Dental Compressor Market

Dental Compressor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709213 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

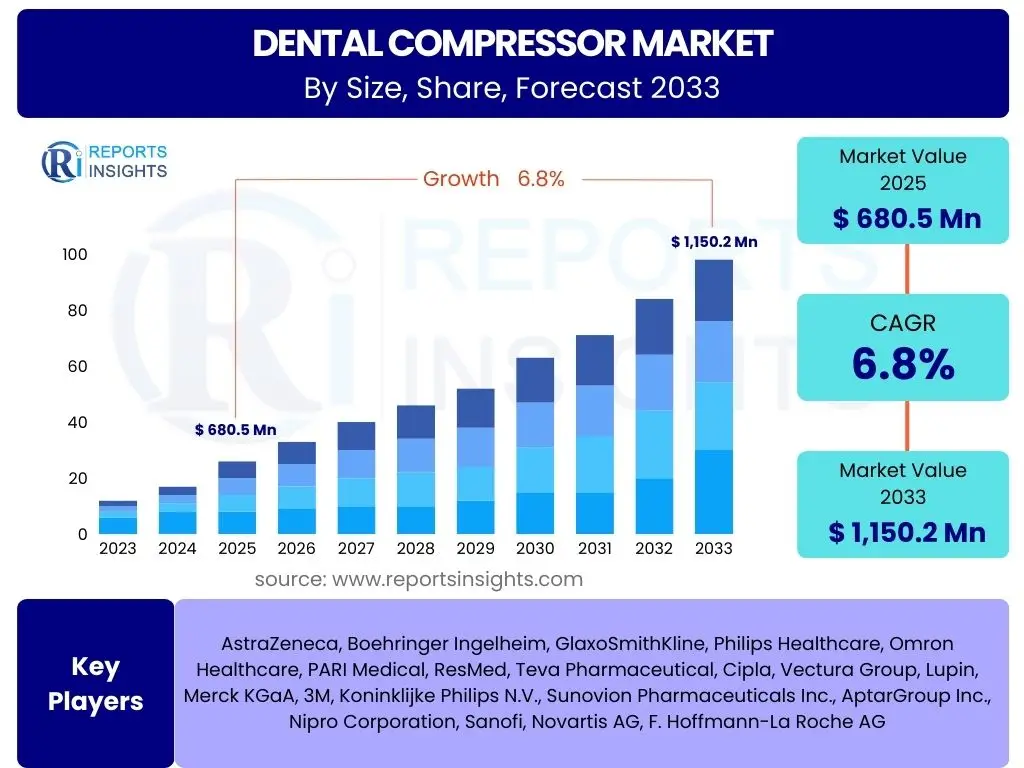

Dental Compressor Market Size

According to Reports Insights Consulting Pvt Ltd, The Dental Compressor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 680.5 Million in 2025 and is projected to reach USD 1,150.2 Million by the end of the forecast period in 2033.

Key Dental Compressor Market Trends & Insights

The dental compressor market is experiencing significant evolution driven by technological advancements and shifting clinical requirements. A prominent trend involves the increasing demand for oil-free and silent compressors, crucial for maintaining aseptic conditions in dental environments and ensuring patient comfort. Furthermore, there's a growing emphasis on energy efficiency and sustainability, compelling manufacturers to innovate with more environmentally friendly and cost-effective solutions. The integration of compressors with advanced digital dentistry workflows and CAD/CAM systems is also becoming a critical aspect, supporting the precise and sophisticated demands of modern dental practices.

Market insights suggest a strong focus on enhancing the reliability and longevity of dental compressors, with features such as predictive maintenance and IoT connectivity gaining traction. The shift towards portable and compact units is also observed, especially for mobile dental clinics and smaller practices where space is a premium. Moreover, the global expansion of dental tourism and increasing awareness of oral hygiene in developing regions are fueling the adoption of high-quality dental equipment, including compressors, indicating a robust growth trajectory for the market.

- Growing demand for oil-free and silent compressor technologies.

- Increased focus on energy-efficient and environmentally sustainable compressor solutions.

- Enhanced integration of dental compressors with digital dentistry and CAD/CAM systems.

- Rising adoption of portable and compact compressor units for diverse clinical settings.

- Emphasis on advanced features like predictive maintenance and IoT connectivity for improved reliability.

AI Impact Analysis on Dental Compressor

The integration of Artificial Intelligence (AI) in the dental compressor domain, while nascent, holds substantial promise for revolutionizing operational efficiency and maintenance. Users are increasingly curious about how AI can contribute to predictive diagnostics, allowing for early detection of potential equipment failures and enabling proactive maintenance schedules. This shift from reactive to preventive maintenance could significantly reduce downtime, extend the lifespan of compressors, and optimize operational costs for dental practices. AI algorithms could analyze performance data, such as pressure fluctuations, motor temperature, and operational hours, to identify patterns indicative of impending issues, thereby enhancing the reliability of critical dental infrastructure.

Beyond maintenance, AI is also anticipated to play a role in optimizing energy consumption and operational parameters of dental compressors. Intelligent systems could learn usage patterns within a clinic, adjusting compressor output to match real-time demand, thereby minimizing energy waste. Furthermore, AI could facilitate seamless integration of compressors into smart dental clinics, allowing for automated control and remote monitoring, which enhances convenience and operational oversight. While the direct application of AI in the mechanical function of compressors is still developing, its impact on the data-driven aspects of management, efficiency, and maintenance is expected to be transformative, shaping the future of dental equipment. The focus remains on making dental clinics smarter, more efficient, and less prone to unexpected equipment failures through intelligent systems.

- AI-powered predictive maintenance for early fault detection and reduced downtime.

- Optimization of energy consumption through intelligent operational adjustments based on usage patterns.

- Integration into smart dental clinic ecosystems for automated control and remote monitoring.

- Enhanced diagnostic capabilities for improved compressor lifespan and reliability.

- Data-driven insights for efficient resource management and operational cost reduction.

Key Takeaways Dental Compressor Market Size & Forecast

The dental compressor market is poised for robust growth, driven by an expanding global demand for dental services and continuous technological advancements. A crucial takeaway is the significant shift towards oil-free and silent compressor models, reflecting a strong market preference for aseptic and patient-friendly environments. This trend is not merely about compliance but also about enhancing the overall quality of care and clinic efficiency, making these features critical differentiators for manufacturers and essential considerations for purchasers. The forecast underscores the importance of innovation in meeting the evolving needs of modern dentistry, particularly with the increasing sophistication of dental procedures and the rise of digital integration.

Another key insight is the regional variance in market growth and adoption rates. While developed economies continue to lead in embracing advanced compressor technologies, emerging markets are rapidly catching up due to increasing healthcare expenditure and a growing middle class with greater access to dental care. This dual growth trajectory presents both opportunities for market penetration in new geographies and challenges in adapting products to diverse regulatory and economic landscapes. Stakeholders must consider the long-term impact of sustainability initiatives and the potential for AI-driven enhancements to maintain competitiveness and capitalize on future market expansion. The market's resilience is further supported by the fundamental and irreplaceable role dental compressors play in virtually every dental procedure, ensuring a steady baseline demand that is consistently amplified by innovation.

- Sustained market expansion driven by increasing global dental care demand.

- Dominant shift towards oil-free and silent dental compressor technologies.

- Critical importance of technological innovation to meet modern dental practice requirements.

- Significant growth opportunities in emerging economies due to rising healthcare spending.

- Potential for AI and IoT integration to redefine maintenance and operational efficiency.

Dental Compressor Market Drivers Analysis

The dental compressor market is significantly propelled by several key factors that underscore the essential role of these devices in modern dentistry. A primary driver is the global increase in dental procedures, encompassing routine check-ups, restorative treatments, and cosmetic dentistry. This surge is attributed to rising awareness of oral health, an aging global population retaining more natural teeth, and the expansion of dental insurance coverage. As the volume and complexity of dental interventions grow, so does the demand for reliable and efficient dental compressors, which are indispensable for powering various dental tools and equipment.

Technological advancements also serve as a crucial market driver, with continuous innovation leading to the development of more sophisticated, quieter, and energy-efficient compressors. The shift towards oil-free compressors, for instance, addresses critical concerns regarding air quality and maintenance in dental settings, providing a cleaner and safer environment for both patients and practitioners. Furthermore, the burgeoning field of digital dentistry, including CAD/CAM systems and intraoral scanners, relies heavily on a consistent supply of clean, dry compressed air, thereby directly stimulating demand for high-performance compressors that can meet these exacting technical requirements. These innovations not only improve operational efficiency but also enhance patient experience, further driving market adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing prevalence of dental diseases and oral health awareness | +1.2% | Global, particularly Asia Pacific & Latin America | Short to Mid-term (2025-2029) |

| Technological advancements in dental compressor design (e.g., oil-free, silent) | +1.0% | North America, Europe, Developed Asia Pacific | Mid to Long-term (2027-2033) |

| Growing adoption of advanced digital dentistry solutions (CAD/CAM) | +0.9% | Global, especially high-income countries | Mid-term (2026-2030) |

| Expansion of dental clinics and hospitals globally | +0.8% | Asia Pacific, Latin America, Middle East & Africa | Short to Mid-term (2025-2029) |

| Rising disposable income and access to dental care services | +0.7% | Emerging economies, developing countries | Long-term (2028-2033) |

Dental Compressor Market Restraints Analysis

Despite the positive growth trajectory, the dental compressor market faces several significant restraints that could impede its expansion. One primary challenge is the relatively high initial investment cost associated with advanced dental compressors, particularly oil-free and high-performance models. This cost can be a substantial barrier for smaller dental practices or those in developing regions with limited budgets, potentially leading them to opt for less sophisticated or older technologies, or to delay equipment upgrades. The economic sensitivity of dental practices, often operating on tight margins, makes capital expenditure a critical decision point that can influence purchasing patterns and market penetration.

Another notable restraint is the stringent regulatory landscape governing medical devices, including dental compressors, which necessitates adherence to various quality standards, certifications, and environmental regulations. Compliance can be costly and time-consuming for manufacturers, affecting product development cycles and market entry. Furthermore, the operational and maintenance expenses associated with dental compressors, including energy consumption, filter replacements, and periodic servicing, can add to the overall cost of ownership. These ongoing expenses, coupled with the potential for technical issues requiring specialized repair, can deter some practices from investing in premium or more complex systems, thereby somewhat limiting the market's full potential for growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment for advanced compressor systems | -0.8% | Global, particularly smaller clinics in developing regions | Short to Mid-term (2025-2029) |

| Stringent regulatory approvals and compliance standards | -0.6% | North America, Europe | Mid-term (2026-2030) |

| Maintenance and operational costs (energy, filter replacement) | -0.5% | Global | Ongoing |

| Intense market competition leading to price pressure | -0.4% | Global | Short to Long-term (2025-2033) |

| Limited awareness or adoption of advanced technologies in underserved markets | -0.3% | Certain parts of Asia Pacific, Latin America, MEA | Long-term (2028-2033) |

Dental Compressor Market Opportunities Analysis

The dental compressor market presents several compelling opportunities for growth and innovation, driven by evolving dental practices and technological advancements. One significant opportunity lies in the expanding demand for silent and oil-free compressors, as dental professionals increasingly prioritize a quiet, sterile, and comfortable environment for patients and staff. Manufacturers who can deliver highly efficient, low-noise, and truly oil-free solutions will find a receptive market, particularly in established regions with high standards for clinical practice. This preference is further amplified by the growing focus on environmental responsibility and occupational health within healthcare settings.

Moreover, the burgeoning markets in Asia Pacific, Latin America, and the Middle East & Africa offer substantial growth prospects. These regions are experiencing rapid economic development, increasing healthcare infrastructure investments, and a rising middle class with greater access to and demand for modern dental care. This demographic shift translates into a need for new dental clinics and equipment, including compressors, providing a fertile ground for market penetration and expansion. Furthermore, the development of smart compressors with IoT capabilities, enabling remote monitoring, predictive maintenance, and optimized performance, represents a significant technological opportunity to enhance product value and create new service revenue streams. The integration of these smart features can cater to the increasing digitalization of dental practices, offering efficiencies that were previously unattainable.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for silent and oil-free compressors in advanced clinics | +1.1% | North America, Europe, Japan | Short to Mid-term (2025-2029) |

| Untapped markets in emerging economies (Asia Pacific, Latin America) | +1.0% | Asia Pacific, Latin America, MEA | Mid to Long-term (2027-2033) |

| Development of smart compressors with IoT and AI for predictive maintenance | +0.9% | Global, particularly tech-forward markets | Mid to Long-term (2027-2033) |

| Increasing adoption of portable and compact compressor solutions | +0.8% | Rural areas, mobile clinics, smaller practices globally | Short to Mid-term (2025-2030) |

| Focus on energy-efficient and eco-friendly compressor models | +0.7% | Europe, North America | Long-term (2028-2033) |

Dental Compressor Market Challenges Impact Analysis

The dental compressor market is not without its challenges, which can impact manufacturers' strategies and market dynamics. One significant challenge is managing the complexities of the global supply chain, which has been susceptible to disruptions in recent years. Fluctuations in raw material prices, availability of electronic components, and logistical bottlenecks can lead to increased production costs and delays, ultimately affecting product availability and market pricing. This volatility demands robust supply chain management and diversification strategies from key players to ensure consistent production and timely delivery.

Another substantial challenge is the intense competitive landscape, characterized by numerous regional and international players. This fierce competition often leads to price wars, diminishing profit margins for manufacturers and making it difficult for new entrants to establish a foothold. Furthermore, the rapid pace of technological change necessitates continuous research and development, which requires significant investment. Keeping up with evolving customer expectations for quieter, more efficient, and digitally integrated solutions, while balancing cost-effectiveness, remains a perpetual challenge. Additionally, the presence of low-quality or counterfeit products, particularly in unregulated markets, poses risks to patient safety and can erode trust in established brands, making it harder for reputable companies to differentiate their offerings and maintain market share.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply chain disruptions and raw material price volatility | -0.7% | Global | Short to Mid-term (2025-2028) |

| Intense competition and price pressure from local manufacturers | -0.6% | Asia Pacific, Europe | Short to Long-term (2025-2033) |

| Rapid technological obsolescence and need for continuous R&D | -0.5% | Global | Ongoing |

| Regulatory complexities and varying standards across regions | -0.4% | North America, Europe, emerging markets | Mid-term (2026-2030) |

| Managing the perception and adoption of newer, costlier technologies | -0.3% | Global, particularly smaller clinics | Long-term (2028-2033) |

Dental Compressor Market - Updated Report Scope

This updated report provides an in-depth, holistic analysis of the global Dental Compressor Market, examining its current size, historical performance, and future growth projections from 2025 to 2033. It comprehensively covers key market trends, significant growth drivers, prevailing restraints, emerging opportunities, and critical challenges impacting the industry landscape. The scope extends to a detailed segmentation analysis by type, technology, application, end-user, and portability, offering granular insights into various market facets. Furthermore, the report includes an exhaustive regional analysis across major geographies and profiles leading market players, presenting a strategic overview for stakeholders. The objective is to equip businesses with actionable intelligence to navigate market dynamics, identify growth avenues, and formulate informed strategies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 680.5 Million |

| Market Forecast in 2033 | USD 1,150.2 Million |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Dürr Dental, KaVo (a subsidiary of Envista Holdings Corporation), Gnatus, Air Techniques, Midmark Corporation, Belmont Equipment, Metasys, DentalEZ, Cattani S.p.A., Bambi Air Compressors, Werther International S.r.l., Woson Medical Instrument, Yoshida Dental Mfg. Co., Ltd., Fedesa, TECNODENT S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The dental compressor market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for a detailed analysis of market dynamics across various product types, technological platforms, end-user applications, and geographic regions. By breaking down the market into these distinct categories, stakeholders can identify specific growth pockets, understand competitive landscapes, and tailor their strategies to target particular market niches. This comprehensive approach ensures that all influential factors contributing to the market's evolution are thoroughly examined.

The segmentation extends to differentiating between oil-lubricated and oil-free compressors, reflecting a significant trend towards cleaner air delivery in dental practices. Furthermore, the analysis by technology, encompassing reciprocating/piston, screw, scroll, and rotary vane compressors, highlights the varying performance characteristics and applications of each type. Segmentation by application and end-user provides insight into demand patterns from dental laboratories, hospitals, clinics, and academic institutions, while the portability segment distinguishes between stationary and portable units, addressing diverse operational needs from large facilities to mobile dental services. This multi-dimensional segmentation is crucial for an exhaustive market assessment and strategic planning.

- By Type:

- Oil-Lubricated

- Oil-Free

- By Technology:

- Reciprocating/Piston

- Screw

- Scroll

- Rotary Vane

- By Application:

- Dental Laboratories

- Dental Hospitals

- Dental Clinics

- Academic & Research Institutes

- By End-User:

- Dental Hospitals

- Dental Clinics

- Academic & Research Institutes

- By Portability:

- Stationary

- Portable

Regional Highlights

- North America: This region consistently leads the dental compressor market, primarily driven by high healthcare expenditure, widespread adoption of advanced dental technologies, and a strong presence of key market players. The demand for technologically sophisticated, oil-free, and silent compressors is particularly high due to stringent regulatory standards and a focus on superior patient care.

- Europe: Europe represents a mature market with significant demand for high-quality dental equipment. Factors such as an aging population requiring extensive dental care, increasing cosmetic dentistry procedures, and a robust framework for healthcare infrastructure contribute to steady market growth. Emphasis on energy efficiency and environmental compliance drives innovation in this region.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rising disposable incomes, increasing awareness of oral hygiene, and the expansion of dental tourism. Countries like China, India, and South Korea are witnessing rapid development in healthcare infrastructure and a growing number of dental clinics, leading to high adoption rates of new equipment.

- Latin America: This region is an emerging market characterized by improving economic conditions, government initiatives to enhance access to dental care, and a growing middle class. While price sensitivity remains a factor, there is an increasing demand for reliable and affordable dental compressors to support expanding dental services.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, primarily due to developing healthcare infrastructure, increasing investment in medical tourism, and government efforts to modernize healthcare facilities. The adoption of advanced dental equipment, including compressors, is on the rise, albeit at a slower pace compared to other emerging regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Dental Compressor Market.- Dürr Dental

- KaVo (a subsidiary of Envista Holdings Corporation)

- Gnatus

- Air Techniques

- Midmark Corporation

- Belmont Equipment

- Metasys

- DentalEZ

- Cattani S.p.A.

- Bambi Air Compressors

- Werther International S.r.l.

- Woson Medical Instrument

- Yoshida Dental Mfg. Co., Ltd.

- Fedesa

- TECNODENT S.p.A.

Frequently Asked Questions

What is a dental compressor and why is it essential for dental practices?

A dental compressor is a specialized air compressor designed to provide a continuous supply of clean, dry, and oil-free compressed air, which is vital for operating various dental tools such as drills, scalers, and air-water syringes. It is essential because standard compressors can introduce oil or moisture, which can contaminate dental procedures and damage delicate equipment, making the quality of air from a dental compressor paramount for patient safety and instrument longevity.

What are the primary advantages of an oil-free dental compressor?

Oil-free dental compressors offer several key advantages, including delivering pure, uncontaminated air essential for aseptic dental environments, eliminating the need for oil changes and associated maintenance, and reducing the risk of equipment damage from oil residue. They contribute to a cleaner, safer clinical setting and often operate more quietly, enhancing both patient comfort and staff working conditions.

How frequently should a dental compressor be serviced?

The service frequency for a dental compressor typically depends on its model, usage intensity, and manufacturer recommendations, but generally, it should be serviced annually or every 2,000 operational hours. Regular maintenance includes checking air filters, inspecting air lines, draining the tank to prevent moisture buildup, and verifying pressure settings to ensure optimal performance and longevity.

What factors should be considered when choosing a dental compressor?

Key factors to consider include the compressor's capacity (liters per minute or cubic feet per minute) relative to the number of dental chairs it will supply, whether it is oil-free or oil-lubricated, noise level (measured in decibels), tank size, energy efficiency, and required maintenance. Additionally, considering the warranty, after-sales support, and compatibility with existing dental equipment is crucial for long-term satisfaction.

What is the market outlook for dental compressors in the coming years?

The market outlook for dental compressors is positive, with projected steady growth driven by the increasing global demand for dental care, technological advancements leading to more efficient and silent units, and the expansion of digital dentistry. The market is expected to benefit from rising oral health awareness, growth in dental tourism, and infrastructure development in emerging economies, alongside a continuous shift towards oil-free and smart compressor technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted