optimizing for power, performance, and area (PPA). This complexity, coupled with the rapid adoption of advanced process nodes such as 7nm, 5nm, and sub-5nm technologies, mandates highly precise and efficient design and verification solutions, thereby driving investment in EDA software and services. The continuous evolution of electronic systems, including artificial intelligence, 5G communication, and the Internet of Things (IoT), further amplifies the need for specialized EDA capabilities that can handle diverse architectural requirements and accelerate time-to-market.

Moreover, the global expansion of the semiconductor manufacturing industry, particularly in Asia Pacific, coupled with increasing fabless design activity, creates a broader customer base for EDA vendors. The imperative to reduce design cycles and manufacturing costs, while simultaneously improving yield and reliability, compels companies to adopt advanced EDA tools. These tools are crucial for simulating, verifying, and optimizing designs before costly physical fabrication, mitigating risks and accelerating product commercialization. The strategic importance of intellectual property (IP) blocks and their efficient integration into complex SoCs also underscores the value proposition of EDA, as design reuse and IP management become critical for competitive advantage.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity of IC Designs | +2.5% | Global | Short to Medium Term |

| Growing Adoption of Advanced Process Nodes | +2.2% | Asia Pacific, North America | Medium Term |

| Rising Demand for IoT, AI, and 5G/6G Applications | +2.0% | Global | Medium to Long Term |

| Emphasis on Faster Time-to-Market | +1.8% | North America, Europe, Asia Pacific | Short Term |

| Emergence of Chiplet and Heterogeneous Integration | +1.5% | North America, Asia Pacific | Medium to Long Term |

Electronic Design Automation Market Restraints Analysis

Despite its robust growth, the Electronic Design Automation (EDA) market faces several notable restraints that can potentially temper its expansion. One significant hurdle is the exceptionally high cost associated with advanced EDA software licenses and maintenance. These prohibitive expenses can be a barrier for smaller design houses, startups, or academic institutions, limiting the widespread adoption of the most cutting-edge tools. The steep investment required for state-of-the-art EDA solutions means that sophisticated tools often remain largely accessible only to well-established, large-scale semiconductor companies, creating a potential disparity in design capabilities across the industry. Furthermore, the specialized nature of these tools often necessitates a continuous financial commitment for upgrades and support, adding to the total cost of ownership.

Another major restraint is the persistent shortage of highly skilled EDA engineers and design verification experts. The complexity of modern semiconductor design requires a deep understanding of both electronic engineering principles and the intricacies of advanced EDA tools. This specialized talent pool is relatively small, and the demand consistently outstrips the supply, leading to increased recruitment costs and potential project delays. Moreover, the inherent complexity and interoperability challenges between different EDA tools from various vendors can also pose a restraint. Integrating diverse tools into a seamless design flow often requires significant customization and effort, which can complicate workflows and slow down design cycles, particularly in large-scale projects involving multiple design teams and legacy systems. Intellectual property (IP) protection concerns, especially with the rise of cloud-based EDA, also present a restraint as companies weigh the benefits of flexible cloud environments against potential security vulnerabilities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Licensing Costs | -1.5% | Emerging Economies, SMEs | Short to Medium Term |

| Shortage of Skilled EDA Professionals | -1.0% | Global | Medium to Long Term |

| Complexity of Tool Integration and Interoperability Issues | -0.8% | Global | Short to Medium Term |

| Intellectual Property (IP) Security Concerns in Cloud Deployments | -0.7% | Global | Medium Term |

Electronic Design Automation Market Opportunities Analysis

The Electronic Design Automation (EDA) market is rich with opportunities, primarily driven by emerging technological paradigms and evolving industry needs. The shift towards cloud-based EDA solutions represents a significant avenue for growth, offering unparalleled scalability, accessibility, and collaboration capabilities. This model democratizes access to high-performance computing resources, enabling smaller companies and startups to leverage advanced design tools without massive upfront infrastructure investments. Cloud EDA also facilitates global collaboration, reducing geographical barriers for design teams and accelerating project timelines. The ongoing innovation in cloud security and data management is steadily addressing initial concerns, paving the way for broader enterprise adoption, particularly for complex and sensitive designs.

Furthermore, the deepening integration of Artificial Intelligence (AI) and Machine Learning (ML) within EDA tools presents a transformative opportunity. AI/ML can automate highly iterative design tasks, predict design outcomes, and optimize performance across various metrics, dramatically improving efficiency and accuracy. This allows designers to explore a broader design space and make more informed decisions, pushing the boundaries of what is possible in chip design. Another burgeoning opportunity lies in the expansion of EDA into specialized and high-growth application sectors, such as advanced driver-assistance systems (ADAS) and autonomous driving in the automotive industry, complex medical devices, and industrial automation. These sectors demand extremely high levels of reliability, safety, and energy efficiency, necessitating sophisticated and validated EDA workflows. Additionally, the development of open-source EDA tools and platforms, while nascent, could foster innovation, reduce entry barriers, and create new collaborative ecosystems for specific niche applications or educational purposes, though adoption by major commercial entities remains limited.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Cloud-Based EDA Solutions | +2.0% | North America, Europe, Asia Pacific | Medium to Long Term |

| Integration of AI and Machine Learning in EDA Workflows | +2.5% | Global | Medium Term |

| Expansion into Niche & High-Growth Applications (e.g., Automotive, Medical) | +1.8% | Europe, Asia Pacific, North America | Long Term |

| Development of Specialized Tools for Heterogeneous Integration & Chiplets | +1.5% | North America, Asia Pacific | Medium to Long Term |

| Strategic Partnerships and Collaborations | +1.2% | Global | Short to Medium Term |

Electronic Design Automation Market Challenges Impact Analysis

The Electronic Design Automation (EDA) market, while robust, confronts several significant challenges that could influence its growth trajectory. A primary challenge is the relentless pace of technological advancement in semiconductor manufacturing. As process nodes shrink to single-digit nanometers, the complexity of design and verification grows exponentially, requiring EDA tools to constantly evolve and adapt at an unprecedented rate. This creates a perpetual development race for EDA vendors to keep their tools compatible and effective for next-generation fabrication processes, often necessitating substantial R&D investments and presenting risks of tool obsolescence if not updated promptly. Ensuring the accuracy and efficiency of these tools at such minute scales becomes a monumental task, impacting simulation fidelity and overall design reliability.

Another critical challenge is managing the vast amounts of design data generated by highly complex ICs and system-on-chips (SoCs). The sheer volume of data for design, verification, and analysis poses significant storage, processing, and transfer challenges, particularly in a collaborative, distributed design environment. This data proliferation can lead to increased infrastructure costs and longer simulation times if not managed effectively with advanced data management solutions. Furthermore, the market faces increasing pressure to balance the desire for innovation with the need to control costs. While cutting-edge EDA tools are essential for competitive designs, their high price points can be a barrier, especially for smaller players. Moreover, the ongoing geopolitical tensions and supply chain vulnerabilities in the semiconductor industry can indirectly impact the EDA market by affecting investment in new fabs and design projects, thus influencing demand for advanced EDA solutions. Cybersecurity risks, particularly for design IP when utilizing cloud-based or distributed design environments, also represent a growing concern that requires continuous mitigation efforts and robust security protocols from EDA providers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Constant Updates | -1.2% | Global | Short Term |

| Managing Exploding Design Data Volumes | -0.9% | Global | Medium Term |

| High Development Costs for Advanced Tools | -0.8% | Global | Short to Medium Term |

| Intellectual Property (IP) Theft and Security Concerns | -0.7% | Global | Medium Term |

| Talent Retention and Recruitment in a Competitive Landscape | -0.6% | Global | Medium to Long Term |

Electronic Design Automation Market - Updated Report Scope

This report provides a comprehensive analysis of the Electronic Design Automation (EDA) market, segmenting it by tool type, application, deployment model, and end-user, along with a detailed regional outlook. It covers historical market performance from 2019 to 2023, provides current estimates for 2024, and projects future growth through 2033. The scope includes an in-depth examination of market drivers, restraints, opportunities, and challenges influencing the industry landscape. Special attention is given to the impact of artificial intelligence and machine learning on EDA, as well as the strategic profiles of leading market players, offering a holistic view of the market's dynamics and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.8 Billion |

| Market Forecast in 2033 | USD 36.0 Billion |

| Growth Rate | 10.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Synopsys, Cadence Design Systems, Siemens EDA (formerly Mentor Graphics), Ansys, Keysight Technologies, Aldec, Altium, Zuken, Silvaco, Rambus, Xilinx (now AMD), Lattice Semiconductor, IAR Systems, Lauterbach, CEVA, Real Intent, OneSpin Solutions (now Siemens), Faraday Technology, Dolphin Design, Arteris IP |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Electronic Design Automation (EDA) market is comprehensively segmented to provide granular insights into its diverse components and drivers. These segmentations are critical for understanding market dynamics, identifying high-growth areas, and developing targeted strategies across the value chain. By categorizing the market based on tool type, application, deployment model, and end-user, the report illuminates how different sectors contribute to the overall market landscape and respond to evolving technological demands. This multi-dimensional analysis allows for a precise evaluation of specific market niches and their growth trajectories, offering a detailed perspective on product adoption patterns and industry-specific requirements.

The segmentation framework highlights the varying needs and preferences of different market participants, from large integrated device manufacturers to specialized fabless companies and emerging startups. Understanding these distinct segments is essential for EDA vendors to tailor their offerings, optimize their sales channels, and enhance customer satisfaction. For instance, the demand for cloud-based solutions is accelerating among design houses seeking flexibility and reduced CapEx, while the automotive and AI sectors require highly specialized verification and synthesis tools to meet stringent performance and safety standards. This detailed segmentation analysis serves as a fundamental guide for strategic planning and competitive positioning within the complex EDA ecosystem.

- By Type: This segment includes various categories of EDA tools and intellectual property.

- Semiconductor Intellectual Property (SIP): Reusable blocks of logic or physical designs for ICs.

- Computer-Aided Design (CAD): Core tools for design entry, simulation, and basic layout.

- IC Physical Design and Verification: Tools for layout, routing, physical verification (DRC, LVS), and timing closure for integrated circuits.

- PCB & MCM Design: Software for designing printed circuit boards and multi-chip modules.

- Services: Customization, consulting, training, and maintenance services related to EDA tools.

- By Application: This segment categorizes EDA usage across different industries.

- Communication: Designing chips for wired and wireless communication systems (5G, networking equipment).

- Consumer Electronics: Chips for smartphones, smart home devices, wearables, etc.

- Automotive: ICs for infotainment, ADAS, power management, and autonomous driving systems.

- Industrial: Chips for industrial automation, robotics, and control systems.

- Medical: Designs for medical imaging, diagnostic devices, and implantable electronics.

- Aerospace & Defense: High-reliability chips for avionics, radar, and defense systems.

- Others: Includes diverse applications such as scientific research and data centers.

- By Deployment: This segment distinguishes between how EDA tools are accessed.

- On-premise: Software installed and run on local servers and workstations.

- Cloud-based: Tools accessed remotely via cloud infrastructure, offering scalability and flexibility.

- By End-User: This segment identifies the primary types of organizations utilizing EDA tools.

- Foundries: Companies that manufacture semiconductor devices for other companies.

- OSATs (Outsourced Semiconductor Assembly and Test): Companies providing assembly, packaging, and testing services.

- Fabless Semiconductor Companies: Companies that design and market hardware devices but outsource their fabrication.

- IDMs (Integrated Device Manufacturers): Companies that design, manufacture, and sell their own integrated circuits.

- Others: Includes design service companies, research institutions, and universities.

Regional Highlights

- North America: This region remains a critical hub for innovation and research and development in the EDA market. Driven by significant investments in cutting-edge technologies like Artificial Intelligence, high-performance computing, and advanced semiconductor manufacturing, North America consistently leads in the adoption and development of sophisticated EDA tools. The presence of major semiconductor design companies and leading EDA software vendors, coupled with a robust ecosystem for venture capital funding, ensures its prominent position. Growth is propelled by continuous advancements in data centers, cloud computing infrastructure, and specialized ICs for next-generation applications.

- Europe: The European EDA market is characterized by strong growth in the automotive electronics and industrial automation sectors. Strict regulatory standards for safety and reliability in these industries necessitate advanced verification and design tools. European research initiatives and collaborations, particularly in areas like embedded systems and IoT, also contribute to the demand for EDA solutions. The region's focus on sustainable and energy-efficient designs further drives the adoption of power-aware EDA tools. Countries such as Germany, France, and the UK are key contributors to the market's expansion through their significant automotive and industrial manufacturing bases.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the EDA market, primarily due to its dominant position in semiconductor manufacturing and a rapidly expanding fabless design industry. Countries like China, Taiwan, South Korea, and Japan are investing heavily in domestic semiconductor capabilities and advanced foundries, leading to a surge in demand for EDA software. The region benefits from a large consumer electronics manufacturing base and increasing adoption of 5G, AI, and IoT technologies, which fuel the need for complex chip designs. Government support and initiatives aimed at fostering local semiconductor ecosystems also play a crucial role in the region's market growth.

- Latin America: While a nascent market compared to other regions, Latin America is showing gradual growth, driven by increasing digitalization and investments in telecommunications infrastructure. The region's expanding consumer electronics market and the nascent growth of local design centers contribute to the demand for EDA tools. However, market adoption is slower due to factors such as higher initial investment costs and a less mature semiconductor ecosystem. Opportunities exist as economies develop and local technology industries mature.

- Middle East and Africa (MEA): The MEA region is at an early stage of EDA market development. Growth is primarily driven by increasing government initiatives in digital transformation, smart city projects, and diversification of economies away from oil dependency. Investments in ICT infrastructure and emerging manufacturing capabilities in certain countries are slowly creating a demand for electronic design tools. However, the market faces challenges related to limited skilled talent, infrastructure constraints, and economic volatility.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electronic Design Automation Market.- Synopsys

- Cadence Design Systems

- Siemens EDA (formerly Mentor Graphics)

- Ansys

- Keysight Technologies

- Aldec

- Altium

- Zuken

- Silvaco

- Rambus

- Xilinx (now AMD)

- Lattice Semiconductor

- IAR Systems

- Lauterbach

- CEVA

- Real Intent

- OneSpin Solutions (now Siemens)

- Faraday Technology

- Dolphin Design

- Arteris IP

Frequently Asked Questions

What is Electronic Design Automation (EDA)?

Electronic Design Automation (EDA) refers to a category of software tools and specialized hardware used for designing, simulating, verifying, and optimizing electronic systems, ranging from integrated circuits (ICs) to printed circuit boards (PCBs). EDA tools are indispensable for developing modern semiconductors, enabling engineers to create complex designs efficiently and accurately before physical fabrication, thus reducing development time and costs.

How is AI transforming EDA?

Artificial Intelligence (AI) is significantly transforming EDA by automating complex design and verification tasks, optimizing power, performance, and area (PPA), and accelerating design cycles. AI-powered algorithms enhance tasks such as synthesis, layout, routing, and anomaly detection during verification, enabling designers to manage increased complexity, reduce errors, and explore broader design spaces more efficiently.

What are the key drivers for the EDA market?

Key drivers for the EDA market include the increasing complexity of integrated circuit designs, the rapid adoption of advanced semiconductor process nodes (e.g., 7nm, 5nm), the rising demand for chips in emerging applications like AI, 5G, and IoT, and the continuous pressure for faster time-to-market. These factors necessitate sophisticated EDA tools that can handle billions of transistors and optimize for critical design parameters.

Which regions are leading in EDA adoption?

North America and Asia Pacific are the leading regions in EDA adoption. North America drives innovation and R&D in advanced design methodologies, while Asia Pacific, particularly countries like China, Taiwan, and South Korea, dominates semiconductor manufacturing and experiences high demand due to its large consumer electronics and fabless design industries. Europe is also significant, driven by automotive and industrial electronics.

What are the future prospects for the EDA industry?

The future prospects for the EDA industry are robust, driven by continued advancements in semiconductor technology and the pervasive demand for electronics across all sectors. Key growth areas include further integration of AI/ML, expansion of cloud-based EDA solutions, specialized tools for heterogeneous integration and chiplet designs, and increasing demand from high-growth application areas such as autonomous vehicles and quantum computing.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted