Edible Packaging Market

Edible Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702299 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

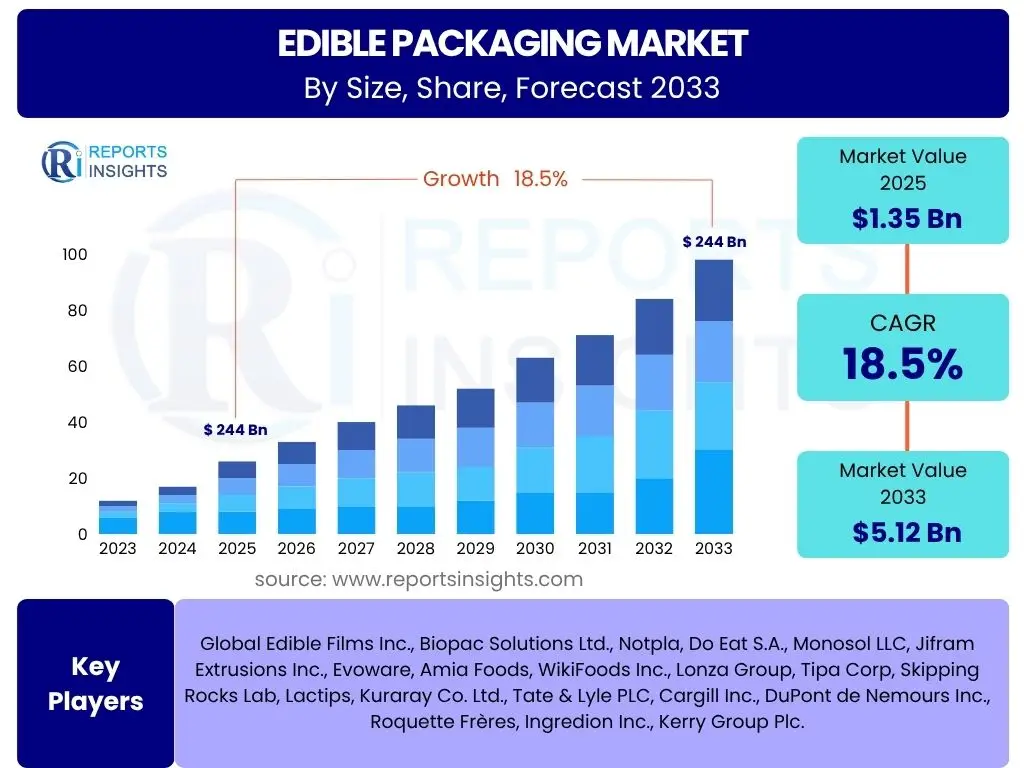

Edible Packaging Market Size

According to Reports Insights Consulting Pvt Ltd, The Edible Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 1.35 Billion in 2025 and is projected to reach USD 5.12 Billion by the end of the forecast period in 2033.

Key Edible Packaging Market Trends & Insights

The edible packaging market is experiencing significant transformation driven by a global shift towards sustainability and a reduction in plastic waste. Consumers and industries alike are increasingly seeking innovative alternatives to traditional packaging, favoring solutions that minimize environmental impact. This growing demand fuels research and development into novel edible materials derived from natural sources, alongside advancements in their application methods and commercial viability.

Technological innovations are playing a crucial role, allowing for the creation of edible films and coatings that offer improved barrier properties, extended shelf life for products, and enhanced food safety. The market is also seeing a rise in specialized applications, moving beyond simple food wraps to include edible cutlery, beverage capsules, and even functional packaging that enhances the nutritional value or taste of the enclosed product. These trends collectively underscore the market's dynamic evolution towards a more eco-conscious and resource-efficient future.

- Growing consumer preference for sustainable and eco-friendly products.

- Stringent government regulations and bans on single-use plastics worldwide.

- Advancements in biodegradable and natural material science, including protein, polysaccharide, and lipid-based films.

- Increasing adoption of edible packaging in the food and beverage industry for extended shelf life and reduced waste.

- Development of functional edible packaging that enhances nutritional value or flavor.

- Rise of innovative applications beyond primary food wrapping, such as edible spoons and cups.

AI Impact Analysis on Edible Packaging

Artificial Intelligence (AI) is poised to revolutionize the edible packaging sector by optimizing various stages of product development, manufacturing, and supply chain management. AI algorithms can analyze vast datasets to identify optimal material compositions, predict material behavior under different environmental conditions, and simulate the barrier properties of novel edible films. This capability significantly accelerates the research and development cycle, leading to the discovery of more effective, cost-efficient, and sustainable packaging solutions. Furthermore, AI can aid in the precise control of manufacturing processes, ensuring consistent quality and reducing waste.

Beyond material science, AI's influence extends to supply chain logistics and waste reduction. Predictive analytics powered by AI can forecast demand more accurately, optimize inventory levels, and minimize spoilage by suggesting ideal storage conditions or distribution routes. This leads to a more efficient use of resources and a reduction in food waste, which is particularly critical given the biodegradable nature of edible packaging. As the industry matures, AI will increasingly become an indispensable tool for enhancing product performance, streamlining operations, and driving sustainable innovation in edible packaging.

- AI-driven optimization of material composition and film development for enhanced barrier properties and shelf life.

- Predictive analytics for quality control and defect detection during manufacturing processes.

- Smart packaging solutions enabled by AI for real-time monitoring of food freshness and spoilage.

- Supply chain optimization and demand forecasting to reduce waste and improve logistics efficiency.

- Personalization of edible packaging designs and functionalities based on consumer preferences and product needs.

- Accelerated R&D through AI simulations for novel edible material discovery and performance testing.

Key Takeaways Edible Packaging Market Size & Forecast

The Edible Packaging Market is on a robust growth trajectory, propelled by increasing environmental consciousness and evolving consumer demands for sustainable products. The substantial projected CAGR signifies a strong industry shift away from traditional, non-biodegradable packaging materials towards innovative, consumable alternatives. This growth is not merely incremental but represents a fundamental transformation in how goods are packaged, driven by regulatory pressures and a collective global commitment to reducing plastic pollution.

The market's expansion is also indicative of successful advancements in material science and processing technologies, making edible packaging more viable and commercially scalable. Key opportunities lie in diversifying applications across various food and beverage segments, as well as addressing existing challenges related to cost, shelf life, and consumer acceptance. Stakeholders investing in research, sustainable practices, and strategic partnerships are well-positioned to capitalize on this burgeoning market and contribute to a more circular economy.

- Significant growth expected due to sustainability demands and plastic waste concerns.

- Rapid innovation in material science is making edible packaging more commercially viable.

- Opportunities for market expansion exist across diverse food and beverage applications.

- Addressing challenges like cost-effectiveness and consumer perception will be crucial for sustained growth.

- The market is shifting towards eco-friendly solutions, indicating a long-term trend.

Edible Packaging Market Drivers Analysis

The global surge in environmental awareness and the escalating crisis of plastic pollution stand as primary drivers for the edible packaging market. Consumers are increasingly scrutinizing the ecological footprint of their purchases, leading to a strong preference for products packaged in sustainable and biodegradable materials. This demand is further amplified by stringent government regulations and outright bans on single-use plastics in numerous countries, compelling industries to seek innovative and compliant alternatives. The collective pressure from consumers, advocacy groups, and regulatory bodies creates a compelling incentive for widespread adoption of edible packaging solutions.

Additionally, continuous advancements in food science and material technology are making edible packaging more feasible and attractive. Researchers are developing new formulations from natural polymers like proteins, polysaccharides, and lipids that offer improved barrier properties, enhanced structural integrity, and longer shelf life, addressing previous limitations. The growing convenience food sector and the need for portion control also present a fertile ground for edible packaging, which can integrate seamlessly into modern lifestyles while contributing to waste reduction.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Consumer Awareness of Plastic Pollution | +1.2% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Stringent Government Regulations & Bans on Single-Use Plastics | +1.5% | Europe, Asia Pacific (China, India), North America (Canada) | Mid-term (2026-2033) |

| Technological Advancements in Edible Material Formulation | +0.9% | Global, especially developed economies with strong R&D | Mid to Long-term (2027-2033) |

| Growing Demand for Sustainable & Eco-Friendly Packaging Solutions | +1.1% | Global, across all income demographics | Short to Mid-term (2025-2030) |

| Rise in Food & Beverage Industry Innovations | +0.8% | Global, especially emerging markets | Mid-term (2026-2033) |

Edible Packaging Market Restraints Analysis

Despite its promising growth, the edible packaging market faces several significant restraints that could impede its widespread adoption and commercial viability. A primary concern is the relatively higher production cost of edible packaging compared to conventional plastic or paper alternatives. The specialized processing techniques, often novel material sourcing, and smaller scale of production contribute to increased expenses, which can deter cost-sensitive businesses and consumers, especially in competitive markets. Achieving economies of scale remains a crucial challenge for many edible packaging manufacturers.

Another considerable restraint involves the inherent limitations of edible materials concerning shelf life, barrier properties, and structural integrity. Many edible films are more susceptible to moisture, oxygen, and microbial degradation than synthetic polymers, potentially compromising food safety and product longevity. Furthermore, consumer acceptance can be a hurdle; educating the public about the safety, benefits, and proper disposal (or consumption) of edible packaging requires significant marketing and outreach efforts, as ingrained perceptions about packaging persist. Regulatory complexities around novel food-contact materials also present a barrier to market entry and expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs Compared to Conventional Packaging | -0.7% | Global, particularly price-sensitive markets | Short to Mid-term (2025-2030) |

| Limited Shelf Life & Barrier Properties of Some Materials | -0.8% | Global, especially for perishable goods | Mid-term (2026-2033) |

| Consumer Acceptance and Perception Challenges | -0.5% | Global, varying by cultural preferences | Short-term (2025-2028) |

| Complex Regulatory Approval Processes for Novel Materials | -0.6% | North America, Europe, Japan | Mid to Long-term (2027-2033) |

| Scalability Issues for Mass Production | -0.4% | Global, emerging manufacturers | Short to Mid-term (2025-2030) |

Edible Packaging Market Opportunities Analysis

The edible packaging market is rife with opportunities stemming from its potential to disrupt traditional packaging norms and address pressing environmental concerns. A significant avenue for growth lies in the expansion into diverse food and beverage segments, particularly those with high volumes of single-use plastic waste, such as confectionery, dairy products, fresh produce, and single-serve snacks. Developing specialized edible packaging solutions tailored to the unique requirements of these segments, including improved moisture resistance or enhanced structural integrity, can unlock substantial market share. The growing global focus on food waste reduction also positions edible packaging as a dual solution, as the packaging itself can be consumed, thereby eliminating traditional waste streams.

Moreover, strategic collaborations between packaging manufacturers, food companies, and academic institutions represent a powerful opportunity for accelerated innovation and market penetration. These partnerships can facilitate knowledge transfer, shared R&D costs, and faster commercialization of new materials and applications. Emerging economies, with their rapidly expanding consumer bases and increasing awareness of environmental issues, also present fertile grounds for market entry and growth, particularly as regulatory frameworks for sustainable packaging become more robust. The integration of edible packaging with smart technologies, such as embedded sensors or QR codes, offers additional value propositions, enhancing consumer engagement and traceability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Potential in Diverse Food & Beverage Segments | +1.3% | Global, specifically developing regions | Mid-term (2026-2033) |

| Technological Innovations in Manufacturing & Application Methods | +1.1% | North America, Europe, East Asia | Mid to Long-term (2027-2033) |

| Strategic Partnerships & Collaborations Across the Value Chain | +0.9% | Global | Short to Mid-term (2025-2030) |

| Emerging Markets with Growing Environmental Consciousness | +1.0% | Asia Pacific (India, Southeast Asia), Latin America | Mid-term (2026-2033) |

| Development of Functional Edible Packaging Solutions | +0.7% | Global, particularly in health and wellness sectors | Long-term (2028-2033) |

Edible Packaging Market Challenges Impact Analysis

The edible packaging market faces inherent challenges that necessitate ongoing innovation and strategic solutions to overcome. A critical hurdle is ensuring the maintenance of adequate structural integrity and barrier properties for a wide range of food products, especially those sensitive to moisture, oxygen, or microbial spoilage. Unlike conventional plastics, edible materials can be delicate and require precise formulations and manufacturing techniques to withstand handling, storage, and transportation stresses, while still providing sufficient protection to the enclosed food. Achieving consistent performance across diverse product types and environmental conditions remains a significant technical challenge.

Furthermore, preventing microbial contamination throughout the supply chain and ensuring the taste neutrality of the packaging are paramount concerns. Any undesirable alteration to the product's flavor or aroma due to packaging interaction can severely impact consumer acceptance. Scaling up production from laboratory to industrial levels also presents considerable engineering and cost challenges, as specialized equipment and processes are often required. Moreover, the establishment of standardized quality control measures and global certifications for edible materials is still evolving, which can create uncertainties for manufacturers and hinder broader market adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Structural Integrity & Barrier Properties | -0.7% | Global, especially for demanding applications | Mid-term (2026-2033) |

| Preventing Microbial Contamination & Ensuring Food Safety | -0.6% | Global, subject to food safety regulations | Short to Mid-term (2025-2030) |

| Ensuring Taste Neutrality and Sensory Acceptance | -0.5% | Global, highly dependent on consumer preferences | Short-term (2025-2028) |

| Scalability & Cost-Effectiveness of Production Technologies | -0.8% | Global, particularly for widespread adoption | Mid-term (2026-2033) |

| Lack of Standardized Regulations & Certifications | -0.4% | Global, varying by regional regulatory bodies | Long-term (2028-2033) |

Edible Packaging Market - Updated Report Scope

This report provides a comprehensive analysis of the global Edible Packaging Market, offering in-depth insights into its current state and future growth prospects. It encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and key trends influencing the industry landscape. The scope includes an assessment of various material types, application areas, and end-use sectors, alongside a thorough regional analysis to highlight geographical market dynamics. The report aims to equip stakeholders with critical data and strategic recommendations necessary for informed decision-making and capitalizing on emerging opportunities in this rapidly evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 5.12 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Edible Films Inc., Biopac Solutions Ltd., Notpla, Do Eat S.A., Monosol LLC, Jifram Extrusions Inc., Evoware, Amia Foods, WikiFoods Inc., Lonza Group, Tipa Corp, Skipping Rocks Lab, Lactips, Kuraray Co. Ltd., Tate & Lyle PLC, Cargill Inc., DuPont de Nemours Inc., Roquette Frères, Ingredion Inc., Kerry Group Plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Edible Packaging Market is comprehensively segmented by material type, application, and end-use, reflecting the diverse approaches and target sectors within this burgeoning industry. Each segment highlights specific technological advancements and market dynamics, offering a granular view of opportunities and challenges. Material segmentation, for instance, categorizes packaging based on its primary composition, ranging from naturally derived proteins to various polysaccharides and lipids, each with distinct barrier properties, shelf life capabilities, and suitability for different food products. This granular analysis provides insights into the prevailing and emerging material technologies driving innovation in the sector.

Application-based segmentation delineates the various food and beverage categories that stand to benefit most from edible packaging, identifying key growth areas such as confectionery, dairy, and fresh produce where the reduction of plastic waste is paramount. Furthermore, the end-use segmentation distinguishes between the food service and retail sectors, highlighting differing requirements for packaging durability, presentation, and consumer interaction. Understanding these segments is crucial for stakeholders to tailor their product offerings, penetrate specific markets, and leverage the most impactful trends.

- By Material: This segment includes protein-based films (e.g., zein, gelatin, casein), polysaccharide-based films (e.g., starch, cellulose, alginate, chitosan), lipid-based coatings (e.g., waxes, fatty acids), and composite materials leveraging combinations for enhanced properties.

- By Application: Encompasses food applications such as bakery and confectionery, dairy products, fruits and vegetables, meat, poultry and seafood, snacks, and other food items. It also covers beverage applications, including liquid beverages and alcoholic beverages.

- By End-Use: Categorizes the market based on where the edible packaging is primarily utilized, dividing it into food service (restaurants, catering, hotels) and retail (supermarkets, convenience stores, online retail).

Regional Highlights

- North America: Expected to hold a significant market share due to increasing consumer awareness regarding sustainable packaging, stringent environmental regulations, and a robust presence of key market players investing in R&D for edible packaging solutions. The region's advanced food processing and packaging infrastructure also facilitates adoption.

- Europe: Anticipated to be a leading region, driven by pioneering environmental policies, strong public demand for plastic-free alternatives, and high investment in green technologies. Countries like Germany, the UK, and France are at the forefront of adopting and innovating in the edible packaging space.

- Asia Pacific (APAC): Projected to witness the fastest growth, primarily fueled by rapid industrialization, a burgeoning population, increasing disposable incomes, and a growing environmental consciousness, particularly in countries like China, India, and Japan. Government initiatives to curb plastic pollution are also contributing significantly to market expansion.

- Latin America: Showing nascent growth, driven by increasing awareness and a push towards sustainable practices. Brazil and Mexico are emerging as key markets, with opportunities for cost-effective edible packaging solutions.

- Middle East and Africa (MEA): Expected to experience gradual growth, influenced by evolving regulatory frameworks for environmental protection and rising consumer interest in innovative, eco-friendly products, though infrastructure and cost remain significant factors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Edible Packaging Market.- Global Edible Films Inc.

- Biopac Solutions Ltd.

- Notpla

- Do Eat S.A.

- Monosol LLC

- Jifram Extrusions Inc.

- Evoware

- Amia Foods

- WikiFoods Inc.

- Lonza Group

- Tipa Corp

- Skipping Rocks Lab

- Lactips

- Kuraray Co. Ltd.

- Tate & Lyle PLC

- Cargill Inc.

- DuPont de Nemours Inc.

- Roquette Frères

- Ingredion Inc.

- Kerry Group Plc.

Frequently Asked Questions

What is edible packaging?

Edible packaging refers to food-grade materials designed to encase food products, which can be consumed along with the product or safely composted/degraded by the environment. It typically consists of natural biopolymers like proteins, polysaccharides, or lipids, offering an eco-friendly alternative to conventional plastic packaging by reducing waste and environmental impact.

What are the primary benefits of edible packaging?

The primary benefits of edible packaging include significant reduction in plastic waste, enhanced sustainability, and decreased environmental footprint. It also offers potential for extended product shelf life by acting as a natural barrier, can be functional by adding nutrients or flavors, and simplifies disposal by eliminating the need for recycling processes.

What materials are commonly used in edible packaging?

Common materials used in edible packaging include protein-based films (e.g., whey protein, gelatin, zein), polysaccharide-based films (e.g., starch, cellulose, alginate, chitosan), and lipid-based coatings (e.g., waxes, fatty acids). These materials are selected for their biodegradability, non-toxicity, and ability to form films or coatings with desired barrier properties.

Is edible packaging safe for consumption?

Yes, edible packaging is designed to be safe for consumption, as it is made from food-grade ingredients and undergoes rigorous testing to meet food safety standards. These materials are generally recognized as safe (GRAS) by regulatory bodies, ensuring that they do not pose health risks or alter the taste and quality of the packaged food.

What are the main challenges facing the edible packaging market?

The main challenges facing the edible packaging market include higher production costs compared to traditional packaging, limitations in shelf life and barrier properties for certain products, and the need for greater consumer acceptance and education. Additionally, issues related to scalability for mass production and developing standardized regulations are significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted