Cardiac Surgery and Heart Valve Device Market

Cardiac Surgery and Heart Valve Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708774 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

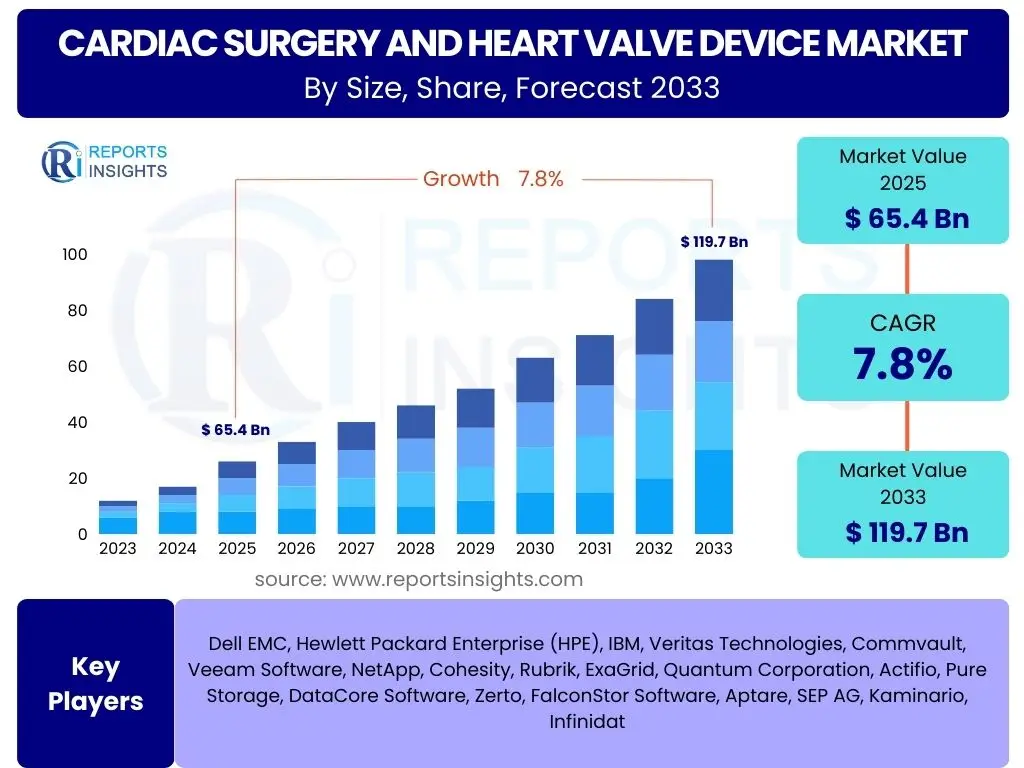

Cardiac Surgery and Heart Valve Device Market Size

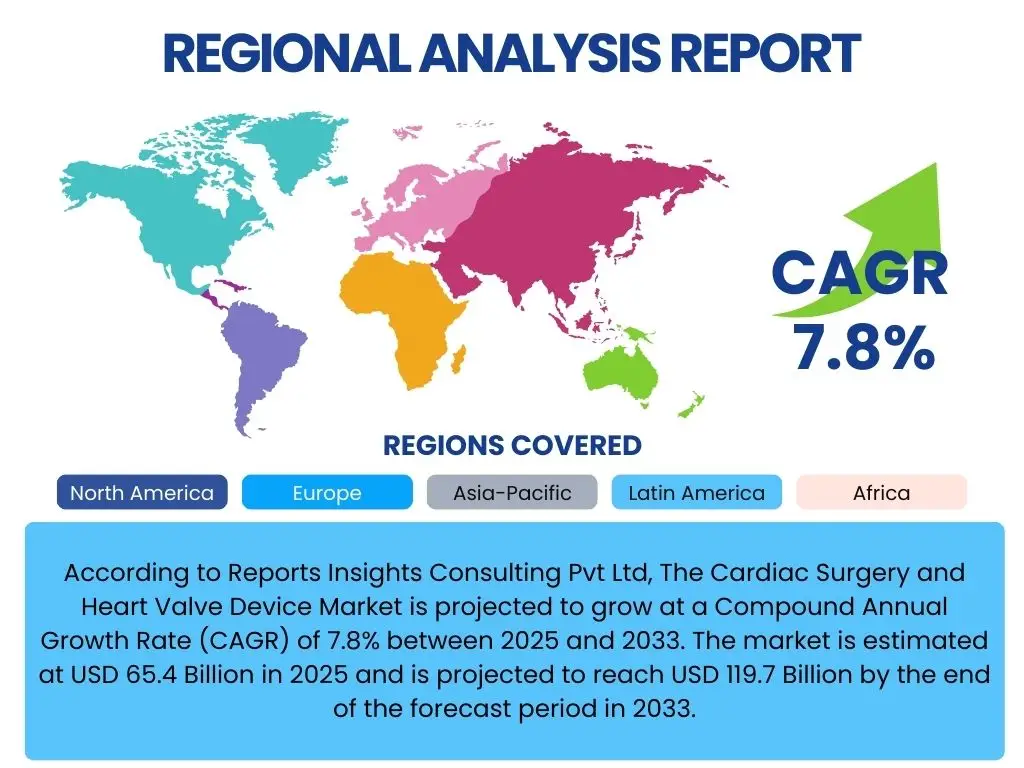

According to Reports Insights Consulting Pvt Ltd, The Cardiac Surgery and Heart Valve Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 65.4 Billion in 2025 and is projected to reach USD 119.7 Billion by the end of the forecast period in 2033.

Key Cardiac Surgery and Heart Valve Device Market Trends & Insights

The cardiac surgery and heart valve device market is currently experiencing significant transformative shifts driven by continuous innovation and evolving patient demographics. A primary trend involves the increasing adoption of minimally invasive surgical techniques, such as Transcatheter Aortic Valve Implantation (TAVI) and Transcatheter Mitral Valve Repair (TMVr), which offer reduced recovery times, lower complication rates, and improved patient outcomes compared to traditional open-heart surgery. These advancements are responding to a growing demand for less invasive treatment options, particularly among an aging patient population with comorbidities.

Furthermore, there is a distinct move towards personalization in cardiac care, with devices and procedures being tailored to individual patient anatomies and specific disease profiles. This includes the development of more advanced imaging technologies for precise pre-operative planning and the creation of custom-fitted devices. The integration of digital health solutions, including remote monitoring and telemedicine, is also gaining traction, enabling better post-operative care and long-term management of cardiac conditions, thereby enhancing patient engagement and improving overall clinical efficiency.

- Shift towards minimally invasive procedures (e.g., TAVI, TMVr).

- Increased adoption of transcatheter technologies for valve repair and replacement.

- Rising demand for personalized and patient-specific cardiac devices.

- Advancements in cardiac imaging for enhanced diagnostic accuracy and procedural guidance.

- Growing integration of digital health and remote patient monitoring solutions.

AI Impact Analysis on Cardiac Surgery and Heart Valve Device

Artificial intelligence is poised to profoundly transform the cardiac surgery and heart valve device market by enhancing precision, efficiency, and diagnostic capabilities across the entire patient care continuum. AI algorithms are increasingly being utilized in the pre-operative phase for advanced image analysis, enabling more accurate diagnosis of cardiac conditions, precise anatomical mapping, and predictive modeling for surgical outcomes. This allows surgeons to develop highly personalized treatment plans and select the most appropriate devices, significantly reducing the risk of complications and optimizing procedural success.

During surgical interventions, AI-powered robotic systems are assisting surgeons by providing enhanced dexterity, tremor filtration, and real-time guidance, leading to more controlled and precise movements, especially in complex minimally invasive procedures. Post-operatively, AI is instrumental in analyzing patient data from wearables and monitoring devices to detect early signs of complications, predict potential readmissions, and personalize rehabilitation protocols. While AI's integration promises substantial improvements, it also brings considerations regarding data security, algorithmic bias, and the need for robust regulatory frameworks to ensure patient safety and ethical implementation.

- Enhanced diagnostic accuracy and predictive analytics for cardiac conditions.

- AI-guided surgical planning and real-time procedural assistance for improved precision.

- Optimization of device selection and personalized treatment strategies.

- Automated analysis of post-operative patient data for early complication detection.

- Development of smart devices with integrated AI for adaptive functionality.

Key Takeaways Cardiac Surgery and Heart Valve Device Market Size & Forecast

The cardiac surgery and heart valve device market is on a robust growth trajectory, primarily fueled by an aging global population and the escalating prevalence of cardiovascular diseases. A key takeaway is the consistent shift towards advanced, less invasive treatment modalities, which are driving market expansion by broadening the eligible patient pool and improving patient acceptance of interventions. Stakeholders must therefore prioritize investment in research and development for innovative transcatheter technologies and advanced diagnostic tools to capitalize on these evolving clinical needs.

Another critical insight is the increasing emphasis on value-based care models, which necessitate devices and procedures that demonstrate clear clinical efficacy and cost-effectiveness. This trend encourages manufacturers to develop solutions that not only offer superior outcomes but also contribute to reduced hospital stays and lower overall healthcare costs. Furthermore, the market's future growth will be significantly influenced by geographic expansion into emerging economies, where improving healthcare infrastructure and increasing awareness present substantial untapped potential for device adoption.

- Strong market growth driven by demographic shifts and rising CVD incidence.

- Minimally invasive therapies represent a significant growth catalyst.

- Innovation in device technology and procedural techniques remains paramount.

- Focus on patient outcomes and cost-efficiency in product development.

- Emerging markets offer substantial growth opportunities for expansion.

Cardiac Surgery and Heart Valve Device Market Drivers Analysis

The cardiac surgery and heart valve device market is significantly propelled by several key factors. The global increase in the geriatric population, which is inherently more susceptible to cardiovascular diseases, directly translates into a higher demand for cardiac surgical procedures and valve replacement devices. Concurrently, the rising global burden of cardiovascular diseases (CVDs), including valvular heart disease, coronary artery disease, and heart failure, necessitates effective interventional and surgical solutions, thereby fueling market growth. Technological advancements, particularly in the realm of minimally invasive surgical techniques and transcatheter heart valve therapies, are also crucial drivers, offering patients safer and more effective treatment options with faster recovery times, which expands the patient base willing to undergo intervention.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Geriatric Population | +1.5% | Global, particularly developed regions (North America, Europe, Japan) | Long-term (2025-2033) |

| Rising Prevalence of Cardiovascular Diseases | +1.2% | Global, with rapid growth in emerging economies (APAC, Latin America) | Mid-to-Long term (2025-2033) |

| Technological Advancements in Minimally Invasive Procedures | +1.8% | North America, Europe, Asia Pacific (innovators & early adopters) | Short-to-Long term (2025-2033) |

| Growing Awareness and Improved Diagnosis of Valvular Heart Disease | +0.8% | Developing economies with expanding healthcare access | Mid-term (2027-2033) |

Cardiac Surgery and Heart Valve Device Market Restraints Analysis

Despite robust growth drivers, the cardiac surgery and heart valve device market faces several significant restraints that could temper its expansion. The high cost associated with advanced cardiac devices and surgical procedures remains a substantial barrier, limiting access for a large segment of the population, particularly in developing countries with constrained healthcare budgets. Furthermore, stringent regulatory approval processes, especially in markets like the United States and Europe, can lead to extended development timelines and increased R&D costs, thereby delaying market entry for innovative products and potentially stifling competition. The risk of product recalls and device-related complications, though relatively low, also creates hesitancy among both clinicians and patients, impacting market confidence and adoption rates.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Devices and Procedures | -1.0% | Global, particularly emerging markets (Latin America, MEA) | Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -0.7% | North America, Europe | Mid-term (2025-2030) |

| Lack of Skilled Cardiologists and Surgeons | -0.5% | Developing regions (Asia Pacific, Africa) | Long-term (2025-2033) |

| Reimbursement Challenges and Healthcare Budget Constraints | -0.6% | Europe, parts of North America | Mid-to-Long term (2025-2033) |

Cardiac Surgery and Heart Valve Device Market Opportunities Analysis

Significant opportunities exist within the cardiac surgery and heart valve device market, particularly in the expansion into untapped emerging economies. Countries in Asia Pacific, Latin America, and the Middle East and Africa are witnessing improving healthcare infrastructure, rising disposable incomes, and increasing awareness of cardiac health, creating a burgeoning demand for advanced cardiac interventions. Another key opportunity lies in the development of personalized medicine approaches, where devices can be tailored to individual patient anatomies and specific disease characteristics, enhancing efficacy and reducing adverse events. The integration of advanced technologies like robotics, artificial intelligence, and virtual reality in surgical planning and execution also presents avenues for product differentiation and market leadership.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Economies | +1.3% | Asia Pacific, Latin America, Middle East & Africa | Mid-to-Long term (2026-2033) |

| Development of Personalized and Customizable Devices | +1.0% | Global, with early adoption in developed markets | Long-term (2028-2033) |

| Integration of Advanced Imaging and AI for Surgical Guidance | +0.9% | North America, Europe, select APAC countries | Short-to-Mid term (2025-2030) |

| Strategic Partnerships and Collaborations for R&D | +0.7% | Global | Short-to-Long term (2025-2033) |

Cardiac Surgery and Heart Valve Device Market Challenges Impact Analysis

The cardiac surgery and heart valve device market faces several challenges that necessitate strategic navigation from industry participants. Intense competition among a growing number of market players, coupled with pricing pressures from healthcare providers and payers, poses a significant hurdle to profitability and market share growth. Ensuring product longevity and minimizing post-implantation complications, such as device thrombosis or structural valve degeneration, remains a persistent clinical and engineering challenge. Furthermore, managing the complex supply chain for highly specialized and regulated medical devices, particularly in the face of geopolitical instability or global health crises, presents operational difficulties that can impact product availability and market responsiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Pricing Pressures | -0.8% | Global | Short-to-Long term (2025-2033) |

| Product Recalls and Post-Marketing Surveillance Issues | -0.6% | Global | Ongoing |

| Technological Obsolescence and Rapid Innovation Cycles | -0.4% | Developed markets (North America, Europe) | Mid-term (2025-2030) |

| Supply Chain Disruptions and Raw Material Volatility | -0.5% | Global | Short-to-Mid term (2025-2028) |

Cardiac Surgery and Heart Valve Device Market - Updated Report Scope

This report provides a comprehensive analysis of the Cardiac Surgery and Heart Valve Device Market, detailing market size estimations, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It covers an in-depth segmentation analysis across product types, applications, and end-use sectors, alongside a thorough examination of regional dynamics and the competitive landscape. The report also highlights the impact of artificial intelligence and offers strategic insights for stakeholders to navigate market complexities and capitalize on future growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.4 Billion |

| Market Forecast in 2033 | USD 119.7 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic plc, Edwards Lifesciences Corporation, Boston Scientific Corporation, Abbott Laboratories, Johnson & Johnson, Siemens Healthineers, GE Healthcare, LivaNova PLC, Getinge AB, Terumo Corporation, B. Braun Melsungen AG, Stereotaxis Inc., Artivion Inc., Lepu Medical Technology, JenaValve Technology GmbH, NeoChord, Inc., Highlife SAS, Braile Biomédica, TTK Healthcare Limited, CryoCath Technologies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cardiac Surgery and Heart Valve Device Market is segmented to provide a granular view of its various components, enabling a detailed understanding of market dynamics across different product categories, applications, and end-use environments. This segmentation helps identify key growth areas, competitive landscapes within specific niches, and emerging opportunities for strategic investment. The comprehensive breakdown facilitates a targeted approach for market players to develop specialized products and services that cater to precise clinical needs and patient populations, ensuring sustained market relevance and expansion.

- By Product Type:

- Heart Valve Devices

- Mechanical Heart Valves

- Bioprosthetic Heart Valves (tissue valves)

- Transcatheter Heart Valves (TAVR/TAVI, TMVr, TPVI)

- Cardiac Surgery Devices

- Cardiopulmonary Bypass Equipment (heart-lung machines, oxygenators)

- Defibrillators (external, internal implantable cardioverter-defibrillators (ICDs))

- Surgical Instruments (forceps, scissors, clamps, retractors)

- Monitoring Devices (ECG systems, hemodynamic monitors, pulse oximeters)

- Anesthesia Delivery Systems

- Heart Valve Devices

- By Application:

- Aortic Stenosis

- Mitral Regurgitation

- Tricuspid Valve Disease

- Pulmonary Stenosis

- Congenital Heart Defects (e.g., Tetralogy of Fallot, Ventricular Septal Defects)

- Coronary Artery Bypass Grafting (CABG)

- Valve Repair/Replacement Procedures

- By End-Use:

- Hospitals (primary settings for complex procedures)

- Ambulatory Surgical Centers (for less invasive interventions)

- Cardiac Catheterization Labs (specialized for transcatheter procedures)

- Specialty Clinics (for diagnosis and follow-up care)

Regional Highlights

- North America: This region dominates the market due to its advanced healthcare infrastructure, high prevalence of cardiovascular diseases, and early adoption of innovative cardiac technologies. Significant investments in R&D, coupled with favorable reimbursement policies and the presence of major market players, further contribute to its leading position. The United States, in particular, drives a substantial portion of this regional market.

- Europe: Europe represents a mature market, characterized by an aging population and a high incidence of valvular heart diseases. Countries such as Germany, France, and the UK are at the forefront of adopting minimally invasive procedures and advanced heart valve devices. Stringent regulatory standards, combined with robust healthcare systems, ensure high-quality care and device innovation across the continent.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate, driven by a rapidly expanding patient pool, improving healthcare expenditure, and increasing awareness of cardiac health. Countries like China, India, and Japan are investing heavily in upgrading their medical facilities and adopting advanced cardiac surgical techniques, presenting lucrative opportunities for market expansion.

- Latin America: This region is experiencing steady growth, fueled by rising healthcare access and increasing medical tourism. Economic development and government initiatives to improve public health services are gradually enhancing the demand for advanced cardiac devices and procedures. Brazil and Mexico are key markets within this region.

- Middle East and Africa (MEA): The MEA market is anticipated to show moderate growth, primarily due to rising healthcare infrastructure development, increased prevalence of lifestyle-related cardiac diseases, and a growing emphasis on medical specialization. Saudi Arabia, UAE, and South Africa are emerging as significant contributors to the regional market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cardiac Surgery and Heart Valve Device Market.- Medtronic plc

- Edwards Lifesciences Corporation

- Boston Scientific Corporation

- Abbott Laboratories

- Johnson & Johnson

- Siemens Healthineers

- GE Healthcare

- LivaNova PLC

- Getinge AB

- Terumo Corporation

- B. Braun Melsungen AG

- Stereotaxis Inc.

- Artivion Inc.

- Lepu Medical Technology

- JenaValve Technology GmbH

- NeoChord, Inc.

- Highlife SAS

- Braile Biomédica

- TTK Healthcare Limited

- CryoCath Technologies Inc.

Frequently Asked Questions

What is the current market size of the Cardiac Surgery and Heart Valve Device Market?

The Cardiac Surgery and Heart Valve Device Market is estimated at USD 65.4 Billion in 2025, demonstrating substantial growth driven by technological advancements and increasing global demand for cardiac interventions.

What are the primary drivers of growth in the Cardiac Surgery and Heart Valve Device Market?

Key drivers include the aging global population, rising prevalence of cardiovascular diseases, and continuous technological advancements, particularly in minimally invasive surgical techniques and transcatheter valve therapies.

How is AI impacting cardiac surgery and heart valve device development?

AI is transforming the market through enhanced diagnostic precision, AI-guided surgical planning, robotic assistance for increased accuracy, and advanced post-operative patient monitoring, leading to improved outcomes and personalized care.

What are the main types of heart valve devices available?

The main types include Mechanical Heart Valves, Bioprosthetic Heart Valves (derived from animal tissue), and Transcatheter Heart Valves (used in minimally invasive procedures like TAVR/TAVI, TMVr, TPVI).

Which regions are expected to show significant growth in this market?

The Asia Pacific region is anticipated to exhibit the highest growth rate due to improving healthcare infrastructure, increasing disposable incomes, and a large patient base, while North America continues to hold a dominant market share.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted