District Heating and Cooling Market

District Heating and Cooling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700524 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

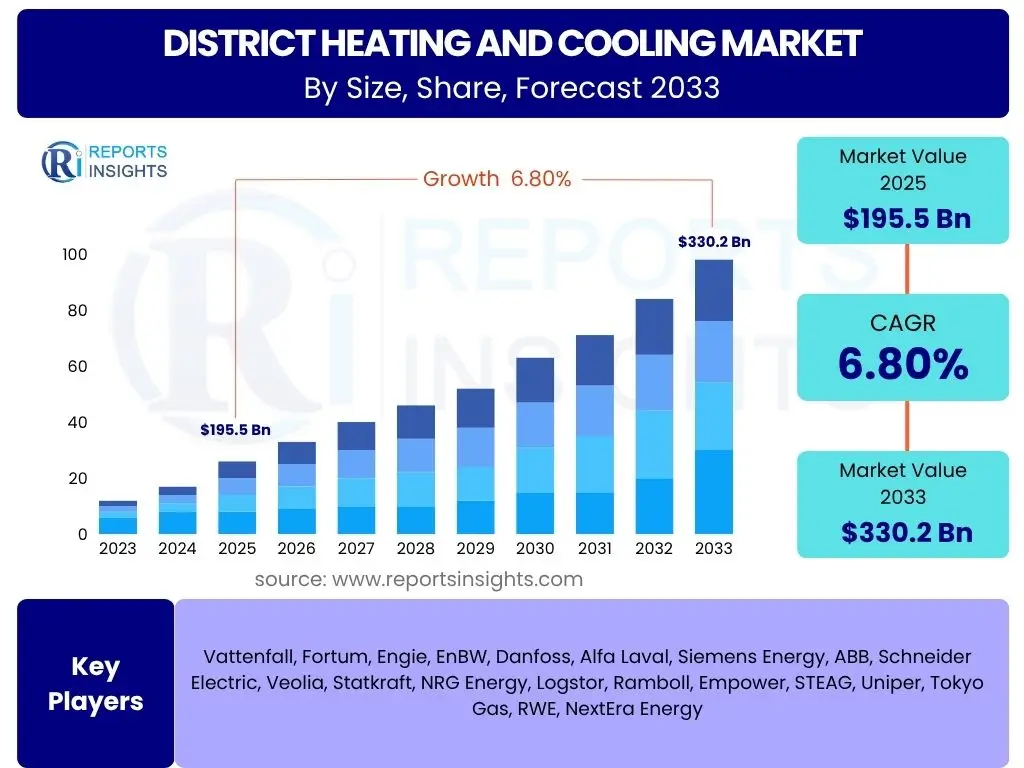

District Heating and Cooling Market Size

District Heating and Cooling Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, valued at USD 195.5 Billion in 2025 and is projected to grow by USD 330.2 Billion by 2033 the end of the forecast period.

Key District Heating and Cooling Market Trends & Insights

The District Heating and Cooling market is witnessing a transformative phase driven by global decarbonization efforts and technological advancements. Key trends include the integration of renewable energy sources, the adoption of smart grid technologies for optimized energy distribution, and the increasing focus on energy efficiency across urban landscapes. The shift towards circular economy principles is also promoting the utilization of waste heat and industrial excess heat, further bolstering the market's growth trajectory. These developments are not only enhancing the sustainability of energy systems but also improving their economic viability and operational resilience.

- Decarbonization and Net-Zero Goals: Aggressive targets set by governments and corporations to reduce carbon emissions are driving the adoption of district energy systems, which offer a collective and efficient pathway to sustainable heating and cooling.

- Integration of Renewable Energy: Increasing incorporation of solar thermal, geothermal, biomass, and heat pumps into district heating and cooling networks, diversifying energy sources and reducing reliance on fossil fuels.

- Smart Grid and Digitalization: Deployment of advanced control systems, IoT sensors, and data analytics for real-time monitoring, predictive maintenance, and optimized energy flow within district networks.

- Urbanization and Smart City Development: Rapid urban growth globally necessitates scalable and efficient energy infrastructure, positioning district heating and cooling as a core component of sustainable urban planning.

- Waste Heat Recovery: Growing emphasis on recovering and reusing waste heat from industrial processes, data centers, and commercial buildings, transforming energy efficiency into a valuable resource.

AI Impact Analysis on District Heating and Cooling

Artificial Intelligence (AI) is set to revolutionize the District Heating and Cooling market by introducing unprecedented levels of efficiency, predictive capabilities, and optimization. AI algorithms can analyze vast datasets from sensors, weather forecasts, and consumption patterns to precisely predict energy demand and optimize supply, minimizing waste and operational costs. This leads to more responsive and resilient district energy networks, capable of adapting to fluctuating conditions and integrating diverse energy sources seamlessly. The application of AI spans from enhancing system design and network management to enabling advanced fault detection and predictive maintenance, ultimately driving the market towards greater intelligence and sustainability.

- Predictive Maintenance: AI algorithms analyze operational data to forecast equipment failures, allowing for proactive maintenance and reducing downtime, thereby improving network reliability.

- Optimized Energy Distribution: AI-driven systems manage the flow of heat and cold within the network, optimizing distribution based on real-time demand and supply, leading to significant energy savings.

- Demand Forecasting: AI models accurately predict future heating and cooling demands by analyzing historical data, weather patterns, and occupant behavior, enabling more efficient energy generation and resource allocation.

- Smart Control Systems: AI empowers intelligent control systems that dynamically adjust parameters like temperature and flow rates to maintain optimal performance and respond to variations in demand or supply.

- Integration of Decentralized Energy Sources: AI facilitates the seamless integration and management of multiple decentralized energy sources, including renewables, ensuring grid stability and efficiency.

Key Takeaways District Heating and Cooling Market Size & Forecast

- The District Heating and Cooling market is projected for robust growth, driven by global sustainability mandates and urban development.

- Significant market expansion is anticipated, with the market value projected to reach USD 330.2 Billion by 2033 from USD 195.5 Billion in 2025.

- A Compound Annual Growth Rate (CAGR) of 6.8% signifies sustained investment and adoption across various regions.

- Technological advancements, particularly in smart systems and renewable energy integration, are pivotal to market evolution.

- Key drivers include stringent environmental regulations and the increasing demand for energy-efficient infrastructure in burgeoning urban centers.

- Challenges such as high initial investment and complex regulatory frameworks continue to influence market dynamics but are increasingly mitigated by policy support and innovative financing models.

- Opportunities for market expansion lie in waste heat recovery, 5th generation district heating and cooling (5GDHC) systems, and penetration into developing economies.

District Heating and Cooling Market Drivers Analysis

The District Heating and Cooling market is propelled by a confluence of macroeconomic and technological factors, primarily centered around the global imperative for energy efficiency and environmental sustainability. Increasing governmental support through favorable policies and incentives for green infrastructure development, coupled with growing urbanization and the demand for reliable and efficient energy services in densely populated areas, are significant accelerators. Furthermore, advancements in renewable energy technologies and the economic benefits derived from large-scale energy production and distribution are making district energy systems an increasingly attractive option for modern cities seeking to reduce their carbon footprint and enhance energy security.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for energy-efficient heating and cooling solutions, driven by rising energy costs and environmental consciousness. | +1.5% | Europe, North America, East Asia | Short to Medium Term |

| Increasing urbanization and rapid development of smart cities requiring integrated and sustainable energy infrastructure. | +1.8% | Asia Pacific, Middle East & Africa | Medium to Long Term |

| Stringent government regulations, policies, and incentives promoting clean energy and carbon emission reductions. | +1.7% | European Union, Nordic Countries, China | Short to Medium Term |

| Rising adoption of renewable energy sources and waste heat recovery systems in district energy networks. | +1.3% | Germany, Denmark, Sweden, Japan | Medium to Long Term |

| Technological advancements in heat pump systems, thermal storage, and smart grid integration improving system efficiency. | +0.5% | Global | Short to Medium Term |

District Heating and Cooling Market Restraints Analysis

Despite significant growth prospects, the District Heating and Cooling market faces several notable restraints that can impede its full potential. The most prominent barrier is the high upfront capital expenditure required for establishing or modernizing these complex networks, which often involves extensive civil engineering works and advanced technological components. This financial hurdle can deter potential investors and project developers, especially in regions with limited access to robust financing mechanisms. Additionally, the protracted and intricate planning and permitting processes, combined with potential public resistance to large-scale infrastructure projects, contribute to project delays and cost overruns, further slowing market expansion. Competition from established individual heating and cooling solutions also poses a challenge, as consumers may perceive these as more convenient or cost-effective in the short term, overlooking the long-term benefits of district energy.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment and long payback periods for large-scale infrastructure projects. | -1.2% | Global, especially developing economies | Short to Medium Term |

| Complexity of land acquisition, extensive civil engineering work, and securing necessary permits. | -0.8% | Dense urban areas, Europe, North America | Medium Term |

| Competition from decentralized or individual heating and cooling systems, often perceived as more flexible. | -0.5% | Global, particularly residential sectors | Short Term |

| Potential public perception issues and lack of awareness regarding the long-term benefits of district energy. | -0.3% | Regions with limited prior exposure to district energy | Short Term |

District Heating and Cooling Market Opportunities Analysis

The District Heating and Cooling market is rich with emerging opportunities driven by evolving energy landscapes and technological innovation. The increasing global focus on decarbonization and achieving net-zero emissions creates a strong impetus for the expansion and modernization of district energy systems, particularly those integrating a higher proportion of renewable sources. The development of fifth-generation district heating and cooling (5GDHC) systems, which operate at lower temperatures and offer increased flexibility, presents a significant technological leap forward, enabling better integration with diverse heat sources and sinks. Furthermore, the immense potential of waste heat recovery from industrial processes, data centers, and even sewage systems represents an untapped resource that can significantly enhance the efficiency and sustainability of district energy networks. Expansion into new geographical markets, especially in rapidly urbanizing developing economies, also offers substantial growth avenues as these regions seek scalable and sustainable energy solutions for their burgeoning cities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with smart grid technologies and advanced digital platforms for enhanced operational efficiency and control. | +1.0% | Global, particularly developed markets | Medium Term |

| Development and deployment of fifth-generation district heating and cooling (5GDHC) systems, offering greater flexibility and efficiency. | +1.1% | Europe, East Asia, North America | Medium to Long Term |

| Expansion into new geographical markets, especially emerging economies in Asia Pacific and Latin America, driven by urbanization. | +1.3% | China, India, Southeast Asia, Brazil | Long Term |

| Increased utilization of waste heat recovery from industrial processes, power plants, and commercial buildings. | +0.9% | Global, especially industrial clusters | Short to Medium Term |

District Heating and Cooling Market Challenges Impact Analysis

The District Heating and Cooling market, while promising, contends with several significant challenges that necessitate strategic solutions. One primary hurdle is the technical complexity involved in integrating diverse energy sources, particularly renewables, into existing or new networks, ensuring optimal system performance and reliability. This often requires advanced engineering and sophisticated control systems. Furthermore, navigating the complex regulatory landscapes and fragmented policy frameworks across different regions and countries can lead to delays and inconsistencies in project development. Securing consistent and long-term financing for the inherently capital-intensive district energy projects remains a persistent challenge, requiring innovative financial models and strong public-private partnerships. Lastly, managing network losses, ensuring thermal efficiency over long distances, and adapting to fluctuating energy demands pose operational challenges that require continuous innovation and maintenance strategies to uphold the economic viability of these systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical complexities in integrating diverse energy sources, including renewables, and ensuring system stability. | -0.7% | Global | Short to Medium Term |

| Complex and fragmented regulatory frameworks, leading to administrative hurdles and slow project approvals. | -0.6% | Europe (due to varying national regulations), North America | Medium Term |

| Securing long-term financing and attracting private investment for large, capital-intensive infrastructure projects. | -0.9% | Global, particularly emerging markets | Short to Medium Term |

| Managing network losses and maintaining thermal efficiency over extended distribution distances, especially in older infrastructure. | -0.4% | Established markets with aging infrastructure (e.g., Eastern Europe) | Short to Medium Term |

District Heating and Cooling Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the District Heating and Cooling Market, offering valuable insights into its size, growth trajectory, and key dynamics. The scope covers historical trends, current market performance, and future projections, enabling stakeholders to make informed strategic decisions. The report meticulously examines market drivers, restraints, opportunities, and challenges, providing a holistic view of the forces shaping the industry. Furthermore, it details key market segments, regional analyses, and the competitive landscape, highlighting the strategies of leading players and the overall outlook for the market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 195.5 Billion |

| Market Forecast in 2033 | USD 330.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 268 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vattenfall, Fortum, Engie, EnBW, Danfoss, Alfa Laval, Siemens Energy, ABB, Schneider Electric, Veolia, Statkraft, NRG Energy, Logstor, Ramboll, Empower, STEAG, Uniper, Tokyo Gas, RWE, NextEra Energy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The District Heating and Cooling market is meticulously segmented to provide a granular understanding of its diverse components and applications. These segmentations are crucial for identifying specific growth pockets, understanding demand patterns, and tailoring strategies for various end-users and technological deployments. The market's segmentation by energy source highlights the ongoing transition from traditional fossil fuels towards a more sustainable energy mix, incorporating a growing share of renewables and waste heat. Component-wise analysis provides insights into the technological infrastructure and investment areas. Application and end-use segmentations further delineate the market by consumer type and specific energy services, offering a comprehensive view of consumption patterns across residential, commercial, and industrial sectors for both heating and cooling needs.

- By Energy Source: This segment categorizes the market based on the primary fuels or energy inputs used to generate heat and cold for district networks.

- Fossil Fuels: Primarily coal, natural gas, and oil, which have historically been dominant but are gradually being phased out due to environmental concerns.

- Renewables: Includes geothermal energy, solar thermal energy, biomass, and heat pumps (air-source, ground-source, water-source), representing the growing shift towards sustainable sources.

- Industrial Waste Heat: Heat recovered from industrial processes, power plants, and data centers that would otherwise be wasted, a key driver for efficiency.

- By Component: This segmentation focuses on the key technological elements that constitute a district heating and cooling system.

- Pumps: Crucial for circulating the heating or cooling medium throughout the network.

- Pipes: Extensive network of insulated pipes for efficient distribution of heat/cold.

- Heat Exchangers: Devices facilitating the transfer of thermal energy between fluids, essential for both central plants and consumer substations.

- Thermal Storage: Technologies like large water tanks or phase-change materials for storing excess heat or cold, enhancing system flexibility and efficiency.

- Metering Equipment: Devices for accurately measuring energy consumption at various points in the network, enabling billing and system optimization.

- By Application: This segment differentiates the market based on the type of establishments utilizing district heating and cooling services.

- Residential: Heating and cooling services provided to residential buildings, including apartments and housing complexes.

- Commercial: Services provided to commercial establishments such as offices, shopping centers, hotels, and educational institutions.

- Industrial: Heating and cooling solutions for various industrial processes and facilities, often leveraging waste heat.

- By End-Use: This segmentation focuses on the specific thermal services provided by the district energy networks.

- Space Heating: Providing warmth to indoor spaces during colder periods.

- Water Heating: Supplying hot water for domestic or commercial use.

- Space Cooling: Providing refrigeration or air conditioning to indoor environments.

- Process Heating/Cooling: Tailored thermal energy for specific industrial or commercial processes requiring precise temperature control.

Regional Highlights

The global District Heating and Cooling market exhibits distinct regional dynamics, influenced by varying energy policies, climate conditions, and levels of urbanization. Each region presents unique opportunities and challenges that shape its contribution to the overall market growth.

- Europe: Europe is a dominant force in the District Heating and Cooling market, particularly the Nordic countries and Central and Eastern Europe. This leadership is driven by long-standing traditions of district energy, robust governmental support for decarbonization, and extensive existing infrastructure. Countries like Denmark, Sweden, Germany, and Finland are pioneers in integrating renewable energy sources, such as geothermal and biomass, and are at the forefront of developing advanced 4th and 5th generation district heating networks. Strict EU directives on energy efficiency and renewable energy adoption further bolster market expansion here.

- Asia Pacific (APAC): The APAC region is poised for the most significant growth, fueled by rapid urbanization, industrialization, and increasing energy demand, especially in China, India, and Southeast Asian countries. Governments in these regions are increasingly investing in modern energy infrastructure to combat air pollution and meet growing energy needs sustainably. While fossil fuels still play a role, there is a strong push towards developing integrated smart energy systems that incorporate renewables and waste heat recovery. The scale of new urban developments in APAC provides immense opportunities for greenfield district energy projects.

- North America: The North American market, though mature in some areas, is undergoing a modernization phase. The focus is on upgrading aging infrastructure, improving efficiency, and integrating more renewable energy sources. Policy incentives at federal and state levels, coupled with a growing emphasis on energy resilience and sustainability in major cities, are driving market growth. The expansion of cooling networks, particularly in the commercial and institutional sectors, is also a notable trend.

- Middle East and Africa (MEA): This region is experiencing considerable growth in district cooling, driven by high ambient temperatures and the rapid development of large-scale commercial and residential complexes, particularly in the Gulf Cooperation Council (GCC) countries. The abundant availability of natural gas has historically supported these systems, but there is an emerging interest in solar cooling and waste heat utilization. The increasing demand for sustainable and efficient cooling solutions in new city developments positions MEA as a promising market for district energy expansion.

- Latin America: While currently a smaller market, Latin America shows emerging potential, particularly in countries like Brazil and Mexico, driven by urbanization and the need for reliable energy infrastructure. Geothermal energy and biomass present significant opportunities for district heating, especially in areas with suitable natural resources. Investment in sustainable infrastructure is gradually increasing, albeit at a slower pace compared to other regions, offering long-term growth prospects as economic development progresses.

Top Key Players:

The market research report covers the analysis of key stake holders of the District Heating and Cooling Market. Some of the leading players profiled in the report include -

- Vattenfall

- Fortum

- Engie

- EnBW

- Danfoss

- Alfa Laval

- Siemens Energy

- ABB

- Schneider Electric

- Veolia

- Statkraft

- NRG Energy

- Logstor

- Ramboll

- Empower

- STEAG

- Uniper

- Tokyo Gas

- RWE

- NextEra Energy

Frequently Asked Questions:

What is District Heating and Cooling?

District Heating and Cooling (DHC) is a centralized system that produces and distributes thermal energy (heat and/or cold) from a central plant to multiple buildings within a defined area, such as a city, neighborhood, or industrial complex, through a network of insulated pipes. This system replaces individual heating and cooling units in each building, offering enhanced efficiency, reduced emissions, and improved energy security.

What are the primary drivers of the District Heating and Cooling market?

The primary drivers of the District Heating and Cooling market include the increasing global emphasis on decarbonization and achieving net-zero emissions, stringent government regulations promoting energy efficiency and renewable energy adoption, rapid urbanization and smart city development, and the economic benefits derived from large-scale, centralized energy production and waste heat recovery.

How does District Heating and Cooling contribute to sustainability?

District Heating and Cooling significantly contributes to sustainability by improving energy efficiency through centralized production and utilizing diverse, often renewable, energy sources and waste heat. This reduces fossil fuel consumption, lowers greenhouse gas emissions, and decreases local air pollution. Its collective nature also facilitates easier integration of intermittent renewable energy sources and enables better management of energy supply and demand, contributing to a more resilient and environmentally friendly energy system.

What are the key technologies used in modern District Energy systems?

Modern District Energy systems employ various key technologies to optimize performance and sustainability. These include highly efficient heat pumps (air-source, ground-source, water-source), advanced thermal energy storage solutions (e.g., large hot water tanks), smart grid integration for real-time monitoring and control, advanced pipe insulation materials to minimize heat loss, and combined heat and power (CHP) plants for simultaneous electricity and heat generation. Additionally, AI-driven predictive analytics are increasingly used for demand forecasting and operational optimization.

Which region leads the global District Heating and Cooling market?

Europe currently leads the global District Heating and Cooling market, particularly Nordic countries like Denmark, Sweden, and Finland, alongside Germany and other Central and Eastern European nations. This leadership is attributed to long-standing government policies supporting district energy, mature existing infrastructure, and significant investments in integrating renewable energy sources and advanced technologies to meet ambitious decarbonization targets.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted