Disability Insurance Market

Disability Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707880 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Disability Insurance Market Size

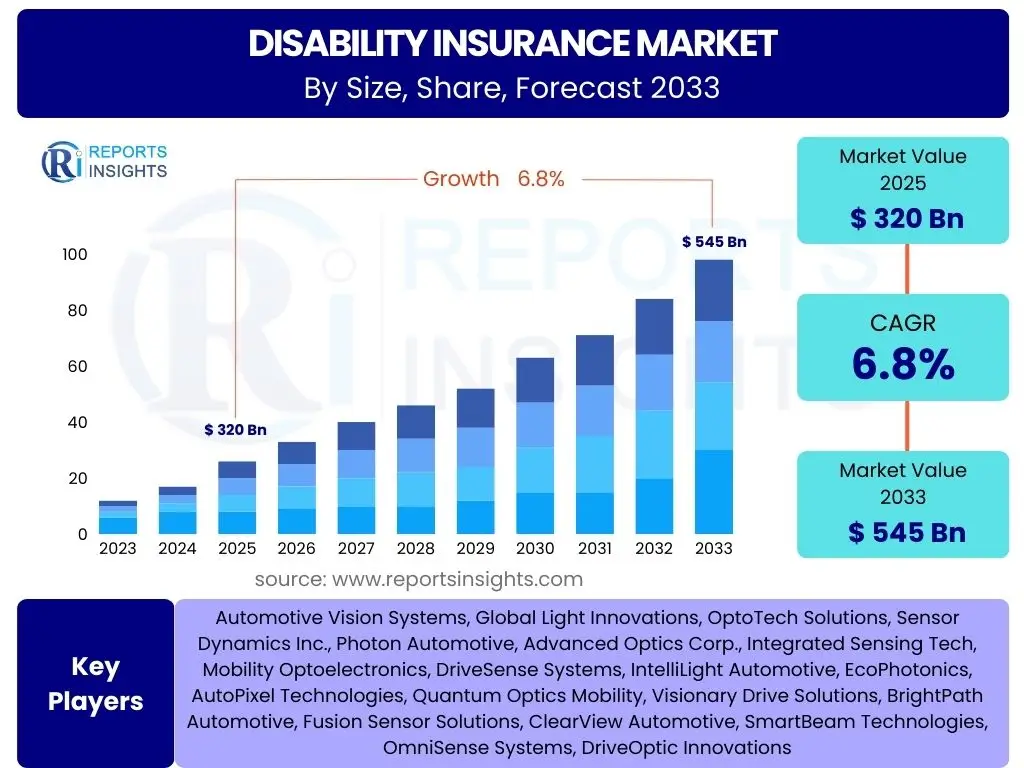

According to Reports Insights Consulting Pvt Ltd, The Disability Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 320 Billion in 2025 and is projected to reach USD 545 Billion by the end of the forecast period in 2033.

Key Disability Insurance Market Trends & Insights

User inquiries into the disability insurance market frequently highlight a demand for adaptable and comprehensive coverage options. There is a growing focus on policies that cater to a wider range of conditions, including mental health disorders and chronic illnesses, reflecting evolving societal understandings of disability. Furthermore, technological integration, particularly in policy administration, claims processing, and personalized risk assessment, is a recurring theme, with users seeking more efficient and user-friendly digital experiences.

Another prominent area of interest concerns the integration of preventative wellness programs and rehabilitation services within insurance offerings. Consumers are increasingly looking for insurance providers that not only offer financial protection but also support proactive health management and facilitate a smoother return to work. The shift towards group disability benefits as a crucial component of employee welfare packages is also gaining traction, driven by employers seeking to enhance their value proposition to talent.

Finally, the market is observing a significant trend towards policy customization. Individuals and groups are seeking plans that can be tailored to specific income levels, occupational risks, and personal circumstances, moving away from one-size-fits-all solutions. This demand for flexibility is reshaping product development and distribution strategies across the industry.

- Digitalization of application and claims processes for enhanced user experience.

- Increased demand for personalized and flexible policy structures.

- Growing inclusion of mental health and chronic illness coverage.

- Integration of wellness programs and rehabilitation support services.

- Expansion of group disability insurance as a key employee benefit.

- Leveraging predictive analytics for refined underwriting and risk assessment.

AI Impact Analysis on Disability Insurance

Common user questions regarding AI's impact on disability insurance reveal a mixed perception, ranging from optimism about improved efficiencies to concerns over data privacy and ethical considerations. Users anticipate that AI will significantly streamline the underwriting process, leading to faster policy approvals and more accurate risk profiling by analyzing vast datasets of health information and behavioral patterns. There is also a strong expectation that AI will enhance claims management, reducing fraud through advanced pattern recognition and accelerating legitimate claim payouts, thereby improving customer satisfaction.

However, users also express a need for transparency in AI-driven decision-making, particularly concerning policy eligibility and claim denials. There are concerns about potential biases in algorithms, which could inadvertently lead to discriminatory outcomes or unfair assessments. The ethical implications of using personal data for AI models, especially sensitive health information, are frequently raised, emphasizing the importance of robust data security and privacy protocols.

Looking ahead, users envision AI playing a crucial role in developing highly personalized insurance products, offering dynamic pricing, and providing proactive support to policyholders through intelligent assistants. The potential for AI to integrate with wearable technology and health monitoring systems to offer preventative care incentives is also a significant area of user interest, aiming to shift insurance from a reactive to a more proactive model.

- Enhanced efficiency in underwriting and risk assessment through machine learning.

- Automated claims processing, leading to faster adjudication and fraud detection.

- Personalized policy recommendations and dynamic pricing models based on individual data.

- Development of AI-powered chatbots for improved customer service and inquiries.

- Integration with health monitoring devices for proactive wellness programs and reduced risk.

- Potential for biased algorithms in decision-making requiring stringent oversight and ethical guidelines.

Key Takeaways Disability Insurance Market Size & Forecast

Analysis of user questions concerning the disability insurance market size and forecast highlights a clear understanding of the market's robust growth trajectory, primarily driven by increasing awareness of financial vulnerabilities and a proactive approach to income protection. Users are keen to understand the specific factors contributing to this expansion, such as demographic shifts, the rising prevalence of chronic conditions, and the evolving nature of work that necessitates flexible coverage options. The consistent year-over-year growth projection underscores the essential role disability insurance plays in modern financial planning.

Furthermore, inquiries often delve into the performance of different market segments, with a particular focus on the growth potential within individual versus group policies, and the regional variations in market maturity and adoption rates. There is significant interest in understanding how macroeconomic factors, regulatory changes, and technological advancements are shaping the market's future, indicating a sophisticated user base seeking deep insights beyond just headline figures. The anticipated market valuation by 2033 further solidifies its position as a critical and expanding sector within the broader insurance industry.

These insights collectively reveal that stakeholders are not merely interested in the 'what' of market growth but also the 'why' and 'how' it will continue to evolve. The demand for granular data on segment-specific growth, regional dynamics, and the impact of external factors points to a strategic interest in identifying lucrative niches and potential areas for innovation and investment within the disability insurance landscape.

- Market demonstrates strong, consistent growth, projected to reach USD 545 Billion by 2033.

- Increasing public and employer awareness of income protection drives demand.

- Demographic shifts and rising chronic disease incidence are significant growth catalysts.

- Technological integration and policy customization are crucial for future market expansion.

- Both individual and group disability insurance segments show promising growth trajectories.

Disability Insurance Market Drivers Analysis

The disability insurance market is primarily propelled by several key factors that underscore the increasing need for financial protection against unforeseen life events. A significant driver is the heightened awareness among individuals and employers regarding the economic consequences of an unexpected disability, leading to a greater inclination to secure income replacement. Concurrently, the rising prevalence of chronic health conditions and lifestyle-related diseases globally contributes significantly to the demand for comprehensive disability coverage, as these conditions are often long-term and can impact earning capacity. Furthermore, supportive regulatory environments and government initiatives aimed at promoting social security and worker welfare, particularly in developed economies, bolster market growth by encouraging or mandating disability coverage.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Awareness of Financial Security Needs | +1.5% | Global, particularly North America, Europe | Short to Medium Term (2025-2029) |

| Rising Incidence of Chronic Diseases and Work-Related Injuries | +1.8% | Global, high in developed nations with aging populations | Medium to Long Term (2025-2033) |

| Supportive Government Regulations and Mandates | +1.2% | Europe, parts of North America (e.g., California, New York) | Medium Term (2026-2031) |

| Aging Global Population and Extended Working Lives | +1.3% | Global, particularly Japan, Western Europe | Long Term (2028-2033) |

| Growth in Group Disability Benefits as an Employee Perk | +1.0% | North America, Western Europe, Emerging Asia | Short to Medium Term (2025-2030) |

Disability Insurance Market Restraints Analysis

Despite its growth, the disability insurance market faces several significant restraints that can impede its expansion. One primary challenge is the relatively high cost of premiums, especially for long-term policies, which can be a deterrent for individuals and small businesses with limited budgets. This cost sensitivity is particularly pronounced in emerging markets where disposable income might be lower. Additionally, a persistent lack of comprehensive awareness regarding the benefits and necessity of disability insurance among potential policyholders, particularly outside of group benefits settings, limits market penetration. Many individuals mistakenly believe that social security or workers' compensation will suffice, overlooking the gaps in coverage.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Premium Costs for Comprehensive Coverage | -1.3% | Global, more pronounced in developing economies | Short to Medium Term (2025-2030) |

| Lack of Awareness and Understanding of Policy Benefits | -1.0% | APAC, Latin America, segments of North America | Medium to Long Term (2026-2033) |

| Complex Policy Terms and Conditions | -0.8% | Global | Short Term (2025-2028) |

| Economic Downturns Affecting Disposable Income | -1.5% | Region-specific, sensitive to global economic cycles | Short Term (Varies) |

| Competition from Government-Provided Social Security | -0.7% | Europe, North America | Long Term (2027-2033) |

Disability Insurance Market Opportunities Analysis

The disability insurance market is ripe with opportunities for innovation and expansion, driven by evolving consumer needs and technological advancements. One significant opportunity lies in the development of highly customized and flexible policy options, allowing individuals and businesses to tailor coverage to specific occupational risks, income levels, and desired benefit periods. This customization can attract a broader demographic, including gig economy workers and small business owners who often require more adaptable insurance solutions. Furthermore, the integration of advanced technologies such as artificial intelligence and big data analytics presents a substantial opportunity to streamline underwriting processes, enhance fraud detection, and offer personalized risk assessments, leading to more efficient operations and competitive pricing.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Customized and Flexible Policy Offerings | +1.4% | Global, particularly North America, Europe | Medium Term (2026-2031) |

| Technological Advancements for Underwriting and Claims | +1.6% | Global | Short to Medium Term (2025-2030) |

| Expansion into Underserved Emerging Markets | +1.1% | APAC, Latin America, MEA | Long Term (2028-2033) |

| Partnerships with Health & Wellness Providers | +0.9% | North America, Europe | Medium Term (2027-2032) |

| Targeting the Gig Economy and Small Business Segment | +1.2% | Global, high growth in developed markets | Short to Medium Term (2025-2030) |

Disability Insurance Market Challenges Impact Analysis

The disability insurance market faces several distinct challenges that necessitate strategic responses from providers. A persistent challenge is the management and mitigation of fraudulent claims, which can significantly inflate operational costs and ultimately lead to higher premiums for legitimate policyholders. Developing robust detection mechanisms without unduly delaying valid claims remains a delicate balance. Furthermore, the intricate and often varying regulatory landscapes across different regions and countries pose compliance hurdles, requiring insurers to invest heavily in legal and administrative resources to navigate diverse legal frameworks. This complexity can hinder market entry for new players and complicate cross-border operations for established ones.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Fraudulent Claims and Moral Hazard | -1.0% | Global | Ongoing |

| Navigating Complex Regulatory and Compliance Frameworks | -0.9% | Europe, North America, highly fragmented regions | Ongoing |

| Data Privacy and Security Concerns with Digitalization | -0.7% | Global | Ongoing |

| Attracting and Educating Younger Demographics | -0.8% | Global, particularly developed markets | Long Term (2028-2033) |

| Economic Volatility and Impact on Affordability | -1.2% | Global, sensitive to macroeconomic cycles | Short to Medium Term (Varies) |

Disability Insurance Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Disability Insurance Market, covering market size estimations, historical data from 2019-2023, and detailed forecasts spanning 2025-2033. The scope includes a thorough examination of key market trends, growth drivers, restraints, opportunities, and challenges. Furthermore, the report offers extensive segmentation analysis by type, provider, distribution channel, end-use, and application, alongside a regional breakdown, to present a holistic view of the market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 320 Billion |

| Market Forecast in 2033 | USD 545 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Liberty Mutual Insurance, Lincoln Financial Group, Guardian Life Insurance Company of America, Principal Financial Group, MetLife, Unum Group, Aflac Inc., The Hartford, Assurity Life Insurance Company, MassMutual, Mutual of Omaha, Ohio National Financial Services, Standard Insurance Company, Reliance Standard Life Insurance Company, Cigna, Anthem, New York Life Insurance Company, AXA, Allianz, Zurich Insurance Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The disability insurance market is segmented to provide a granular view of its diverse landscape, enabling a deeper understanding of consumer needs and market dynamics. Key segments include categorization by the type of coverage, distinguishing between short-term and long-term disability policies, which cater to different durations of income replacement needs. Further segmentation by provider type differentiates between public and private insurers, highlighting the varying roles government programs and commercial entities play in the market. The distribution channel segment, encompassing agents, direct sales, bancassurance, and online platforms, illustrates how policies reach consumers, reflecting the evolving preference for digital accessibility.

- By Type:

- Short-Term Disability (STD)

- Long-Term Disability (LTD)

- By Provider:

- Public Disability Insurance

- Private Disability Insurance

- By Distribution Channel:

- Agents & Brokers

- Direct Sales

- Bancassurance

- Online & Digital Platforms

- By End-Use:

- Individual

- Group (Employer-Sponsored, Association-Sponsored)

- By Application:

- Illness-Related Disability

- Accident-Related Disability

Regional Highlights

- North America: This region holds a significant market share, driven by high awareness levels, robust employer-sponsored group benefits, and the increasing cost of healthcare. The United States, in particular, demonstrates a mature market with high demand for both individual and group long-term disability policies, supported by a strong regulatory framework and a proactive approach to employee welfare.

- Europe: The European market is characterized by a blend of public social security systems and private insurance offerings. Countries like Germany, the UK, and France show considerable adoption, influenced by varying national legislations concerning social protection and a growing recognition of the need for supplementary private coverage. Digitalization and customized solutions are key growth areas.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by expanding economies, increasing disposable incomes, and a rapidly growing middle class. Countries such as China, India, and Australia are witnessing rising awareness about financial planning and the importance of disability insurance, alongside a younger workforce entering the market.

- Latin America: This region presents emerging opportunities with increasing urbanization and economic development. While market penetration is currently lower, growing awareness and the expansion of organized employment sectors are expected to drive demand, particularly for group disability schemes.

- Middle East and Africa (MEA): The MEA market is in its nascent stages but is demonstrating potential for growth, primarily influenced by infrastructure development, rising expat populations, and government initiatives to diversify economies. Awareness campaigns and the establishment of robust regulatory frameworks will be crucial for accelerating adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Disability Insurance Market.- Liberty Mutual Insurance

- Lincoln Financial Group

- Guardian Life Insurance Company of America

- Principal Financial Group

- MetLife

- Unum Group

- Aflac Inc.

- The Hartford

- Assurity Life Insurance Company

- MassMutual

- Mutual of Omaha

- Ohio National Financial Services

- Standard Insurance Company

- Reliance Standard Life Insurance Company

- Cigna

- Anthem

- New York Life Insurance Company

- AXA

- Allianz

- Zurich Insurance Group

Frequently Asked Questions

What is disability insurance and why is it important?

Disability insurance provides income replacement if you are unable to work due to illness or injury. It is crucial for financial stability, as it helps cover living expenses and maintain your standard of living when your regular income stops.

What are the main types of disability insurance policies?

The primary types are Short-Term Disability (STD), which covers temporary periods (typically up to two years), and Long-Term Disability (LTD), which offers coverage for extended periods, potentially until retirement age, depending on the policy terms.

How much does disability insurance cost?

The cost of disability insurance varies based on factors such as your age, occupation, income, health status, the benefit amount, waiting period, and benefit period. Generally, premiums range from 1% to 3% of your annual income.

Does disability insurance cover mental health conditions?

Many modern disability insurance policies now offer coverage for mental health conditions, though the specifics can vary greatly by provider and policy. It is essential to review the policy details to understand the extent of mental health coverage.

How can I choose the right disability insurance policy?

Selecting the right policy involves assessing your financial needs, income, occupation, and existing coverage. Consider the benefit amount, waiting period, benefit period, and any riders that might be beneficial, often consulting with a financial advisor is recommended.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted