Diisobutylene Market

Diisobutylene Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710018 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

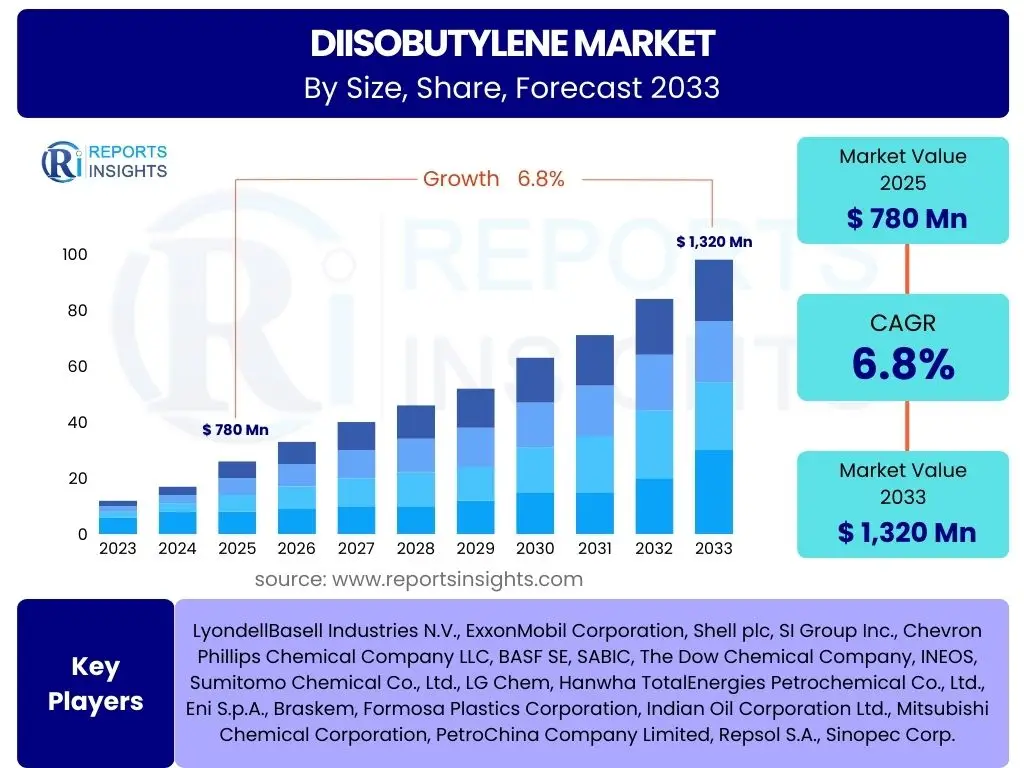

Diisobutylene Market Size

According to Reports Insights Consulting Pvt Ltd, The Diisobutylene Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 780 Million in 2025 and is projected to reach USD 1,320 Million by the end of the forecast period in 2033.

Key Diisobutylene Market Trends & Insights

The Diisobutylene (DIB) market is currently experiencing dynamic shifts driven by evolving industrial demands and a greater emphasis on efficiency and sustainability in chemical processes. A prominent trend involves the increasing adoption of DIB as a high-octane gasoline additive and a critical building block in the synthesis of specialty chemicals, where its unique branched structure offers enhanced performance characteristics. The automotive industry's pursuit of cleaner fuels and advanced materials is significantly influencing this trajectory, pushing manufacturers to innovate in DIB production and application technologies.

Furthermore, there is a noticeable trend towards optimizing production processes to reduce environmental impact and improve cost-effectiveness. This includes exploring novel catalytic routes and feedstock diversification, moving beyond traditional petroleum-based sources to potentially incorporate bio-based alternatives in the long term. Geographically, Asia Pacific continues to emerge as a dominant force, fueled by rapid industrialization and burgeoning chemical manufacturing sectors, while North America and Europe focus on regulatory compliance and high-performance applications.

- Increasing demand for high-octane gasoline additives to meet stricter emission standards.

- Growing utilization of DIB as an intermediate in the synthesis of advanced chemicals and polymers.

- Emphasis on sustainable production methods and greener chemical processes.

- Regional shifts in manufacturing capabilities, particularly towards Asia Pacific.

- Development of new derivatives for niche applications in lubricants and plasticizers.

AI Impact Analysis on Diisobutylene

The integration of Artificial Intelligence (AI) and machine learning technologies is poised to revolutionize various facets of the Diisobutylene market, primarily by enhancing operational efficiency, optimizing resource utilization, and accelerating research and development. Common inquiries surrounding AI's role often pertain to its potential in predictive maintenance for complex chemical plants, intelligent process control to minimize waste and energy consumption, and sophisticated data analysis for market forecasting and supply chain management. Stakeholders are keen to understand how AI can reduce production costs, improve product quality, and offer a competitive edge in a volatile market.

AI's influence extends to the design and discovery of new catalytic systems for DIB synthesis, where algorithms can screen vast chemical libraries and predict optimal reaction pathways far more rapidly than traditional experimental methods. This capability could lead to more efficient and environmentally friendly production processes. Moreover, AI-driven analytics are increasingly being employed to monitor market dynamics, anticipate demand fluctuations, and optimize logistics, thereby mitigating risks associated with raw material price volatility and supply chain disruptions.

- Optimization of Diisobutylene production processes through AI-driven predictive control, leading to improved yields and reduced energy consumption.

- Enhanced predictive maintenance schedules for chemical reactors and machinery, minimizing downtime and operational costs.

- AI-powered simulation and modeling for new DIB derivative development and application testing, accelerating product innovation.

- Improved supply chain visibility and risk management through AI-driven forecasting of raw material availability and demand.

- Automated quality control systems using computer vision and machine learning for consistent product specifications.

Key Takeaways Diisobutylene Market Size & Forecast

The Diisobutylene market is projected for substantial growth, driven by its versatile applications across multiple industries. A primary insight from the market forecast indicates that the increasing global demand for high-performance fuels and specialized chemical intermediates will be the core accelerator for market expansion. The market's resilience is underscored by its diverse end-uses, ranging from automotive applications to the production of various industrial chemicals, which collectively contribute to a stable and growing demand curve.

Furthermore, key takeaways highlight the strategic importance of regional markets, with emerging economies demonstrating significant potential for consumption growth due to rapid industrialization and infrastructure development. Companies are increasingly focusing on capacity expansion and technological advancements to capitalize on this burgeoning demand. The forecast also suggests a persistent emphasis on sustainable and efficient production methods to navigate evolving environmental regulations and meet consumer expectations for greener chemical products.

- Steady growth projected for the Diisobutylene market, driven by expanding applications in fuel additives and specialty chemicals.

- Asia Pacific remains a pivotal region for market growth, characterized by significant industrial expansion and increasing demand.

- Technological advancements in production processes and derivative synthesis will be crucial for competitive differentiation.

- Regulatory landscapes concerning environmental impact and fuel efficiency will continue to shape market dynamics.

- Diversification of end-use applications, particularly in polymer synthesis and advanced materials, offers long-term growth avenues.

Diisobutylene Market Drivers Analysis

The Diisobutylene market is primarily driven by its essential role as a high-octane blending component in gasoline and its versatile application as an intermediate in the synthesis of a wide array of specialty chemicals. The global automotive industry's continuous evolution, coupled with more stringent fuel efficiency and emission standards, significantly fuels the demand for DIB. Its ability to enhance fuel performance without contributing excessively to aromatic content makes it a preferred additive, particularly in regions focused on reducing environmental pollution from vehicular emissions. This sustained demand from the fuel sector forms a robust foundation for market expansion.

Beyond fuel applications, the burgeoning demand for specialty chemicals, including adhesives, lubricants, and various polymers, serves as another powerful driver. Diisobutylene is a crucial building block in the creation of these high-value products, which are integral to industries such as construction, packaging, and manufacturing. As these industries continue to grow globally, especially in developing economies, the need for DIB as a foundational chemical input escalates. The increasing investment in chemical manufacturing capacities worldwide further underpins the growth trajectory of the Diisobutylene market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for High-Octane Fuel Additives | +1.2% | Global, particularly APAC & North America | Mid-term to Long-term |

| Increasing Use in Specialty Chemical Synthesis | +1.0% | Global, especially China, India, Germany | Mid-term |

| Expansion of Automotive and Chemical Industries | +0.8% | Emerging Economies (APAC, Latin America) | Long-term |

| Advancements in Polymer and Rubber Manufacturing | +0.6% | Europe, North America, Japan | Mid-term |

Diisobutylene Market Restraints Analysis

The Diisobutylene market faces significant restraints primarily due to the volatility of raw material prices, particularly isobutylene, which is derived from crude oil. Fluctuations in global oil prices directly impact the cost of DIB production, leading to unpredictable manufacturing expenses and potentially narrowing profit margins for producers. This cost variability can deter new investments and complicate long-term strategic planning, making it challenging for market participants to maintain stable pricing and supply to end-users. The dependence on a fossil fuel-derived feedstock introduces inherent market instability.

Furthermore, stringent environmental regulations and increasing scrutiny over chemical manufacturing processes pose another substantial restraint. Regulatory bodies in various regions are implementing stricter controls on emissions, waste disposal, and the overall environmental footprint of chemical plants. Compliance with these evolving regulations often necessitates significant capital expenditure in new technologies and process upgrades, which can increase operational costs and, in some cases, limit production capacity. The search for greener alternatives or substitutes, driven by environmental concerns, also presents a long-term challenge to the market's traditional growth patterns.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Isobutylene) | -0.9% | Global | Short-term to Mid-term |

| Stringent Environmental Regulations | -0.7% | Europe, North America, Japan | Mid-term to Long-term |

| Availability of Substitute Fuel Additives | -0.5% | Global, particularly developed markets | Long-term |

| High Production Costs Associated with Purification | -0.4% | Global | Short-term |

Diisobutylene Market Opportunities Analysis

Significant opportunities in the Diisobutylene market stem from the continuous innovation in application development and the exploration of new end-use industries. Research and development efforts are increasingly focused on leveraging DIB's unique chemical properties to create novel derivatives for high-performance materials, such as advanced polymers, specialty resins, and sophisticated lubricant additives. These emerging applications, particularly in sectors like aerospace, electronics, and medical devices, represent high-value markets that can drive substantial growth and diversification for DIB producers.

Additionally, the expansion into rapidly developing economies presents a lucrative opportunity. Countries in Asia Pacific, Latin America, and the Middle East and Africa are experiencing substantial industrial growth, leading to increased demand for fuels and chemicals. Establishing production facilities or strengthening distribution networks in these regions can enable companies to tap into new customer bases and benefit from the rising consumption patterns. Furthermore, the push towards bio-based chemicals offers a long-term opportunity for DIB manufacturers to explore sustainable feedstock options, potentially mitigating dependency on fossil fuels and aligning with global sustainability initiatives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| R&D for New Diisobutylene Derivatives & Applications | +1.1% | Global, especially developed markets | Mid-term to Long-term |

| Expansion into Emerging Economies | +0.9% | APAC, Latin America, MEA | Mid-term |

| Development of Bio-based Diisobutylene Production | +0.7% | Europe, North America | Long-term |

| Strategic Partnerships and Collaborations | +0.5% | Global | Short-term to Mid-term |

Diisobutylene Market Challenges Impact Analysis

The Diisobutylene market faces several critical challenges, notably intense competition from alternative fuel additives and chemical intermediates. The market is characterized by the presence of various established products and newer innovations that can fulfill similar functional requirements, leading to pricing pressures and the need for continuous product differentiation. This competitive landscape demands significant investment in R&D and marketing to maintain market share, particularly when new regulations or technological breakthroughs favor alternative solutions, making it difficult for DIB to consistently outperform.

Another significant challenge is managing complex and often fragmented supply chains, which can be susceptible to disruptions from geopolitical events, natural disasters, or logistical bottlenecks. The global nature of DIB production and consumption necessitates robust supply chain management to ensure timely delivery and stable pricing, which is increasingly difficult given global uncertainties. Furthermore, the industry grapples with the need to address environmental concerns related to the production and use of DIB, including waste management and carbon footprint reduction, posing both regulatory and public perception hurdles that require ongoing commitment and innovation from manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Alternative Products | -0.8% | Global | Mid-term |

| Supply Chain Disruptions and Volatility | -0.6% | Global | Short-term to Mid-term |

| Managing Environmental and Sustainability Concerns | -0.5% | Europe, North America | Long-term |

| Technological Obsolescence Risks | -0.3% | Global | Long-term |

Diisobutylene Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Diisobutylene market, covering historical data, current market dynamics, and future projections. It delves into the market size, growth drivers, restraints, opportunities, and challenges, offering a holistic view of the industry landscape. The report segments the market by type, application, and end-use industry across key geographical regions, providing strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 780 Million |

| Market Forecast in 2033 | USD 1,320 Million |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | LyondellBasell Industries N.V., ExxonMobil Corporation, Shell plc, SI Group Inc., Chevron Phillips Chemical Company LLC, BASF SE, SABIC, The Dow Chemical Company, INEOS, Sumitomo Chemical Co., Ltd., LG Chem, Hanwha TotalEnergies Petrochemical Co., Ltd., Eni S.p.A., Braskem, Formosa Plastics Corporation, Indian Oil Corporation Ltd., Mitsubishi Chemical Corporation, PetroChina Company Limited, Repsol S.A., Sinopec Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Diisobutylene market is comprehensively segmented to provide granular insights into its various facets, enabling a detailed understanding of market dynamics across different product types, applications, and end-use industries. This segmentation helps in identifying specific growth pockets and understanding the influence of various factors on each segment. The analysis encompasses the chemical composition of DIB isomers, their functional roles in diverse applications, and their ultimate consumption by major industrial sectors, offering a multi-dimensional perspective of the market landscape.

- By Type: The market is segmented into 2,4,4-Trimethyl-1-pentene (Alpha-Diisobutylene), 2,4,4-Trimethyl-2-pentene (Beta-Diisobutylene), and mixed Diisobutylene isomers. Each isomer possesses distinct chemical properties and reactivity, influencing their specific applications.

- By Application: Key applications include fuel additives (as an octane booster in gasoline and a component in aviation fuel), specialty chemicals (for synthesizing neodecanoic acid and other complex molecules), polymer synthesis (particularly for polyisobutylene), adhesives & sealants, solvents & chemical intermediates, lubricant additives, and pharmaceuticals.

- By End-Use Industry: Major end-use industries driving demand are automotive (for fuel and material components), chemical & petrochemical (as a versatile building block), construction (in adhesives and sealants), packaging (for various polymers), pharmaceutical, oil & gas, and paints & coatings.

- By Region: The market is geographically segmented into North America, Europe, Asia Pacific (APAC), Latin America, and Middle East & Africa (MEA), analyzing regional consumption patterns, production capacities, and regulatory environments.

Regional Highlights

- Asia Pacific (APAC): Dominates the Diisobutylene market due to rapid industrialization, burgeoning automotive industries, and significant investments in chemical manufacturing, particularly in China, India, and Southeast Asian countries. The region's increasing demand for fuels and specialty chemicals fuels substantial market growth.

- North America: Characterized by a mature chemical industry, strong focus on high-performance fuel additives, and advanced research in new DIB derivatives. The U.S. remains a key consumer and innovator in the market, driven by stringent environmental regulations and demand for premium products.

- Europe: Holds a significant market share with a strong emphasis on regulatory compliance, sustainability, and high-value specialty chemical applications. Countries like Germany, France, and the Netherlands are at the forefront of DIB production and consumption, driven by their robust automotive and chemical sectors.

- Latin America: Expected to witness moderate growth, primarily driven by expanding petrochemical industries, increasing fuel consumption, and infrastructure development, with Brazil and Mexico being key contributors.

- Middle East & Africa (MEA): Shows emerging potential, propelled by investments in petrochemical capacities and growing energy demands, particularly in GCC countries seeking to diversify their economies beyond crude oil exports.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Diisobutylene Market.- LyondellBasell Industries N.V.

- ExxonMobil Corporation

- Shell plc

- SI Group Inc.

- Chevron Phillips Chemical Company LLC

- BASF SE

- SABIC

- The Dow Chemical Company

- INEOS

- Sumitomo Chemical Co., Ltd.

- LG Chem

- Hanwha TotalEnergies Petrochemical Co., Ltd.

- Eni S.p.A.

- Braskem

- Formosa Plastics Corporation

- Indian Oil Corporation Ltd.

- Mitsubishi Chemical Corporation

- PetroChina Company Limited

- Repsol S.A.

- Sinopec Corp.

Frequently Asked Questions

Analyze common user questions about the Diisobutylene market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Diisobutylene (DIB) and what are its primary uses?

Diisobutylene (DIB) refers to isomers of octene, primarily 2,4,4-trimethyl-1-pentene and 2,4,4-trimethyl-2-pentene, produced by the dimerization of isobutylene. Its main uses include acting as a high-octane blending component in gasoline to improve fuel efficiency and reduce emissions, and as a vital chemical intermediate in the synthesis of specialty chemicals like neodecanoic acid, plasticizers, and various polymers.

What is the current market size and projected growth rate of the Diisobutylene market?

The global Diisobutylene market is estimated at USD 780 Million in 2025 and is projected to reach USD 1,320 Million by 2033. It is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period from 2025 to 2033, driven by increasing demand in its diverse applications.

Which regions are key contributors to the Diisobutylene market growth?

Asia Pacific (APAC) is the leading region in terms of market growth, fueled by rapid industrialization and expansion of automotive and chemical industries in countries like China and India. North America and Europe also contribute significantly, driven by demand for high-performance fuels and specialty chemicals, alongside stringent environmental regulations.

What are the main drivers influencing the Diisobutylene market?

Key drivers include the growing global demand for high-octane gasoline additives to meet stricter fuel efficiency and emission standards, the increasing utilization of DIB as an intermediate in specialty chemical synthesis for various industries (e.g., construction, packaging), and the overall expansion of the automotive and chemical manufacturing sectors worldwide.

What challenges does the Diisobutylene market face?

The market faces challenges such as volatile raw material prices, particularly for isobutylene derived from crude oil, which impacts production costs. Additionally, stringent environmental regulations requiring significant investments in compliance, intense competition from alternative products, and potential supply chain disruptions pose ongoing hurdles for market players.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted