Education Cyber Security Market

Education Cyber Security Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705088 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

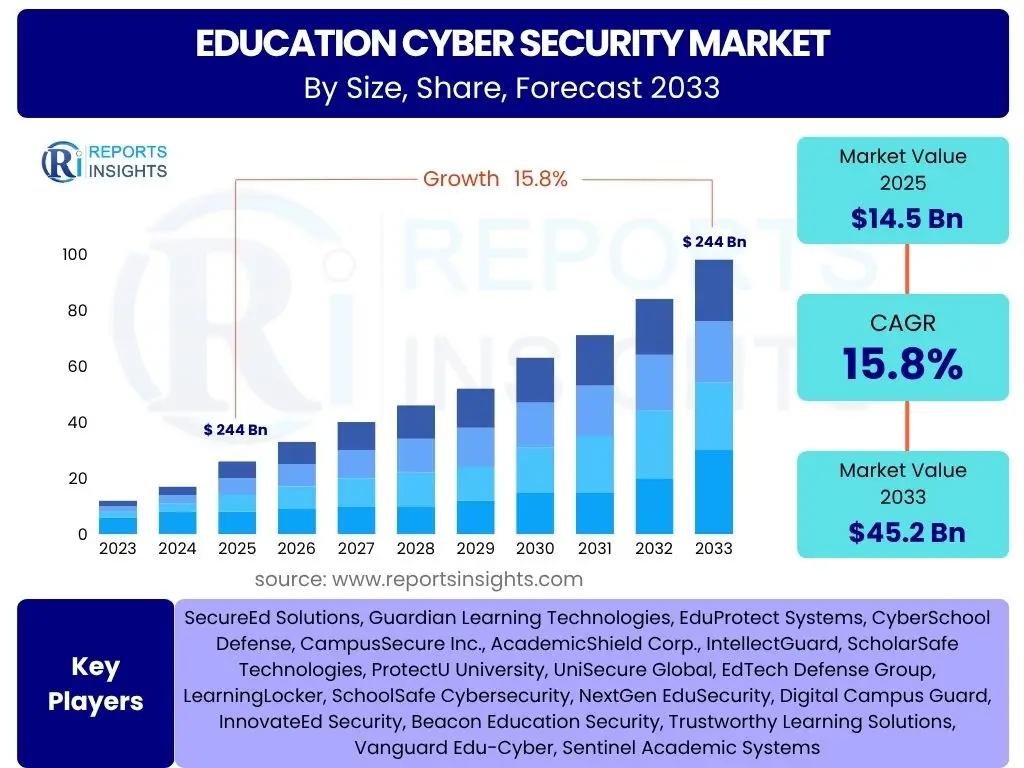

Education Cyber Security Market Size

According to Reports Insights Consulting Pvt Ltd, The Education Cyber Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2033. The market is estimated at USD 14.5 Billion in 2025 and is projected to reach USD 45.2 Billion by the end of the forecast period in 2033.

Key Education Cyber Security Market Trends & Insights

The education sector is undergoing a rapid digital transformation, fueled by the widespread adoption of online learning platforms, remote collaboration tools, and cloud-based educational resources. This shift, while enhancing accessibility and flexibility, has significantly expanded the attack surface for cyber threats. Consequently, educational institutions are increasingly prioritizing robust cybersecurity measures to protect sensitive student data, intellectual property, and critical infrastructure.

A prominent trend is the growing emphasis on data privacy and compliance, driven by regulations such as GDPR, FERPA, and CCPA. Institutions are investing in solutions that ensure the confidentiality and integrity of personal identifiable information (PII) and academic records. Furthermore, the integration of advanced security technologies like Artificial Intelligence (AI) and Machine Learning (ML) for threat detection and anomaly analysis is gaining traction, moving beyond traditional perimeter defenses to more proactive and intelligent security postures.

The rise of hybrid learning models post-pandemic has also necessitated a re-evaluation of security strategies, focusing on securing diverse endpoints, networks, and cloud environments that bridge physical and virtual classrooms. This includes the implementation of Zero Trust architectures and comprehensive security awareness training programs for faculty, staff, and students, recognizing that human error remains a significant vulnerability.

- Proliferation of digital learning platforms and remote education.

- Increased focus on data privacy regulations and compliance.

- Adoption of AI and ML for advanced threat detection and response.

- Shift towards Zero Trust security models.

- Emphasis on comprehensive cybersecurity awareness training.

- Growth in cloud-based security solutions for educational institutions.

- Demand for integrated security frameworks across diverse IT environments.

AI Impact Analysis on Education Cyber Security

The integration of Artificial Intelligence (AI) into education cybersecurity is a transformative development, addressing the escalating sophistication and volume of cyber threats. Users are keenly interested in how AI can automate and enhance threat detection, moving from reactive responses to proactive defense mechanisms. This includes AI's capacity to analyze vast datasets for unusual patterns, identify emerging malware signatures, and detect phishing attempts with greater accuracy than traditional methods, thereby reducing response times and minimizing potential damage.

However, concerns persist regarding the ethical implications of AI, particularly concerning data privacy and the potential for algorithmic bias when processing sensitive student information. Users also question the readiness of educational institutions to deploy and manage complex AI-driven security systems, given existing budget and skill constraints. There is an expectation that AI will not only improve defensive capabilities but also contribute to personalized security training and adaptive risk assessment, tailoring security measures to individual user behaviors and institutional needs.

While AI offers significant promise for bolstering the education cybersecurity posture, its successful implementation hinges on careful consideration of its limitations, robust governance frameworks, and the continuous upskilling of cybersecurity personnel. The balance between leveraging AI's analytical power and mitigating its inherent risks will define its long-term impact on securing educational environments.

- Enhanced threat detection and anomaly identification through machine learning algorithms.

- Automation of security operations, reducing manual intervention and response times.

- Predictive analytics for anticipating future cyberattack vectors.

- Personalized security awareness training based on user behavior patterns.

- Improved vulnerability management and patch prioritization.

- Potential for AI-powered phishing detection and email security.

- Challenges related to data privacy, algorithmic bias, and ethical AI deployment.

Key Takeaways Education Cyber Security Market Size & Forecast

The Education Cyber Security Market is poised for substantial growth over the forecast period, driven by the pervasive digital transformation across educational institutions and the increasing sophistication of cyber threats. This expansion signifies a critical shift in priorities, as institutions recognize that robust cybersecurity is no longer an optional add-on but a fundamental necessity for protecting student data, intellectual property, and maintaining operational continuity. The market's significant projected value indicates a strong commitment from the sector to invest in advanced security solutions and services.

A crucial insight is the dynamic interplay between technological advancements, regulatory pressures, and evolving threat landscapes. The market's growth is inherently linked to the continuous innovation in security technologies, particularly in areas like AI-driven defense and cloud security, which are becoming indispensable for handling distributed learning environments. Furthermore, the global emphasis on data privacy and the legal ramifications of breaches compel educational bodies to adopt comprehensive compliance frameworks, fueling demand for specialized security solutions.

The market forecast also underscores the increasing recognition of human factors in cybersecurity. Beyond technological solutions, there is a growing investment in security awareness training and a focus on cultivating a strong security culture within institutions. This holistic approach, combining technological defense with human preparedness, will be pivotal in shaping the resilience of the education sector against cyberattacks.

- Significant market growth driven by digital transformation and rising cyber threats.

- Investment in cybersecurity is becoming a top priority for educational institutions.

- Data privacy and regulatory compliance are key market growth catalysts.

- AI and cloud security are emerging as critical components of future security strategies.

- Human element, particularly security awareness training, is vital for comprehensive defense.

- Market expansion reflects a shift towards proactive and resilient cybersecurity postures.

Education Cyber Security Market Drivers Analysis

The rapid digitalization of the education sector, encompassing online learning platforms, cloud-based data storage, and pervasive connectivity, has undeniably broadened the attack surface for cyber threats. This digital shift, while offering unparalleled access to education and resources, necessitates robust cybersecurity measures to safeguard sensitive student data, intellectual property, and operational integrity. Institutions are compelled to invest in advanced security solutions to maintain trust and ensure business continuity.

Furthermore, the escalating sophistication and frequency of cyberattacks targeting educational institutions, including ransomware, phishing, and data breaches, are significant drivers. Attackers increasingly view educational networks as lucrative targets due to the vast amounts of personal information and valuable research data they house. This constant threat landscape compels institutions to adopt proactive and comprehensive cybersecurity frameworks, moving beyond basic protections to advanced threat detection and response systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of Digital Learning & Remote Education | +4.2% | Global, particularly North America, Europe, APAC | Short to Mid-term (2025-2029) |

| Increasing Sophistication of Cyber Threats | +3.8% | Global | Short to Long-term (2025-2033) |

| Stringent Data Privacy Regulations (e.g., FERPA, GDPR) | +3.5% | North America, Europe, parts of Asia | Mid-term (2027-2031) |

| Growing Adoption of Cloud-based Educational Infrastructure | +3.0% | Global, particularly emerging economies | Short to Mid-term (2025-2029) |

| Need to Protect Sensitive Student & Research Data | +2.9% | Global | Short to Long-term (2025-2033) |

Education Cyber Security Market Restraints Analysis

One of the primary restraints impeding the growth of the education cybersecurity market is the persistent issue of budgetary constraints within educational institutions. Unlike corporate entities, educational bodies often operate with limited funding, making it challenging to allocate sufficient resources for cutting-edge cybersecurity solutions, skilled personnel, and continuous security upgrades. This financial limitation can lead to delayed adoption of necessary technologies and an over-reliance on basic, less effective security measures, leaving institutions vulnerable.

Furthermore, the complexity of integrating new cybersecurity solutions with existing legacy IT infrastructure presents a significant hurdle. Many educational institutions have disparate systems that have evolved over years, making seamless integration difficult and costly. This complexity can lead to operational disruptions, increased implementation times, and a reluctance to transition to more modern, integrated security platforms. Additionally, a notable shortage of qualified cybersecurity professionals within the education sector compounds these challenges, as institutions struggle to recruit and retain the expertise required to manage advanced security systems effectively.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Budgetary Constraints & Limited Funding | -3.7% | Global, particularly developing regions | Short to Long-term (2025-2033) |

| Lack of Skilled Cybersecurity Professionals | -3.2% | Global | Mid to Long-term (2027-2033) |

| Complexity of Integrating New Solutions with Legacy Systems | -2.8% | Global, particularly established institutions | Short to Mid-term (2025-2029) |

| Resistance to Change & Low Awareness | -2.5% | Certain traditional educational settings | Short to Mid-term (2025-2029) |

| Decentralized IT Management in Large Institutions | -2.0% | North America, Europe | Short to Mid-term (2025-2029) |

Education Cyber Security Market Opportunities Analysis

The burgeoning field of advanced security technologies, particularly those leveraging Artificial Intelligence (AI) and Machine Learning (ML), presents a significant growth opportunity within the education cybersecurity market. These technologies offer capabilities for predictive threat intelligence, automated incident response, and highly accurate anomaly detection, which are crucial for protecting dynamic and complex educational networks. As cyber threats evolve, institutions are increasingly seeking sophisticated solutions that can adapt and defend against emerging attack vectors, creating a fertile ground for innovators in AI/ML security.

Moreover, the growing awareness surrounding cybersecurity risks among educational stakeholders – from administrators to students – is creating a burgeoning demand for comprehensive security awareness and training programs. Beyond technical solutions, educating users about phishing, social engineering, and safe online practices is a critical layer of defense. This growing emphasis on human factors presents an opportunity for service providers to offer tailored training modules and simulations, enhancing the overall security posture of institutions. The expansion of managed security services (MSS) specifically designed for the education sector also represents a substantial opportunity, allowing institutions to outsource complex cybersecurity operations to expert providers, thereby mitigating staffing and resource constraints.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI/ML-driven Security Solutions | +4.0% | Global | Short to Mid-term (2025-2029) |

| Growth in Cybersecurity Awareness Training & Education | +3.6% | Global | Short to Long-term (2025-2033) |

| Rising Demand for Managed Security Services (MSS) | +3.3% | North America, Europe, parts of Asia | Mid to Long-term (2027-2033) |

| Specialized Solutions for K-12 and Higher Education Needs | +2.9% | Global | Short to Mid-term (2025-2029) |

| Increased Public-Private Partnerships for Cybersecurity | +2.5% | North America, Europe | Mid to Long-term (2027-2033) |

Education Cyber Security Market Challenges Impact Analysis

The education sector faces unique cybersecurity challenges due to its highly collaborative and open environment, often characterized by diverse user groups and numerous endpoints. Phishing and ransomware attacks specifically targeting educational institutions remain a pervasive threat, exploiting vulnerabilities in human behavior and outdated systems. These attacks can lead to significant data breaches, operational downtime, and severe reputational damage, particularly given the sensitive nature of student and research data. Institutions struggle to implement effective, sector-specific defenses against these sophisticated social engineering tactics.

Furthermore, managing insider threats and mitigating human error represents a considerable challenge. Faculty, staff, and students, often with varying levels of cybersecurity awareness, interact with a multitude of devices and applications, increasing the risk of accidental data exposure or malicious activity from within. The 'Bring Your Own Device' (BYOD) trend further complicates endpoint security and network segmentation, making it difficult to enforce consistent security policies across a highly dispersed and dynamic digital environment. Keeping pace with the rapid evolution of the threat landscape, combined with the inherent constraints of educational budgets and personnel, requires continuous adaptation and strategic investment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Persistent Phishing & Ransomware Attacks | -3.5% | Global | Short to Long-term (2025-2033) |

| Managing Insider Threats & Human Error | -3.0% | Global | Short to Mid-term (2025-2029) |

| Securing Diverse & Distributed IT Environments (BYOD, Cloud) | -2.8% | Global | Short to Mid-term (2025-2029) |

| Keeping Pace with Evolving Threat Landscape | -2.6% | Global | Short to Long-term (2025-2033) |

| Lack of Centralized Security Governance & Policy Enforcement | -2.3% | Large, decentralized institutions | Mid-term (2027-2031) |

Education Cyber Security Market - Updated Report Scope

This report provides an exhaustive analysis of the global Education Cyber Security market, offering comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges. It segments the market by component, deployment, end-user, and security type, providing a detailed understanding of key market dynamics and competitive landscapes across major regions. The report is designed to assist stakeholders in making informed strategic decisions by delivering a forward-looking perspective on market trends and forecasts from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 45.2 Billion |

| Growth Rate | 15.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SecureEd Solutions, Guardian Learning Technologies, EduProtect Systems, CyberSchool Defense, CampusSecure Inc., AcademicShield Corp., IntellectGuard, ScholarSafe Technologies, ProtectU University, UniSecure Global, EdTech Defense Group, LearningLocker, SchoolSafe Cybersecurity, NextGen EduSecurity, Digital Campus Guard, InnovateEd Security, Beacon Education Security, Trustworthy Learning Solutions, Vanguard Edu-Cyber, Sentinel Academic Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Education Cyber Security market is meticulously segmented to provide a granular view of its diverse landscape and address specific security requirements across various facets of the education sector. This comprehensive segmentation allows for a detailed analysis of market dynamics, identifying high-growth areas and tailoring solutions to precise needs. Understanding these segments is crucial for stakeholders to develop targeted strategies and allocate resources effectively, ensuring comprehensive protection across all educational environments.

The market is primarily segmented by component, distinguishing between robust security solutions and critical support services that enable effective deployment and ongoing management of cybersecurity frameworks. Furthermore, it is categorized by deployment model, reflecting the evolving preferences for cloud-based, on-premise, or hybrid infrastructure. Crucially, the end-user segmentation differentiates between K-12 schools, higher education institutions, and vocational training centers, acknowledging their unique operational contexts and varying threat profiles. Finally, segmentation by security type highlights the specialized focus on protecting networks, endpoints, applications, data, and cloud environments, addressing the multi-layered nature of modern cyber threats in education.

- By Component:

- Solutions:

- Identity & Access Management (IAM)

- Data Loss Prevention (DLP)

- Endpoint Security

- Network Security

- Cloud Security

- Security Information & Event Management (SIEM)

- Encryption

- Vulnerability Management

- Other Solutions (e.g., Web Security, Email Security)

- Services:

- Consulting Services

- Implementation Services

- Managed Security Services (MSS)

- Support & Maintenance Services

- Training & Awareness Programs

- Solutions:

- By Deployment:

- Cloud-based

- On-Premise

- Hybrid

- By End-User:

- K-12 Education (Primary & Secondary Schools)

- Higher Education (Colleges & Universities)

- Vocational & Skill Development Institutions

- By Security Type:

- Network Security

- Endpoint Security

- Application Security

- Data Security

- Cloud Security

Regional Highlights

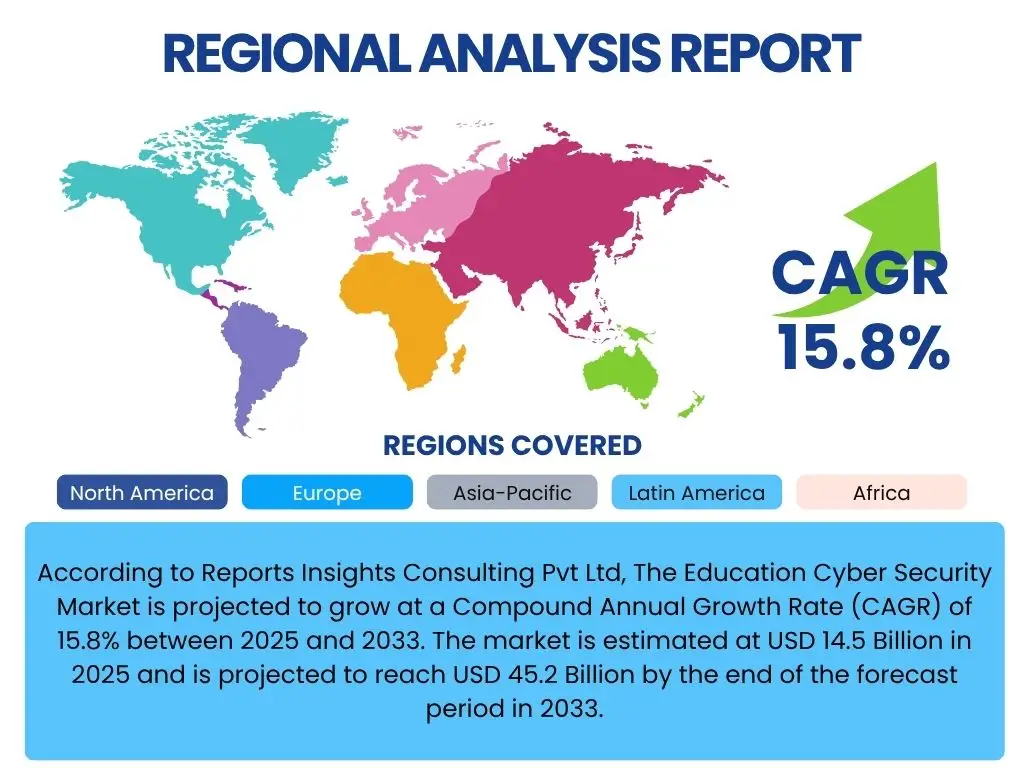

North America is anticipated to lead the Education Cyber Security Market, primarily driven by early and widespread adoption of digital learning technologies, stringent data privacy regulations like FERPA, and a high prevalence of sophisticated cyberattacks targeting its extensive academic research infrastructure. The region benefits from significant investments in advanced security solutions by both government initiatives and private educational institutions, alongside a strong presence of key cybersecurity solution providers and a well-developed IT infrastructure. The increasing shift to remote and hybrid learning models post-pandemic further necessitates robust cybersecurity frameworks, propelling market growth.

Europe also represents a substantial market share, largely influenced by comprehensive data protection regulations such as GDPR, which mandate high levels of data security for educational data. The region's focus on digital education initiatives, coupled with an increasing awareness of cyber threats, is driving the adoption of advanced security technologies. European countries are actively investing in cybersecurity infrastructure for their educational institutions, often through national and EU-level programs aimed at enhancing digital resilience and protecting academic integrity.

Asia Pacific (APAC) is projected to exhibit the highest growth rate during the forecast period, fueled by the rapid expansion of its education sector, growing internet penetration, and the increasing adoption of online learning platforms across developing economies. While still facing challenges related to budget constraints and awareness in some areas, the region's massive student population and burgeoning digital transformation efforts present immense opportunities for cybersecurity vendors. Governments in countries like China, India, Japan, and Australia are increasingly recognizing the importance of securing educational data and infrastructure, leading to greater investments and policy development.

Latin America and the Middle East & Africa (MEA) are emerging markets for education cybersecurity. In Latin America, the push for digital inclusion in education, combined with growing cybercrime rates, is driving demand. MEA is witnessing increased awareness and investment in cybersecurity as digital education initiatives gain momentum, particularly in Gulf Cooperation Council (GCC) countries. However, these regions often face unique challenges such as limited budgets, fragmented IT infrastructure, and a nascent cybersecurity talent pool, which may affect the pace of adoption compared to more developed markets.

- North America: Dominant market share due to advanced digital infrastructure, stringent regulations (FERPA), and high cyberattack incidence.

- Europe: Strong growth driven by GDPR compliance, widespread digital education adoption, and government cybersecurity initiatives.

- Asia Pacific (APAC): Fastest-growing market fueled by massive student population, increasing digitalization, and rising cyber awareness in emerging economies.

- Latin America: Emerging market with increasing adoption spurred by digital education initiatives and rising cyber threats.

- Middle East & Africa (MEA): Growing market due to digital transformation efforts and increasing awareness of cybersecurity importance, particularly in the GCC region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Education Cyber Security Market.- SecureEd Solutions

- Guardian Learning Technologies

- EduProtect Systems

- CyberSchool Defense

- CampusSecure Inc.

- AcademicShield Corp.

- IntellectGuard

- ScholarSafe Technologies

- ProtectU University

- UniSecure Global

- EdTech Defense Group

- LearningLocker

- SchoolSafe Cybersecurity

- NextGen EduSecurity

- Digital Campus Guard

- InnovateEd Security

- Beacon Education Security

- Trustworthy Learning Solutions

- Vanguard Edu-Cyber

- Sentinel Academic Systems

Frequently Asked Questions

Analyze common user questions about the Education Cyber Security market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size of Education Cyber Security?

The Education Cyber Security Market is estimated at USD 14.5 Billion in 2025, reflecting significant investment in protecting digital learning environments.

What are the primary drivers of growth in the Education Cyber Security market?

Key drivers include the rapid digitalization of education, the increasing sophistication of cyber threats targeting institutions, stringent data privacy regulations, and the expansion of remote and hybrid learning models.

How is AI impacting cybersecurity in the education sector?

AI is transforming education cybersecurity by enabling advanced threat detection, automating security operations, and facilitating predictive analytics, though concerns remain regarding data privacy and ethical deployment.

What are the main challenges faced by the Education Cyber Security market?

Significant challenges include persistent phishing and ransomware attacks, managing insider threats, securing diverse IT environments (e.g., BYOD), and overcoming budgetary constraints within educational institutions.

Which regions are leading in the Education Cyber Security market?

North America currently holds the largest market share due to advanced digital infrastructure and strict regulations, while Asia Pacific is projected to experience the fastest growth due to rapid digitalization of its education sector.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted