Electronic Circuit Board Underfill Material Market

Electronic Circuit Board Underfill Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700723 | Last Updated : July 27, 2025 |

Format : ![]()

![]()

![]()

![]()

Electronic Circuit Board Underfill Material Market Size

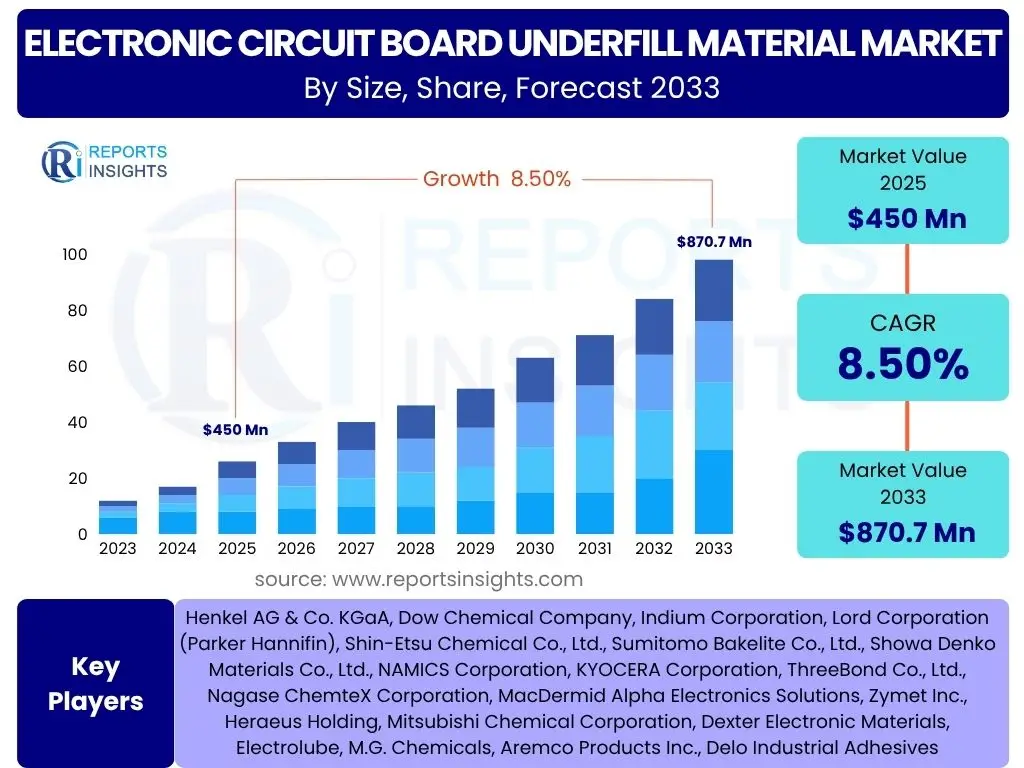

Electronic Circuit Board Underfill Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 870.7 Million by the end of the forecast period in 2033.

The electronic circuit board underfill material market demonstrates robust growth, primarily fueled by the escalating demand for compact, high-performance, and reliable electronic devices across diverse industries. Underfill materials are critical for enhancing the mechanical integrity, thermal management, and electrical performance of advanced packaging technologies such as flip-chip, Ball Grid Array (BGA), and Chip Scale Package (CSP) assemblies. Their ability to reduce stress on solder joints, improve thermal cycling reliability, and prevent delamination is indispensable for modern electronic manufacturing, leading to a consistent expansion in market valuation.

This market expansion is further propelled by the continuous innovation in material science, leading to the development of advanced underfill formulations that offer superior flow characteristics, faster cure times, and enhanced adhesion properties. As electronic components become smaller and more densely packed, the role of underfill materials in ensuring long-term device functionality and durability becomes increasingly pronounced. The forecast period anticipates sustained growth, underpinned by the ubiquitous integration of electronics into new applications and the relentless pursuit of higher reliability in existing ones.

Key Electronic Circuit Board Underfill Material Market Trends & Insights

The Electronic Circuit Board Underfill Material market is profoundly shaped by several evolving trends that address the demands of next-generation electronics. Common user inquiries often revolve around how miniaturization, high-density packaging, and emerging technologies are influencing the need for advanced underfill solutions. Users are keen to understand the shift towards new material chemistries, faster processing, and improved thermal management capabilities in these materials. Furthermore, there is significant interest in the sustainability aspects and application challenges posed by complex electronic designs, all contributing to the dynamic evolution of underfill technologies.

The miniaturization of electronic components remains a primary driver, necessitating underfill materials that can flow into increasingly smaller gaps while maintaining structural integrity. This trend is closely linked to the proliferation of advanced packaging technologies such as flip-chip, wafer-level packaging (WLP), and 3D ICs, where underfill is critical for mitigating thermal and mechanical stresses on interconnections. The push for higher performance and reliability in diverse applications, from consumer electronics to automotive systems, dictates the continuous innovation in underfill formulations. These advancements include lower coefficient of thermal expansion (CTE), improved fracture toughness, and enhanced dielectric properties to support high-frequency signals.

Another significant trend is the development of non-fluxing and no-flow underfills, which simplify manufacturing processes by eliminating separate flux application and cleaning steps, thereby reducing cycle times and costs. The demand for eco-friendly and halogen-free underfill solutions is also rising, driven by increasing environmental regulations and corporate sustainability initiatives. Furthermore, the automotive electronics sector's rapid growth, fueled by electric vehicles (EVs), autonomous driving, and advanced driver-assistance systems (ADAS), places stringent demands on underfill materials for high-temperature stability and long-term reliability in harsh environments. The increasing integration of IoT devices and 5G technology also drives the need for high-performance, durable underfills capable of supporting complex, multi-chip modules.

- Miniaturization and proliferation of advanced packaging technologies (Flip-Chip, BGA, WLP).

- Increased demand for high-performance and high-reliability underfill materials in consumer electronics and automotive.

- Development of non-fluxing, no-flow, and pre-applied underfill solutions for streamlined manufacturing.

- Growing adoption of halogen-free and environmentally friendly underfill formulations.

- Emergence of advanced thermal management underfills for high power density applications.

- Rising integration of underfill in 3D ICs and heterogeneous integration for improved performance.

- Focus on faster curing times and lower processing temperatures for increased production efficiency.

AI Impact Analysis on Electronic Circuit Board Underfill Material

User queries regarding the impact of Artificial intelligence (AI) on the Electronic Circuit Board Underfill Material market often center on its influence on electronic device design, manufacturing processes, and material innovation. There is considerable interest in how AI-driven simulation and optimization tools might accelerate the development of new underfill formulations, predict material performance, and enhance quality control in production. Users also explore the indirect impact of AI's proliferation in end-use devices, which inherently demands more sophisticated and robust electronic components, consequently increasing the need for high-performance underfill materials. The consensus points towards AI acting as both a catalyst for demand and an enabler for more efficient and precise material engineering.

The pervasive integration of AI across various industries directly impacts the demand for underfill materials by driving the need for more powerful, compact, and reliable electronic circuits. AI applications, particularly in data centers, autonomous vehicles, 5G infrastructure, and advanced consumer electronics, require high-density interconnects and robust thermal management, making underfill an essential component for ensuring the longevity and performance of these sophisticated systems. The increased complexity and power consumption of AI-enabled processors and modules necessitate superior mechanical protection and thermal dissipation, roles perfectly addressed by advanced underfill solutions.

Furthermore, AI is increasingly being leveraged within the manufacturing and research and development processes for underfill materials themselves. AI-driven algorithms can optimize material formulations by predicting properties based on molecular structures, accelerating the discovery of novel compounds with desired characteristics like improved flow, adhesion, or thermal conductivity. In manufacturing, AI can enhance process control and quality assurance, leading to more consistent and defect-free underfill application, reducing waste, and improving overall production efficiency. Predictive maintenance for underfill dispensing equipment, informed by AI, also contributes to minimized downtime and optimized operational performance, thereby indirectly boosting market efficiency and material adoption.

- Increased demand for high-performance underfill due to complex AI processors and modules.

- AI-driven optimization in material R&D for faster development of new underfill formulations.

- Enhanced quality control and process monitoring in underfill manufacturing using AI.

- Predictive analytics for equipment maintenance, improving efficiency of underfill application.

- Simulation of underfill performance under various stress conditions, informed by AI models.

- Indirect growth from AI's pervasive adoption across industries like automotive, healthcare, and IoT.

- Acceleration of product innovation cycles in electronics, driving demand for advanced underfill.

Key Takeaways Electronic Circuit Board Underfill Material Market Size & Forecast

Common user questions about the key takeaways from the Electronic Circuit Board Underfill Material market size and forecast reveal a strong interest in understanding the core growth drivers, the critical role of technology in shaping the market, and the overall strategic implications for market participants. Users frequently inquire about the segments offering the most significant growth potential, the primary regional dynamics influencing market expansion, and the long-term sustainability of the observed growth trajectory. The synthesized insights highlight that the market is on a robust upward trajectory, primarily driven by technological advancements in electronics packaging and an increasing emphasis on device reliability and performance across a spectrum of end-use applications.

The market's substantial Compound Annual Growth Rate (CAGR) signifies a continuous and escalating demand for underfill solutions, integral to the progression of advanced electronics manufacturing. This growth is intrinsically linked to the relentless pursuit of miniaturization, higher integration densities, and enhanced performance in electronic devices, ranging from consumer gadgets to highly critical automotive and industrial systems. The forecast period underscores that underfill materials are not merely auxiliary components but fundamental enablers of next-generation electronic design, validating their indispensable role in modern technological ecosystems.

Key strategic takeaways for businesses in this sector include the imperative for continuous innovation in material science, focusing on formulations that address specific performance challenges such as thermal management, faster cure times, and environmental compliance. Furthermore, understanding the regional nuances of electronic manufacturing, particularly the rapid expansion in Asia Pacific, is crucial for market penetration and strategic investment. The market's resilience and growth potential are sustained by the ever-increasing complexity and reliability requirements of electronic components, making it a pivotal area within the broader electronics materials industry.

- Robust market expansion driven by miniaturization and advanced packaging technologies.

- Critical role of underfill in enhancing reliability and thermal management of electronic circuits.

- Significant growth opportunities in automotive electronics, 5G infrastructure, and IoT devices.

- Asia Pacific region identified as the primary growth engine due to dominant electronics manufacturing.

- Increasing emphasis on eco-friendly and halogen-free underfill formulations.

- Continuous material innovation is essential to meet evolving performance requirements.

- Strong long-term market outlook sustained by ongoing advancements in semiconductor and electronics industries.

Electronic Circuit Board Underfill Material Market Drivers Analysis

The Electronic Circuit Board Underfill Material market is primarily propelled by the ever-increasing demand for miniaturized and high-performance electronic devices across various sectors. As electronic components become smaller and more densely packed, the critical need for enhanced reliability, thermal management, and mechanical protection of solder joints becomes paramount. Underfill materials are indispensable in mitigating stresses, preventing cracks, and improving the overall lifespan of these advanced electronic assemblies, directly fueling market growth.

Moreover, the widespread adoption of advanced packaging technologies such, as flip-chip, Ball Grid Array (BGA), and Chip Scale Package (CSP), significantly drives the demand for underfill materials. These technologies, integral to modern electronics, rely heavily on underfill to ensure the structural integrity and electrical performance of high-density interconnections. The continuous innovation in consumer electronics, including smartphones, wearables, and high-definition televisions, further contributes to the market's expansion, as these devices necessitate robust and reliable internal circuitry capable of withstanding various operational stresses.

The rapid expansion of the automotive electronics sector, particularly with the advent of electric vehicles, autonomous driving systems, and advanced driver-assistance systems (ADAS), is another substantial driver. These applications demand extremely durable and high-temperature-resistant electronic components to ensure safety and long-term performance in harsh environmental conditions. Underfill materials provide the necessary thermal and mechanical stability for critical automotive electronic control units (ECUs) and power modules, thereby solidifying their market relevance and fostering sustained growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization of Electronic Devices | +1.2% | Global (APAC, North America) | 2025-2033 |

| Adoption of Advanced Packaging Technologies (Flip-Chip, BGA) | +1.5% | Global (Asia Pacific Dominant) | 2025-2033 |

| Increasing Demand for Consumer Electronics | +1.0% | Global (Asia Pacific, North America) | 2025-2030 |

| Growth in Automotive Electronics Sector | +1.3% | Europe, North America, Asia Pacific | 2025-2033 |

| Rising Need for Enhanced Reliability and Thermal Management | +0.8% | Global | 2025-2033 |

Electronic Circuit Board Underfill Material Market Restraints Analysis

Despite significant growth prospects, the Electronic Circuit Board Underfill Material market faces several restraints that could impede its full potential. One primary concern is the complexity and precision required for underfill application processes. Achieving uniform flow and void-free encapsulation, especially in ultra-fine pitch and low-gap electronic packages, demands highly specialized equipment and skilled labor. This complexity can lead to increased manufacturing costs and potential production bottlenecks, particularly for smaller manufacturers or those transitioning to advanced packaging technologies.

Another significant restraint is the relatively high cost of advanced underfill materials, particularly those formulated for high-performance applications or specialized properties like rapid curing and superior thermal conductivity. These material costs, coupled with the expenses associated with their precise application, can add a substantial overhead to the overall manufacturing cost of electronic devices. This factor can be a barrier for cost-sensitive applications or for companies operating on tighter profit margins, potentially leading them to seek less optimal but cheaper alternatives or simpler packaging solutions where underfill is not mandatory.

Furthermore, challenges related to reworkability and repair often pose a restraint on the adoption of underfill materials. Once applied and cured, underfill forms a strong bond, making it difficult to rework or repair defective components without damaging the entire circuit board. This issue can lead to higher scrap rates and increased warranty costs, especially in high-value electronic assemblies. Environmental regulations, particularly concerning hazardous substances and solvent use in some underfill formulations, also present a growing challenge, compelling manufacturers to invest in research and development for more compliant and eco-friendly alternatives, which can be a slow and costly process.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Application and Process Control | -0.7% | Global | 2025-2033 |

| High Material Costs and Equipment Investment | -0.8% | Global (Emerging Economies) | 2025-2033 |

| Challenges with Rework and Repair of Underfilled Components | -0.5% | Global | 2025-2030 |

| Environmental Regulations and Disposal Concerns | -0.4% | Europe, North America, APAC (China) | 2025-2033 |

| Competition from Alternative Encapsulation Methods | -0.3% | Global | 2028-2033 |

Electronic Circuit Board Underfill Material Market Opportunities Analysis

Significant opportunities exist within the Electronic Circuit Board Underfill Material market, driven by the continuous evolution of electronic device architecture and emerging technological paradigms. The rapid global rollout of 5G technology, for instance, presents a substantial opportunity. 5G devices and infrastructure require high-frequency, high-performance circuits that are more susceptible to thermal and mechanical stresses. Underfill materials are crucial for ensuring the long-term reliability of these components, particularly in demanding environments, thereby creating new avenues for market expansion and specialized product development.

The proliferation of the Internet of Things (IoT) and wearable devices also creates lucrative opportunities for underfill material manufacturers. These devices are characterized by their compact size, flexible designs, and often operate in diverse environmental conditions, necessitating robust and highly reliable electronic packaging. The demand for flexible and stretchable electronics, a burgeoning segment, further opens doors for innovative underfill solutions that can accommodate dynamic mechanical stresses without compromising electrical performance. Developing underfills tailored for these unique applications represents a key area for market growth.

Furthermore, advancements in semiconductor manufacturing, particularly the increasing adoption of advanced packaging techniques like 3D ICs, fan-out wafer-level packaging (FOWLP), and heterogeneous integration, present significant growth potential. These complex architectures require highly specialized underfills with superior flow characteristics, low Coefficient of Thermal Expansion (CTE), and excellent adhesion to diverse substrates. The push towards sustainable and environmentally friendly manufacturing also offers opportunities for companies to develop and commercialize bio-based, solvent-free, or low-VOC (volatile organic compound) underfill materials, aligning with global environmental compliance trends and appealing to a growing segment of environmentally conscious manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Adoption of 5G Technology and Infrastructure | +1.1% | Global (North America, Asia Pacific) | 2025-2030 |

| Proliferation of IoT and Wearable Devices | +0.9% | Global | 2025-2033 |

| Advancements in Semiconductor Packaging (3D ICs, FOWLP) | +1.3% | Asia Pacific, North America | 2025-2033 |

| Development of Flexible and Stretchable Electronics | +0.7% | North America, Europe, Asia Pacific | 2028-2033 |

| Focus on Eco-friendly and Sustainable Material Solutions | +0.6% | Europe, North America | 2025-2033 |

Electronic Circuit Board Underfill Material Market Challenges Impact Analysis

The Electronic Circuit Board Underfill Material market encounters several significant challenges that necessitate continuous innovation and strategic adaptation from manufacturers. One key challenge is the escalating complexity of electronic packaging designs, particularly the trend towards ultra-fine pitch interconnects and smaller die gaps. These advancements demand underfill materials with extremely precise rheological properties, including very low viscosity and excellent capillary flow, to ensure complete void-free filling without trapping air. Achieving these characteristics consistently across high-volume production remains a formidable technical hurdle.

Another pressing challenge is the dynamic nature of material compatibility and adhesion across diverse substrate materials. Modern electronic assemblies often incorporate a wide array of materials, from various types of solder bumps to different substrate finishes and encapsulants. Ensuring robust adhesion and long-term reliability of underfill across all these interfaces, especially under harsh thermal cycling or mechanical stress, requires sophisticated material science and extensive testing. This complexity extends to thermal management, where underfills must effectively dissipate heat from increasingly powerful chips while maintaining structural integrity, often in space-constrained designs.

Furthermore, global supply chain disruptions and raw material price volatility pose significant operational challenges for underfill manufacturers. The reliance on specialized chemicals and polymers, which can be subject to geopolitical factors, trade policies, or unforeseen events, can lead to material shortages and fluctuating costs, impacting production schedules and profitability. The intense competitive landscape, characterized by numerous established players and emerging entrants, also pressures companies to continuously innovate and differentiate their products while managing cost efficiencies. This necessitates substantial investment in research and development to stay ahead of technological requirements and market demands.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity of Packaging Designs (Ultra-fine Pitch) | -0.6% | Global | 2025-2033 |

| Material Compatibility and Adhesion Challenges Across Diverse Substrates | -0.5% | Global | 2025-2030 |

| Supply Chain Volatility and Raw Material Price Fluctuations | -0.7% | Global | 2025-2030 |

| Stringent Thermal Management Requirements for High-Power Devices | -0.4% | Global | 2025-2033 |

| Rapid Technological Obsolescence and Need for Continuous Innovation | -0.3% | Global | 2025-2033 |

Electronic Circuit Board Underfill Material Market - Updated Report Scope

This market research report provides a comprehensive analysis of the Electronic Circuit Board Underfill Material market, encompassing detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope includes an in-depth examination of market drivers, restraints, opportunities, and challenges, offering a holistic view of the factors influencing market growth. It also features a detailed impact analysis of Artificial Intelligence on the underfill market, addressing both direct and indirect influences. The report aims to equip stakeholders with actionable intelligence for strategic decision-making and investment planning within this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 870.7 Million |

| Growth Rate | 8.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Henkel AG & Co. KGaA, Dow Chemical Company, Indium Corporation, Lord Corporation (Parker Hannifin), Shin-Etsu Chemical Co., Ltd., Sumitomo Bakelite Co., Ltd., Showa Denko Materials Co., Ltd., NAMICS Corporation, KYOCERA Corporation, ThreeBond Co., Ltd., Nagase ChemteX Corporation, MacDermid Alpha Electronics Solutions, Zymet Inc., Heraeus Holding, Mitsubishi Chemical Corporation, Dexter Electronic Materials, Electrolube, M.G. Chemicals, Aremco Products Inc., Delo Industrial Adhesives |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Electronic Circuit Board Underfill Material market is comprehensively segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market landscape. This segmentation allows for precise analysis of market dynamics, growth drivers, and opportunities across various product types, application areas, material forms, and packaging technologies. Understanding these distinct segments is crucial for identifying niche markets, tailoring product development, and devising effective market entry and expansion strategies for stakeholders within the electronics materials industry.

The segmentation by product type categorizes underfills based on their chemical composition, influencing their performance characteristics such as adhesion strength, thermal stability, and cure time. Application-based segmentation highlights the primary end-use industries driving demand, reflecting the specific requirements and growth trajectories of sectors like consumer electronics, automotive, and industrial. Furthermore, distinguishing between liquid and film underfills based on their form offers insights into manufacturing process preferences and technological advancements. The segmentation by packaging type, such as flip-chip and BGA, is particularly vital as it directly correlates with the demand for specific underfill properties tailored for advanced interconnect technologies.

- By Product Type:

- Epoxy-based Underfill: Widely used for excellent adhesion and mechanical strength.

- Urethane-based Underfill: Offers flexibility and good adhesion for certain applications.

- Silicone-based Underfill: Known for high-temperature stability and flexibility.

- Acrylic-based Underfill: Provides fast curing and good adhesion.

- Others: Including advanced polymer blends and specialty formulations.

- By Application:

- Smartphones & Tablets: Driven by miniaturization and drop reliability.

- Automotive Electronics: Demanding high reliability and thermal stability for ECUs, ADAS.

- Consumer Electronics (excluding Smartphones & Tablets): Televisions, laptops, gaming consoles, wearables.

- Industrial Electronics: Automation systems, power electronics, robust devices.

- Medical Devices: Compact, reliable, and often biocompatible applications.

- Aerospace & Defense: High-reliability and extreme environment applications.

- Others: Telecommunications, IoT devices, smart home appliances.

- By Form:

- Liquid Underfills: Applied via dispensing, predominant in current manufacturing.

- Film Underfills: Pre-applied films offering precise thickness control and ease of automation.

- By Packaging Type:

- Flip-Chip: Primary application for underfill, enabling high-density integration.

- Ball Grid Array (BGA): Enhances mechanical integrity and thermal cycling reliability.

- Chip Scale Package (CSP): Similar to BGA but smaller, requiring precise underfill application.

- Wafer-Level Packaging (WLP): Emerging segment for compact and cost-effective solutions.

Regional Highlights

- Asia Pacific (APAC): Dominates the Electronic Circuit Board Underfill Material market due to its robust electronics manufacturing base, including major players in consumer electronics, semiconductors, and automotive components in countries like China, South Korea, Taiwan, and Japan. The region's extensive production capabilities and continuous investment in advanced packaging technologies drive substantial demand for underfill materials. Furthermore, the rapid adoption of 5G infrastructure and IoT devices within APAC further accelerates market growth.

- North America: Represents a significant market driven by innovation in high-performance computing, advanced automotive electronics, and aerospace and defense sectors. The region is a hub for research and development in new material formulations and advanced packaging solutions, fostering demand for premium underfill materials. Strict reliability standards in critical applications also bolster the market in this region.

- Europe: Characterized by a strong automotive industry and a growing focus on industrial electronics and medical devices. European manufacturers emphasize high reliability, long-term performance, and environmental compliance, driving the demand for specialized and eco-friendly underfill solutions. Investments in Industry 4.0 and smart manufacturing also contribute to the market's expansion.

- Latin America, Middle East, and Africa (MEA): These regions are emerging markets for Electronic Circuit Board Underfill Materials, driven by increasing industrialization, growing consumer electronics adoption, and developing automotive sectors. While smaller in market share compared to APAC, North America, and Europe, these regions offer untapped potential as their manufacturing capabilities and electronic device consumption continue to expand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electronic Circuit Board Underfill Material Market.- Henkel AG & Co. KGaA

- Dow Chemical Company

- Indium Corporation

- Lord Corporation (Parker Hannifin)

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- Showa Denko Materials Co., Ltd.

- NAMICS Corporation

- KYOCERA Corporation

- ThreeBond Co., Ltd.

- Nagase ChemteX Corporation

- MacDermid Alpha Electronics Solutions

- Zymet Inc.

- Heraeus Holding

- Mitsubishi Chemical Corporation

- Dexter Electronic Materials

- Electrolube

- M.G. Chemicals

- Aremco Products Inc.

- Delo Industrial Adhesives

Frequently Asked Questions

Analyze common user questions about the Electronic Circuit Board Underfill Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Electronic Circuit Board Underfill Material?

Electronic circuit board underfill material is a polymeric resin typically dispensed into the gap between a silicon chip (die) and a substrate, particularly in advanced packaging technologies like flip-chip and BGA. It encapsulates solder bumps, providing mechanical support, mitigating thermal expansion mismatch stress, and enhancing the reliability and lifespan of electronic assemblies.

Why is Underfill Material important in modern electronics?

Underfill material is crucial for modern electronics because it significantly improves the reliability and performance of densely packed circuits. It protects solder joints from mechanical shock, vibration, and thermal cycling stress, which are increasingly common in compact, high-performance devices. This protection prevents premature failure, ensuring long-term functionality and durability.

What are the primary types of Underfill Materials used?

The primary types of underfill materials include epoxy-based, urethane-based, silicone-based, and acrylic-based formulations. Epoxy-based underfills are the most common due to their excellent adhesion and mechanical strength. Each type offers specific properties like flexibility, thermal stability, or rapid curing, tailored for different application requirements and packaging technologies.

Which industries are the largest consumers of Underfill Materials?

The largest consumers of underfill materials are the consumer electronics industry (smartphones, tablets, wearables), the automotive electronics sector (ADAS, ECUs, EVs), and the industrial electronics market. Other significant applications include medical devices, telecommunications infrastructure (5G), and aerospace & defense, all requiring high-reliability electronic components.

What are the key trends shaping the future of Underfill Materials?

Key trends shaping the future of underfill materials include continuous miniaturization and the adoption of advanced packaging techniques (e.g., 3D ICs, WLP), increasing demand for high thermal conductivity and eco-friendly formulations, the rise of no-flow and non-fluxing underfills for simplified manufacturing, and the development of materials for flexible and stretchable electronics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted