Direct Imaging System Market

Direct Imaging System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705062 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Direct Imaging System Market Size

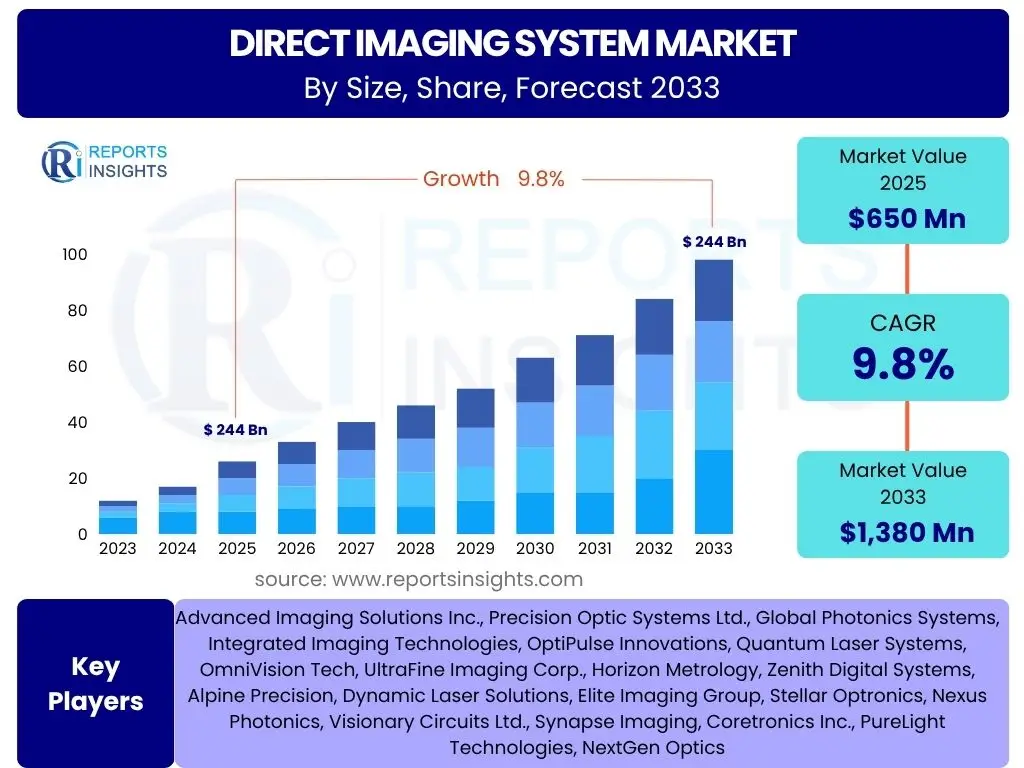

According to Reports Insights Consulting Pvt Ltd, The Direct Imaging System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 650 Million in 2025 and is projected to reach USD 1,380 Million by the end of the forecast period in 2033. This growth trajectory is underpinned by the increasing demand for high-precision manufacturing across various industries, coupled with continuous technological advancements in imaging and automation. The market’s expansion is indicative of a broader industry shift towards more efficient, accurate, and automated production processes.

The substantial growth projected for the Direct Imaging System Market reflects its critical role in modern electronics manufacturing and other precision-dependent sectors. As industries strive for miniaturization and enhanced performance in their products, the capabilities offered by direct imaging systems—such as superior resolution, faster processing speeds, and reduced operational costs compared to traditional photolithography—become indispensable. This market valuation highlights the robust investment and adoption trends expected over the next decade, driven by innovation and evolving industrial requirements.

Key Direct Imaging System Market Trends & Insights

The Direct Imaging System Market is undergoing significant transformations driven by technological innovation and evolving industry demands. Users commonly inquire about the overarching shifts influencing the market's trajectory, seeking to understand not only current best practices but also future directions. Key themes emerging from these inquiries include the pervasive drive towards automation, the increasing integration of smart manufacturing principles, and the relentless pursuit of higher resolution and precision in imaging processes. Additionally, there is a strong focus on sustainability and efficiency, prompting advancements in energy-saving direct imaging solutions and waste reduction.

These trends collectively shape the competitive landscape and product development within the direct imaging sector. Manufacturers and end-users are keen on solutions that not only enhance throughput and yield but also offer greater flexibility and adaptability to diverse production needs. The convergence of hardware improvements, sophisticated software, and data analytics is redefining the capabilities of direct imaging systems, making them more versatile and powerful. This continuous evolution is crucial for supporting advancements in areas like advanced packaging, flexible electronics, and high-density interconnects, which are critical for next-generation electronic devices.

- Miniaturization and High-Density Interconnect (HDI) Demand: Growing need for smaller, more powerful electronic devices drives demand for high-resolution direct imaging.

- Automation and Industry 4.0 Integration: Seamless integration with automated production lines and smart factory environments for enhanced efficiency and reduced human intervention.

- Increased Adoption in Advanced Packaging: Direct imaging systems are becoming critical for complex packaging technologies like System-in-Package (SiP) and Through-Silicon Via (TSV).

- Sustainable Manufacturing Practices: Development of energy-efficient systems and processes that reduce chemical waste, aligning with environmental regulations and corporate sustainability goals.

- Software and Data Analytics Integration: Enhanced software capabilities for process control, defect detection, and predictive maintenance, leveraging big data for optimized performance.

AI Impact Analysis on Direct Imaging System

The integration of Artificial Intelligence (AI) is a prominent topic of user inquiry regarding Direct Imaging Systems, with common questions revolving around how AI can enhance system performance, automate decision-making, and improve manufacturing processes. Users are keenly interested in AI’s potential to revolutionize aspects such as defect detection, yield optimization, predictive maintenance, and overall operational efficiency. The expectation is that AI will move direct imaging beyond mere automation to intelligent process control, capable of learning and adapting to dynamic manufacturing conditions.

AI's influence is anticipated to transform direct imaging systems into more autonomous and intelligent machines. This includes the deployment of machine learning algorithms for real-time image analysis, leading to more accurate and faster identification of anomalies and defects, thereby significantly reducing false positives and human errors. Furthermore, AI can optimize exposure parameters, calibrate systems dynamically, and predict potential equipment failures, ensuring consistent quality and maximizing uptime. The ability of AI to process vast amounts of imaging and process data will enable manufacturers to gain deeper insights into their operations, leading to continuous improvement and cost reduction.

- Enhanced Defect Detection: AI-powered algorithms for rapid and accurate identification of microscopic defects, reducing false positives and improving quality control.

- Process Optimization: Machine learning models optimize exposure settings, focus, and alignment in real-time, leading to improved throughput and yield.

- Predictive Maintenance: AI analyzes system performance data to predict potential equipment failures, enabling proactive maintenance and minimizing downtime.

- Automated Quality Control: AI automates quality assurance checks, ensuring consistency and adherence to specifications without manual intervention.

- Data-Driven Insights: AI processes large datasets from imaging operations to provide actionable insights for process improvement and manufacturing efficiency.

Key Takeaways Direct Imaging System Market Size & Forecast

Users frequently seek concise summaries of the Direct Imaging System market's future trajectory and its underlying drivers, often asking about the most critical insights from market size and forecast data. The primary takeaway is a robust and sustained growth outlook, primarily fueled by the accelerating global demand for advanced electronics and the increasing complexity of printed circuit boards (PCBs) and semiconductor manufacturing. This sustained expansion underscores the indispensable nature of direct imaging technology in meeting the precision and efficiency requirements of modern production environments.

Another crucial insight is the market's resilience and adaptability, driven by ongoing innovation in AI, automation, and material science. The projected financial figures confirm that direct imaging systems are not merely a transitional technology but a foundational component for future manufacturing. Stakeholders should note the expanding application areas beyond traditional electronics, signaling new revenue streams and opportunities for market participants. The emphasis on high throughput, superior resolution, and environmental sustainability will continue to be pivotal differentiators in a competitive landscape.

- Significant Market Expansion: The market is poised for strong growth, projecting a near doubling in value by 2033, driven by pervasive digitalization and advanced manufacturing.

- Technology as a Catalyst: Continuous innovation in direct imaging technology, particularly AI integration, is a primary growth engine and competitive differentiator.

- Broadening Application Scope: Increasing adoption across diverse sectors beyond traditional PCB, including advanced packaging, flexible electronics, and medical devices.

- Efficiency and Precision Imperative: The market is fundamentally driven by the need for higher precision, faster turnaround times, and greater automation in manufacturing.

- Strategic Investment Potential: The consistent growth forecast suggests a stable and attractive market for strategic investments in R&D, infrastructure, and market expansion.

Direct Imaging System Market Drivers Analysis

The Direct Imaging System Market is primarily propelled by several compelling factors, most notably the relentless demand for miniaturization and high-density electronic devices. As consumer electronics, automotive systems, and medical devices become increasingly sophisticated and compact, the need for precise and intricate circuitry grows exponentially. Direct imaging systems offer the unparalleled resolution and accuracy required to produce these advanced components, making them indispensable in modern manufacturing. This continuous drive for smaller, more powerful devices directly translates into sustained demand for high-performance direct imaging solutions.

Another significant driver is the widespread adoption of automation and smart manufacturing practices across industries. Manufacturers are increasingly investing in technologies that enhance efficiency, reduce human error, and streamline production processes. Direct imaging systems, with their inherent automation capabilities and integration potential into Industry 4.0 frameworks, perfectly align with these objectives. They enable faster prototyping, quicker design iterations, and higher production yields, which are critical for maintaining competitiveness in a rapidly evolving global market. The transition from traditional analog processes to digital, automated direct imaging is a testament to this driving force.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization & HDI Demand | +1.5% | Global, particularly APAC | Long-term |

| Automation & Industry 4.0 Integration | +1.2% | North America, Europe, APAC | Mid-term to Long-term |

| Growing Electronics Manufacturing | +1.0% | APAC, particularly China, South Korea, Taiwan | Long-term |

| Demand for Flexible Electronics | +0.8% | North America, Europe, APAC | Mid-term |

Direct Imaging System Market Restraints Analysis

Despite the robust growth prospects, the Direct Imaging System Market faces certain restraints that could impede its full potential. A primary challenge is the high initial capital investment required for acquiring and implementing these advanced systems. Direct imaging equipment, particularly high-end models with superior resolution and throughput capabilities, comes with a substantial price tag. This significant upfront cost can be a barrier for smaller to medium-sized enterprises (SMEs) or companies with limited budgets, potentially slowing down wider adoption, especially in cost-sensitive regions or emerging markets.

Another notable restraint is the inherent complexity of integrating direct imaging systems into existing manufacturing workflows. While these systems offer advanced automation, their successful deployment often requires significant retooling, employee training, and adaptation of current processes. This integration complexity can lead to longer implementation cycles, initial operational disruptions, and a need for specialized technical expertise, which might deter some potential adopters. Furthermore, the rapid pace of technological obsolescence in the electronics industry means that companies must continually invest in upgrades or new systems to remain competitive, adding to the total cost of ownership over time.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Cost | -0.9% | Global, particularly SMEs | Mid-term |

| Technological Complexity & Integration Challenges | -0.7% | Global | Short-term to Mid-term |

| Skilled Workforce Requirement | -0.5% | Global | Long-term |

| Market Volatility & Economic Downturns | -0.3% | Global, varies by region | Short-term |

Direct Imaging System Market Opportunities Analysis

The Direct Imaging System Market is rich with opportunities, driven by evolving technological landscapes and expanding application areas. A significant opportunity lies in the burgeoning adoption of direct imaging technology in emerging applications beyond traditional PCB manufacturing, such as advanced packaging for semiconductors, micro-electromechanical systems (MEMS), and specialized medical devices. These sectors demand extremely high precision and consistency, attributes perfectly addressed by direct imaging, thus opening new avenues for market penetration and revenue growth for system providers.

Furthermore, the ongoing advancements in material science and the development of new substrate technologies present additional opportunities. As new flexible, stretchable, and unconventional materials gain traction in electronics, direct imaging systems, with their non-contact and highly adaptable capabilities, become critical for processing these novel substrates. This creates a niche for manufacturers to develop and optimize direct imaging solutions specifically tailored for these advanced materials. Moreover, expansion into developing economies, particularly those investing heavily in domestic electronics manufacturing capabilities, offers considerable untapped market potential, provided the right strategies for market entry and localized support are implemented.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications (e.g., Medical, Automotive Sensors) | +1.1% | North America, Europe, APAC | Long-term |

| Growth in Flexible & Printed Electronics | +0.9% | Global | Mid-term to Long-term |

| Market Expansion in Developing Economies | +0.7% | Southeast Asia, India, Latin America | Long-term |

| Integration with Additive Manufacturing | +0.6% | Global | Mid-term |

Direct Imaging System Market Challenges Impact Analysis

The Direct Imaging System Market, while promising, faces several challenges that require strategic navigation. Intense competition among key players is a significant hurdle, as numerous manufacturers vie for market share by offering increasingly sophisticated and specialized systems. This competitive pressure often leads to price erosion and necessitates continuous investment in research and development to maintain a technological edge, which can strain profit margins, particularly for smaller market entrants. Innovation cycles are shortening, meaning companies must rapidly adapt to new demands or risk falling behind.

Another crucial challenge is managing complex global supply chains, particularly for critical optical components, laser sources, and high-precision mechanical parts. Geopolitical tensions, trade disputes, and unforeseen global events can disrupt these supply chains, leading to increased lead times, higher component costs, and production delays. Maintaining robust and resilient supply networks is paramount for manufacturers to ensure consistent product delivery and avoid operational bottlenecks. Furthermore, the inherent technical complexity of these systems and the need for specialized service and support in diverse geographical locations pose ongoing challenges related to scalability and customer satisfaction.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition | -0.8% | Global | Long-term |

| Supply Chain Disruptions | -0.6% | Global | Short-term to Mid-term |

| Rapid Technological Obsolescence | -0.4% | Global | Mid-term |

| High R&D Investment Required | -0.3% | Global | Long-term |

Direct Imaging System Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Direct Imaging System Market, providing an in-depth analysis of its current landscape, historical performance, and future projections. It encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The scope extends to critical technological trends, the transformative impact of AI, and an exhaustive profiling of leading market participants, offering a strategic overview for stakeholders seeking to navigate and capitalize on this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650 Million |

| Market Forecast in 2033 | USD 1,380 Million |

| Growth Rate | 9.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Imaging Solutions Inc., Precision Optic Systems Ltd., Global Photonics Systems, Integrated Imaging Technologies, OptiPulse Innovations, Quantum Laser Systems, OmniVision Tech, UltraFine Imaging Corp., Horizon Metrology, Zenith Digital Systems, Alpine Precision, Dynamic Laser Solutions, Elite Imaging Group, Stellar Optronics, Nexus Photonics, Visionary Circuits Ltd., Synapse Imaging, Coretronics Inc., PureLight Technologies, NextGen Optics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Direct Imaging System Market is extensively segmented based on several critical parameters, offering a granular view of its diverse landscape and enabling targeted strategic planning. These segmentations allow for a comprehensive understanding of how different technologies, applications, end-user industries, and system components contribute to the overall market dynamics. Analyzing each segment individually helps in identifying specific growth pockets, emerging niches, and areas requiring further technological advancement, thereby facilitating informed decision-making for market participants.

Each segment holds unique growth drivers and competitive intensities. For instance, the technology segmentation highlights the shift towards more advanced laser and LED-based systems due to their superior performance and efficiency, while application-based segmentation showcases the dominance of PCB manufacturing but also the rapid expansion into semiconductor packaging and medical devices. Understanding these detailed breakdowns is crucial for manufacturers to tailor their product offerings, for investors to identify lucrative opportunities, and for end-users to select the most appropriate direct imaging solutions for their specific operational needs and industry requirements.

- By Technology:

- UV Lasers

- LED Exposure

- Hybrid Systems

- By Application:

- Printed Circuit Boards (PCBs)

- Inner Layer

- Outer Layer

- Solder Mask

- Semiconductor Packaging

- Flat Panel Displays

- Medical Devices

- MEMS

- Automotive

- Aerospace & Defense

- Printed Circuit Boards (PCBs)

- By End-User Industry:

- Electronics Industry

- Automotive Industry

- Healthcare Industry

- Industrial Sector

- Consumer Goods

- By Component:

- Light Sources

- Optics & Lenses

- Mechanical Stages & Platforms

- Software & Control Systems

- Automation & Handling Systems

Regional Highlights

- Asia Pacific (APAC): Dominates the Direct Imaging System Market due to its robust electronics manufacturing base, particularly in China, South Korea, Taiwan, and Japan. The region benefits from significant investments in advanced semiconductor and PCB production facilities, coupled with a large consumer electronics market driving demand for miniaturized devices. Government initiatives supporting high-tech manufacturing further bolster market growth.

- North America: Represents a significant market, driven by strong R&D activities, innovation in advanced packaging, and the presence of leading technology companies. Demand is high for direct imaging systems in high-precision applications like aerospace, defense, and specialized medical device manufacturing, emphasizing quality and technological leadership.

- Europe: A mature market characterized by stringent quality standards and a focus on industrial automation and automotive electronics. Countries like Germany, France, and the UK are key contributors, driven by their well-established manufacturing sectors and ongoing investments in Industry 4.0 initiatives. The region also exhibits strong growth in niche applications such as micro-electromechanical systems (MEMS).

- Latin America: An emerging market for direct imaging systems, with gradual growth attributed to increasing industrialization and expanding electronics assembly operations, particularly in Mexico and Brazil. Investment in modern manufacturing infrastructure is slowly increasing, signaling future opportunities.

- Middle East & Africa (MEA): Currently a smaller market but showing potential, driven by diversifying economies and nascent efforts to establish local manufacturing capabilities in sectors like automotive and consumer electronics. The region's growth is anticipated to be slower but consistent, as infrastructure development progresses.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Direct Imaging System Market.- Advanced Imaging Solutions Inc.

- Precision Optic Systems Ltd.

- Global Photonics Systems

- Integrated Imaging Technologies

- OptiPulse Innovations

- Quantum Laser Systems

- OmniVision Tech

- UltraFine Imaging Corp.

- Horizon Metrology

- Zenith Digital Systems

- Alpine Precision

- Dynamic Laser Solutions

- Elite Imaging Group

- Stellar Optronics

- Nexus Photonics

- Visionary Circuits Ltd.

- Synapse Imaging

- Coretronics Inc.

- PureLight Technologies

- NextGen Optics

Frequently Asked Questions

What is a Direct Imaging System?

A Direct Imaging (DI) System is an advanced photolithography technology that uses a highly focused light source (e.g., UV laser or LED) to directly "write" circuit patterns onto a photosensitive material, typically a PCB or semiconductor wafer, without the need for a physical photomask. This digital process significantly enhances precision, throughput, and flexibility in manufacturing.

What are the primary applications of Direct Imaging Systems?

Direct Imaging Systems are primarily utilized in the manufacturing of Printed Circuit Boards (PCBs) for creating inner layers, outer layers, and solder masks. Their applications also extend to semiconductor packaging, flat panel display production, micro-electromechanical systems (MEMS), and specialized areas within the medical, automotive, and aerospace industries requiring high-resolution patterning.

What are the key benefits of using Direct Imaging over traditional methods?

Direct Imaging offers several advantages, including superior resolution for fine-line circuitry, faster processing speeds, and improved yield due to digital accuracy. It eliminates the need for expensive and fragile photomasks, reducing operational costs and material waste. Furthermore, DI systems provide greater flexibility for design changes and prototypes, supporting quicker time-to-market for complex electronic products.

How is AI impacting the Direct Imaging System Market?

AI is transforming Direct Imaging Systems by enhancing defect detection accuracy through machine learning algorithms, optimizing exposure parameters in real-time for improved yield, and enabling predictive maintenance to minimize downtime. AI integration leads to more intelligent, autonomous systems capable of continuous self-optimization and providing deeper insights into manufacturing processes, boosting overall efficiency and quality.

What is the projected growth rate for the Direct Imaging System Market?

The Direct Imaging System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. This robust growth trajectory is driven by increasing demand for miniaturized and high-density electronic components across diverse industries globally.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted