Dry Film Lubricant Market

Dry Film Lubricant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701555 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

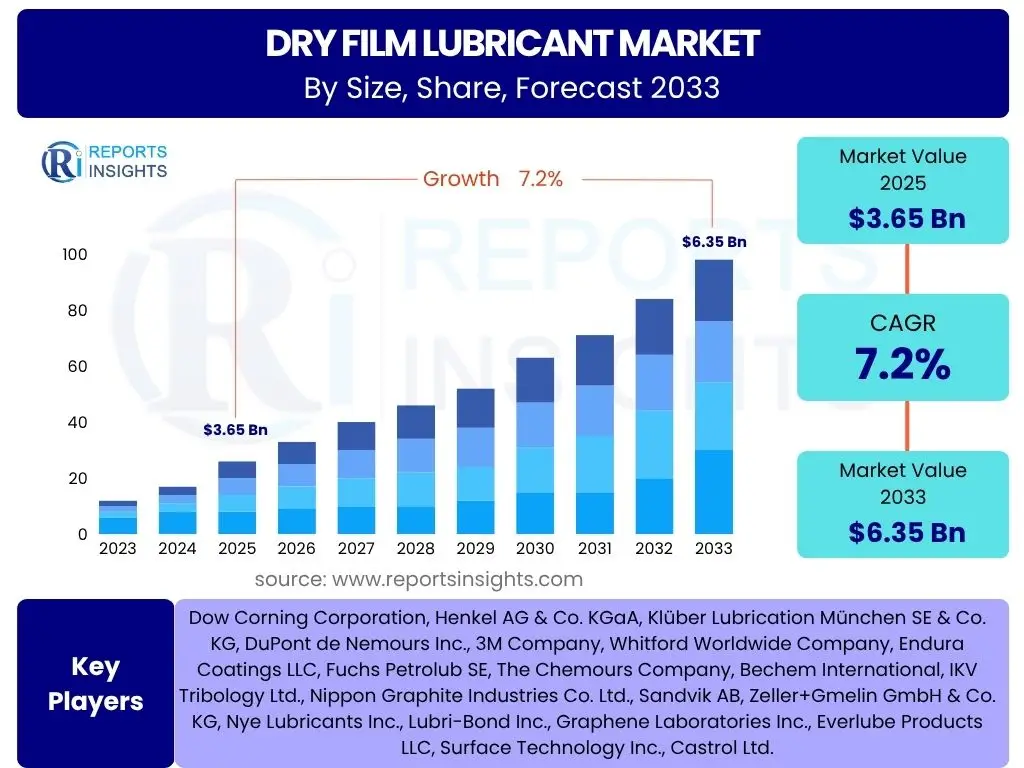

Dry Film Lubricant Market Size

According to Reports Insights Consulting Pvt Ltd, The Dry Film Lubricant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 3.65 Billion in 2025 and is projected to reach USD 6.35 Billion by the end of the forecast period in 2033.

Key Dry Film Lubricant Market Trends & Insights

Common user inquiries about the Dry Film Lubricant market frequently center on evolving material compositions, application technologies, and industry adoption patterns. The market is currently undergoing a significant transformation driven by advancements in material science, leading to the development of enhanced formulations that offer superior performance under extreme conditions. Furthermore, the push towards sustainable manufacturing practices and stricter environmental regulations is influencing a shift towards eco-friendly and solvent-free dry film lubricant solutions.

Another prominent trend involves the increasing integration of dry film lubricants in specialized applications such as electric vehicles, medical devices, and aerospace components, where traditional wet lubricants may not be suitable due to contamination risks, extreme temperatures, or vacuum environments. The demand for lightweight materials in various industries also directly impacts the adoption of dry film lubricants, as they provide effective friction and wear reduction without adding significant weight. This indicates a market that is not only expanding in volume but also diversifying in application and technological sophistication.

- Development of advanced composite and nano-material based dry film lubricants offering enhanced durability and performance.

- Increasing demand for environmentally friendly and REACH-compliant dry film lubricant formulations.

- Growing adoption in electric vehicle (EV) manufacturing for quiet operation and extended component life.

- Miniaturization of electronic components driving demand for ultra-thin, precise dry film applications.

- Expansion of additive manufacturing (3D printing) requiring specialized dry film lubricants for moving parts.

AI Impact Analysis on Dry Film Lubricant

User queries regarding the impact of AI on the Dry Film Lubricant market predominantly focus on how artificial intelligence can optimize material discovery, enhance application precision, and improve predictive maintenance strategies. There is significant interest in AI's potential to accelerate the development of novel dry film formulations by simulating molecular interactions and predicting performance characteristics, thereby reducing traditional R&D cycles. Furthermore, users are curious about AI-driven automation in the application processes, aiming for higher consistency and reduced waste.

Another key area of concern and expectation revolves around AI's role in quality control and in-service performance monitoring. Users anticipate that AI algorithms can analyze real-time operational data from components treated with dry film lubricants to predict wear patterns, optimize re-lubrication schedules, and identify potential failures before they occur. This shift towards data-driven lubrication management represents a significant leap from traditional maintenance practices, promising improved operational efficiency and extended component lifespan across various industrial sectors.

- AI-driven material discovery and formulation optimization, accelerating new product development.

- Enhanced quality control through AI-powered image processing and defect detection during application.

- Predictive maintenance analytics for components utilizing dry film lubricants, optimizing re-application schedules.

- Automated robotic application systems integrated with AI for precise and uniform coating thickness.

- Supply chain optimization for raw materials and finished products using AI forecasting and logistics management.

Key Takeaways Dry Film Lubricant Market Size & Forecast

Common user questions regarding key takeaways from the Dry Film Lubricant market size and forecast reveal a strong interest in understanding the primary growth drivers, the resilience of the market against potential restraints, and the emerging opportunities that will shape its future trajectory. Users are keen to identify the industries most poised for dry film lubricant adoption and the technological advancements underpinning the projected market expansion. The core insight sought is how sustainable this growth is and what factors will contribute most significantly to its continued upward trend.

The forecast suggests a robust expansion driven by increasing demand for high-performance, maintenance-free lubrication solutions in specialized and harsh operating environments. Key takeaways highlight the critical role of material innovation and application technology in meeting diverse industry needs, from aerospace and automotive to medical devices and industrial machinery. The market's resilience is further supported by its ability to address challenges like environmental regulations through the development of eco-friendly formulations, positioning dry film lubricants as an indispensable component in advanced engineering applications.

- The Dry Film Lubricant market is poised for substantial growth, driven by increasing industrialization and specialized application demands.

- Technological advancements in material science and application methods are crucial enablers for market expansion.

- Automotive, aerospace, and industrial machinery sectors remain primary demand drivers for dry film lubricants.

- The market is adapting to environmental regulations by focusing on sustainable and non-toxic formulations.

- Opportunities in emerging sectors like electric vehicles and additive manufacturing are significant for long-term growth.

Dry Film Lubricant Market Drivers Analysis

The dry film lubricant market is significantly propelled by the escalating demand for high-performance materials in extreme operating conditions across various industries. Traditional liquid lubricants often fail under high temperatures, vacuum environments, or heavy loads, creating a clear void that dry film lubricants effectively fill. Industries such as aerospace, defense, and high-performance automotive continually seek solutions that can provide lubrication without the risk of contamination, leakage, or degradation inherent to wet lubricants, thus driving adoption of dry films.

Furthermore, the global push towards lightweighting in automotive and aerospace sectors to improve fuel efficiency and reduce emissions is a critical driver. Dry film lubricants contribute to this by enabling the use of lighter materials that might otherwise be prone to excessive wear and friction. The increasing complexity and miniaturization of electronic and medical devices also necessitate precise, non-migratory lubrication solutions, where dry film lubricants offer distinct advantages over traditional alternatives. Stringent environmental regulations encouraging cleaner manufacturing processes further bolster the demand for solvent-free and low-VOC dry film solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand in Aerospace & Defense | +1.5% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Adoption in Automotive Sector (EVs) | +1.2% | Asia Pacific, Europe, North America | Mid-to-Long-term (2026-2033) |

| Need for High-Performance in Extreme Conditions | +0.8% | Global | Ongoing (2025-2033) |

| Miniaturization of Components | +0.7% | Asia Pacific, Europe | Mid-term (2025-2029) |

| Stringent Environmental Regulations | +0.6% | Europe, North America | Ongoing (2025-2033) |

Dry Film Lubricant Market Restraints Analysis

Despite significant growth prospects, the dry film lubricant market faces several restraints that could temper its expansion. One primary challenge is the higher initial application cost associated with dry film lubricants compared to conventional wet lubricants. The specialized equipment and skilled labor required for precise application processes, such as vapor deposition or sputtering, can deter smaller manufacturers or those with limited capital investment capabilities from adopting these advanced solutions. This cost barrier is particularly prominent in price-sensitive markets or industries where the long-term benefits might not immediately outweigh the upfront expenditure.

Another significant restraint is the difficulty or impossibility of re-lubrication for many dry film applications. Once applied, these films are often designed to last for the component's lifetime, but if the film is damaged or wears out prematurely, reapplication can be complex, costly, or simply not feasible for certain sealed or intricate parts. This limitation can make end-users hesitant to commit to dry film solutions, especially in applications where regular maintenance and re-lubrication are standard practice. Furthermore, a general lack of awareness regarding the specific advantages and appropriate applications of dry film lubricants among potential users, particularly in less specialized industrial sectors, continues to act as a market impediment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Application Cost | -0.9% | Global, particularly SMEs | Ongoing (2025-2033) |

| Limited Re-lubrication Capabilities | -0.7% | Global | Long-term (2025-2033) |

| Competition from Traditional Lubricants | -0.5% | Emerging Economies | Mid-term (2025-2029) |

| Application Complexity and Expertise Required | -0.4% | Global | Ongoing (2025-2033) |

Dry Film Lubricant Market Opportunities Analysis

The dry film lubricant market is presented with significant opportunities stemming from the rapid evolution of several key industries. The burgeoning electric vehicle (EV) market, for instance, offers a substantial growth avenue. EVs demand quiet, efficient, and maintenance-free components, where dry film lubricants can prevent noise from braking systems, reduce friction in power electronics, and enhance the longevity of various moving parts without contamination risk, unlike traditional liquid lubricants that can interfere with electrical systems. This emerging sector is poised to drive considerable demand for specialized dry film solutions.

Another compelling opportunity lies within the medical device manufacturing sector. The need for biocompatible, sterile, and precisely lubricated components in surgical tools, implants, and diagnostic equipment creates a niche where dry film lubricants excel due to their cleanliness and ability to operate without attracting particles. Similarly, the expanding landscape of additive manufacturing (3D printing) requires novel lubrication strategies for complex geometries and moving assemblies that are difficult to access for traditional lubrication. Dry film lubricants can be integrated during or post-printing, offering innovative solutions for these intricate applications. The increasing focus on renewable energy, particularly wind turbines and solar tracking systems, also presents opportunities, as these applications require durable, low-maintenance lubrication for components exposed to harsh environmental conditions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicle (EV) Manufacturing | +1.8% | Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Expanding Medical Devices Sector | +1.0% | North America, Europe | Mid-to-Long-term (2026-2033) |

| Integration with Additive Manufacturing (3D Printing) | +0.9% | Global | Long-term (2027-2033) |

| Demand from Renewable Energy Sector | +0.7% | Europe, North America, Asia Pacific | Mid-to-Long-term (2026-2033) |

| Development of Niche High-Value Applications | +0.5% | Global | Ongoing (2025-2033) |

Dry Film Lubricant Market Challenges Impact Analysis

The dry film lubricant market faces several inherent challenges that demand continuous innovation and strategic adaptation. One significant challenge is the ongoing need to develop new formulations that can perform reliably under increasingly extreme and diverse operating conditions. As industries push for higher temperatures, greater loads, and more aggressive chemical environments, existing dry film technologies may fall short, necessitating extensive research and development into novel materials and application techniques. Ensuring consistent, long-term durability and predictable wear life across various substrates and environmental factors remains a complex engineering hurdle.

Another key challenge involves the complexity and cost associated with achieving uniform film thickness and adhesion, especially on intricate geometries or large surfaces. The specialized application equipment and controlled environmental conditions required for optimal deposition can be a barrier for wider adoption. Furthermore, regulatory compliance, particularly regarding the use of certain chemicals and their environmental impact, presents an ongoing challenge. Manufacturers must navigate a complex web of regional and international regulations (e.g., REACH in Europe, EPA in the U.S.) while simultaneously meeting performance demands, driving the need for continuous formulation adjustments towards safer, more sustainable alternatives without compromising performance. Educating the market about the distinct advantages and proper implementation of dry film lubricants also remains a significant hurdle.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Developing Formulations for Extreme Conditions | -0.8% | Global | Ongoing (2025-2033) |

| Achieving Uniform Film Thickness & Adhesion | -0.6% | Global | Ongoing (2025-2033) |

| Navigating Stringent Regulatory Compliance | -0.5% | Europe, North America | Ongoing (2025-2033) |

| Educating End-Users on Application & Benefits | -0.3% | Emerging Economies | Long-term (2025-2033) |

Dry Film Lubricant Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Dry Film Lubricant Market, covering historical data from 2019 to 2023, with detailed market size estimations for 2025 and projections up to 2033. It offers insights into key market trends, growth drivers, restraints, opportunities, and challenges influencing market dynamics. The study segments the market by type, end-use industry, application method, and form, providing regional and country-level analysis to offer a holistic view of the market landscape. Competitive intelligence on leading players and their strategic initiatives is also included.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.65 Billion |

| Market Forecast in 2033 | USD 6.35 Billion |

| Growth Rate | 7.2% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Dow Corning Corporation, Henkel AG & Co. KGaA, Klüber Lubrication München SE & Co. KG, DuPont de Nemours Inc., 3M Company, Whitford Worldwide Company, Endura Coatings LLC, Fuchs Petrolub SE, The Chemours Company, Bechem International, IKV Tribology Ltd., Nippon Graphite Industries Co. Ltd., Sandvik AB, Zeller+Gmelin GmbH & Co. KG, Nye Lubricants Inc., Lubri-Bond Inc., Graphene Laboratories Inc., Everlube Products LLC, Surface Technology Inc., Castrol Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Dry Film Lubricant market is meticulously segmented to provide a granular understanding of its diverse applications and material compositions. This segmentation allows for targeted analysis of specific market niches, identifying areas of high growth and emerging demand. The classification by type focuses on the chemical composition of the lubricants, highlighting the prevalence and performance characteristics of each material, while end-use industry segmentation sheds light on the primary sectors driving adoption. Application method analysis details the various techniques employed for deposition, reflecting technological advancements and industry practices.

Further segmentation by form provides insights into the commercial presentation and usability of these lubricants, catering to different operational requirements. Each segment plays a crucial role in the overall market dynamics, with interdependencies driving innovation and competition. Understanding these distinct segments is essential for stakeholders to develop tailored strategies, optimize product portfolios, and effectively capitalize on market opportunities.

- By Type: Molybdenum Disulfide (MoS2), Graphite, Polytetrafluoroethylene (PTFE), Tungsten Disulfide (WS2), Diamond-like Carbon (DLC), Other Types (Silanes, Boron Nitride).

- By End-Use Industry: Automotive (Passenger Cars, Commercial Vehicles, Electric Vehicles), Aerospace & Defense, Industrial Machinery & Manufacturing, Medical Devices, Electronics & Semiconductors, Consumer Goods, Energy (Oil & Gas, Wind), Others.

- By Application Method: Spray Coating, Dip Coating, Roll Coating, Powder Coating, Sputtering, Electroplating, Vapor Deposition.

- By Form: Liquid Dispersion, Powder, Grease, Aerosol.

Regional Highlights

- North America: This region represents a mature yet continually innovating market for dry film lubricants, driven by robust aerospace and defense sectors, alongside significant advancements in automotive electrification. The United States and Canada are leading the adoption of high-performance dry film solutions for demanding applications, including satellites, aircraft components, and advanced manufacturing processes. Strict regulatory frameworks regarding environmental impact also encourage the development and use of eco-friendly dry film variants. The presence of key industry players and a strong R&D infrastructure further solidifies North America's position as a vital market for dry film lubricants.

- Europe: Europe is a key market propelled by its strong automotive industry, particularly the transition towards electric vehicles, and a burgeoning industrial machinery sector. Countries like Germany, France, and the UK are at the forefront of adopting dry film lubricants for precision engineering, robotics, and renewable energy applications. The region's stringent environmental regulations, such as REACH, significantly influence product development, fostering innovation in sustainable and non-toxic dry film formulations. Continuous investment in research and development, coupled with a focus on enhancing efficiency and durability in industrial processes, further contributes to the market's growth in Europe.

- Asia Pacific (APAC): The Asia Pacific region is anticipated to exhibit the highest growth rate in the dry film lubricant market due to rapid industrialization, expanding manufacturing bases, and significant investments in automotive production, particularly in China, India, Japan, and South Korea. The burgeoning electronics industry, coupled with increasing demand for consumer goods and machinery, drives the need for advanced lubrication solutions. Government initiatives supporting manufacturing and infrastructure development, alongside a growing focus on electric vehicles, provide substantial opportunities for market expansion. The sheer scale of industrial output across diverse sectors in APAC makes it a critical region for dry film lubricant manufacturers.

- Latin America: The Latin American market for dry film lubricants is experiencing gradual growth, primarily driven by industrial expansion, particularly in countries like Brazil and Mexico. The automotive sector, alongside mining and heavy machinery industries, represents key demand areas. While still developing compared to other regions, increasing foreign direct investment in manufacturing and infrastructure projects is expected to fuel the adoption of advanced lubrication technologies, including dry films. The growing awareness regarding the benefits of dry film lubricants for enhanced operational efficiency and component longevity is contributing to market penetration in the region.

- Middle East and Africa (MEA): The MEA region presents emerging opportunities for the dry film lubricant market, largely influenced by investments in infrastructure, manufacturing, and diversification away from oil-dependent economies. Countries in the GCC region are investing in industrial and technological advancements, creating demand for specialized lubricants in sectors such as aerospace, defense, and power generation. The challenging environmental conditions, including high temperatures and dusty environments, make dry film lubricants an attractive solution for critical equipment. As industrialization continues and awareness of advanced lubrication solutions increases, the MEA market is projected to witness steady growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Dry Film Lubricant Market.- Dow Corning Corporation

- Henkel AG & Co. KGaA

- Klüber Lubrication München SE & Co. KG

- DuPont de Nemours Inc.

- 3M Company

- Whitford Worldwide Company

- Endura Coatings LLC

- Fuchs Petrolub SE

- The Chemours Company

- Bechem International

- IKV Tribology Ltd.

- Nippon Graphite Industries Co. Ltd.

- Sandvik AB

- Zeller+Gmelin GmbH & Co. KG

- Nye Lubricants Inc.

- Lubri-Bond Inc.

- Graphene Laboratories Inc.

- Everlube Products LLC

- Surface Technology Inc.

- Castrol Ltd.

Frequently Asked Questions

Analyze common user questions about the Dry Film Lubricant market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are dry film lubricants and their primary uses?

Dry film lubricants are solid lubricants applied as thin coatings to surfaces to reduce friction and wear. They are primarily used in applications where traditional wet lubricants are unsuitable, such as extreme temperatures, vacuum environments, high loads, cleanroom conditions, or for long-lasting, maintenance-free lubrication in industries like aerospace, automotive, and medical devices.

What advantages do dry film lubricants offer over traditional wet lubricants?

Dry film lubricants offer several advantages, including operation in extreme temperatures (both high and low), prevention of contamination (no oil mist or residue), resistance to dust and dirt adhesion, suitability for vacuum environments, clean and non-migratory application, and providing long-term lubrication for sealed or inaccessible components without frequent reapplication.

Which industries are the major consumers of dry film lubricants?

The primary industries consuming dry film lubricants include aerospace and defense for aircraft and satellite components, the automotive sector for engine parts and electric vehicle components, industrial machinery for gears and bearings, medical devices for surgical instruments and implants, and electronics for miniature components requiring precise lubrication.

What are the key types of materials used in dry film lubricants?

Common materials used in dry film lubricants include Molybdenum Disulfide (MoS2), Graphite, Polytetrafluoroethylene (PTFE), Tungsten Disulfide (WS2), and Diamond-like Carbon (DLC). Each material offers distinct tribological properties and is chosen based on specific application requirements like load, temperature, and chemical compatibility.

How do environmental regulations impact the dry film lubricant market?

Environmental regulations significantly impact the dry film lubricant market by driving the demand for eco-friendly, solvent-free, and low-VOC (Volatile Organic Compound) formulations. Manufacturers are increasingly focusing on developing sustainable alternatives to comply with strict norms like REACH in Europe and similar regulations globally, influencing product innovation and market shifts.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted