Data Center Cooling Market

Data Center Cooling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708046 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

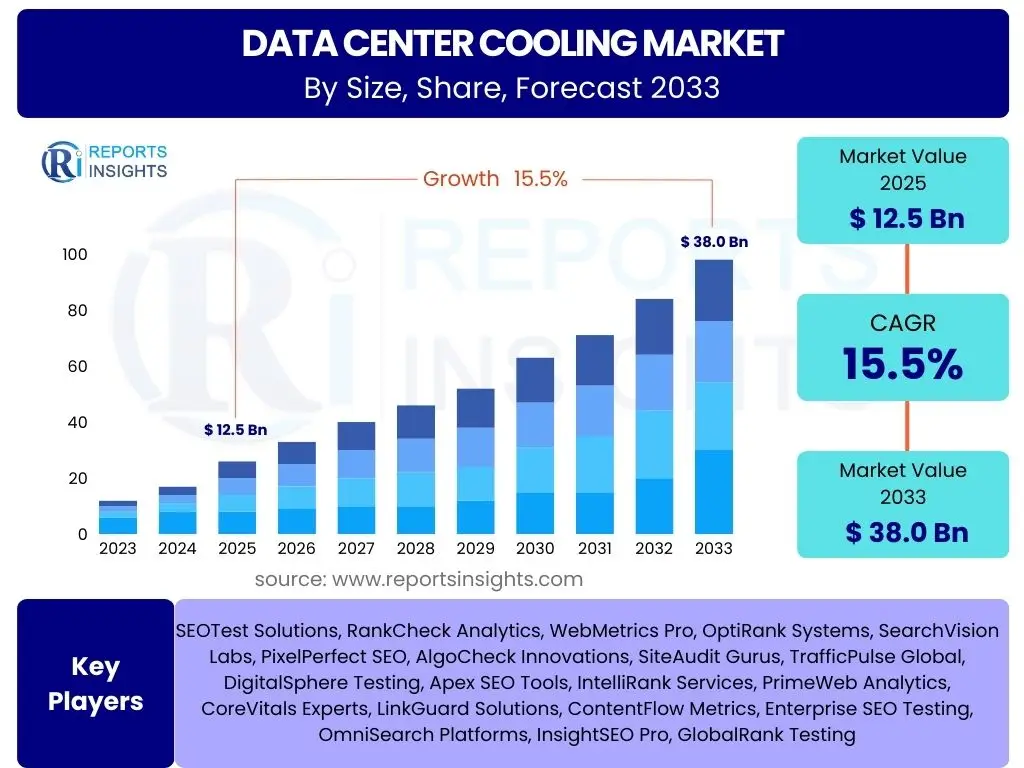

Data Center Cooling Market Size

According to Reports Insights Consulting Pvt Ltd, The Data Center Cooling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 38.0 Billion by the end of the forecast period in 2033.

Key Data Center Cooling Market Trends & Insights

Market inquiries frequently highlight the accelerating demand for energy-efficient and sustainable cooling solutions as data center power densities increase. Users are keen to understand how emerging technologies like liquid cooling and AI-driven thermal management are shaping the industry. There is a strong emphasis on reducing operational costs and environmental impact, driving innovation towards more eco-friendly and economically viable cooling strategies.

The proliferation of artificial intelligence, machine learning, and high-performance computing workloads necessitates more advanced and effective cooling methods to prevent overheating and ensure optimal performance. This shift is leading to a significant evolution from traditional air-based cooling towards hybrid and liquid-based systems. Additionally, the move towards modular and scalable data center designs also influences cooling infrastructure, requiring flexible solutions that can adapt to varying load requirements and physical constraints.

- Increased adoption of liquid cooling technologies (e.g., immersion cooling, direct-to-chip).

- Rising demand for energy-efficient and sustainable cooling solutions.

- Integration of Artificial Intelligence (AI) and Machine Learning (ML) for optimized thermal management.

- Growth of edge computing necessitating compact and efficient cooling systems.

- Emphasis on Power Usage Effectiveness (PUE) and Water Usage Effectiveness (WUE) improvements.

- Development of modular and scalable cooling infrastructure.

- Utilization of waste heat recovery systems for energy reuse.

AI Impact Analysis on Data Center Cooling

Common user questions regarding AI's impact on data center cooling often center on how these advanced technologies will manage the unprecedented heat generated by AI workloads. Users express concerns about the increased power density of AI servers and the need for more efficient, real-time cooling solutions. They are also interested in how AI itself can be leveraged to optimize cooling systems, reduce energy consumption, and predict potential failures, thereby enhancing overall operational efficiency and reliability.

The deployment of AI and machine learning applications introduces significant challenges for traditional cooling infrastructures due to the substantial computational power required, resulting in higher heat flux densities at the chip and rack levels. This necessitates a paradigm shift towards more direct and effective cooling methods, such as direct-to-chip liquid cooling or full immersion cooling, which can efficiently dissipate intense heat loads. Beyond simply addressing increased heat, AI is also revolutionizing cooling management by enabling predictive analytics, smart control systems, and automated adjustments to optimize cooling performance and energy consumption dynamically.

- Higher heat generation from AI/ML chips demands more advanced cooling solutions.

- AI-driven analytics optimize cooling system performance, predicting failures and adjusting settings.

- Increased adoption of liquid cooling specifically for high-density AI server racks.

- Enhanced energy efficiency through intelligent thermal management reduces PUE.

- Facilitates dynamic cooling adjustments based on real-time workload demands.

- Drives innovation in heat recovery and reuse from high-temperature AI exhaust.

Key Takeaways Data Center Cooling Market Size & Forecast

User inquiries about key takeaways from the Data Center Cooling market size and forecast consistently highlight the critical role of cooling in supporting the explosive growth of data centers driven by digital transformation and AI. Stakeholders are keen to understand the financial implications of adopting advanced cooling technologies and the long-term ROI. The market is clearly moving towards solutions that balance high performance with sustainability and cost-effectiveness, emphasizing innovation as a core driver.

The forecast period reveals a market undergoing rapid evolution, characterized by significant investment in research and development to address the escalating thermal management challenges. Key takeaways underscore that conventional air-cooling methods are increasingly insufficient for modern high-density data centers, particularly with the rise of AI workloads. Consequently, the market growth is significantly propelled by the imperative to adopt more efficient, scalable, and environmentally conscious cooling technologies, directly impacting data center operational expenditures and environmental footprint.

- Rapid market growth driven by increasing data center power densities and AI adoption.

- Significant shift from traditional air cooling to advanced liquid cooling solutions.

- Strong emphasis on energy efficiency and sustainability as primary investment criteria.

- Opportunities for innovation in AI-driven thermal management and waste heat recovery.

- Increasing capital expenditure (CAPEX) on sophisticated cooling infrastructure.

- Regulatory pressures and corporate sustainability goals are shaping market direction.

Data Center Cooling Market Drivers Analysis

The proliferation of digital services, cloud computing, and advanced analytics worldwide is fundamentally transforming the data center landscape, significantly driving the demand for more robust and efficient cooling solutions. As enterprises increasingly migrate their operations to the cloud and adopt hyper-converged infrastructure, the density of IT equipment within data centers escalates, leading to higher heat loads that traditional cooling systems struggle to manage. This persistent increase in data processing and storage requirements necessitates continuous innovation in thermal management to ensure optimal operational performance and prevent hardware failures.

Furthermore, the escalating adoption of Artificial Intelligence (AI) and Machine Learning (ML) applications across various industries is a paramount driver. These computationally intensive workloads generate unprecedented levels of heat within servers, pushing the boundaries of existing cooling technologies. Consequently, there is an urgent need for advanced cooling methods, such as direct-to-chip liquid cooling and immersion cooling, which are more effective at dissipating concentrated heat. Additionally, the growing focus on energy efficiency, driven by rising energy costs and stringent environmental regulations, compels data center operators to invest in cooling solutions that reduce power consumption and improve Power Usage Effectiveness (PUE), thereby lowering operational expenses and contributing to sustainability goals.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Data Center Density and IT Workloads | +3.0-4.0% | Global, particularly North America, APAC, Europe | Short to Medium Term (2025-2030) |

| Rising Adoption of AI, ML, and HPC | +3.5-4.5% | Global, especially US, China, Western Europe | Short to Long Term (2025-2033) |

| Growth of Cloud Computing and Edge Data Centers | +2.5-3.5% | Global, all emerging economies | Medium Term (2026-2032) |

| Focus on Energy Efficiency and Sustainability | +2.0-3.0% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

| Stringent Environmental Regulations and PUE Targets | +1.5-2.5% | Europe, North America | Medium to Long Term (2027-2033) |

| Need for Reduced Operational Costs (OpEx) | +1.0-2.0% | Global | Short to Medium Term (2025-2030) |

Data Center Cooling Market Restraints Analysis

Despite the robust growth drivers, the data center cooling market faces several significant restraints that could impede its expansion. One primary challenge is the substantial capital expenditure (CAPEX) associated with deploying advanced cooling infrastructure, particularly liquid cooling systems. The initial investment required for specialized equipment, redesigned data center layouts, and a different operational paradigm can be prohibitive for many organizations, especially small and medium-sized enterprises (SMEs) or those with legacy infrastructure that would require extensive retrofitting.

Another key restraint is the high operational complexity and maintenance requirements of sophisticated cooling systems. Implementing and managing liquid cooling or hybrid systems often demands specialized skills and knowledge that are not readily available in the existing workforce, leading to increased training costs and potential operational inefficiencies. Furthermore, the significant energy consumption of cooling systems, even advanced ones, continues to be a concern, contributing to a substantial portion of a data center's total energy bill and raising environmental impact issues. While new technologies aim to improve energy efficiency, the sheer scale of data center operations means that even marginal inefficiencies can lead to considerable energy waste and higher carbon footprints, posing a constant challenge for operators striving for sustainability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure (CAPEX) | -2.0-3.0% | Global, particularly SMEs | Short to Medium Term (2025-2030) |

| Operational Complexity and Maintenance Requirements | -1.5-2.5% | Global, particularly developing regions | Medium Term (2026-2032) |

| Significant Energy Consumption of Cooling Systems | -1.0-2.0% | Global, especially regions with high energy costs | Short to Long Term (2025-2033) |

| Legacy Infrastructure and Retrofitting Challenges | -1.0-1.5% | North America, Europe | Medium to Long Term (2027-2033) |

| Concerns over Liquid Leaks and System Reliability | -0.5-1.0% | Global | Short to Medium Term (2025-2030) |

Data Center Cooling Market Opportunities Analysis

The evolving data center landscape presents numerous opportunities for innovation and market expansion in cooling technologies. One significant opportunity lies in the continued advancements and broader adoption of liquid cooling solutions, including direct-to-chip, immersion, and hybrid systems. As server power densities surge, particularly with the advent of AI and high-performance computing, traditional air cooling reaches its limits, creating a compelling need for more efficient and localized liquid-based heat dissipation. This shift opens new avenues for manufacturers to develop and commercialize highly specialized and scalable liquid cooling products that cater to ultra-high-density environments.

Furthermore, the growing emphasis on sustainability and energy efficiency across all industries presents a substantial opportunity for data center cooling providers. Innovations in waste heat recovery systems, which capture and reuse excess heat generated by IT equipment for other purposes (e.g., district heating, facility warming), are gaining traction. This not only reduces the overall carbon footprint of data centers but also offers potential cost savings and compliance with green initiatives. Additionally, the proliferation of edge computing, demanding compact, low-latency data processing closer to the source, creates a distinct market for smaller, more modular, and highly efficient cooling solutions tailored for diverse and often remote environments, offering new design and deployment models for cooling infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanded Adoption of Liquid Cooling Technologies | +3.0-4.0% | Global, particularly developed regions | Short to Long Term (2025-2033) |

| Development of AI-driven Predictive Cooling Solutions | +2.5-3.5% | Global, with emphasis on tech hubs | Medium to Long Term (2026-2033) |

| Integration of Waste Heat Recovery Systems | +2.0-3.0% | Europe, North America, Japan | Medium Term (2027-2032) |

| Growth in Modular and Edge Data Center Cooling Solutions | +1.5-2.5% | Global, especially emerging markets | Short to Medium Term (2025-2030) |

| Partnerships for Hybrid Cooling System Development | +1.0-2.0% | Global | Medium Term (2026-2032) |

Data Center Cooling Market Challenges Impact Analysis

The data center cooling market confronts significant challenges in optimizing Power Usage Effectiveness (PUE) and Water Usage Effectiveness (WUE) metrics, which are crucial for both environmental sustainability and operational cost efficiency. Achieving optimal PUE requires sophisticated integration of cooling systems with IT workloads, dynamic adjustments, and continuous monitoring, often proving complex in real-world scenarios, particularly for older data centers. Similarly, the growing concern over global water scarcity places immense pressure on data center operators to minimize water consumption, pushing for the development of alternative cooling methods that require less or no water, such as adiabatic or dry cooling systems, which can be challenging to implement at scale.

Another substantial challenge stems from the increasing carbon footprint associated with data center operations, a significant portion of which is attributable to cooling. As regulatory bodies and corporate sustainability goals become more stringent, there is an urgent need to deploy ultra-efficient cooling technologies powered by renewable energy sources, which presents complexities in terms of infrastructure investment and grid integration. Moreover, the rapid pace of technological advancements, particularly in high-density computing and AI, often outstrips the development and adoption of corresponding cooling solutions. This creates a perpetual cycle where cooling infrastructure struggles to keep pace with the ever-increasing thermal demands of new IT equipment, leading to potential performance bottlenecks and design obsolescence.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Difficulty in Achieving Optimal PUE and WUE | -2.0-3.0% | Global | Short to Medium Term (2025-2030) |

| Growing Concerns Over Water Scarcity and Usage | -1.5-2.5% | MEA, APAC, arid regions | Medium to Long Term (2026-2033) |

| Increasing Carbon Footprint of Data Centers | -1.0-2.0% | Europe, North America | Medium to Long Term (2027-2033) |

| Lack of Skilled Workforce for Advanced Cooling Systems | -1.0-1.5% | Global, particularly developing economies | Short to Medium Term (2025-2030) |

| Rapid Technological Obsolescence of Cooling Infrastructure | -0.5-1.0% | Global | Short Term (2025-2028) |

Data Center Cooling Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the Data Center Cooling Market, offering an exhaustive analysis of its size, growth trajectory, and influential factors. The report provides detailed insights into market segmentation, competitive landscape, and regional trends, equipping stakeholders with critical intelligence for strategic decision-making. It highlights the evolving technological landscape, including the impact of AI and sustainable practices, to present a holistic view of current and future market opportunities and challenges.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 38.0 Billion |

| Growth Rate | 15.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vertiv, Schneider Electric, Eaton, Rittal, Stulz GmbH, Daikin Industries, Ltd., Asetek, Submer, Fujitsu Ltd., IBM Corporation, Dell Technologies, Inc., Huawei Technologies Co., Ltd., Green Revolution Cooling, Inc., CoolIT Systems, Inc., Motivair Corporation, Danfoss A/S, Emerson Electric Co., Johnson Controls International plc, Siemens AG, Alfa Laval AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Data Center Cooling Market is extensively segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for precise analysis of market trends, growth drivers, and opportunities across different cooling technologies, system components, service offerings, and end-user verticals. Understanding these distinct segments is crucial for identifying niche markets, tailoring product development, and devising effective market penetration strategies.

Each segment, from the type of cooling technology employed to the specific industry vertical benefiting from these solutions, exhibits unique growth patterns and demands. For instance, the liquid-based cooling segment is projected for substantial growth due to its efficiency in managing high heat loads from AI, while the service segment reflects the increasing need for specialized expertise in installation, maintenance, and optimization. This detailed breakdown ensures that all facets of the market are thoroughly examined, providing a comprehensive outlook for stakeholders.

- By Type:

- Air-based Cooling:

- CRAC/CRAH (Computer Room Air Conditioner/Handler) Units

- Chillers (Air-cooled, Water-cooled)

- Cooling Towers

- Free Cooling Units (Economizers)

- In-Row/In-Rack Coolers

- Liquid-based Cooling:

- Direct-to-Chip Cooling

- Immersion Cooling (Single-phase, Two-phase)

- Hybrid Cooling Systems

- Coolant Distribution Units (CDUs)

- By Component:

- Cooling Systems

- Cooling Distribution Units (CDUs)

- Pumps

- Heat Exchangers

- Control Systems (Software, Sensors)

- Others (Piping, Racks, Monitoring Devices)

- By Service:

- Installation and Deployment Services

- Maintenance and Support Services

- Consulting and Professional Services

- Managed Cooling Services

- By End-User:

- Colocation Data Centers

- Enterprise Data Centers

- Cloud Providers

- Telecom Operators

- Edge Computing Facilities

- Hyperscale Data Centers

- By Industry Vertical:

- IT and Telecommunications

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare and Life Sciences

- Retail and E-commerce

- Government and Defense

- Media and Entertainment

- Energy and Utilities

- Manufacturing

- Others

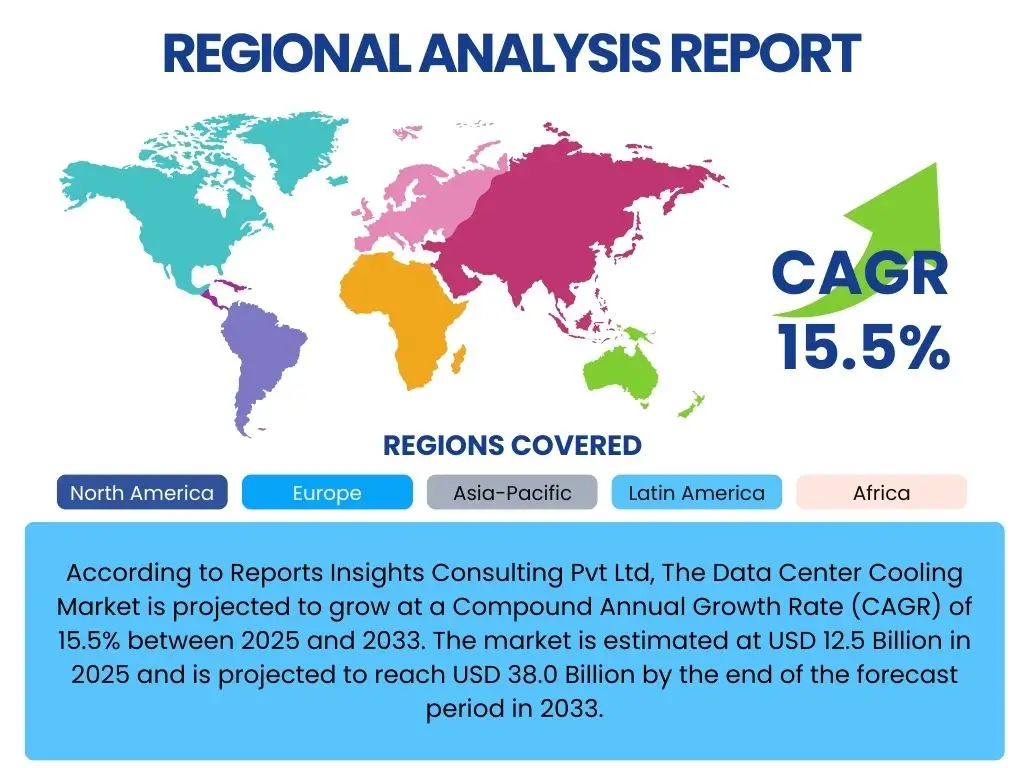

Regional Highlights

- North America: This region is a dominant force in the Data Center Cooling Market, driven by a high concentration of hyperscale data centers, robust cloud adoption, and significant investments in AI and high-performance computing. The presence of major tech giants and stringent energy efficiency regulations further accelerates the adoption of advanced cooling solutions. Innovation in liquid cooling and modular data centers is particularly strong here.

- Europe: Europe exhibits strong growth, fueled by increasing data localization laws, an intensifying focus on sustainability, and ambitious carbon neutrality goals. Countries like Germany, the UK, and the Nordics are at the forefront of adopting free cooling and waste heat recovery technologies, driven by both regulatory mandates and a high consciousness for environmental impact.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to rapid digitalization, expanding internet penetration, and massive investments in data center infrastructure across countries like China, India, Japan, and Australia. The burgeoning e-commerce, cloud services, and telecom sectors are driving demand, although energy costs and access to sustainable power remain key considerations.

- Latin America: This region is experiencing a gradual but steady increase in data center deployments, with Brazil and Mexico leading the adoption. The market growth is primarily supported by rising cloud services demand, digital transformation initiatives, and the establishment of local data centers to improve data sovereignty and reduce latency.

- Middle East and Africa (MEA): MEA is an emerging market for data center cooling, with significant investments in digital infrastructure, particularly in the UAE, Saudi Arabia, and South Africa. The region faces unique challenges related to climate and water scarcity, spurring interest in efficient, water-conserving cooling technologies and renewable energy integration.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Data Center Cooling Market.- Vertiv

- Schneider Electric

- Eaton

- Rittal

- Stulz GmbH

- Daikin Industries, Ltd.

- Asetek

- Submer

- Fujitsu Ltd.

- IBM Corporation

- Dell Technologies, Inc.

- Huawei Technologies Co., Ltd.

- Green Revolution Cooling, Inc.

- CoolIT Systems, Inc.

- Motivair Corporation

- Danfoss A/S

- Emerson Electric Co.

- Johnson Controls International plc

- Siemens AG

- Alfa Laval AB

Frequently Asked Questions

Analyze common user questions about the Data Center Cooling market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is data center cooling and why is it essential?

Data center cooling refers to the systems and methods used to remove heat generated by IT equipment to maintain optimal operating temperatures. It is essential to prevent hardware failure, ensure system stability, and maximize the efficiency and lifespan of servers and other critical infrastructure. Without effective cooling, data centers would quickly overheat, leading to costly downtime and equipment damage.

What are the primary types of data center cooling technologies?

The primary types of data center cooling include air-based cooling and liquid-based cooling. Air-based systems use CRAC/CRAH units, chillers, and cooling towers to circulate cooled air. Liquid-based cooling, such as direct-to-chip or immersion cooling, uses fluids that are significantly more efficient at dissipating heat, especially for high-density AI and HPC workloads.

How do AI and Machine Learning influence data center cooling solutions?

AI and Machine Learning significantly influence data center cooling by generating higher heat loads that demand more advanced cooling methods like liquid cooling. Simultaneously, AI can optimize cooling systems through predictive analytics, real-time adjustments, and automated controls to improve energy efficiency (PUE) and reduce operational costs by anticipating thermal needs and preventing issues.

What are the main drivers and challenges in the Data Center Cooling Market?

Key drivers include the surge in data center density, widespread adoption of AI/ML, and the growth of cloud and edge computing. Major challenges involve the high initial capital expenditure for advanced systems, the operational complexity of managing new technologies, persistent energy consumption concerns, and the need for skilled personnel to implement and maintain these sophisticated solutions.

What are the future trends in data center cooling?

Future trends in data center cooling emphasize increased adoption of liquid cooling technologies (immersion and direct-to-chip), greater integration of AI for smart thermal management, a strong focus on energy efficiency and sustainability through waste heat recovery, and the development of modular cooling solutions for edge computing. The industry is moving towards highly efficient, environmentally conscious, and scalable systems.

- Air-based Cooling:

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted