EDA Tool Market

EDA Tool Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707953 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

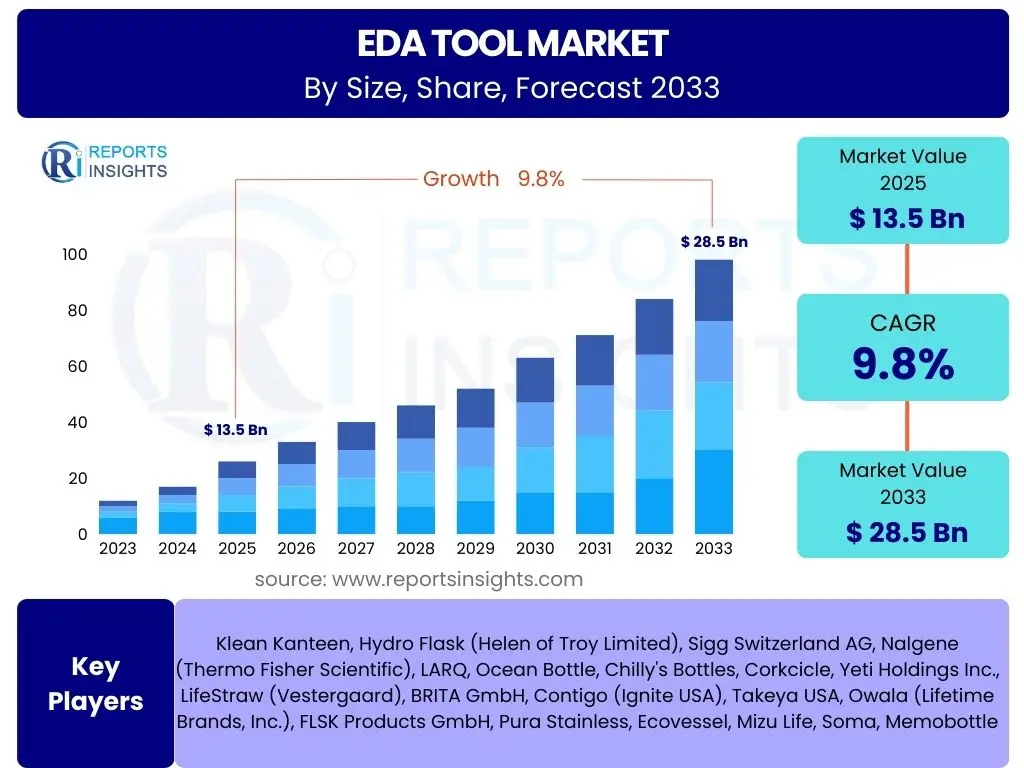

EDA Tool Market Size

According to Reports Insights Consulting Pvt Ltd, The EDA Tool Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 13.5 Billion in 2025 and is projected to reach USD 28.5 Billion by the end of the forecast period in 2033.

Key EDA Tool Market Trends & Insights

The Electronic Design Automation (EDA) tool market is experiencing rapid evolution driven by the increasing complexity of integrated circuit (IC) designs and the relentless demand for smaller, faster, and more power-efficient electronic devices. Key trends indicate a significant shift towards advanced verification methodologies, the integration of artificial intelligence and machine learning (AI/ML) into design flows, and the adoption of cloud-based EDA solutions to enhance flexibility and scalability. Furthermore, the growing demand for specialized EDA tools for advanced packaging, heterogeneous integration, and domain-specific architectures such as those for automotive and high-performance computing are shaping market dynamics.

Another prominent trend involves the rise of design for manufacturability (DFM) and design for testability (DFT) capabilities within EDA suites, ensuring that complex designs are not only functional but also economically viable to produce and easily testable. The market is also witnessing an increased focus on cybersecurity within the design process, addressing vulnerabilities from the earliest stages of chip development. These trends collectively underscore the industry's response to the challenges of Moore's Law, pushing the boundaries of what is possible in semiconductor design and laying the groundwork for future technological advancements.

- Increased integration of AI/ML for design optimization and verification.

- Shift towards cloud-based EDA platforms for enhanced scalability and collaboration.

- Rising adoption of advanced packaging and heterogeneous integration techniques.

- Growing demand for specialized EDA tools for automotive, 5G, and IoT applications.

- Emphasis on design for manufacturability (DFM) and design for testability (DFT).

- Development of comprehensive digital twin solutions for system-level design.

- Enhanced focus on security from design inception (Shift-Left Security).

AI Impact Analysis on EDA Tool

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming the Electronic Design Automation (EDA) landscape, addressing critical bottlenecks in chip design and verification. Users are keenly interested in how AI can automate repetitive tasks, improve optimization algorithms, and accelerate the overall design cycle. Common concerns revolve around the reliability of AI-generated designs, the need for human oversight, and the ethical implications of autonomous design processes. Expectations are high for AI to enhance design quality, reduce verification time, and enable the exploration of vast design spaces that are infeasible with traditional methods, ultimately leading to more efficient and innovative semiconductor products.

AI's influence spans various stages of the EDA workflow, from architectural exploration and logic synthesis to physical design, verification, and testing. It allows for predictive analysis in design rule checking, intelligent power optimization, and even anomaly detection in post-silicon validation. The application of deep learning for pattern recognition in design data, reinforcement learning for optimal placement and routing, and natural language processing for specification analysis are becoming increasingly prevalent. This paradigm shift promises to significantly mitigate the challenges associated with escalating design complexity and tight market windows, making AI a cornerstone of future EDA tool development.

- Design Optimization: AI/ML algorithms optimize power, performance, and area (PPA) across various design stages.

- Verification Acceleration: AI enhances test generation, coverage analysis, and bug detection, reducing verification cycles.

- Predictive Analysis: Machine learning predicts design failures, manufacturability issues, and timing violations early in the flow.

- Automated Layout: AI assists in intelligent placement and routing, potentially achieving better results than human experts.

- Reduced Design Cycle: Automation of complex tasks leads to faster time-to-market for new chips.

- Data-Driven Insights: AI extracts valuable insights from vast design data, improving future design choices.

- System-Level Design: AI aids in architecting complex systems-on-chip (SoCs) and heterogeneous integrations.

Key Takeaways EDA Tool Market Size & Forecast

The EDA Tool market is poised for robust expansion, driven primarily by the escalating demand for advanced semiconductor technologies across diverse end-use industries. Key takeaways from the market size and forecast indicate a consistent upward trajectory, with significant growth fueled by the imperative for highly efficient and compact electronic systems. Users frequently inquire about the primary drivers behind this growth, the sustainability of the projected CAGR, and the sectors expected to contribute most significantly to market expansion. The forecast highlights that continued innovation in chip design, coupled with the proliferation of AI, IoT, and 5G technologies, will be central to sustaining this momentum.

A crucial insight is the increasing capital expenditure by semiconductor companies in research and development, directly translating into higher investments in sophisticated EDA tools. The market's resilience against economic fluctuations is also notable, largely due to the foundational role of EDA in technological advancement. Furthermore, the forecast underscores the strategic importance of geographical regions, particularly Asia Pacific, as both a manufacturing hub and a rapidly expanding consumer market for advanced electronics. This indicates that companies focusing on these high-growth areas, and those continually enhancing their tool capabilities to address emerging technological challenges, are best positioned to capitalize on the projected market growth.

- The market is projected for substantial growth, driven by increasing semiconductor design complexity.

- Integration of AI/ML and cloud technologies will be pivotal for future market expansion.

- Asia Pacific is anticipated to be a dominant region for both EDA consumption and innovation.

- Investments in R&D by semiconductor firms are directly fueling EDA tool adoption.

- The need for faster time-to-market and enhanced design efficiency remains a critical growth driver.

- Advanced packaging and heterogeneous integration are emerging as significant demand generators.

EDA Tool Market Drivers Analysis

The proliferation of highly complex integrated circuits (ICs) and Systems-on-Chip (SoCs) is a primary driver for the EDA Tool market. As semiconductor technology scales down to advanced nodes, the challenges associated with design, verification, and manufacturing intensify exponentially. EDA tools become indispensable for managing this complexity, enabling designers to create intricate circuits while adhering to stringent performance, power, and area (PPA) specifications. The relentless innovation in consumer electronics, automotive, telecommunications, and industrial sectors continuously fuels the demand for more powerful and sophisticated chips, thereby necessitating advanced EDA solutions.

Furthermore, the burgeoning adoption of emerging technologies such such as Artificial Intelligence (AI), the Internet of Things (IoT), 5G communication, and high-performance computing (HPC) significantly contributes to market expansion. These technologies require specialized and highly optimized silicon, driving the development and adoption of advanced EDA tools for domain-specific architecture design, power management, and real-time data processing capabilities. The increasing need for faster time-to-market, coupled with the pressure to reduce design costs and errors, further compels semiconductor companies to invest in comprehensive and efficient EDA ecosystems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity of IC/SoC Designs | +2.5% | Global, particularly North America, APAC | Long-term (2025-2033) |

| Growing Demand for Advanced Electronics (AI, IoT, 5G, Automotive) | +2.0% | Global, strong in APAC, Europe, North America | Long-term (2025-2033) |

| Need for Faster Time-to-Market and Reduced Design Cycles | +1.5% | Global | Mid-to-Long-term (2025-2030) |

| Shift Towards Advanced Packaging Technologies | +1.0% | APAC, North America | Mid-to-Long-term (2026-2033) |

| Rising R&D Investment in Semiconductor Industry | +0.8% | North America, APAC, Europe | Long-term (2025-2033) |

EDA Tool Market Restraints Analysis

Despite the robust growth projections, the EDA Tool market faces several significant restraints that could temper its expansion. One of the primary challenges is the incredibly high cost associated with developing and acquiring advanced EDA software and hardware. The steep licensing fees, coupled with the substantial capital investment required for high-performance computing infrastructure, can deter smaller companies and startups from fully adopting cutting-edge solutions, thereby limiting broader market penetration. This financial barrier often leads to a consolidation of market share among major players who can afford such extensive R&D and licensing costs, stifling competition and innovation from new entrants.

Another critical restraint is the scarcity of highly skilled design engineers and verification experts capable of effectively utilizing complex EDA tools. The sophisticated nature of modern chip design demands specialized expertise in areas such as advanced node design, analog mixed-signal design, and AI-driven verification methodologies. The global shortage of such talent poses a significant impediment to the efficient deployment and optimal use of EDA tools, leading to extended design cycles and potential project delays. Furthermore, intellectual property (IP) protection concerns and the intricate legal frameworks surrounding design reuse and licensing agreements can also introduce friction and complexity into the EDA ecosystem.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Licensing Costs of EDA Software | -1.5% | Global, particularly emerging economies | Long-term (2025-2033) |

| Shortage of Skilled Design and Verification Engineers | -1.0% | Global, strong in North America, Europe | Long-term (2025-2033) |

| Complexity of Learning and Using Advanced EDA Tools | -0.8% | Global | Mid-term (2025-2029) |

| Intellectual Property (IP) Protection Concerns | -0.5% | Global | Long-term (2025-2033) |

| Long Product Development Cycles for New EDA Solutions | -0.3% | Global | Short-term (2025-2027) |

EDA Tool Market Opportunities Analysis

The EDA Tool market is rich with opportunities stemming from the continuous evolution of semiconductor technology and the emergence of new application domains. One significant opportunity lies in the expanding adoption of cloud-based EDA solutions. Cloud computing offers unparalleled scalability, reduced upfront infrastructure costs, and enhanced collaboration capabilities, making advanced design tools accessible to a wider range of users, including startups and smaller design houses. This shift democratizes access to high-performance computing resources necessary for complex simulations and verification, thereby fostering innovation and accelerating product development cycles across the industry.

Another key opportunity is the development of specialized EDA tools tailored for novel materials and advanced architectures. As the industry moves beyond traditional silicon and explores materials like gallium nitride (GaN) and silicon carbide (SiC) for power electronics, or integrates photonic and quantum computing elements, there is a growing need for EDA tools that can accurately model and simulate these new physical properties. Furthermore, the increasing demand for domain-specific accelerators, particularly for AI/ML workloads and edge computing, presents a lucrative niche for EDA vendors to develop highly optimized design flows that can address the unique performance and efficiency requirements of these specialized chips. The open-source hardware movement also offers a fertile ground for developing more accessible and customizable EDA tools, potentially fostering a larger community of developers and users.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Adoption of Cloud-Based EDA Platforms | +1.8% | Global | Long-term (2025-2033) |

| Development of Specialized EDA for Emerging Technologies (e.g., Quantum Computing, Photonics) | +1.5% | North America, Europe, APAC | Mid-to-Long-term (2027-2033) |

| Growth in Domain-Specific Architectures (AI Accelerators, Edge Computing) | +1.2% | Global | Long-term (2025-2033) |

| Expansion into New End-User Industries (e.g., Healthcare, Aerospace) | +0.9% | Global | Mid-to-Long-term (2026-2033) |

| Open-Source Hardware and EDA Tool Development Initiatives | +0.7% | Global | Mid-to-Long-term (2026-2033) |

EDA Tool Market Challenges Impact Analysis

The EDA Tool market faces significant challenges that necessitate continuous innovation and adaptation from vendors. One prominent challenge is managing the ever-increasing complexity and sheer volume of data generated by advanced IC designs. As designs grow exponentially in transistor count and integrate diverse functionalities, the computational resources and algorithms required for simulation, verification, and analysis become incredibly demanding. This data explosion poses significant hurdles in terms of storage, processing power, and the efficiency of data transfer within the design flow, impacting overall design cycle times and infrastructure costs for users.

Another critical challenge involves ensuring interoperability across disparate EDA tools and design flows. The semiconductor design ecosystem often comprises tools from multiple vendors, each specializing in different aspects of the design process. Achieving seamless data exchange, maintaining design integrity across different stages, and integrating new tools into existing workflows can be a formidable task. This lack of universal interoperability can lead to inefficiencies, errors, and increased design time. Furthermore, the rapid pace of technological change and the constant need to support new process nodes, materials, and design methodologies mean that EDA tool developers must continually invest heavily in research and development to avoid technological obsolescence, presenting a persistent financial and engineering challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Exponentially Increasing Design Complexity and Data Volume | -1.2% | Global | Long-term (2025-2033) |

| Ensuring Interoperability Across Diverse EDA Toolchains | -0.9% | Global | Long-term (2025-2033) |

| Rapid Technological Obsolescence and Need for Constant Updates | -0.7% | Global | Long-term (2025-2033) |

| Ensuring Security and Integrity of Design Intellectual Property (IP) | -0.6% | Global | Long-term (2025-2033) |

| Developing EDA Tools for Heterogeneous Integration Challenges | -0.4% | Global | Mid-term (2025-2029) |

EDA Tool Market - Updated Report Scope

This comprehensive market insights report provides an in-depth analysis of the Electronic Design Automation (EDA) Tool market, covering historical performance, current dynamics, and future projections. The scope encompasses detailed segmentation by type, application, deployment, and end-user, offering a granular view of market trends and growth opportunities across key geographical regions. It includes an exhaustive competitive landscape analysis, profiling leading companies and their strategic initiatives, while also examining the impact of pivotal market drivers, restraints, opportunities, and challenges that shape the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.5 Billion |

| Market Forecast in 2033 | USD 28.5 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Synopsys, Cadence Design Systems, Siemens EDA, Ansys, Keysight Technologies, Altium LLC, Silvaco Inc., OneSpin Solutions, Zuken Inc., Mentor Graphics (now Siemens EDA), Aldec, Inc., Real Intent, Inc., Apache Design Solutions, Inc. (now Ansys), Empyrean Technology, Xilinx (now AMD), Rambus, Inc., CeNSE Technologies, Lauterbach GmbH, Tanner EDA (now Mentor Graphics), Xpeedic Technology |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The EDA Tool market is meticulously segmented to provide a detailed understanding of its diverse components and their respective growth trajectories. These segmentations are critical for identifying niche opportunities, understanding competitive dynamics, and tailoring strategic initiatives. The market is primarily divided by type, encompassing crucial tool categories like Semiconductor IP, Computer-Aided Engineering (CAE) for simulation and analysis, IC Physical Design & Verification for layout and testing, and PCB & MCM Design for board-level and multi-chip integration, alongside specialized services. Each segment addresses specific needs within the semiconductor design ecosystem, reflecting the modular nature of the design process.

Further segmentation by application highlights the key industries leveraging EDA tools, including high-growth sectors such as communication, consumer electronics, and automotive, which are major drivers of advanced chip demand. Deployment models, differentiating between traditional on-premise and increasingly popular cloud-based solutions, demonstrate evolving infrastructure preferences. Finally, the end-user segmentation categorizes primary consumers of EDA tools, such as semiconductor foundries, fabless companies, and integrated device manufacturers (IDMs), providing insights into varying design philosophies and operational scales across the industry. This layered segmentation offers a holistic view, crucial for market stakeholders to navigate the complex EDA landscape.

- By Type: Semiconductor IP, CAE (Computer-Aided Engineering), IC Physical Design & Verification, PCB & MCM (Multi-Chip Module) Design, Services

- By Application: Communication, Consumer Electronics, Automotive, Industrial, Medical, Aerospace & Defense, Others

- By Deployment: On-premise, Cloud-based

- By End-User: Semiconductor Foundries, Fabless Semiconductor Companies, IDMs (Integrated Device Manufacturers), OEMs (Original Equipment Manufacturers), Academia & Research

Regional Highlights

- North America: Expected to maintain a significant market share due to the presence of key industry players, robust R&D activities, and early adoption of advanced technologies like AI and quantum computing in chip design. The region continues to be a hub for semiconductor innovation and high-tech manufacturing.

- Europe: Demonstrating steady growth, driven by strong automotive and industrial sectors that demand specialized and reliable semiconductor solutions. Initiatives like the European Chips Act are further bolstering investment in local semiconductor manufacturing and design capabilities.

- Asia Pacific (APAC): Projected to be the fastest-growing region, fueled by expanding electronics manufacturing bases, a booming consumer electronics market, and increasing government investments in semiconductor self-sufficiency, particularly in countries like China, Taiwan, South Korea, and India. This region is a major hub for both production and consumption of chips.

- Latin America: Showing nascent but growing potential, with increasing foreign investments in technology and a developing electronics manufacturing base, particularly in automotive and industrial sectors.

- Middle East & Africa (MEA): Witnessing gradual adoption, primarily driven by investments in digital infrastructure, smart city initiatives, and diversification efforts away from oil-based economies, leading to a modest demand for advanced electronic components.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the EDA Tool Market.- Synopsys

- Cadence Design Systems

- Siemens EDA

- Ansys

- Keysight Technologies

- Altium LLC

- Silvaco Inc.

- OneSpin Solutions

- Zuken Inc.

- Aldec, Inc.

- Real Intent, Inc.

- Empyrean Technology

- Rambus, Inc.

- CeNSE Technologies

- Lauterbach GmbH

- Xpeedic Technology

- Tanner EDA

- Achronix Semiconductor

- Dassault Systèmes

- Intellectual Ventures

Frequently Asked Questions

What is an EDA Tool and why is it essential for the semiconductor industry?

An EDA Tool, or Electronic Design Automation Tool, refers to software and hardware solutions used for designing, simulating, verifying, and manufacturing electronic systems, particularly integrated circuits (ICs) and printed circuit boards (PCBs). It is essential because it automates complex design tasks, reduces human error, accelerates the design cycle, and enables the creation of highly complex and miniaturized electronic devices that would be impossible to design manually, thereby driving innovation in the semiconductor industry.

How is Artificial Intelligence (AI) impacting the development and functionality of EDA Tools?

AI is profoundly impacting EDA tools by enhancing various aspects of the design flow. It is used for intelligent design optimization (e.g., power, performance, area), accelerating verification processes, enabling predictive analysis of design flaws, and automating complex layout tasks. AI-driven EDA tools help designers manage increasing complexity, reduce design time, and achieve better performance metrics for next-generation chips.

What are the primary challenges faced by the EDA Tool market?

The primary challenges in the EDA Tool market include managing the exponentially increasing complexity and data volume of IC designs, ensuring seamless interoperability across diverse toolchains from multiple vendors, and the rapid pace of technological obsolescence requiring constant updates. Additionally, the high cost of advanced tools and the global shortage of skilled engineers capable of utilizing them effectively also pose significant hurdles.

Which geographical region is expected to lead the EDA Tool market growth and why?

The Asia Pacific (APAC) region is expected to lead the EDA Tool market growth. This is primarily due to its robust and expanding electronics manufacturing ecosystem, a large and growing consumer electronics market, and significant government investments in semiconductor research, development, and domestic production capabilities across countries like China, Taiwan, South Korea, and India.

What are the key opportunities for growth in the EDA Tool market?

Key opportunities for growth in the EDA Tool market include the increasing adoption of cloud-based EDA platforms for enhanced accessibility and scalability, the development of specialized tools for emerging technologies such as quantum computing and photonics, and the rising demand for domain-specific architectures like AI accelerators and edge computing solutions. Expansion into new end-user industries and the growth of open-source hardware initiatives also present significant growth avenues.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted