Diagnostic Audiometer Market

Diagnostic Audiometer Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706782 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Diagnostic Audiometer Market Size

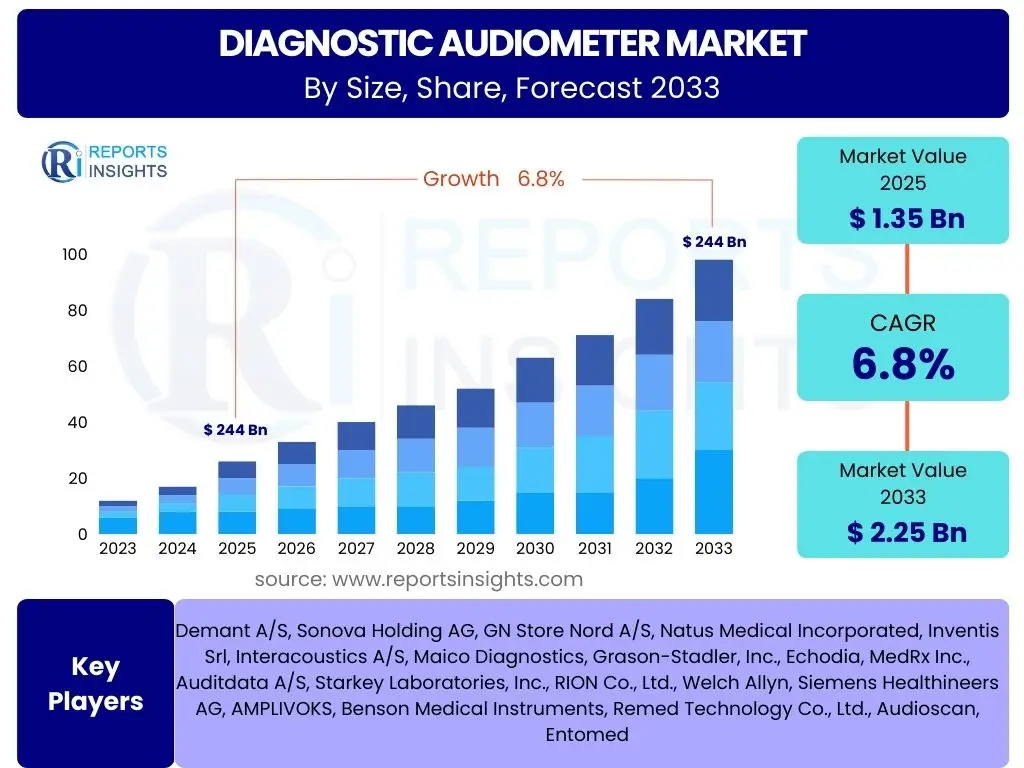

According to Reports Insights Consulting Pvt Ltd, The Diagnostic Audiometer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.35 Billion in 2025 and is projected to reach USD 2.25 Billion by the end of the forecast period in 2033.

Key Diagnostic Audiometer Market Trends & Insights

The Diagnostic Audiometer market is currently shaped by several transformative trends, primarily driven by technological advancements and evolving healthcare needs. A significant shift is observed towards more sophisticated, user-friendly, and portable devices, catering to both clinical and remote diagnostic requirements. This includes the integration of digital platforms and cloud connectivity, facilitating efficient data management and telemedicine capabilities, thereby expanding the accessibility of audiological services beyond traditional clinic settings.

Furthermore, the market is experiencing an increasing demand for automated and AI-assisted audiometry solutions, which aim to enhance diagnostic accuracy, reduce testing time, and lower the dependency on highly specialized personnel. There is also a growing emphasis on devices that offer comprehensive diagnostic capabilities, combining pure-tone audiometry with other tests like tympanometry and otoacoustic emissions (OAEs) within a single, integrated system. This trend reflects the need for more efficient and thorough diagnostic workflows in audiology clinics and hospitals.

Additionally, the market is witnessing the emergence of direct-to-consumer hearing health solutions, driven by increased public awareness regarding hearing loss and the availability of over-the-counter hearing aids. This indirectly influences the diagnostic audiometer market by increasing the need for initial screenings and professional diagnostic confirmations, often necessitating streamlined and accessible testing methods. The push for early detection and intervention, particularly in pediatric audiology and occupational health, also continues to drive innovation in screening and diagnostic equipment.

- Integration of advanced digital and cloud-based platforms for enhanced data management.

- Rising adoption of portable and handheld diagnostic audiometers for greater accessibility.

- Growing interest in AI-powered and automated audiometry for improved efficiency and accuracy.

- Expansion of telehealth and remote audiology services utilizing connected devices.

- Emphasis on multi-functional diagnostic systems combining various audiological tests.

- Increasing public awareness promoting early detection and intervention for hearing loss.

AI Impact Analysis on Diagnostic Audiometer

Artificial intelligence is poised to significantly revolutionize the Diagnostic Audiometer market, fundamentally altering the landscape of audiological assessment and management. User expectations surrounding AI's influence primarily revolve around enhanced diagnostic precision, automation of routine tasks, and the ability to process complex audiological data more efficiently. AI algorithms can analyze vast datasets from audiograms, patient histories, and other diagnostic tests to identify subtle patterns indicative of specific hearing conditions, potentially leading to earlier and more accurate diagnoses.

Concerns often center on data privacy, ethical considerations of autonomous diagnosis, and the need for robust validation of AI algorithms in clinical settings. Despite these considerations, the potential for AI to streamline workflows is immense. For instance, AI can automate parts of the audiometry testing process, such as stimulus presentation, response interpretation, and report generation, reducing the burden on clinicians and allowing them to focus on complex cases requiring expert human judgment. This automation can also improve consistency across different testers and clinics.

Furthermore, AI holds promise in predicting the progression of hearing loss and personalizing treatment plans, including the fine-tuning of hearing aids based on individual audiological profiles and lifestyle factors. It can also support in-depth research by uncovering new insights from aggregated anonymized patient data, driving innovation in both diagnostic tools and therapeutic interventions. The integration of AI will likely lead to a new generation of smart audiometers that are more intuitive, adaptable, and capable of providing comprehensive, data-driven insights, ultimately improving patient outcomes and expanding access to quality hearing healthcare.

- Enhanced diagnostic accuracy through AI-driven pattern recognition in audiometric data.

- Automation of testing protocols and preliminary result interpretation, increasing efficiency.

- Development of predictive models for hearing loss progression and personalized treatment.

- Streamlined data analysis and report generation, reducing clinician workload.

- Potential for remote diagnostics and tele-audiology supported by AI algorithms.

- Ethical considerations and data privacy challenges requiring robust frameworks.

Key Takeaways Diagnostic Audiometer Market Size & Forecast

The Diagnostic Audiometer market is on a robust growth trajectory, driven primarily by the escalating global prevalence of hearing impairments across all age groups and a heightened awareness regarding the importance of early detection. The forecast indicates sustained expansion, underpinned by continuous technological advancements that are making diagnostic tools more accessible, efficient, and precise. This growth is also significantly influenced by an aging global population, which disproportionately experiences age-related hearing loss, thereby creating a consistently expanding patient pool requiring audiological assessment.

Technological innovation, particularly in the realm of digitalization and portability, stands out as a critical accelerator for market expansion. The shift from traditional, bulky equipment to compact, PC-based, and even handheld devices is broadening the reach of diagnostic services, especially in underserved or remote areas. Furthermore, the increasing integration of AI and machine learning capabilities into audiometers is expected to deliver more accurate diagnoses and personalized treatment insights, solidifying the market's forward momentum.

While the market exhibits strong growth potential, it also faces challenges such as the high cost of advanced equipment and the need for skilled professionals. However, opportunities in emerging economies, coupled with favorable government initiatives promoting hearing health, are expected to mitigate these restraints. The market's future will largely be defined by its ability to balance technological sophistication with affordability and widespread accessibility, ensuring that diagnostic audiometry services can reach a larger segment of the global population in need.

- Market size projected to reach USD 2.25 Billion by 2033, indicating strong growth.

- Aging global population and rising hearing impairment prevalence are primary growth drivers.

- Technological advancements in portability, digitalization, and AI integration are key enablers.

- Significant opportunities exist in emerging markets and telehealth expansion.

- Market faces challenges related to high equipment costs and skilled personnel shortages.

- Focus on early detection and preventative care continues to drive demand for diagnostic tools.

Diagnostic Audiometer Market Drivers Analysis

The Diagnostic Audiometer market is propelled by a confluence of demographic shifts, technological innovations, and increasing healthcare awareness. The escalating global prevalence of hearing loss, particularly among the elderly population and due to noise-induced hearing damage in younger demographics, creates a consistent and expanding demand for diagnostic services. This demographic pressure is further compounded by a growing recognition of the impact of untreated hearing loss on quality of life, cognitive function, and social engagement, prompting greater seeking of professional assessment.

Technological advancements are another significant driver, leading to the development of more sophisticated, user-friendly, and versatile diagnostic audiometers. Innovations such as PC-based systems, portable devices, and the integration of advanced software for data analysis and management are enhancing the efficiency and accuracy of audiological testing. These technological improvements also support the expansion of telehealth and remote diagnostic capabilities, making services more accessible, especially in geographically dispersed or underserved regions, thus broadening the market reach.

Furthermore, increased healthcare expenditure, supportive government initiatives, and improved reimbursement policies in various regions are contributing to market growth. Public health campaigns promoting early detection of hearing impairments, along with mandatory newborn hearing screening programs in many countries, are driving the adoption of diagnostic audiometers in diverse clinical settings. The rising focus on preventive care and early intervention further fuels the demand for advanced and reliable diagnostic tools, securing the market's upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Hearing Loss | +1.5% | Global (North America, Europe, APAC) | 2025-2033 (Long-term) |

| Aging Global Population | +1.2% | North America, Europe, Japan, China | 2025-2033 (Long-term) |

| Technological Advancements & Portability | +1.0% | Global (Developed & Developing Economies) | 2025-2030 (Mid-term) |

| Rising Awareness & Early Detection Programs | +0.8% | Global (Especially Emerging Markets) | 2025-2033 (Long-term) |

| Growth in Healthcare Expenditure | +0.7% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

Diagnostic Audiometer Market Restraints Analysis

Despite robust growth drivers, the Diagnostic Audiometer market faces several notable restraints that could temper its expansion. One significant hurdle is the high initial cost of advanced diagnostic audiometers, which can be prohibitive for smaller clinics, individual practitioners, and healthcare facilities in developing economies with limited budgets. This capital expenditure, coupled with ongoing maintenance and calibration costs, can deter widespread adoption, particularly when simpler, more affordable screening tools might be considered sufficient for basic needs.

Another major restraint is the shortage of skilled audiologists and trained professionals required to operate and accurately interpret results from sophisticated diagnostic audiometers. Many regions, especially rural areas and emerging markets, lack sufficient qualified personnel, which restricts the effective utilization and accessibility of these devices. The complex nature of audiological diagnostics often necessitates specialized training, and the scarcity of such expertise can limit the reach of comprehensive hearing healthcare services, irrespective of device availability.

Furthermore, unfavorable reimbursement policies and a lack of adequate healthcare infrastructure in certain regions pose significant challenges. In some countries, reimbursement for audiological diagnostic tests may be limited or non-existent, impacting the economic viability for clinics to invest in new equipment. Moreover, stringent regulatory frameworks and lengthy approval processes for new devices can delay market entry and innovation, while the fragmented nature of healthcare systems in some parts of the world can create barriers to consistent adoption and utilization of diagnostic audiometers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Devices | -0.8% | Global (Especially Emerging & Low-Income Regions) | 2025-2033 (Long-term) |

| Shortage of Skilled Audiologists | -0.7% | Global (Particularly Rural Areas, Africa, Parts of Asia) | 2025-2033 (Long-term) |

| Limited Reimbursement Policies | -0.5% | Specific Regions (e.g., Parts of Asia, Latin America) | 2025-2030 (Mid-term) |

| Lack of Adequate Healthcare Infrastructure | -0.4% | Developing Countries (Africa, Southeast Asia) | 2025-2033 (Long-term) |

Diagnostic Audiometer Market Opportunities Analysis

The Diagnostic Audiometer market presents significant opportunities for growth and innovation, particularly through strategic geographical expansion and the integration of emerging technologies. Emerging economies, characterized by large populations, increasing healthcare expenditure, and improving awareness of hearing health, represent vast untapped markets. Countries in Asia Pacific, Latin America, and the Middle East and Africa are witnessing a rise in disposable incomes and a greater focus on upgrading healthcare infrastructure, providing fertile ground for the adoption of diagnostic audiometers, especially portable and cost-effective solutions.

Technological advancements, notably in AI, machine learning, and connectivity, offer substantial avenues for market expansion. The development of AI-powered diagnostic algorithms can enhance accuracy, automate testing procedures, and provide predictive insights, thereby improving clinical efficiency and patient outcomes. Furthermore, the increasing demand for telehealth and remote audiology services, particularly amplified by recent global health events, creates a strong opportunity for manufacturers to develop cloud-connected, easy-to-use devices that facilitate remote diagnostics and monitoring, broadening patient access to care.

Moreover, the integration of diagnostic audiometers with electronic health records (EHRs) and other healthcare IT systems can streamline workflows, improve data management, and facilitate comprehensive patient care. Opportunities also lie in developing specialized audiometers for specific applications, such as occupational health screening, military applications, and personalized hearing aid fitting. Collaborative efforts between manufacturers, healthcare providers, and research institutions can further accelerate the development of next-generation diagnostic tools and expand their clinical utility, addressing unmet needs in hearing healthcare globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Markets | +1.3% | Asia Pacific, Latin America, MEA | 2025-2033 (Long-term) |

| Integration of AI and Machine Learning | +1.0% | Global (Developed Economies Leading) | 2025-2030 (Mid-term) |

| Growth of Telehealth & Remote Audiology | +0.9% | North America, Europe, Asia Pacific | 2025-2030 (Mid-term) |

| Development of Portable & Home-based Solutions | +0.8% | Global (Especially Remote Areas) | 2025-2033 (Long-term) |

| Focus on Early Detection & Screening Programs | +0.7% | Global (Newborn Screening, Occupational Health) | 2025-2033 (Long-term) |

Diagnostic Audiometer Market Challenges Impact Analysis

The Diagnostic Audiometer market, while growing, faces several pertinent challenges that necessitate strategic navigation for sustained expansion. A significant challenge lies in the intense competitive landscape, characterized by numerous established players and new entrants vying for market share. This high level of competition often leads to price pressures and demands for continuous innovation, requiring manufacturers to invest heavily in research and development to maintain a competitive edge, which can be particularly challenging for smaller companies.

Another key challenge involves the complex regulatory environment and the need for stringent quality control measures. Diagnostic medical devices, including audiometers, are subject to rigorous regulatory approvals in various regions (e.g., FDA in the US, CE Mark in Europe). Navigating these diverse and often evolving regulatory pathways can be time-consuming and expensive, delaying market entry for new products and innovations. Ensuring compliance with cybersecurity standards for connected devices and data privacy regulations, such as GDPR and HIPAA, also adds layers of complexity.

Furthermore, the rapid pace of technological advancements, while an opportunity, also poses a challenge in terms of product obsolescence and the need for continuous upgrades. Healthcare providers may delay new purchases awaiting more advanced models or struggle with integrating legacy systems with newer technologies. Educating healthcare professionals on the effective use of sophisticated new devices and overcoming resistance to change also remain consistent challenges, requiring significant investment in training and technical support from manufacturers to ensure optimal adoption and utilization of diagnostic audiometers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Price Pressure | -0.6% | Global (Highly Competitive Developed Markets) | 2025-2030 (Mid-term) |

| Stringent Regulatory Landscape & Compliance | -0.5% | North America, Europe, China, Japan | 2025-2033 (Long-term) |

| Technological Obsolescence & Integration Issues | -0.4% | Global | 2025-2030 (Mid-term) |

| Data Security & Privacy Concerns (for connected devices) | -0.3% | Global | 2025-2033 (Long-term) |

| Limited Awareness and Adoption in Underserved Areas | -0.2% | Developing Regions, Rural Areas | 2025-2033 (Long-term) |

Diagnostic Audiometer Market - Updated Report Scope

This report provides an in-depth analysis of the Diagnostic Audiometer market, encompassing historical data from 2019 to 2023, current market estimations for 2024, and comprehensive forecasts extending to 2033. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders. Key market trends, the impact of artificial intelligence, and a thorough segmentation analysis by product type, device type, modality, and end-use are also covered. The geographical scope spans across major regions, providing a holistic view of regional dynamics and competitive landscapes.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 2.25 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Demant A/S, Sonova Holding AG, GN Store Nord A/S, Natus Medical Incorporated, Inventis Srl, Interacoustics A/S, Maico Diagnostics, Grason-Stadler, Inc., Echodia, MedRx Inc., Auditdata A/S, Starkey Laboratories, Inc., RION Co., Ltd., Welch Allyn, Siemens Healthineers AG, AMPLIVOKS, Benson Medical Instruments, Remed Technology Co., Ltd., Audioscan, Entomed |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Diagnostic Audiometer market is comprehensively segmented to provide granular insights into its diverse components, reflecting varied product offerings, technological applications, and end-user preferences. This segmentation highlights key growth areas and niche markets, enabling a deeper understanding of market dynamics and strategic opportunities. The market is primarily categorized by product type, device type, modality, and end-use, each with specific characteristics driving demand and adoption across different healthcare settings.

By product type, the market differentiates between stand-alone, PC-based, hybrid, and portable/handheld audiometers, indicating a shift towards more flexible and integrated solutions. Device type segmentation includes pure-tone, speech, impedance audiometers, and advanced Otoacoustic Emission (OAE) and Auditory Brainstem Response (ABR) devices, reflecting the diverse range of diagnostic capabilities required for comprehensive audiological assessment. Modality segmentation further distinguishes between air conduction and bone conduction testing methods, fundamental to diagnosing various types of hearing loss.

The end-use segment provides critical insight into where these devices are predominantly utilized, covering hospitals, specialized diagnostic centers, ENT clinics, research institutes, and increasingly, home care settings. Each segment presents unique market demands and regulatory considerations, influencing product development and distribution strategies. This detailed segmentation analysis is crucial for stakeholders to identify lucrative segments, tailor product offerings, and develop targeted marketing strategies to address specific market needs effectively.

- By Product Type:

- Stand-alone Audiometers: Traditional, self-contained units offering comprehensive diagnostic capabilities.

- PC-based Audiometers: Software-driven systems leveraging computer interfaces for enhanced functionality and data management.

- Hybrid Audiometers: Devices combining features of both stand-alone and PC-based systems, offering versatility.

- Portable/Handheld Audiometers: Compact and lightweight devices designed for screenings and diagnostics in mobile or remote settings.

- By Device Type:

- Pure-tone Audiometers: Used to determine hearing thresholds across various frequencies.

- Speech Audiometers: Assess a person's ability to hear and understand speech.

- Impedance Audiometers: Measure middle ear function (e.g., tympanometry, acoustic reflex testing).

- Otoacoustic Emission (OAE) Devices: Detect sounds produced by the inner ear, often used for newborn screening.

- Auditory Brainstem Response (ABR) Devices: Measure electrical activity in the brainstem in response to sound, used for objective hearing assessment.

- By Modality:

- Air Conduction: Tests how well sound travels through the outer and middle ear to the inner ear.

- Bone Conduction: Bypasses the outer and middle ear to test the inner ear directly.

- By End-use:

- Hospitals: Large healthcare facilities offering comprehensive audiology departments.

- Diagnostic Centers: Specialized centers focused solely on diagnostic testing services.

- ENT Clinics: Physician-led clinics specializing in ear, nose, and throat conditions.

- Research Institutes: Academic and private institutions conducting hearing-related research.

- Home Care Settings: Emerging segment driven by portable devices and telehealth for at-home diagnostics.

Regional Highlights

- North America: This region is a dominant force in the Diagnostic Audiometer market, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong emphasis on early diagnosis and treatment of hearing impairments. The presence of key market players, coupled with favorable reimbursement policies and increasing awareness campaigns, drives significant adoption of sophisticated diagnostic devices. The aging population and the prevalence of noise-induced hearing loss further contribute to consistent market growth, especially in the United States and Canada, where technological innovation and adoption rates are high.

- Europe: Europe represents a mature market for diagnostic audiometers, exhibiting steady growth influenced by comprehensive healthcare systems, robust R&D activities, and a high incidence of age-related hearing loss. Countries like Germany, the UK, France, and Nordic nations are key contributors, driven by government initiatives for hearing health and an increasing focus on integrated care pathways. The region is also witnessing a surge in demand for portable and PC-based audiometers due to their flexibility and efficiency in diverse clinical settings, including community clinics and private practices.

- Asia Pacific (APAC): The APAC region is poised for significant and rapid growth in the Diagnostic Audiometer market, primarily due to its large and aging population, improving healthcare access, and rising awareness about hearing health. Countries such as China, India, Japan, and South Korea are key growth engines, spurred by increasing healthcare investments, a growing number of diagnostic centers, and the expanding presence of international and domestic manufacturers. The demand for cost-effective yet efficient solutions, including portable audiometers, is particularly high in this region to cater to its vast and diverse patient base, including rural areas.

- Latin America: This region is an emerging market for diagnostic audiometers, driven by improvements in healthcare infrastructure, increasing healthcare spending, and a growing recognition of hearing health issues. Countries like Brazil, Mexico, and Argentina are leading the adoption of diagnostic audiometers. While market penetration is still lower compared to developed regions, the rising prevalence of hearing loss and efforts to expand access to diagnostic services create substantial opportunities for market expansion, particularly for affordable and user-friendly devices.

- Middle East and Africa (MEA): The MEA region presents nascent but growing opportunities in the Diagnostic Audiometer market. Growth is primarily driven by increasing healthcare investments, developing medical tourism, and a rising focus on enhancing healthcare infrastructure in countries such as Saudi Arabia, UAE, and South Africa. Challenges related to limited awareness and economic disparities in certain sub-regions persist, yet ongoing efforts to improve healthcare accessibility and awareness campaigns for hearing health are expected to stimulate future market growth for diagnostic audiometers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Diagnostic Audiometer Market.- Demant A/S

- Sonova Holding AG

- GN Store Nord A/S

- Natus Medical Incorporated

- Inventis Srl

- Interacoustics A/S

- Maico Diagnostics

- Grason-Stadler, Inc.

- Echodia

- MedRx Inc.

- Auditdata A/S

- Starkey Laboratories, Inc.

- RION Co., Ltd.

- Welch Allyn

- Siemens Healthineers AG

- AMPLIVOKS

- Benson Medical Instruments

- Remed Technology Co., Ltd.

- Audioscan

- Entomed

Frequently Asked Questions

What is a Diagnostic Audiometer?

A Diagnostic Audiometer is a specialized electronic device used by audiologists and other healthcare professionals to measure a person's hearing sensitivity and identify the presence and type of hearing loss. It produces pure tones, speech, and other sounds at various frequencies and intensities to determine the softest sounds an individual can hear, providing a detailed audiogram.

What are the different types of Diagnostic Audiometers?

Diagnostic audiometers come in several types, including stand-alone units for comprehensive clinical use, PC-based audiometers that integrate with computer software for advanced functionality, and portable or handheld audiometers designed for screening and mobile testing. They also vary by the specific tests they perform, such as pure-tone, speech, impedance (tympanometry), Otoacoustic Emission (OAE), and Auditory Brainstem Response (ABR) devices.

Who uses Diagnostic Audiometers?

Diagnostic audiometers are primarily used by audiologists, otolaryngologists (ENT doctors), and other hearing healthcare professionals in various settings including hospitals, specialized diagnostic centers, private ENT clinics, schools for hearing screenings, and research institutions. Increasingly, portable versions are also used by primary care physicians and in home care settings for preliminary assessments.

What is the projected growth rate of the Diagnostic Audiometer market?

The Diagnostic Audiometer market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. This growth is driven by factors such as the increasing prevalence of hearing loss globally, an aging population, technological advancements in device capabilities, and rising awareness regarding the importance of early diagnosis and intervention.

What key trends are influencing the Diagnostic Audiometer market?

Key trends influencing the Diagnostic Audiometer market include the increasing adoption of portable and PC-based audiometers for improved accessibility, the integration of artificial intelligence (AI) and machine learning for enhanced diagnostic accuracy, the expansion of telehealth and remote audiology services, and the development of multi-functional diagnostic systems that combine various audiological tests into single units.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted