Drag Chain Cable Market

Drag Chain Cable Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701276 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

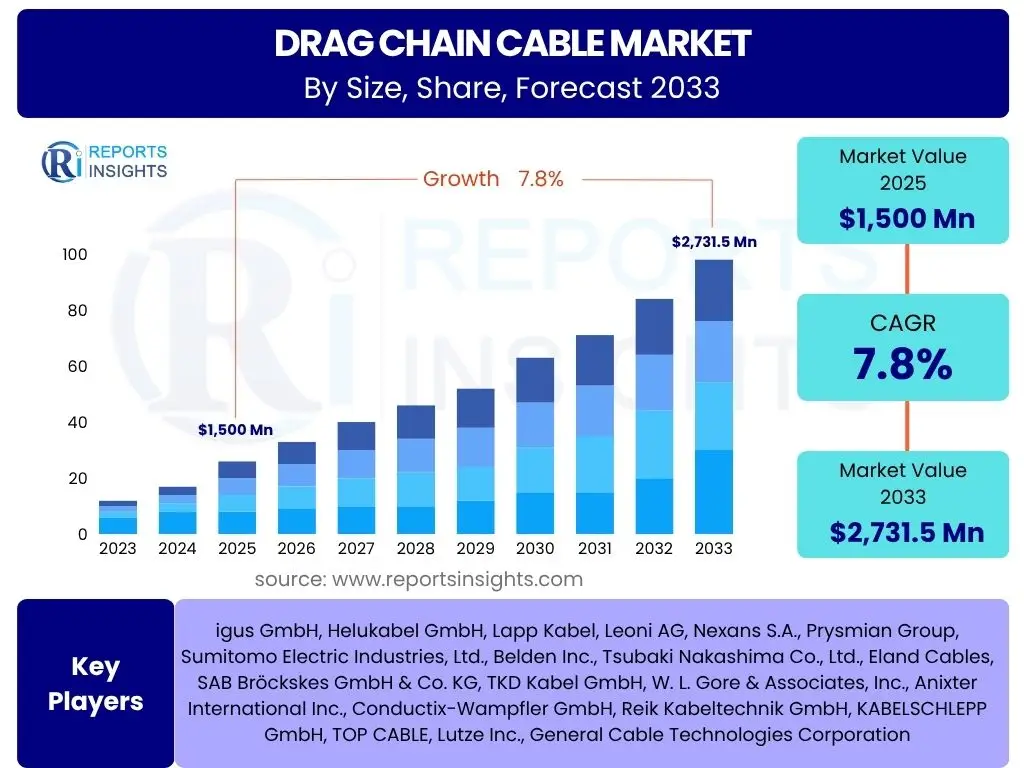

Drag Chain Cable Market Size

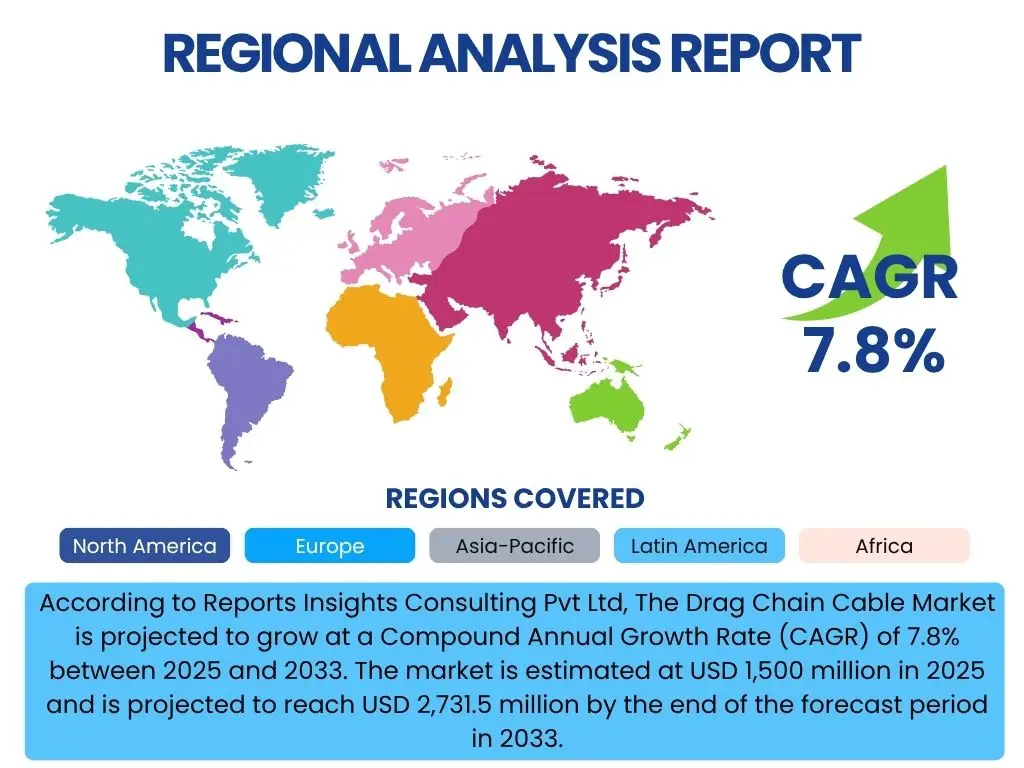

According to Reports Insights Consulting Pvt Ltd, The Drag Chain Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1,500 million in 2025 and is projected to reach USD 2,731.5 million by the end of the forecast period in 2033.

Key Drag Chain Cable Market Trends & Insights

The drag chain cable market is witnessing significant transformation driven by advancements in industrial automation and the proliferation of smart manufacturing paradigms. A key trend involves the increasing demand for highly flexible and durable cables capable of withstanding continuous motion and harsh industrial environments. Users frequently inquire about the integration of these cables into high-speed, dynamic applications, alongside developments in materials science that enhance cable longevity and performance. The shift towards miniaturization in robotics and automation equipment also influences cable design, leading to thinner, lighter, yet robust solutions. Furthermore, there is a growing emphasis on energy efficiency and data transmission capabilities, prompting innovation in hybrid cable designs that combine power and signal lines.

Another prominent trend is the rising adoption of Industry 4.0 principles, which necessitates cables with enhanced data transfer capabilities and compatibility with various communication protocols. The demand for customized drag chain cables, tailored to specific application requirements such as resistance to chemicals, oils, or extreme temperatures, is also on the rise. Stakeholders are keen to understand how manufacturers are addressing the need for reduced downtime and extended service life through superior cable engineering and predictive maintenance integration. The market is also observing a gradual shift towards halogen-free and eco-friendly cable solutions, reflecting growing environmental consciousness and stricter regulatory frameworks globally. These trends collectively underscore a market moving towards higher performance, greater customization, and improved sustainability.

- Increased adoption of industrial automation and robotics across diverse sectors.

- Growing demand for high-flexibility, durable, and compact cable designs.

- Integration of advanced materials for enhanced chemical, temperature, and abrasion resistance.

- Rising prevalence of hybrid cables combining power, data, and fiber optic lines.

- Emphasis on energy-efficient and eco-friendly (halogen-free) cable solutions.

- Expansion of Industry 4.0 and smart factory initiatives driving demand for intelligent cables.

- Development of application-specific and customized cable solutions for specialized machinery.

AI Impact Analysis on Drag Chain Cable

The influence of Artificial Intelligence (AI) on the drag chain cable market is multifaceted, primarily impacting manufacturing processes, predictive maintenance, and operational efficiencies. Common user inquiries revolve around how AI can optimize cable design, enhance quality control, and integrate with smart monitoring systems to prevent failures. AI-driven algorithms are increasingly being utilized in the design phase to simulate cable performance under various stress conditions, allowing manufacturers to optimize material composition, conductor geometry, and insulation properties for superior durability and flexibility. This leads to reduced prototyping costs and faster time-to-market for new cable innovations.

Beyond design, AI plays a crucial role in predictive maintenance for industrial systems where drag chain cables are extensively used. By analyzing real-time data from sensors embedded in machinery or the cables themselves, AI can detect subtle anomalies or signs of wear, predicting potential cable failures before they occur. This capability significantly reduces unscheduled downtime, lowers maintenance costs, and extends the operational life of equipment, directly benefiting end-users. Furthermore, AI-powered automation in cable manufacturing facilities can optimize production lines, improve quality consistency, and minimize waste, enhancing the overall efficiency and competitiveness of cable producers. The integration of AI therefore transforms the entire lifecycle of drag chain cables, from conceptualization to operational deployment and maintenance.

- Optimization of cable design through AI-driven simulation and material analysis.

- Enhanced quality control and defect detection in manufacturing processes using AI vision systems.

- Implementation of AI for predictive maintenance in industrial automation systems using drag chain cables.

- Improved operational efficiency and reduced downtime in manufacturing environments.

- Development of smart cables with integrated sensors for real-time performance monitoring and AI analysis.

Key Takeaways Drag Chain Cable Market Size & Forecast

Key insights from the drag chain cable market size and forecast data underscore a robust growth trajectory, primarily fueled by the accelerating pace of industrial automation and the global expansion of manufacturing capabilities. A significant takeaway is the consistent demand for high-performance and resilient cable solutions that can withstand the rigorous demands of continuous motion in diverse industrial applications. The market's projected expansion signifies continued investment in advanced machinery and robotic systems across sectors like automotive, manufacturing, and material handling, which are primary consumers of these specialized cables.

Furthermore, the forecast highlights the critical role of technological advancements in material science and intelligent system integration in sustaining market momentum. As industries increasingly adopt Industry 4.0 principles and smart factory concepts, the need for cables that not only transmit power and data reliably but also offer features like extended lifespan and enhanced environmental resistance will intensify. Stakeholders should recognize the imperative to innovate in cable design, focusing on customization and sustainability, to capitalize on emerging opportunities and maintain competitive advantage in this evolving market landscape. The market trajectory indicates a clear shift towards higher value, application-specific solutions.

- The market is poised for significant growth, driven by pervasive industrial automation and robotics adoption.

- Demand for highly durable, flexible, and reliable cables will continue to escalate across key industries.

- Technological innovation in cable materials and design is crucial for meeting evolving application requirements.

- Customization and application-specific solutions represent key growth avenues for manufacturers.

- Predictive maintenance and smart factory integration are becoming increasingly vital for end-users.

- Asia Pacific is expected to remain a dominant region due to expanding manufacturing bases and infrastructure.

Drag Chain Cable Market Drivers Analysis

The drag chain cable market is primarily propelled by the burgeoning growth in industrial automation and the widespread adoption of robotics across various manufacturing and processing sectors. As industries strive for increased efficiency, precision, and productivity, the deployment of automated machinery, including articulated robots, CNC machines, and automated guided vehicles (AGVs), has become indispensable. These systems heavily rely on specialized drag chain cables to reliably transmit power, data, and signals while accommodating continuous flexural movements within cable carriers. This fundamental shift towards automation acts as a core impetus for market expansion.

Another significant driver is the global emphasis on smart factories and Industry 4.0 initiatives. The implementation of interconnected systems, real-time data exchange, and advanced analytics in manufacturing environments necessitates robust and intelligent cabling infrastructure. Drag chain cables, especially those integrated with communication protocols and capable of high-speed data transmission, are critical components in these sophisticated setups. Furthermore, the expansion of industries such as automotive, aerospace, packaging, and material handling, which are undergoing modernization and automation drives, directly translates into increased demand for these high-performance cables, reinforcing the market's growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Industrial Automation & Robotics | +2.5% | Global, particularly Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Rise of Industry 4.0 & Smart Manufacturing | +1.8% | Europe, North America, Japan, China | Mid to Long-term (2025-2033) |

| Increasing Demand for High-Performance Machinery | +1.5% | Global, especially Germany, USA, China | Mid-term (2025-2030) |

| Expansion of Electric Vehicle (EV) Manufacturing | +0.8% | China, Germany, USA, South Korea | Mid to Long-term (2026-2033) |

Drag Chain Cable Market Restraints Analysis

Despite the positive growth outlook, the drag chain cable market faces certain restraints that could impede its full potential. One primary constraint is the relatively high initial investment associated with premium drag chain cable systems. These specialized cables, designed for extreme durability and flexibility, often utilize advanced materials and complex manufacturing processes, resulting in a higher per-unit cost compared to conventional static cables. This cost factor can be a barrier for small and medium-sized enterprises (SMEs) or budget-constrained projects, potentially leading them to opt for less optimal, albeit cheaper, alternatives, which may compromise long-term performance and reliability.

Another significant restraint is the volatility in raw material prices, particularly for copper, PVC, PUR, and other polymer compounds essential for cable manufacturing. Fluctuations in these commodity prices can directly impact the production costs of drag chain cables, leading to unstable pricing for end-users and reduced profit margins for manufacturers. This unpredictability makes long-term planning and fixed-price contracts challenging. Additionally, the availability of alternative wireless communication technologies for certain applications, though not fully replacing physical cables for power transmission, could marginally restrain growth in specific data-only scenarios. These factors necessitate strategic management of supply chains and cost optimization efforts by market players to mitigate their impact.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Cost | -0.7% | Global, particularly emerging markets | Long-term (2025-2033) |

| Volatility in Raw Material Prices | -0.5% | Global, especially Asia Pacific, Europe | Mid-term (2025-2030) |

| Lack of Standardization in Niche Applications | -0.3% | Europe, North America | Short to Mid-term (2025-2028) |

| Competition from Wireless Technologies (for data) | -0.2% | Global, primarily advanced industrial sectors | Long-term (2028-2033) |

Drag Chain Cable Market Opportunities Analysis

Significant opportunities in the drag chain cable market arise from the expanding applications in emerging industries and the increasing demand for highly customized solutions. As new manufacturing processes and automation needs emerge, particularly in specialized fields like medical devices, aerospace, and renewable energy, there is a growing requirement for cables designed to meet unique environmental and performance specifications. This includes cables that can operate reliably in cleanroom environments, withstand extreme temperatures, or offer specific chemical resistance. The ability of manufacturers to provide bespoke cable solutions tailored to these niche applications presents a substantial avenue for market growth and differentiation.

Furthermore, the rapid industrialization and infrastructure development in emerging economies, particularly in Asia Pacific and parts of Latin America, offer immense untapped potential. As these regions increasingly adopt advanced manufacturing techniques and invest in automation technologies, the demand for sophisticated drag chain cables will surge. Companies that strategically expand their distribution networks, establish local manufacturing capabilities, and adapt their product offerings to regional market needs can capture significant market share. Additionally, continuous advancements in material science, leading to the development of lighter, more flexible, and even self-healing cable materials, present opportunities for innovation and the creation of next-generation products with enhanced performance characteristics.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets & Industries | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Development of Application-Specific & Custom Cables | +1.0% | Global | Mid to Long-term (2025-2033) |

| Advancements in Material Science & Hybrid Designs | +0.8% | Global, particularly developed economies | Mid-term (2025-2030) |

| Integration with Predictive Maintenance Solutions | +0.7% | North America, Europe, Japan | Mid to Long-term (2026-2033) |

Drag Chain Cable Market Challenges Impact Analysis

The drag chain cable market faces several challenges that can affect its growth and operational efficiency. One significant challenge is the intense competition and price pressure from a multitude of global and regional players. The market is fragmented, with numerous manufacturers offering similar products, leading to aggressive pricing strategies that can erode profit margins, especially for smaller companies. Maintaining a competitive edge requires continuous investment in research and development to differentiate products through superior performance, longevity, or unique features, which can be resource-intensive.

Another critical challenge involves the complexities associated with global supply chain disruptions. Geopolitical tensions, natural disasters, and global health crises can severely impact the availability of raw materials and components, leading to production delays and increased costs. Manufacturers must develop robust and diversified supply chain strategies to mitigate these risks. Furthermore, ensuring high-quality standards and combating the proliferation of counterfeit or substandard cables poses a significant challenge. Inferior products can lead to frequent breakdowns, safety hazards, and damage the reputation of legitimate manufacturers, requiring stringent quality control measures and active market monitoring to protect brand integrity and customer trust.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Price Pressure | -0.6% | Global, particularly Asia Pacific | Long-term (2025-2033) |

| Supply Chain Disruptions & Material Shortages | -0.4% | Global | Short to Mid-term (2025-2028) |

| Technical Complexities for High-Performance Needs | -0.3% | Global, particularly specialized applications | Mid-term (2025-2030) |

| Counterfeit Products & Quality Assurance | -0.2% | Emerging Markets | Long-term (2025-2033) |

Drag Chain Cable Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Drag Chain Cable Market, offering a detailed assessment of market size, growth drivers, restraints, opportunities, and challenges across various segments and geographical regions. It includes historical data from 2019-2023 and provides forecasts up to 2033, enabling stakeholders to gain a holistic understanding of market dynamics and future growth prospects. The report also highlights key trends shaping the industry and profiles leading market players, offering valuable strategic insights for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1,500 million |

| Market Forecast in 2033 | USD 2,731.5 million |

| Growth Rate | 7.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | igus GmbH, Helukabel GmbH, Lapp Kabel, Leoni AG, Nexans S.A., Prysmian Group, Sumitomo Electric Industries, Ltd., Belden Inc., Tsubaki Nakashima Co., Ltd., Eland Cables, SAB Bröckskes GmbH & Co. KG, TKD Kabel GmbH, W. L. Gore & Associates, Inc., Anixter International Inc., Conductix-Wampfler GmbH, Reik Kabeltechnik GmbH, KABELSCHLEPP GmbH, TOP CABLE, Lutze Inc., General Cable Technologies Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The drag chain cable market is extensively segmented to provide a granular understanding of its diverse applications and product types, allowing for precise market analysis and strategic planning. These segmentations highlight the varied demands across different industrial environments and technological requirements. Understanding these segments is crucial for manufacturers to tailor their product offerings and for end-users to select the most appropriate cable solutions for their specific operational needs, ranging from standard industrial use to highly specialized and demanding applications.

Each segment, whether defined by cable material, core configuration, or end-use application, represents distinct market dynamics and growth drivers. For instance, the demand for TPE and PUR cables is surging due to their superior performance in harsh environments, while hybrid cables are gaining traction for their ability to consolidate multiple functions. Analyzing these segments helps identify high-growth areas and provides insights into technological preferences and regional consumption patterns, underpinning the comprehensive market overview presented in this report.

- By Cable Type: Includes PVC Cables, PUR Cables, TPE Cables, Halogen-Free Cables, and Other Material Cables, reflecting varied material properties and application suitability.

- By Core Type: Categorized into Single-Core Cables, Multi-Core Cables, Coaxial Cables, Fiber Optic Cables, and Hybrid Cables, distinguishing by conductor configuration and data transmission capabilities.

- By Application: Encompasses Industrial Automation & Robotics, Machine Tools, Material Handling Equipment, Cranes & Conveyors, Automotive Manufacturing, Packaging Machinery, Cleanroom Applications, Medical Equipment, Wind Turbines, and Other Industrial Applications, showcasing diverse end-uses.

- By End-Use Industry: Covers Manufacturing, Automotive, Aerospace & Defense, Food & Beverage, Pharmaceuticals, Energy & Utilities, Mining, Construction, and Other Industries, indicating the broad industry penetration.

Regional Highlights

The global drag chain cable market exhibits distinct regional dynamics, with certain geographies playing a pivotal role in market growth and technological adoption. Asia Pacific is anticipated to remain the dominant region due to its expansive manufacturing base, rapid industrialization, and significant investments in automation and robotics, particularly in countries like China, Japan, and South Korea. The region's robust automotive, electronics, and machinery industries are primary contributors to the high demand for drag chain cables.

Europe is another crucial market, driven by advanced manufacturing capabilities, strong emphasis on Industry 4.0, and a mature automation sector, with Germany leading the way in machine tools and industrial robotics. North America also represents a substantial market, characterized by technological innovation, increasing adoption of automation across diverse sectors including aerospace and defense, and a focus on upgrading existing manufacturing infrastructure. Latin America, the Middle East, and Africa are emerging markets, showing promising growth potential as they progressively adopt industrial automation solutions and invest in infrastructure development, albeit at a slower pace compared to developed regions.

- Asia Pacific (APAC): Dominant market due to rapid industrialization, extensive manufacturing activities, and significant adoption of robotics and automation, led by China, Japan, and South Korea.

- Europe: Strong market driven by advanced manufacturing capabilities, focus on Industry 4.0, and high demand from the automotive and machine tool industries, with Germany as a key contributor.

- North America: Robust market with high technological adoption, ongoing industrial modernization, and demand from diverse sectors including automotive, aerospace, and general manufacturing, prominently in the United States.

- Latin America (LATAM): Emerging market with growing industrial automation needs and increasing investments in manufacturing infrastructure, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Gradually expanding market driven by infrastructure development projects, diversification of economies, and growing interest in industrial automation, albeit from a lower base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Drag Chain Cable Market.- igus GmbH

- Helukabel GmbH

- Lapp Kabel

- Leoni AG

- Nexans S.A.

- Prysmian Group

- Sumitomo Electric Industries, Ltd.

- Belden Inc.

- Tsubaki Nakashima Co., Ltd.

- Eland Cables

- SAB Bröckskes GmbH & Co. KG

- TKD Kabel GmbH

- W. L. Gore & Associates, Inc.

- Anixter International Inc.

- Conductix-Wampfler GmbH

- Reik Kabeltechnik GmbH

- KABELSCHLEPP GmbH

- TOP CABLE

- Lutze Inc.

- General Cable Technologies Corporation

Frequently Asked Questions

What is a drag chain cable and why is it essential?

A drag chain cable is a specialized electrical cable designed for continuous flexing applications within cable carriers (drag chains) in automated machinery. It is essential because it reliably transmits power, data, and signals while enduring constant bending, torsion, and environmental stresses, ensuring uninterrupted operation and longevity of dynamic industrial equipment like robots, CNC machines, and material handling systems.

Which industries primarily drive the demand for drag chain cables?

The primary industries driving the demand for drag chain cables include industrial automation and robotics, automotive manufacturing, machine tools, material handling, packaging, and renewable energy (e.g., wind turbines). These sectors heavily rely on automated processes that require durable and high-performance cables to withstand continuous motion and harsh operating conditions.

How do advancements in materials science impact the drag chain cable market?

Advancements in materials science significantly impact the drag chain cable market by enabling the development of cables with enhanced flexibility, durability, and resistance to environmental factors. New materials like advanced PUR (Polyurethane) and TPE (Thermoplastic Elastomers) offer superior abrasion, oil, chemical, and temperature resistance, extending cable lifespan and performance in demanding industrial applications.

What are the key factors contributing to the growth of the drag chain cable market?

Key factors contributing to the market's growth include the global surge in industrial automation and robotics adoption, the increasing integration of Industry 4.0 and smart manufacturing concepts, and the rising demand for high-performance and reliable components in advanced machinery across various sectors. The need for reduced downtime and enhanced operational efficiency also fuels demand.

What challenges do drag chain cable manufacturers face?

Drag chain cable manufacturers face challenges such as intense market competition leading to price pressure, volatility in raw material costs, the complexities of ensuring high-quality and consistent performance for diverse applications, and managing global supply chain disruptions. Additionally, combating counterfeit products and meeting evolving technical standards pose ongoing challenges.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted