Rotogravure Printing Ink Market

Rotogravure Printing Ink Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701519 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

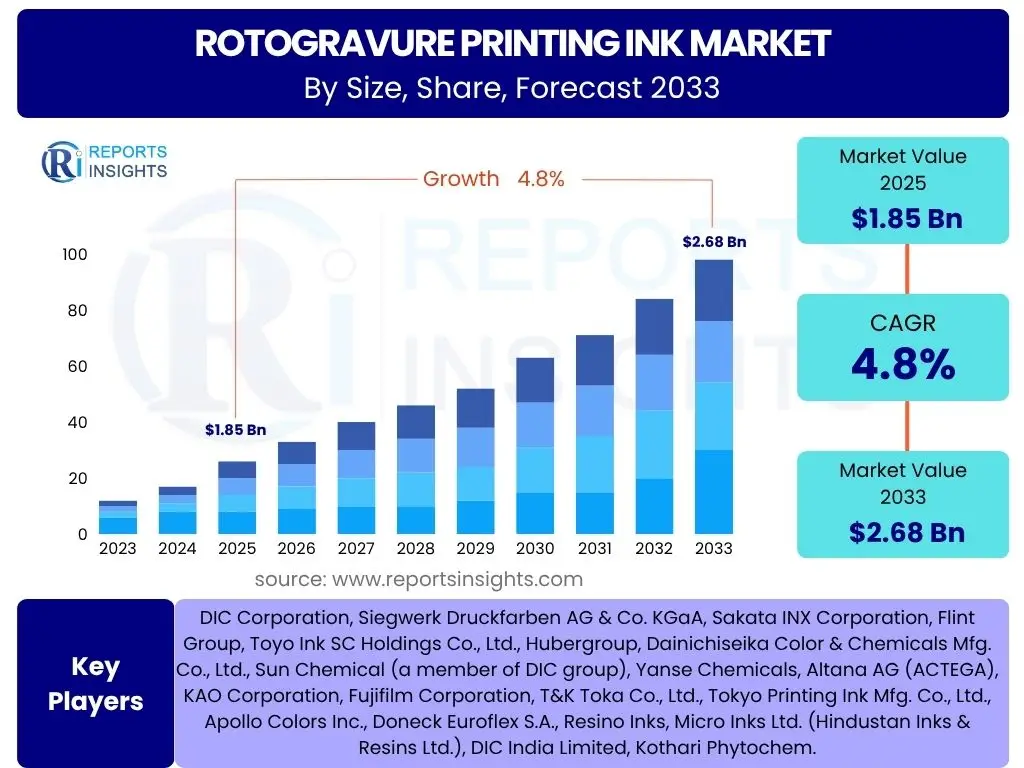

Rotogravure Printing Ink Market Size

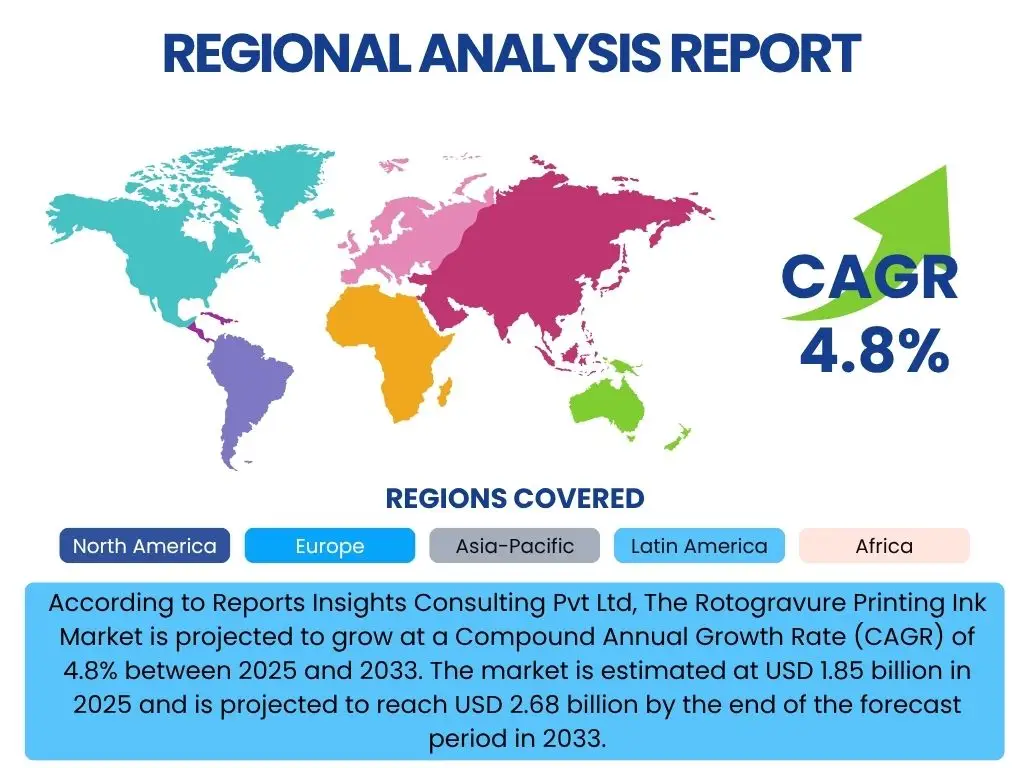

According to Reports Insights Consulting Pvt Ltd, The Rotogravure Printing Ink Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 2.68 billion by the end of the forecast period in 2033.

The consistent expansion of the packaging industry, particularly flexible packaging, is a primary catalyst for this growth. Rotogravure printing offers superior print quality, high-speed production, and excellent durability, making it an ideal choice for long print runs required in various consumer goods sectors. This inherent capability ensures its continued relevance despite the emergence of alternative printing technologies.

Geographic market dynamics also play a crucial role, with emerging economies demonstrating robust demand fueled by increasing disposable incomes and expanding manufacturing bases. Investments in advanced printing machinery and a growing preference for high-quality, aesthetically appealing packaging solutions are further reinforcing the market's trajectory towards significant valuation by the end of the forecast period.

Key Rotogravure Printing Ink Market Trends & Insights

Common user inquiries about the Rotogravure Printing Ink market frequently revolve around its adaptability to evolving industry standards, the impact of sustainability initiatives, and the integration of advanced technologies. Users are keen to understand how traditional printing methods like rotogravure are evolving to meet demands for eco-friendliness, customization, and operational efficiency, alongside the competitive landscape posed by digital printing advancements. There is also significant interest in the regional growth disparities and the influence of raw material pricing on overall market stability and innovation.

The market is witnessing a pronounced shift towards sustainable and eco-friendly ink formulations. This trend is driven by stringent environmental regulations globally and increasing consumer awareness regarding sustainable packaging. Consequently, manufacturers are investing heavily in research and development to produce water-based and bio-based rotogravure inks that offer comparable performance to traditional solvent-based inks, but with a reduced environmental footprint.

Furthermore, the demand for high-quality, vibrant, and durable prints, particularly in the flexible packaging and publication sectors, continues to bolster the rotogravure ink market. Customization and personalization trends, especially in niche product segments, are pushing ink manufacturers to innovate with specialized formulations that can deliver enhanced aesthetic and functional properties, such as improved adhesion, scratch resistance, and color vibrancy across diverse substrates. This emphasis on performance combined with sustainability defines the core trends shaping the market's future.

- Growing demand for sustainable and eco-friendly ink formulations, including water-based and bio-based inks.

- Increasing adoption of rotogravure printing in flexible packaging due to superior print quality and durability.

- Technological advancements in ink chemistry leading to enhanced performance characteristics.

- Shift towards high-definition and vibrant color printing for premium product presentation.

- Emergence of smart packaging trends requiring specialized ink functionalities.

- Consolidation among key market players to leverage economies of scale and expand product portfolios.

AI Impact Analysis on Rotogravure Printing Ink

User queries regarding the impact of Artificial Intelligence (AI) on the Rotogravure Printing Ink market typically focus on operational efficiencies, quality assurance, and supply chain optimization. There is keen interest in how AI can streamline ink formulation, predict maintenance needs for printing machinery, and enhance overall production processes. Concerns often relate to the initial investment required for AI integration and the potential need for workforce reskilling, alongside the perceived value proposition in terms of cost savings and improved output consistency. Expectations largely center on AI's ability to drive greater precision, reduce waste, and provide deeper market insights for strategic decision-making within the printing ink ecosystem.

AI's influence is increasingly observable in the optimization of ink formulation and manufacturing processes. Machine learning algorithms can analyze vast datasets related to pigment properties, resin characteristics, and solvent interactions to predict optimal ink formulations for specific applications, reducing trial-and-error and accelerating product development. This precision leads to significant savings in raw materials and energy, contributing to more sustainable production practices. Furthermore, AI-powered systems can monitor production parameters in real-time, identifying anomalies and potential quality issues before they escalate, thereby ensuring consistent ink quality and minimizing batch rejections.

Beyond formulation, AI is poised to revolutionize the supply chain and logistics of rotogravure printing inks. Predictive analytics can forecast demand patterns with greater accuracy, enabling manufacturers to optimize inventory levels and reduce lead times. AI-driven predictive maintenance for printing presses and ink mixing equipment can prevent costly downtimes by scheduling maintenance proactively, based on sensor data analysis. This holistic integration of AI across the value chain promises to enhance operational efficiency, reduce waste, and improve overall profitability for ink manufacturers and end-users alike, solidifying its role as a transformative technology in the industry.

- Enhanced quality control and defect detection in ink production through machine vision and predictive analytics.

- Optimization of ink formulations and color matching using AI algorithms, leading to reduced waste and improved consistency.

- Predictive maintenance for printing machinery and ink mixing equipment, minimizing downtime and operational costs.

- Supply chain optimization and demand forecasting for raw materials and finished inks, improving inventory management.

- Automation of routine tasks in ink manufacturing and quality testing, freeing human resources for complex problem-solving.

- Data-driven insights for market trend analysis and product innovation, enabling more targeted R&D efforts.

Key Takeaways Rotogravure Printing Ink Market Size & Forecast

Common user questions regarding the key takeaways from the Rotogravure Printing Ink market size and forecast typically center on identifying the primary growth drivers, understanding regional market dominance, and pinpointing lucrative investment avenues. Users are particularly interested in the long-term viability of rotogravure printing amidst technological shifts and the impact of sustainability trends on market expansion. There is also a strong desire to understand the critical success factors for market players and the overall outlook for innovation and competitive differentiation within the sector.

The market's sustained growth is predominantly driven by the robust expansion of the flexible packaging industry, which heavily relies on rotogravure for its high-quality, durable, and high-volume printing requirements. This fundamental demand ensures a stable base for the rotogravure printing ink sector, even as other printing technologies gain traction. Emerging economies, particularly in the Asia Pacific region, are expected to be significant growth engines due to increasing consumer spending and burgeoning manufacturing capabilities, presenting substantial opportunities for market participants.

Furthermore, the emphasis on developing eco-friendly and performance-enhanced ink formulations represents a critical strategic imperative for companies aiming to capture market share. Innovations in water-based and bio-based inks, coupled with advancements in ink chemistry that improve adhesion, drying times, and substrate compatibility, will be pivotal. These developments are not only addressing environmental concerns but also expanding the application scope of rotogravure printing, thereby solidifying its position in specialized and high-value segments of the printing industry.

- The market is poised for steady growth, primarily fueled by the expanding flexible packaging sector globally.

- Asia Pacific remains the dominant and fastest-growing region, driven by industrialization and consumer demand.

- Sustainability initiatives are critical, with a growing shift towards eco-friendly and bio-based ink formulations.

- Technological advancements in ink properties, such as enhanced durability and color vibrancy, are key for market differentiation.

- Investment in research and development for specialized and functional inks presents significant long-term opportunities.

- Despite competition, rotogravure printing maintains a strong foothold in high-volume, high-quality print applications.

Rotogravure Printing Ink Market Drivers Analysis

The Rotogravure Printing Ink Market is propelled by several key factors that underpin its sustained growth trajectory. Foremost among these is the escalating demand from the flexible packaging industry, which benefits immensely from rotogravure's capacity for high-speed, high-quality, and cost-effective production of packaging materials. The increasing global consumption of packaged food, beverages, and other consumer goods directly translates into a higher requirement for durable and aesthetically pleasing flexible packaging, thereby boosting the demand for rotogravure inks.

Another significant driver is the growing preference for high-quality visual appeal and brand differentiation in product packaging. Rotogravure printing excels in delivering vibrant colors, intricate designs, and consistent print quality over long runs, which is crucial for brand owners seeking to capture consumer attention on crowded retail shelves. This emphasis on visual appeal extends to other applications like magazines, catalogs, and decorative laminates, where superior print fidelity is paramount.

Furthermore, rapid urbanization and rising disposable incomes in developing economies are stimulating consumer spending on various packaged goods, contributing to the expansion of the printing and packaging sectors. This demographic and economic shift creates a fertile ground for the increased adoption of rotogravure printing, particularly in regions where manufacturing bases are expanding and consumer markets are maturing, thereby accelerating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Flexible Packaging Industry | +1.5% | Global, particularly APAC & MEA | 2025-2033 |

| Increasing Demand for High-Quality Prints | +1.2% | North America, Europe, APAC | 2025-2033 |

| Rising Consumer Spending & Urbanization | +0.8% | Emerging Economies (China, India, Brazil) | 2025-2033 |

| Technological Advancements in Ink Formulation | +0.7% | Global | 2025-2033 |

Rotogravure Printing Ink Market Restraints Analysis

Despite the inherent advantages of rotogravure printing, the market for its inks faces several significant restraints that could impede its growth. One major challenge is the increasing stringency of environmental regulations concerning Volatile Organic Compound (VOC) emissions from solvent-based inks. Governments and regulatory bodies worldwide are pushing for stricter limits on these emissions, compelling ink manufacturers to invest heavily in reformulating inks, which often entails higher production costs and a complex transition period for users.

Another substantial restraint is the volatile pricing of raw materials essential for ink production, such as resins, pigments, and solvents. Global supply chain disruptions, geopolitical tensions, and fluctuating crude oil prices directly impact the cost of these components. This volatility can lead to unpredictable manufacturing costs, squeeze profit margins for ink producers, and potentially drive up prices for end-users, thereby affecting overall market demand and competitiveness.

Furthermore, the rising competition from alternative printing technologies, particularly digital printing and advanced flexography, poses a threat to the rotogravure market. While rotogravure excels in long runs and high quality, digital printing offers flexibility, customization, and cost-effectiveness for shorter print runs, appealing to a different segment of the market. Similarly, advancements in flexographic printing have narrowed the quality gap with rotogravure, offering a viable alternative for some applications and potentially diverting market share.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations (VOCs) | -1.0% | Europe, North America, increasingly APAC | 2025-2033 |

| Volatile Raw Material Prices | -0.8% | Global | 2025-2033 |

| Competition from Digital & Flexographic Printing | -0.7% | Global | 2025-2033 |

| High Initial Investment for Rotogravure Equipment | -0.5% | Emerging Markets (Entry Barrier) | 2025-2033 |

Rotogravure Printing Ink Market Opportunities Analysis

Despite the challenges, the Rotogravure Printing Ink Market is rich with opportunities that can foster significant growth and innovation. A prime opportunity lies in the development and widespread adoption of sustainable and eco-friendly ink solutions, such as water-based, bio-based, and UV-curable inks. As environmental concerns escalate and regulatory pressures intensify, there is a burgeoning demand for inks that offer reduced VOC emissions, improved biodegradability, and lower toxicity. Companies that successfully innovate and scale production of these greener alternatives stand to gain a significant competitive advantage and capture an increasing share of the market.

Another promising avenue stems from the expansion into specialized and functional ink applications. Beyond conventional printing, rotogravure inks can be tailored for unique functionalities required in smart packaging, security printing, and advanced industrial applications. This includes inks with properties like conductivity for integrated electronics, thermochromic or photochromic features for interactive packaging, and enhanced barrier properties. Tapping into these high-value, niche segments allows manufacturers to diversify their portfolios and command premium pricing.

Furthermore, the continuous growth of emerging markets, particularly in Asia Pacific, Latin America, and Africa, presents a vast untapped potential. As these regions experience rapid industrialization, urbanization, and a surge in consumer goods consumption, the demand for high-quality packaging and printed materials is set to soar. Strategic expansion into these markets, coupled with localized product offerings and distribution networks, can unlock substantial growth opportunities for rotogravure printing ink manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable & Eco-friendly Inks | +1.3% | Global, particularly Europe & North America | 2025-2033 |

| Expansion into Functional & Smart Packaging Applications | +1.1% | Global (High-value segments) | 2025-2033 |

| Growth in Emerging Economies | +0.9% | APAC, Latin America, MEA | 2025-2033 |

| Technological Advancements in Printing Processes | +0.6% | Global | 2025-2033 |

Rotogravure Printing Ink Market Challenges Impact Analysis

The Rotogravure Printing Ink Market faces several formidable challenges that require strategic navigation from industry players. A significant challenge is the complex and ever-evolving regulatory landscape, particularly concerning environmental protection and chemical safety. Compliance with varying regional and international standards for VOC emissions, heavy metal content, and food contact safety necessitates continuous product reformulation and rigorous testing, which adds considerable cost and complexity to manufacturing processes and can slow down market entry for new products.

Another critical challenge is managing supply chain disruptions and ensuring the consistent availability and quality of raw materials. The global nature of the ink industry makes it susceptible to geopolitical events, natural disasters, and logistical bottlenecks that can disrupt the supply of key pigments, resins, and solvents. Such disruptions can lead to raw material shortages, price spikes, and production delays, ultimately impacting product availability and profitability for ink manufacturers and users.

Furthermore, the mature nature of the rotogravure printing technology, combined with the emergence of highly competitive digital and flexographic alternatives, presents a market share challenge. While rotogravure maintains its niche in high-volume, high-quality runs, there is pressure to justify its higher initial setup costs and specialized operational requirements against the flexibility and lower entry barriers of other methods. This necessitates continuous innovation in ink performance and cost-efficiency to maintain competitiveness and prevent market erosion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Regulatory Compliance (Environmental, Safety) | -0.9% | Global, especially EU & US | 2025-2033 |

| Supply Chain Vulnerabilities & Raw Material Scarcity | -0.7% | Global | 2025-2033 |

| Intensifying Competition from Alternative Printing Technologies | -0.6% | Global | 2025-2033 |

| Need for Specialized Skilled Labor | -0.4% | Global (developed regions) | 2025-2033 |

Rotogravure Printing Ink Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Rotogravure Printing Ink market, covering historical trends, current market dynamics, and future projections. It offers a detailed examination of market size, growth drivers, restraints, opportunities, and challenges affecting the industry from 2019 to 2033. The report segments the market by various types, applications, and end-use industries, providing granular insights into each category. Furthermore, it includes a thorough regional analysis and profiles of key market players, offering a holistic view of the competitive landscape and strategic recommendations for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.68 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DIC Corporation, Siegwerk Druckfarben AG & Co. KGaA, Sakata INX Corporation, Flint Group, Toyo Ink SC Holdings Co., Ltd., Hubergroup, Dainichiseika Color & Chemicals Mfg. Co., Ltd., Sun Chemical (a member of DIC group), Yanse Chemicals, Altana AG (ACTEGA), KAO Corporation, Fujifilm Corporation, T&K Toka Co., Ltd., Tokyo Printing Ink Mfg. Co., Ltd., Apollo Colors Inc., Doneck Euroflex S.A., Resino Inks, Micro Inks Ltd. (Hindustan Inks & Resins Ltd.), DIC India Limited, Kothari Phytochem. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Rotogravure Printing Ink market is meticulously segmented to provide a comprehensive understanding of its diverse components and driving forces. These segmentations allow for a detailed analysis of market dynamics across various ink types, technological bases, and end-use applications, offering valuable insights into specific market niches and their growth potential. Understanding these segments is crucial for stakeholders to identify key growth areas, tailor product development, and formulate targeted marketing strategies.

The market is broadly categorized by resin type, which determines the ink's properties such as adhesion, flexibility, and resistance; by pigment type, which dictates color vibrancy and opacity; and by technology, distinguishing between solvent-based, water-based, and UV-cured formulations based on their environmental impact and performance characteristics. Each of these classifications plays a vital role in defining the ink's suitability for different substrates and printing requirements, catering to specific industry needs.

Furthermore, the market is segmented by application, including flexible packaging, publications, and labels, which represent the largest consumers of rotogravure inks due to their demand for high-quality, high-volume prints. The segmentation by end-use industry, such as food & beverages, pharmaceuticals, and cosmetics, highlights the diverse sectors that rely on rotogravure printing for their packaging and product branding. This multi-faceted segmentation provides a holistic view of the market's structure and its intricate interdependencies.

- By Resin Type:

- Nitrocellulose

- Polyamide

- Polyurethane

- Acrylic

- Others (Vinyl, Polyester)

- By Pigment Type:

- Organic Pigments

- Inorganic Pigments

- By Technology:

- Solvent-Based

- Water-Based

- UV-Cured

- By Application:

- Flexible Packaging

- Publications (Magazines, Catalogs)

- Decorative Laminates

- Labels

- Others (Textile, Wall Coverings)

- By End-Use Industry:

- Food & Beverages

- Cosmetics & Personal Care

- Pharmaceutical

- Automotive

- Printing & Publishing

- Others (Industrial, Textile)

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market for rotogravure printing inks, primarily driven by robust growth in manufacturing, particularly in the flexible packaging sector, and increasing consumer demand for packaged goods in countries like China, India, Indonesia, and Southeast Asian nations. Rapid urbanization, rising disposable incomes, and the expansion of the food and beverage industry are key contributors to market expansion in this region.

- Europe: A mature market characterized by stringent environmental regulations and a strong focus on sustainable ink solutions. While growth might be slower compared to APAC, the region leads in the adoption of water-based and UV-curable inks, driven by innovation and a push towards eco-friendly manufacturing. Germany, the UK, France, and Italy are key contributors due to their established packaging and publishing industries.

- North America: A significant market with a stable demand for high-quality packaging and publication printing. The region is characterized by technological advancements and a growing emphasis on functional inks for specialized applications. The shift towards sustainable practices and the increasing adoption of automated printing processes are shaping market dynamics in the United States and Canada.

- Latin America: An emerging market exhibiting considerable growth potential, fueled by expanding industrialization, particularly in Brazil, Mexico, and Argentina. The rising middle class, coupled with increasing investments in infrastructure and manufacturing, is boosting the demand for flexible packaging and printed materials, creating new opportunities for rotogravure ink manufacturers.

- Middle East and Africa (MEA): A developing market experiencing steady growth, largely driven by infrastructure development, expanding food processing industries, and rising consumer spending. Investments in packaging facilities and a growing demand for high-quality printed materials, especially in countries like Saudi Arabia, UAE, and South Africa, are contributing to the regional market's expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Rotogravure Printing Ink Market.- DIC Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Sakata INX Corporation

- Flint Group

- Toyo Ink SC Holdings Co., Ltd.

- Hubergroup

- Dainichiseika Color & Chemicals Mfg. Co., Ltd.

- Sun Chemical (a member of DIC group)

- Yanse Chemicals

- Altana AG (ACTEGA)

- KAO Corporation

- Fujifilm Corporation

- T&K Toka Co., Ltd.

- Tokyo Printing Ink Mfg. Co., Ltd.

- Apollo Colors Inc.

- Doneck Euroflex S.A.

- Resino Inks

- Micro Inks Ltd. (Hindustan Inks & Resins Ltd.)

- DIC India Limited

- Kothari Phytochem

Frequently Asked Questions

What is rotogravure printing ink primarily used for?

Rotogravure printing ink is primarily utilized in high-volume, high-quality printing applications, predominantly for flexible packaging, such as food wraps, pouches, and laminates. It is also extensively used for publications like magazines and catalogs, as well as for decorative laminates and labels, due to its ability to produce vibrant colors, fine details, and consistent print quality over long runs.

What are the key types of rotogravure printing inks available in the market?

The key types of rotogravure printing inks are categorized by their solvent base or curing mechanism. These include solvent-based inks, known for their fast drying and strong adhesion; water-based inks, favored for their environmental benefits and reduced VOC emissions; and UV-cured inks, which offer instant drying and high resistance properties through ultraviolet light polymerization.

How do environmental regulations impact the rotogravure printing ink market?

Environmental regulations, particularly those targeting Volatile Organic Compound (VOC) emissions, significantly impact the rotogravure printing ink market. These regulations compel manufacturers to innovate and shift towards eco-friendly formulations like water-based and bio-based inks, reducing the reliance on traditional solvent-based systems. Compliance often leads to increased research and development costs but also opens new market opportunities for sustainable products.

What is the future outlook for the rotogravure printing ink market?

The future outlook for the rotogravure printing ink market is positive, driven by the continuous expansion of the flexible packaging industry, especially in emerging economies. While facing competition from digital and flexographic printing, rotogravure's strengths in high-quality, high-volume production ensure its sustained relevance. Innovation in sustainable inks and functional applications will be crucial for long-term growth and market competitiveness.

Which region dominates the rotogravure printing ink market?

The Asia Pacific (APAC) region currently dominates the rotogravure printing ink market. This dominance is attributed to rapid industrialization, burgeoning manufacturing sectors, and increasing consumer demand for packaged goods in countries like China, India, and Southeast Asian nations. The region's expanding food and beverage industry and growing disposable incomes further fuel the demand for high-quality packaging and printed materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted