Decoy Flare Market

Decoy Flare Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709824 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

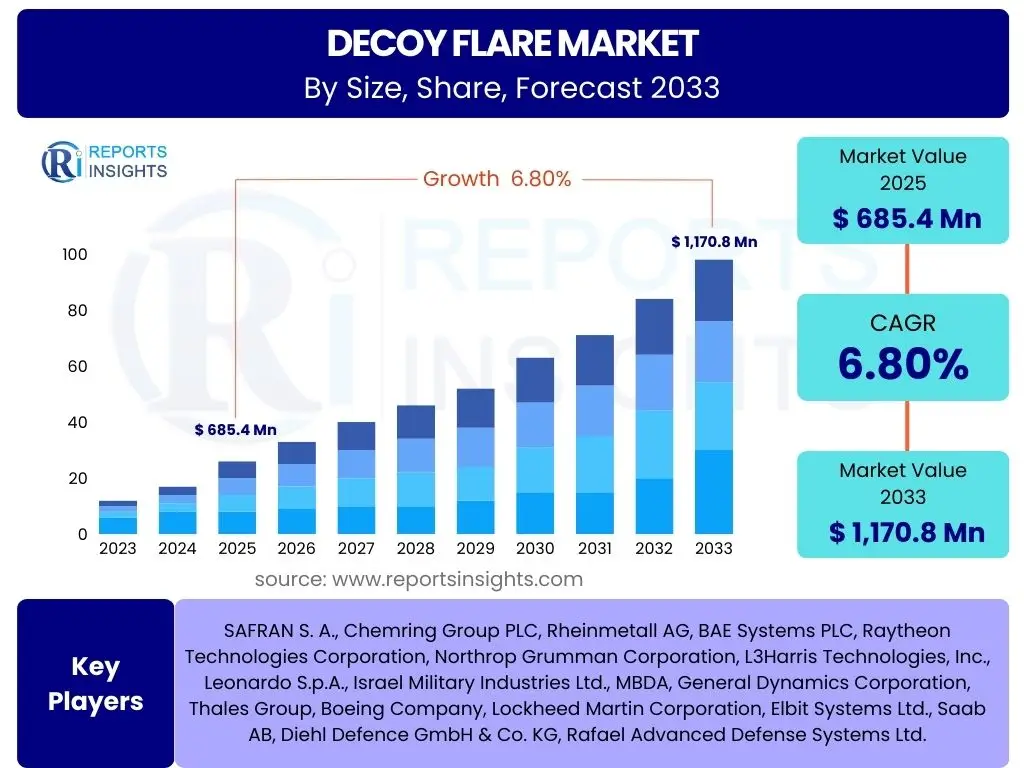

Decoy Flare Market Size

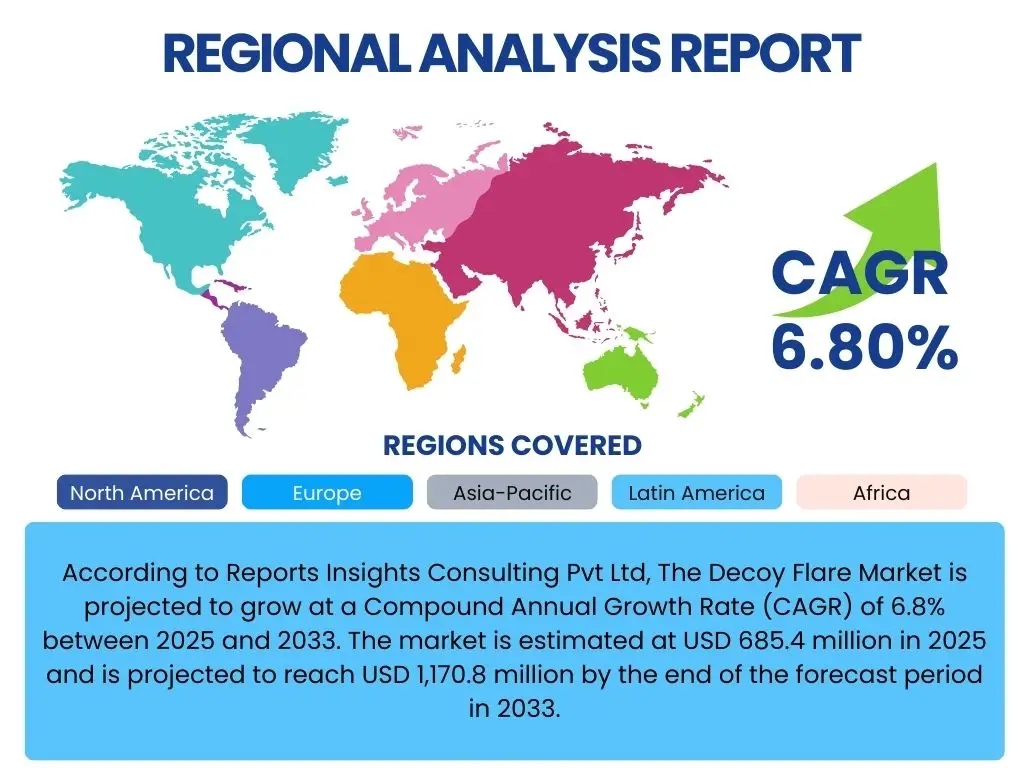

According to Reports Insights Consulting Pvt Ltd, The Decoy Flare Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 685.4 million in 2025 and is projected to reach USD 1,170.8 million by the end of the forecast period in 2033.

Key Decoy Flare Market Trends & Insights

The Decoy Flare market is undergoing significant transformation driven by evolving aerial and missile threats, demanding more sophisticated and effective countermeasures. Current trends indicate a strong shift towards multi-spectral capabilities, allowing flares to deceive advanced infrared (IR) and radio frequency (RF) guided systems simultaneously. This development is crucial as modern threats often employ multi-mode seekers, necessitating a broader defensive spectrum. Furthermore, miniaturization and lighter form factors are becoming paramount, enabling integration into smaller platforms such as unmanned aerial vehicles (UAVs) and enhancing the payload capacity for larger aircraft.

Another prominent insight revolves around the increasing emphasis on smart decoy systems. These systems are not merely reactive but are designed to integrate with onboard electronic warfare (EW) suites, leveraging threat intelligence to deploy flares with optimal timing and pattern. The development of environmentally friendly pyrotechnic materials and non-pyrotechnic alternatives is also gaining traction, addressing concerns related to environmental impact, safety during storage, and operational costs. This innovation pathway aims to provide effective deception while minimizing collateral effects and logistical burdens for defense forces globally.

- Development of multi-spectral decoy flares to counter advanced IR and RF threats.

- Miniaturization and lighter-weight designs for integration into smaller platforms and UAVs.

- Integration of smart decoy systems with electronic warfare (EW) suites for enhanced effectiveness.

- Growing demand for non-pyrotechnic and environmentally friendly flare alternatives.

- Emphasis on programmable and adaptive flare deployment strategies.

- Increased adoption in naval and ground-based defense systems alongside traditional aerial platforms.

AI Impact Analysis on Decoy Flare

Artificial Intelligence (AI) is poised to revolutionize the Decoy Flare market by introducing unparalleled levels of sophistication in threat detection, response, and material optimization. Users are particularly keen on how AI can enhance the adaptive deployment of countermeasures, moving beyond pre-programmed sequences to real-time, context-aware responses. This involves AI algorithms analyzing incoming threat parameters—such as missile velocity, trajectory, and seeker type—to determine the most effective flare type, quantity, and release pattern, thereby maximizing survivability and optimizing resource usage.

Concerns often center on the reliability and robustness of AI systems in high-stress combat scenarios, alongside the cybersecurity implications of integrating advanced AI into sensitive defense platforms. However, expectations are high for AI to enable predictive maintenance for decoy systems, optimize flare manufacturing processes for efficiency and quality, and even assist in the design of new, more effective decoy materials through advanced simulation and material science. The ultimate goal is to create autonomous defensive systems that can adapt to novel threats without direct human intervention, providing a significant edge in rapidly evolving threat environments.

- AI-powered threat analysis and classification for optimized flare deployment.

- Real-time adaptive deployment strategies based on missile trajectory and seeker characteristics.

- Predictive maintenance for decoy flare systems, enhancing readiness and reliability.

- Optimization of flare design and material composition through AI-driven simulations.

- Integration of AI with electronic warfare (EW) for synergistic countermeasure effects.

- Autonomous decision-making in high-threat environments for rapid response.

Key Takeaways Decoy Flare Market Size & Forecast

The Decoy Flare market is set for substantial growth, driven by increasing geopolitical instability and the continuous evolution of advanced missile and aerial threats globally. The forecast highlights a robust Compound Annual Growth Rate, indicating sustained investment in defense capabilities by nations seeking to protect critical assets and personnel. This growth is not merely quantitative but also qualitative, reflecting a shift towards more intelligent, multi-spectral, and platform-agnostic countermeasure solutions. Market participants should anticipate rising demand for systems that offer enhanced survivability against sophisticated threats while also addressing logistical and environmental considerations.

A key takeaway from the market forecast is the imperative for innovation in material science and system integration. Success in this market will depend on developing flares that can effectively jam or deceive the latest generation of multi-mode seekers and integrate seamlessly with existing or next-generation electronic warfare and platform management systems. Furthermore, the expansion into new platforms, such as unmanned systems and diverse naval vessels, represents a significant growth avenue. The market's future will be shaped by ongoing research and development aimed at improving effectiveness, reducing operational costs, and meeting stringent safety and environmental regulations.

- Sustained market growth driven by escalating global defense spending and evolving threats.

- Shift towards advanced multi-spectral and smart decoy solutions for enhanced effectiveness.

- Increased integration of decoy systems with broader electronic warfare ecosystems.

- Significant opportunities in upgrading existing defense platforms and equipping new ones.

- Emphasis on innovative materials and manufacturing processes to improve performance and safety.

- Growing adoption across diverse platforms including aerial, naval, and ground systems.

Decoy Flare Market Drivers Analysis

The Decoy Flare market is significantly propelled by an escalating global defense expenditure, primarily fueled by rising geopolitical tensions and the modernization efforts of national militaries worldwide. As nations perceive heightened threats from sophisticated adversaries, there is an urgent demand for advanced defensive countermeasures to protect critical aerial, naval, and ground assets. This includes the upgrade of existing fleets with next-generation decoy systems and the outfitting of newly acquired platforms with state-of-the-art protection capabilities. The proliferation of advanced anti-aircraft and anti-ship missile systems necessitates more effective and adaptable decoy technologies.

Furthermore, the continuous development and deployment of stealth aircraft and unmanned aerial vehicles (UAVs) by various military forces also contribute to market expansion. While stealth technology aims to reduce detectability, decoy flares remain a crucial last line of defense against unexpected engagements or when stealth is compromised. The adaptability of modern decoy flares to a wider range of platforms, from fighter jets and transport aircraft to naval vessels and even ground convoys, significantly broadens their addressable market and drives continuous innovation in their design and functionality.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Global Geopolitical Tensions | +1.5% | Global, particularly Asia Pacific, Middle East, Europe | Short to Mid-term (2025-2030) |

| Modernization of Military Air Forces | +1.2% | North America, Europe, China, India | Mid-term (2026-2032) |

| Development of Advanced Missile Systems | +1.0% | Global, especially Russia, China, USA | Long-term (2028-2033) |

| Increased Adoption of Unmanned Aerial Vehicles (UAVs) | +0.8% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2031) |

Decoy Flare Market Restraints Analysis

Despite the strong growth drivers, the Decoy Flare market faces several significant restraints that could temper its expansion. One primary concern is the high cost associated with research and development (R&D) for advanced multi-spectral and smart decoy systems. Developing new materials, complex electronic components, and sophisticated software for AI-driven deployment strategies requires substantial investment, often leading to higher unit costs for the end-users. This can be a barrier for smaller defense budgets or nations looking for more cost-effective solutions, potentially limiting widespread adoption of the most advanced technologies.

Furthermore, stringent regulatory requirements and the need for rigorous certification processes act as a considerable restraint. Decoy flares, by their nature, involve pyrotechnic materials and precise deployment mechanisms, necessitating extensive testing and compliance with international and national safety standards. The long lead times for qualification and integration into existing aircraft and naval platforms can delay market entry for new products and innovations. Additionally, concerns regarding environmental impact from pyrotechnic residue and increasing pressure for "green" defense solutions pose challenges for manufacturers, driving up R&D costs for environmentally compliant alternatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development Costs | -0.9% | Global | Long-term (2027-2033) |

| Strict Regulatory & Certification Processes | -0.7% | North America, Europe | Mid-term (2026-2031) |

| Budgetary Constraints in Smaller Militaries | -0.6% | Developing Regions, Latin America, Africa | Short to Mid-term (2025-2030) |

| Environmental Concerns & Disposal Issues | -0.5% | Europe, North America | Mid-term (2026-2032) |

Decoy Flare Market Opportunities Analysis

The Decoy Flare market presents several compelling opportunities for growth and innovation. One significant area lies in the extensive upgrade programs for aging defense fleets across numerous countries. Many nations operate older aircraft and naval vessels that require modernization of their electronic warfare and countermeasure systems to remain viable against contemporary threats. This creates a sustained demand for compatible, advanced decoy flare systems that can be integrated into existing platforms, offering manufacturers a substantial retrofit market rather than solely relying on new platform sales.

Another major opportunity stems from the increasing adoption of unmanned aerial vehicles (UAVs) in military operations. As UAVs become more sophisticated and operate in contested airspace, equipping them with lightweight, compact, and effective decoy flare systems becomes crucial for their survivability. This segment demands specialized decoy solutions that are miniaturized and require minimal power, opening new design and manufacturing avenues. Furthermore, the development of non-pyrotechnic or "safe" flares, which reduce logistical burdens, fire hazards, and environmental impact, offers a significant competitive advantage and addresses growing industry and regulatory demands, expanding market acceptance and usage scenarios.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Upgrade Programs for Existing Defense Platforms | +1.3% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2031) |

| Integration with Unmanned Aerial Vehicles (UAVs) | +1.1% | Global | Mid-term (2026-2032) |

| Development of Non-Pyrotechnic Decoy Solutions | +0.9% | Europe, North America | Long-term (2028-2033) |

| Expansion into Naval and Ground-Based Countermeasures | +0.7% | Asia Pacific, Middle East | Mid-term (2026-2031) |

Decoy Flare Market Challenges Impact Analysis

The Decoy Flare market faces several significant challenges that could hinder its growth and operational effectiveness. One critical challenge is the rapid advancement of missile seeker technology, which continuously introduces new frequencies, multi-mode capabilities, and enhanced discrimination algorithms. This technological arms race forces decoy manufacturers into a perpetual cycle of innovation, striving to develop countermeasures that can effectively deceive increasingly sophisticated threats. Keeping pace with these evolving threats requires substantial R&D investments and often results in higher product development costs and shorter product lifecycles for current generation flares.

Another challenge is the increasing complexity of integrating advanced decoy systems with existing and next-generation electronic warfare (EW) suites. Effective decoy deployment is no longer a standalone function but rather a coordinated response within a larger EW ecosystem. Achieving seamless interoperability and real-time data exchange between decoy systems, threat warning sensors, and mission computers presents significant technical and logistical hurdles. Furthermore, global supply chain disruptions, especially for specialized materials and components, can impact manufacturing timelines and increase production costs, particularly for defense-grade products requiring high reliability and performance under extreme conditions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Evolution of Missile Seeker Technology | -1.0% | Global | Ongoing (2025-2033) |

| Complex Integration with Electronic Warfare Suites | -0.8% | Global | Mid-term (2026-2032) |

| Supply Chain Vulnerabilities for Specialized Components | -0.6% | Global | Short to Mid-term (2025-2030) |

| Balancing Cost-Effectiveness with Advanced Performance | -0.5% | Global | Ongoing (2025-2033) |

Decoy Flare Market - Updated Report Scope

This report provides a comprehensive analysis of the global Decoy Flare market, offering in-depth insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and regions. It meticulously examines current market trends, technological advancements, and the competitive landscape to deliver a holistic understanding of the industry dynamics. The scope extends to a detailed forecast, projecting market performance up to 2033, considering the impact of geopolitical shifts, defense modernization efforts, and emerging threat paradigms.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 685.4 million |

| Market Forecast in 2033 | USD 1,170.8 million |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SAFRAN S. A., Chemring Group PLC, Rheinmetall AG, BAE Systems PLC, Raytheon Technologies Corporation, Northrop Grumman Corporation, L3Harris Technologies, Inc., Leonardo S.p.A., Israel Military Industries Ltd., MBDA, General Dynamics Corporation, Thales Group, Boeing Company, Lockheed Martin Corporation, Elbit Systems Ltd., Saab AB, Diehl Defence GmbH & Co. KG, Rafael Advanced Defense Systems Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Decoy Flare market is comprehensively segmented to provide a granular view of its various components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper understanding of market trends, specific product demands, and regional preferences, enabling stakeholders to identify niche opportunities and tailor their strategies effectively. The primary segmentation revolves around the type of flare, the platform on which it is deployed, the end-user, and the material composition, each presenting distinct technological requirements and market characteristics.

Further sub-segmentation within these categories allows for a more precise analysis. For instance, the 'By Platform' segment differentiates between fixed-wing aircraft, rotary-wing aircraft, and unmanned aerial vehicles, recognizing their varied operational needs and integration complexities. Similarly, 'By Type' distinguishes between Infrared (IR), Radio Frequency (RF), and the increasingly prevalent Multi-Spectral flares, reflecting the technological evolution in countermeasure capabilities. Understanding these segments is crucial for manufacturers to align their product development with specific market demands and for defense organizations to make informed procurement decisions.

- By Type: Infrared (IR) Flares, Radio Frequency (RF) Flares, Multi-Spectral Flares, Others (e.g., Chaff)

- By Platform: Aerial (Fixed-Wing Aircraft, Rotary-Wing Aircraft, UAVs), Naval Vessels (Surface Combatants, Submarines), Ground Vehicles

- By End-User: Military, Homeland Security, Commercial Aviation (Limited application)

- By Material: Pyrotechnic, Non-Pyrotechnic (e.g., Expendable Active Decoys)

- By Deployment System: Manual, Automated, Integrated EW

- By Range: Short-Range, Medium-Range, Long-Range

- By Application: Aircraft Self-Protection, Naval Vessel Protection, Ground Convoy Protection, Strategic Asset Defense

Regional Highlights

- North America: This region consistently holds a significant market share due to substantial defense budgets, robust R&D capabilities, and the presence of major defense contractors. The United States, in particular, drives demand through extensive military modernization programs and the procurement of advanced aircraft and naval assets, along with a strong focus on AI integration into EW systems.

- Europe: The European market is characterized by increasing defense spending, especially in Eastern European countries, fueled by heightened geopolitical tensions. Western European nations are investing in upgrading existing fleets and developing next-generation multi-spectral countermeasures, with a strong emphasis on indigenous manufacturing and compliance with strict environmental regulations.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, primarily due to the rapid militarization of countries like China and India, alongside sustained defense investments by South Korea, Japan, and Australia. The focus here is on acquiring advanced defense systems to counter regional threats and enhance maritime security, leading to high demand for both new platforms and retrofits.

- Middle East and Africa (MEA): This region experiences steady growth driven by ongoing conflicts, border disputes, and the need to protect critical infrastructure. Countries like Saudi Arabia, UAE, and Israel are investing heavily in sophisticated countermeasure systems for their air forces and naval fleets, often relying on imports from Western manufacturers.

- Latin America: The market in Latin America is relatively smaller but shows consistent demand for basic and upgraded decoy flare systems, primarily for air force modernization and maritime patrol aircraft. Budgetary constraints often lead to a focus on cost-effective solutions and maintenance of existing platforms rather than extensive new acquisitions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Decoy Flare Market.- SAFRAN S. A.

- Chemring Group PLC

- Rheinmetall AG

- BAE Systems PLC

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Israel Military Industries Ltd.

- MBDA

- General Dynamics Corporation

- Thales Group

- Boeing Company

- Lockheed Martin Corporation

- Elbit Systems Ltd.

- Saab AB

- Diehl Defence GmbH & Co. KG

- Rafael Advanced Defense Systems Ltd.

Frequently Asked Questions

What is a decoy flare and how does it work?

A decoy flare is an airborne countermeasure designed to protect aircraft, naval vessels, or ground assets from heat-seeking or radar-guided missiles. It works by emitting intense infrared (IR) radiation or radio frequency (RF) signals, creating a more attractive target for the missile's seeker, thus diverting the missile away from the protected platform. Modern flares can be multi-spectral, countering both IR and RF threats simultaneously.

What types of platforms primarily use decoy flares?

Decoy flares are predominantly used on military aircraft, including fighter jets, attack helicopters, and transport planes. Increasingly, they are also integrated into naval vessels for anti-ship missile defense and, in some specialized applications, on ground vehicles or as part of static defensive systems to protect high-value assets. Unmanned Aerial Vehicles (UAVs) are also emerging as a significant platform for miniaturized decoy flares.

What are the key technological advancements in decoy flares?

Key technological advancements include the development of multi-spectral flares capable of defeating both IR and RF seekers, miniaturization for smaller platforms like UAVs, and the integration of smart deployment systems leveraging AI to optimize release patterns based on real-time threat analysis. There is also a push towards non-pyrotechnic and environmentally friendly flare alternatives.

Who are the major manufacturers in the Decoy Flare market?

The Decoy Flare market is dominated by a few key players, primarily large defense contractors and specialized pyrotechnic manufacturers. These include companies like Chemring Group PLC, Rheinmetall AG, BAE Systems PLC, Raytheon Technologies Corporation, Northrop Grumman Corporation, and SAFRAN S. A., among others.

What factors are driving the growth of the Decoy Flare market?

The market growth is primarily driven by increasing global geopolitical tensions, continuous modernization efforts by national militaries, the proliferation of advanced missile threats, and the growing adoption of unmanned aerial vehicles (UAVs) across various defense applications. The need for enhanced survivability against sophisticated weaponry fuels sustained demand for advanced decoy solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted