Display ICs Market

Display ICs Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708015 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

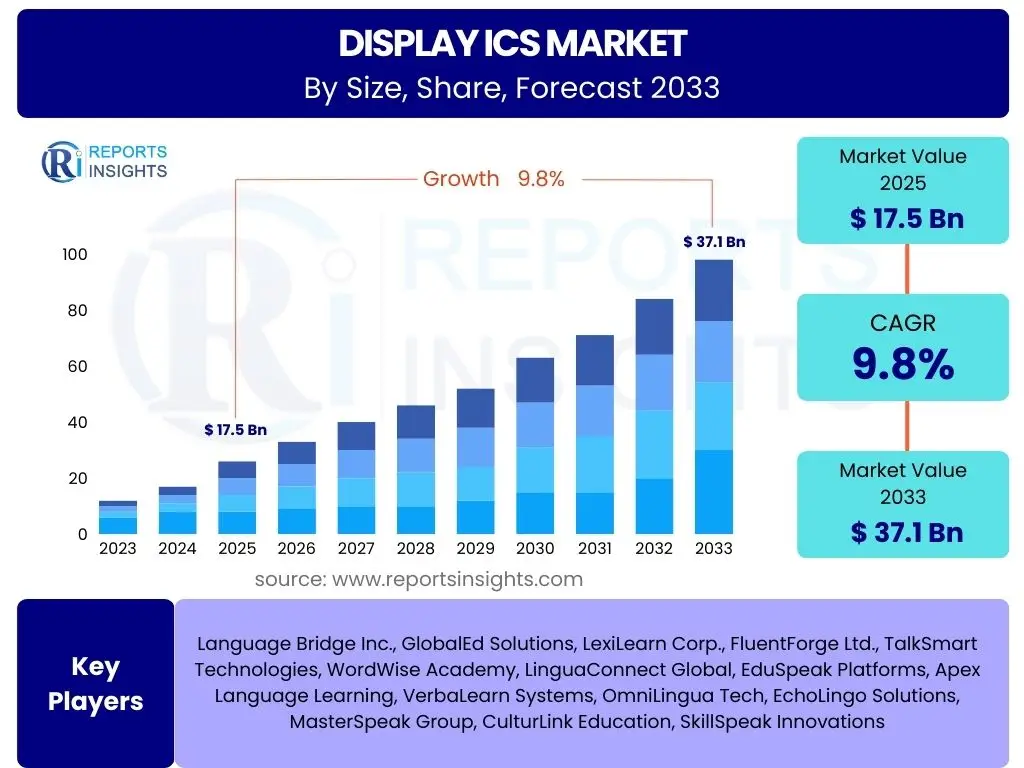

Display ICs Market Size

According to Reports Insights Consulting Pvt Ltd, The Display ICs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 17.5 Billion in 2025 and is projected to reach USD 37.1 Billion by the end of the forecast period in 2033.

Key Display ICs Market Trends & Insights

The Display ICs market is currently experiencing significant transformative trends driven by evolving consumer demands and technological advancements across various end-use industries. A primary driver is the accelerating adoption of high-resolution and advanced display technologies, such as OLED, Mini-LED, and Micro-LED, which necessitate more sophisticated and integrated Display ICs for optimal performance. Consumers and industries are increasingly seeking enhanced visual experiences, characterized by superior color accuracy, higher contrast ratios, and faster refresh rates, directly fueling innovation in Display IC design and manufacturing.

Furthermore, the proliferation of connected devices and the expansion into new application areas are reshaping market dynamics. The automotive sector, for instance, is witnessing a surge in large-format, interactive displays for infotainment and digital cockpits, demanding robust and reliable Display ICs capable of operating in diverse environmental conditions. Similarly, the growing market for augmented reality (AR) and virtual reality (VR) devices, as well as smart wearables, is creating demand for highly specialized, compact, and energy-efficient Display IC solutions that can support immersive and portable visual experiences.

Another critical trend is the increasing focus on power efficiency and system integration. With devices becoming thinner, lighter, and requiring longer battery life, manufacturers are prioritizing Display ICs that consume less power without compromising performance. This drives innovation in process technology and architectural design, leading to more integrated solutions that combine multiple functionalities, such as timing control, power management, and touch control, onto a single chip, thereby reducing component count and system complexity.

- Escalating demand for high-resolution and high-refresh-rate displays.

- Rapid adoption of OLED, Mini-LED, and future Micro-LED technologies.

- Integration of advanced displays in automotive infotainment and digital cockpits.

- Growth of AR/VR devices and smart wearables requiring specialized Display ICs.

- Emphasis on power efficiency and higher levels of system integration (SiP).

AI Impact Analysis on Display ICs

The integration of Artificial Intelligence (AI) is profoundly influencing the design, functionality, and performance optimization of Display ICs, moving beyond traditional image processing to enable more adaptive and intelligent display systems. User questions frequently revolve around how AI can enhance visual quality, improve power management, and introduce new capabilities to display technology. AI algorithms are being embedded directly into Display ICs to perform real-time image enhancement, such as dynamic contrast adjustment, color gamut mapping, and upscaling low-resolution content to match high-resolution screens, delivering a more vibrant and crisp visual experience without relying solely on static processing methods.

Beyond visual fidelity, AI's impact extends to critical operational aspects, particularly power management. Modern displays, especially those with high resolutions and refresh rates, are significant power consumers. AI-driven power management units within Display ICs can analyze content in real-time and dynamically adjust backlight levels, pixel drive voltages, and refresh rates based on the scene and ambient lighting conditions. This intelligent optimization significantly reduces power consumption, extending battery life for mobile devices and improving energy efficiency for larger displays, directly addressing a key concern for both consumers and manufacturers.

Furthermore, AI is enabling the development of more personalized and interactive display experiences. Future Display ICs, enhanced with AI capabilities, could adapt display characteristics based on user preferences, viewing habits, or even biometric data, offering a tailored visual output. This could involve dynamically adjusting color temperature, brightness, or even content presentation based on the user's focus or emotional state. The influence of AI is therefore not limited to mere performance boosts but is also paving the way for a new generation of smart, context-aware, and highly responsive display technologies.

- Real-time AI-powered image and video enhancement (upscaling, contrast, color correction).

- Intelligent power management for dynamic backlight and refresh rate optimization.

- Adaptive display technology for personalized user experiences based on context.

- AI-driven anomaly detection for display quality control during manufacturing.

- Facilitation of generative content and interactive display interfaces.

Key Takeaways Display ICs Market Size & Forecast

Analysis of the Display ICs market size and forecast reveals a robust growth trajectory, driven primarily by an insatiable demand for advanced visual experiences across an expanding array of devices. Key user questions often center on the sustainability of this growth, the primary factors underpinning it, and the long-term outlook for investment. The market's projected Compound Annual Growth Rate (CAGR) signifies a sustained period of expansion, indicating that Display ICs are not merely components but foundational elements for future technological advancements, from consumer electronics to highly specialized industrial applications.

A significant takeaway is the pivotal role of technological innovation in propelling market expansion. The continuous evolution of display technologies, such as the transition from LCD to OLED, and the emerging potential of Mini-LED and Micro-LED, directly fuels the demand for increasingly sophisticated and specialized Display IC solutions. This necessitates ongoing research and development investments by market participants to remain competitive and cater to the stringent performance requirements of next-generation displays, highlighting innovation as a critical success factor.

Furthermore, the diversification of Display IC applications beyond traditional smartphones and televisions underscores a broad and resilient market. The growing integration of advanced displays in automotive systems, augmented and virtual reality headsets, and industrial human-machine interfaces (HMIs) provides multiple avenues for market growth. This expansive application landscape reduces reliance on any single sector, ensuring market stability and offering diverse opportunities for specialized product development and market penetration over the forecast period.

- The Display ICs market is poised for significant and sustained growth through 2033.

- Technological advancements in display panels are primary growth accelerators.

- Diversification of applications, including automotive and AR/VR, ensures market resilience.

- Investment in R&D for next-generation Display ICs is crucial for market leadership.

- Increased integration of functionalities within single ICs drives efficiency and adoption.

Display ICs Market Drivers Analysis

The Display ICs market is primarily propelled by the relentless pursuit of superior visual experiences and the proliferation of display-equipped devices across nearly every industry sector. Consumers are continuously seeking higher resolution, richer colors, faster response times, and more immersive interfaces, which directly translates into demand for more advanced and powerful Display ICs. This fundamental desire for enhanced visual fidelity acts as a core, long-term driver for the entire display ecosystem.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for high-resolution and advanced displays (OLED, Mini-LED) | +2.5% | Global, particularly Asia Pacific (manufacturing & consumption) | Long-term (2025-2033) |

| Expansion of automotive infotainment and digital cockpit systems | +1.8% | North America, Europe, Asia Pacific (China, South Korea, Japan) | Medium to Long-term (2026-2033) |

| Proliferation of smart devices and wearables (smartphones, smartwatches, AR/VR) | +2.1% | Global, strong in Asia Pacific and North America | Medium to Long-term (2025-2033) |

| Technological advancements in display panel manufacturing | +1.5% | Asia Pacific (South Korea, China, Taiwan, Japan) | Continuous |

| Growth of IoT and smart home devices requiring interactive displays | +1.2% | North America, Europe, Asia Pacific | Medium-term (2025-2030) |

Display ICs Market Restraints Analysis

Despite robust growth, the Display ICs market faces several restraints that could temper its expansion. These primarily involve the significant investment required for advanced manufacturing, the complexities of global supply chains, and the inherent challenges of rapid technological obsolescence. Intense price competition, especially in mature segments, also puts pressure on profit margins, potentially hindering innovation and market entry for smaller players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and manufacturing costs for advanced process nodes | -1.3% | Global, impacts key manufacturing regions (Taiwan, South Korea) | Long-term |

| Supply chain vulnerabilities and geopolitical tensions | -1.0% | Global, impacts all regions reliant on semiconductor manufacturing | Medium-term (intermittent) |

| Intense price competition and commoditization in certain segments | -0.8% | Global, particularly Asia Pacific consumer electronics markets | Long-term |

| Rapid technological obsolescence requiring frequent product updates | -0.7% | Global | Continuous |

| Shortage of skilled semiconductor design engineers | -0.5% | Global, particularly North America, Europe, East Asia | Long-term |

Display ICs Market Opportunities Analysis

Significant opportunities exist within the Display ICs market, driven by emerging display technologies, the expansion into niche applications, and the increasing demand for highly integrated and intelligent solutions. The development of flexible, foldable, and transparent displays presents new design challenges and market avenues for specialized Display ICs, moving beyond rigid panel limitations. Furthermore, the convergence of display technology with artificial intelligence and machine learning creates avenues for smart, adaptive display systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Micro-LED and next-generation display technologies | +2.0% | Global, strong R&D in Asia Pacific, North America, Europe | Long-term (2028-2033) |

| Increased adoption of flexible, foldable, and transparent displays | +1.7% | Asia Pacific (South Korea, China), North America | Medium to Long-term (2026-2033) |

| Integration of AI/ML for enhanced display performance and adaptive features | +1.5% | Global, strong R&D in North America, Europe, Asia Pacific | Medium to Long-term (2025-2033) |

| Expansion into industrial, medical, and niche specialized display applications | +1.3% | North America, Europe, Asia Pacific | Long-term |

| Demand for highly integrated System-on-Panel (SOP) solutions | +1.0% | Global | Medium-term (2025-2030) |

Display ICs Market Challenges Impact Analysis

The Display ICs market faces several inherent challenges, including the complex demands of miniaturization, the ongoing quest for reduced power consumption, and the critical need for advanced thermal management solutions. These technical hurdles require significant engineering expertise and capital investment, making innovation a costly and continuous endeavor. Additionally, intellectual property disputes and the rapid pace of technological change pose strategic challenges for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Demands for extreme miniaturization and higher integration density | -1.2% | Global, impacts design and manufacturing globally | Continuous |

| Managing power consumption in high-resolution, high-refresh-rate displays | -0.9% | Global | Continuous |

| Complex thermal management in compact and high-performance devices | -0.8% | Global | Continuous |

| Intense competition for intellectual property and patent infringement risks | -0.6% | Global | Long-term |

| Rapid evolution of display standards and interface technologies | -0.5% | Global | Continuous |

Display ICs Market - Updated Report Scope

This comprehensive market report offers an in-depth analysis of the global Display ICs market, providing a detailed examination of its size, growth drivers, restraints, opportunities, and challenges. The scope encompasses a thorough segmentation by type, display technology, application, resolution, and end-use industry, alongside a meticulous regional analysis. The report aims to furnish stakeholders with critical insights into market dynamics, competitive landscape, and future projections, enabling informed strategic decision-making within the rapidly evolving display technology sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 17.5 Billion |

| Market Forecast in 2033 | USD 37.1 Billion |

| Growth Rate | 9.8% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Electronics, LG Display, Novatek Microelectronics, Himax Technologies, Synaptics, Dialog Semiconductor (now Renesas), Silicon Works (LG Innotek), FocalTech Systems, Raydium Semiconductor, MediaTek, MagnaChip, Goodix Technology, OmniVision Technologies, Texas Instruments, STMicroelectronics, NXP Semiconductors, Analog Devices, Rohm Semiconductor, Toshiba Electronic Devices & Storage, Parade Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Display ICs market is extensively segmented to provide a granular understanding of its diverse components and evolving landscape. This segmentation allows for precise analysis of market dynamics, growth drivers, and competitive strategies across various product types, display technologies, and end-use applications. By categorizing the market based on these critical dimensions, a clearer picture emerges of where innovation is most concentrated and where demand is strongest.

- By Type: This segment includes Driver ICs (gate drivers, source drivers), Controller ICs (display processors, graphic controllers), Timing Controllers (T-CON), Power Management ICs (PMICs) specifically for displays, and Touch Screen Controller ICs, each playing a crucial role in display operation.

- By Display Technology: Key categories are Liquid Crystal Display (LCD), Organic Light Emitting Diode (OLED), Mini-LED, Micro-LED, and other emerging technologies like Quantum Dot and flexible displays. Each technology demands specialized Display ICs optimized for its unique characteristics.

- By Application: The market is segmented across a broad range of applications including Smartphones & Tablets, Televisions, Laptops & Monitors, Automotive Displays (infotainment, instrument clusters), Wearable Devices (smartwatches, fitness trackers), Industrial & Medical Displays, Augmented Reality (AR) & Virtual Reality (VR) Devices, and Digital Signage.

- By Resolution: This covers displays from High Definition (HD - 720p) and Full HD (1080p) to higher resolutions such as 4K (Ultra HD) and 8K, with specific requirements for AR/VR devices pushing even higher pixel densities.

- By End-Use Industry: Major industries include Consumer Electronics, Automotive, Healthcare, Industrial, Retail, and Aerospace & Defense, each integrating displays for specific functionalities and user experiences.

Regional Highlights

- Asia Pacific (APAC): Dominates the global Display ICs market due to being the primary hub for display panel manufacturing, semiconductor production, and the largest consumer electronics market. Countries like China, South Korea, Japan, and Taiwan are at the forefront of display technology innovation and production, driving significant demand and supply for Display ICs. The region's robust industrial base and extensive consumer market ensure continued growth.

- North America: Characterized by strong innovation in high-end displays, AR/VR technologies, and advanced automotive applications. The presence of leading technology companies and a high adoption rate of premium consumer electronics contribute significantly to market growth, particularly for advanced and specialized Display ICs. Research and development activities, coupled with significant investments in next-generation display technologies, bolster its position.

- Europe: A key market for automotive displays, industrial human-machine interfaces, and niche medical display applications. European manufacturers are focused on high-quality, durable, and energy-efficient display solutions, leading to demand for robust and reliable Display ICs. Stringent regulations and a focus on industrial automation also shape the regional market for display components.

- Latin America: Exhibits steady growth, primarily driven by increasing penetration of smartphones, digital televisions, and the expanding automotive sector. The region's rising disposable income and urbanization contribute to the demand for various display-equipped consumer electronics.

- Middle East and Africa (MEA): Emerging as a growth region with increasing adoption of consumer electronics, infrastructure development, and smart city initiatives. Investments in digital signage, automotive displays, and the gradual expansion of smart device usage contribute to the demand for Display ICs, albeit from a smaller base compared to other regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Display ICs Market.- Samsung Electronics

- LG Display

- Novatek Microelectronics

- Himax Technologies

- Synaptics

- Renesas (Dialog Semiconductor)

- Silicon Works (LG Innotek)

- FocalTech Systems

- Raydium Semiconductor

- MediaTek

- MagnaChip

- Goodix Technology

- OmniVision Technologies

- Texas Instruments

- STMicroelectronics

- NXP Semiconductors

- Analog Devices

- Rohm Semiconductor

- Toshiba Electronic Devices & Storage

- Parade Technologies

Frequently Asked Questions

What is a Display IC?

A Display IC (Integrated Circuit) is an electronic component that controls and processes image signals to be shown on a display panel. It manages functions like timing control, pixel data transfer, power management, and often includes touch control capabilities, enabling the display to render visual content from a source device.

What drives the growth of the Display IC market?

The Display IC market growth is primarily driven by the increasing demand for high-resolution, advanced displays (OLED, Mini-LED), the proliferation of smart devices and wearables, expansion of automotive infotainment systems, and the continuous innovation in display technologies across consumer and industrial applications.

How does AI impact Display ICs?

AI impacts Display ICs by enabling advanced real-time image processing for enhanced visual quality, intelligent power management for energy efficiency, and adaptive display features that personalize user experience. AI algorithms are integrated to optimize display performance dynamically based on content and environmental conditions.

Which display technologies are most reliant on advanced Display ICs?

Advanced display technologies such as OLED, Mini-LED, and the emerging Micro-LED are highly reliant on sophisticated Display ICs. These technologies demand precise pixel control, complex power management, and high data transfer rates that only advanced Display ICs can provide to achieve their superior visual performance.

What are the primary applications of Display ICs?

Display ICs are essential in a wide range of applications, including smartphones, tablets, televisions, laptops, monitors, automotive infotainment systems, smartwatches, AR/VR headsets, industrial control panels, and medical imaging devices. They are fundamental to any product that utilizes a digital screen.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted