Cyber Security Insurance Market

Cyber Security Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705437 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

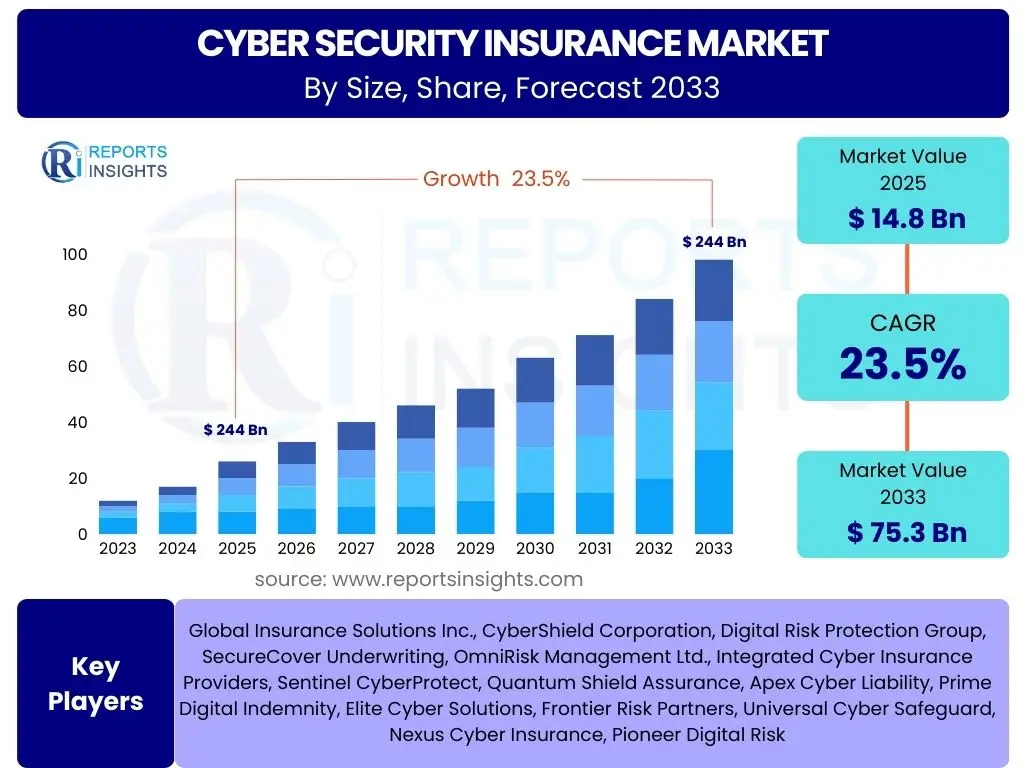

Cyber Security Insurance Market Size

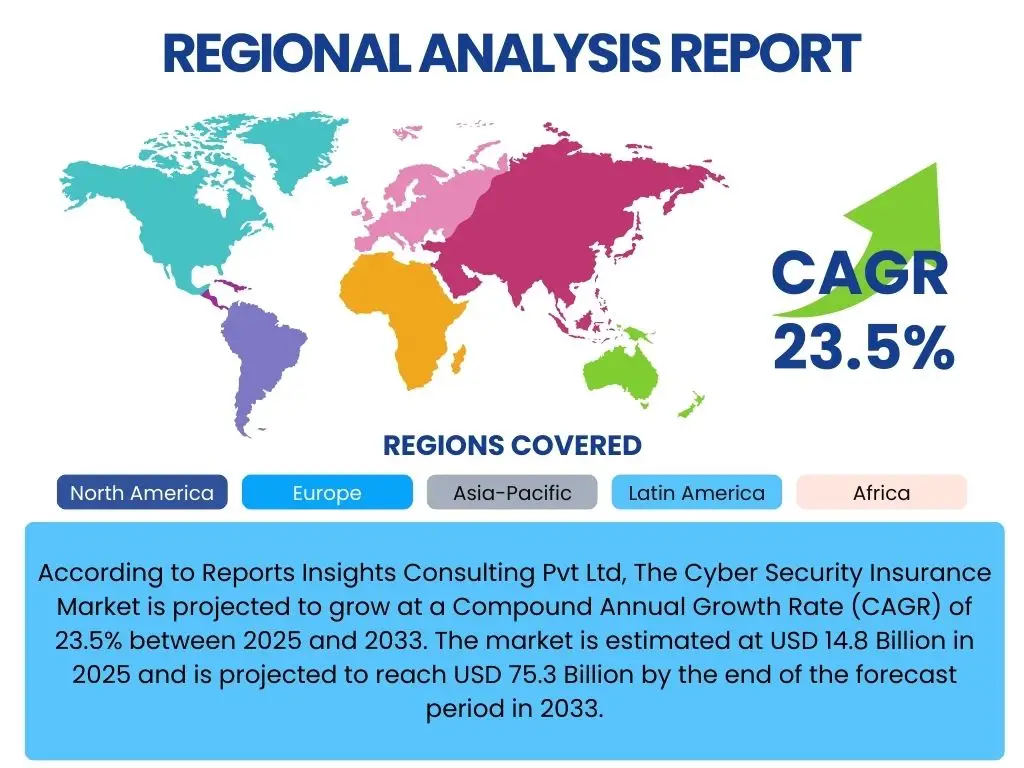

According to Reports Insights Consulting Pvt Ltd, The Cyber Security Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 23.5% between 2025 and 2033. The market is estimated at USD 14.8 Billion in 2025 and is projected to reach USD 75.3 Billion by the end of the forecast period in 2033.

Key Cyber Security Insurance Market Trends & Insights

The Cyber Security Insurance market is undergoing significant transformation, driven by a confluence of escalating cyber threats and evolving regulatory landscapes. Users frequently inquire about the impact of ransomware, phishing attacks, and data breaches on insurance premiums and policy structures. The increasing sophistication of cyber adversaries necessitates more dynamic and comprehensive insurance offerings, leading to a shift from basic liability coverage to more holistic risk management solutions that include pre-breach services, incident response, and post-breach recovery assistance. There is a growing demand for policies that are not merely reactive but integrate proactive measures to enhance an organization's overall cyber resilience.

Another prominent trend is the rising integration of cyber insurance with broader enterprise risk management frameworks. Organizations are recognizing that cyber risk is an enterprise-wide concern, not just an IT issue, leading to a greater collaboration between IT, legal, finance, and risk management departments when procuring cyber insurance. This holistic approach is prompting insurers to offer more tailored policies that account for an organization's specific industry, threat landscape, and existing security posture. Furthermore, the growth of cloud computing and remote work models has expanded the attack surface, increasing the complexity of underwriting and claims, and driving the need for policies that adequately cover these distributed environments.

The market also exhibits a trend towards greater standardization and transparency in policy language, although significant variations still exist. Insurers are leveraging advanced data analytics and artificial intelligence to refine risk assessment models, aiming for more accurate premium calculations and better understanding of emerging threats. This technological adoption helps in developing more customized products and improving the efficiency of claims processing. Moreover, the increasing regulatory scrutiny on data protection and privacy, such as GDPR and CCPA, is making cyber insurance a compliance imperative for many businesses, especially those operating across multiple jurisdictions, further solidifying its position as an essential business safeguard.

- Escalating sophistication and frequency of cyberattacks (e.g., ransomware, supply chain attacks).

- Increased regulatory pressure and compliance requirements (e.g., data privacy laws).

- Shift towards comprehensive risk management, integrating pre-breach and post-breach services.

- Growing demand for tailored policies for specific industries and business sizes.

- Wider adoption of cloud services and remote work models expanding attack surfaces.

- Greater use of data analytics and AI for enhanced risk assessment and underwriting.

- Emphasis on transparency and standardization in policy terms and conditions.

AI Impact Analysis on Cyber Security Insurance

The integration of Artificial Intelligence (AI) is profoundly reshaping the Cyber Security Insurance landscape, addressing key user questions regarding risk assessment accuracy, claims efficiency, and the evolving nature of cyber threats. AI's capacity to process vast datasets enables insurers to develop highly sophisticated underwriting models that can more accurately assess an applicant's cyber risk profile, analyzing historical breach data, security posture, industry benchmarks, and behavioral patterns. This leads to more precise premium calculations and a clearer understanding of potential liabilities, moving away from generalized assumptions to data-driven insights. Moreover, AI-powered tools can monitor real-time threat intelligence, providing dynamic risk scores that allow for adaptive policy adjustments.

However, AI's impact is dual-edged. While it enhances defensive capabilities for insurers and policyholders, it also empowers cybercriminals to launch more sophisticated and evasive attacks. Users frequently express concerns about AI-powered phishing campaigns, automated malware, and intelligent denial-of-service attacks that are harder to detect and mitigate with traditional security measures. This escalation in attack sophistication places greater pressure on insurance policies to cover novel and rapidly evolving threat vectors, potentially leading to increased claims complexity and payout amounts. Insurers must continuously adapt their offerings to account for these AI-driven threats, perhaps by requiring policyholders to implement AI-powered security solutions as a condition for coverage or lower premiums.

Furthermore, AI is streamlining operations within the insurance sector itself. In claims processing, AI can automate the initial assessment of incidents, rapidly identifying the scope of a breach, estimating potential damages, and flagging fraudulent claims, thereby accelerating the payout process for legitimate incidents. For policyholders, AI-driven security tools can provide continuous monitoring, early warning systems, and automated incident response, reducing the likelihood and severity of cyber events, which in turn can lead to lower insurance premiums. The ongoing challenge lies in balancing the benefits of AI in risk mitigation and operational efficiency against the escalating risks posed by AI-enabled cyber threats, necessitating a proactive and adaptive approach from both insurers and policyholders.

- Enhanced risk assessment and underwriting through advanced data analytics and predictive modeling.

- Improved fraud detection and claims processing efficiency.

- Development of personalized policies based on dynamic risk profiles.

- Increased sophistication of cyberattacks powered by AI, leading to new threat vectors.

- Potential for AI-driven security solutions to become a prerequisite for certain coverages.

- Automation of threat intelligence gathering and real-time risk scoring.

- Challenges in quantifying and insuring against novel AI-generated cyber risks.

Key Takeaways Cyber Security Insurance Market Size & Forecast

The Cyber Security Insurance market is poised for robust and sustained growth, driven by an ever-expanding digital footprint across all industries and the increasing financial and reputational costs associated with cyber breaches. Common user questions highlight the criticality of understanding not just the market's size but also the underlying factors that will sustain its momentum. A primary takeaway is that cyber insurance is transitioning from a niche offering to an essential component of enterprise risk management, reflecting a broader recognition that no organization is entirely immune to cyber threats. This shift is fueling demand across diverse sectors, from large enterprises with complex IT infrastructures to small and medium-sized enterprises (SMEs) that often lack dedicated cybersecurity resources.

Another significant takeaway is the market's dynamic evolution, characterized by continuous innovation in policy design and service offerings. Insurers are increasingly bundling pre-breach services, such as vulnerability assessments and employee training, with post-breach incident response and recovery support. This integrated approach aims to reduce both the frequency and severity of cyber incidents, ultimately benefiting both policyholders and insurers. The forecast indicates that this trend towards comprehensive solutions will accelerate, making policies more valuable and driving further market penetration, particularly as organizations seek to mitigate not just direct financial losses but also business interruption and regulatory fines.

Furthermore, the market's strong growth trajectory is underpinned by a global increase in regulatory mandates concerning data protection and breach notification. Compliance requirements in regions like North America and Europe are compelling businesses to seek robust insurance coverage to manage potential liabilities. This regulatory push, combined with heightened corporate governance expectations regarding cyber resilience, ensures a steady demand for specialized cyber insurance products. The market's future will also be shaped by technological advancements, including the pervasive influence of AI on both cyber defense and offense, necessitating adaptive underwriting practices and flexible policy structures to address the rapidly evolving threat landscape.

- The Cyber Security Insurance market demonstrates strong, sustained growth due to pervasive digitalization and escalating cyber threats.

- Cyber insurance is evolving into a core component of enterprise risk management for businesses of all sizes.

- Policy innovation is driving comprehensive offerings, bundling pre-breach services with incident response and recovery.

- Regulatory compliance and corporate governance mandates are key demand drivers across regions.

- Technological advancements, particularly in AI, will continue to reshape both risks and insurance solutions.

- Increased awareness of financial and reputational risks from cyber incidents is boosting adoption rates.

- The market is expanding beyond traditional large enterprises to include underserved SMEs.

Cyber Security Insurance Market Drivers Analysis

The proliferation of sophisticated cyberattacks globally stands as a primary catalyst for the expansion of the Cyber Security Insurance market. As threat actors leverage advanced techniques such as ransomware-as-a-service, supply chain attacks, and AI-powered phishing, businesses face unprecedented levels of risk to their data, operations, and financial stability. This escalating threat landscape compels organizations across all sectors to seek financial protection and risk transfer mechanisms, thereby driving the demand for specialized cyber insurance policies. The increasing frequency and severity of breaches mean that the potential costs of recovery, legal fees, regulatory fines, and reputational damage are too significant for most businesses to absorb without insurance, making it a critical safeguard in the modern digital economy.

Stringent data privacy regulations worldwide are also significantly contributing to market growth. Laws such as the General Data Protection Regulation (GDPR) in Europe, the California Consumer Privacy Act (CCPA) in the United States, and similar legislations in other regions impose substantial penalties for data breaches and mandate strict notification requirements. These regulatory frameworks heighten a company's financial exposure in the event of a cyber incident, making cyber insurance an indispensable tool for compliance and liability management. Businesses are proactively acquiring cyber insurance not only to cover potential fines and legal costs but also to demonstrate due diligence in protecting sensitive customer and corporate data, thereby reducing regulatory and legal vulnerabilities.

The rapid pace of digital transformation, including the widespread adoption of cloud computing, IoT devices, and remote work models, has expanded the attack surface for organizations. This increased interconnectedness and reliance on digital infrastructure create new vulnerabilities and complexities in securing corporate assets. As businesses migrate critical operations and data to cloud environments or enable employees to work remotely, the risks associated with these distributed ecosystems necessitate specialized insurance coverage that can address incidents originating from various points within the expanded digital perimeter. Cyber insurance provides a vital safety net for organizations navigating these evolving digital landscapes, offering protection against the unique risks associated with modern IT architectures.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalation of Cyberattacks and Data Breaches | +7.5% | Global, particularly North America, Europe, APAC | Short to Medium Term (2025-2029) |

| Growing Regulatory Scrutiny and Compliance Requirements | +6.8% | Europe (GDPR), North America (CCPA, HIPAA), Asia Pacific (e.g., PDPA) | Medium Term (2026-2031) |

| Increasing Digital Transformation and Cloud Adoption | +5.2% | Global, especially emerging economies in APAC and Latin America | Short to Medium Term (2025-2030) |

| Rising Awareness and Understanding of Cyber Risks | +4.1% | Global, particularly SMEs in all regions | Medium to Long Term (2027-2033) |

| Demand for Comprehensive Risk Management Solutions | +3.9% | Developed economies in North America and Europe | Medium Term (2026-2032) |

Cyber Security Insurance Market Restraints Analysis

One significant restraint impacting the Cyber Security Insurance market is the high cost of premiums, particularly for small and medium-sized enterprises (SMEs) and organizations operating in high-risk sectors. As cyberattacks become more frequent and sophisticated, insurers face greater potential liabilities, leading to increased premiums. For many businesses, especially those with limited budgets, the cost of comprehensive cyber insurance can be prohibitive, acting as a barrier to adoption. This is compounded by the fact that many insurers are still refining their risk models, which can lead to conservative pricing that does not always align with a company's specific risk exposure, making it difficult for some to justify the investment in insurance.

The lack of standardized policies and clear definitions within cyber insurance contracts presents another significant challenge. Unlike traditional insurance products, cyber insurance is a relatively new and evolving field, resulting in considerable variation in policy wordings, exclusions, and coverage limits across different providers. This lack of standardization can create confusion for policyholders regarding what is actually covered, leading to potential disputes during claims and a general hesitance to invest in policies perceived as ambiguous or overly complex. The technical nature of cyber risks also makes it difficult for non-experts to fully understand policy terms, further exacerbating this issue and limiting market transparency.

Another major restraint stems from the difficulty in accurately quantifying cyber risks and assessing an applicant's true security posture. Cyber threats evolve rapidly, making it challenging for insurers to keep pace with new vulnerabilities and attack methods. This uncertainty makes precise risk modeling and underwriting difficult, often leading to either overly broad or overly restrictive policies. Furthermore, businesses may not always provide complete or accurate information about their cybersecurity measures, leading to information asymmetry that complicates risk assessment. This inherent difficulty in precise risk quantification can lead to mispriced policies, high claim ratios for insurers, and dissatisfaction among policyholders who feel their premiums do not accurately reflect their efforts in cybersecurity.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Premiums and Cost Barriers for SMEs | -4.5% | Global, particularly developing regions | Short to Medium Term (2025-2029) |

| Lack of Standardization and Complex Policy Language | -3.8% | Global, particularly less mature markets | Medium Term (2026-2031) |

| Difficulty in Accurate Risk Quantification and Underwriting | -3.1% | Global, impacts both mature and emerging markets | Short to Medium Term (2025-2030) |

| Moral Hazard and Adverse Selection Issues | -2.5% | Developed economies with higher policy adoption rates | Medium Term (2027-2032) |

| Exclusions and Limited Coverage for Advanced Threats | -2.0% | Global, particularly for cutting-edge technologies | Long Term (2028-2033) |

Cyber Security Insurance Market Opportunities Analysis

The burgeoning demand from small and medium-sized enterprises (SMEs) represents a significant growth opportunity for the Cyber Security Insurance market. While large corporations have increasingly adopted cyber insurance, SMEs, which often lack the dedicated cybersecurity resources and expertise of larger entities, remain largely underserved. These businesses are equally, if not more, vulnerable to cyberattacks and often bear disproportionate financial burdens from breaches. Developing tailored, affordable, and easy-to-understand cyber insurance products specifically designed for SMEs, coupled with simplified underwriting processes and integrated cybersecurity advisory services, can unlock a vast untapped market segment globally, driving substantial revenue growth for insurers.

Integration of cyber insurance with broader cybersecurity services presents another compelling opportunity. As organizations seek comprehensive risk management solutions, insurers can differentiate themselves by offering bundled packages that combine insurance coverage with proactive cybersecurity measures, such as threat intelligence, vulnerability assessments, incident response planning, and security awareness training. This value-added approach not only enhances a policyholder's cyber resilience, potentially reducing claims, but also establishes insurers as strategic partners in risk mitigation rather than just financial indemnifiers. Such integrated offerings can attract a wider client base and foster stronger, long-term relationships, creating a more robust ecosystem for cyber risk management.

The continuous evolution of digital technologies and the emergence of new threat vectors create opportunities for specialized and innovative policy development. As industries adopt emerging technologies like Artificial Intelligence, blockchain, quantum computing, and advanced IoT, new cyber risks arise that existing policies may not fully address. Insurers have an opportunity to develop highly specialized policies that cater to the unique risk profiles of specific industries (e.g., healthcare, critical infrastructure, manufacturing) or cover risks associated with novel technologies. Furthermore, the development of parametric insurance models, which trigger payouts based on pre-defined events (e.g., a specific type of ransomware attack) rather than traditional damage assessment, could offer more rapid and transparent claims processing, attracting businesses seeking clearer and faster compensation mechanisms.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Market in Small and Medium-sized Enterprises (SMEs) | +5.5% | Global, particularly Asia Pacific and Latin America | Medium to Long Term (2027-2033) |

| Integration with Broader Cybersecurity Services | +4.8% | North America, Europe, mature markets in APAC | Short to Medium Term (2025-2030) |

| Development of Specialized and Tailored Policies | +4.1% | Global, targeting specific industries and advanced technologies | Medium Term (2026-2032) |

| Expansion into Critical Infrastructure and OT Security | +3.5% | North America, Europe, select APAC countries | Medium to Long Term (2028-2033) |

| Leveraging Advanced Analytics and AI for Personalized Products | +3.0% | Developed economies with high tech adoption | Short to Medium Term (2025-2029) |

Cyber Security Insurance Market Challenges Impact Analysis

The rapid and unpredictable evolution of cyber threats poses a significant challenge for the Cyber Security Insurance market. Threat actors constantly innovate, developing new attack vectors, malware strains, and social engineering techniques that can quickly bypass existing security defenses. This dynamic threat landscape makes it incredibly difficult for insurers to accurately assess future risks, price policies appropriately, and ensure that coverage remains relevant. Policies can quickly become outdated as new threats emerge, leading to coverage gaps or unexpected liabilities for insurers, which in turn can lead to higher premiums or more restrictive policy terms for businesses. Maintaining pace with this evolving threat environment requires continuous investment in threat intelligence and advanced risk modeling capabilities.

Another major challenge is the inherent difficulty in accurately quantifying the financial impact of cyber incidents. Unlike tangible property damage, the costs associated with a data breach or ransomware attack can be multifaceted and elusive, encompassing not only direct financial losses from business interruption, ransom payments, and data recovery but also indirect costs such as reputational damage, customer churn, loss of intellectual property, and long-term legal liabilities. This complexity makes it challenging for both insurers to underwrite policies precisely and for policyholders to understand the full extent of their potential losses. The lack of standardized metrics for measuring cyber risk and financial impact across industries further compounds this issue, hindering transparency and comparability within the market.

The global shortage of skilled cybersecurity professionals presents a systemic challenge for the insurance market. As organizations struggle to find and retain talent capable of implementing robust security measures and responding effectively to incidents, their overall cyber risk profile increases. Insurers often require policyholders to demonstrate a certain level of cybersecurity maturity, but the talent gap can make it difficult for businesses, particularly SMEs, to meet these requirements. This shortage can also impact the availability and quality of incident response services, which are often a critical component of cyber insurance policies. Without adequate skilled personnel to manage and mitigate risks, both insured entities and insurers face elevated exposure to cyber events.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapidly Evolving Cyber Threat Landscape | -5.0% | Global, impacts all industries | Short to Medium Term (2025-2029) |

| Difficulty in Quantifying Cyber Risks and Financial Impact | -4.2% | Global, impacts underwriting accuracy | Medium Term (2026-2031) |

| Lack of Qualified Cybersecurity Professionals | -3.6% | Global, particularly North America and Europe | Medium to Long Term (2027-2033) |

| Systemic Risk and Accumulation Exposure for Insurers | -2.9% | Global, impacts large insurers and reinsurers | Long Term (2028-2033) |

| Ensuring Adequate Coverage for Novel and Emerging Technologies | -2.3% | Global, particularly for cutting-edge tech adopters | Short to Medium Term (2025-2030) |

Cyber Security Insurance Market - Updated Report Scope

This report offers a comprehensive analysis of the global Cyber Security Insurance Market, detailing market size estimations, growth drivers, restraints, opportunities, and challenges. It provides deep insights into market trends, competitive landscape, and regional dynamics, utilizing a robust methodology to deliver actionable intelligence for stakeholders. The scope covers various segmentation categories, offering a granular view of market performance and future projections.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.8 Billion |

| Market Forecast in 2033 | USD 75.3 Billion |

| Growth Rate | 23.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Insurance Solutions Inc., CyberShield Corporation, Digital Risk Protection Group, SecureCover Underwriting, OmniRisk Management Ltd., Integrated Cyber Insurance Providers, Sentinel CyberProtect, Quantum Shield Assurance, Apex Cyber Liability, Prime Digital Indemnity, Elite Cyber Solutions, Frontier Risk Partners, Universal Cyber Safeguard, Nexus Cyber Insurance, Pioneer Digital Risk |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cyber Security Insurance market is meticulously segmented to provide a comprehensive understanding of its diverse landscape and to cater to the varied needs of businesses globally. These segmentations allow for a granular analysis of market dynamics, revealing key areas of growth, adoption patterns, and competitive strategies across different dimensions of the market. Understanding these segments is crucial for stakeholders to identify niche opportunities and develop targeted solutions.

- By Component:

- Solution (Standalone, Packaged)

- Service (Consulting, Training and Education, Risk Assessment, Incident Response, Others)

- By Coverage:

- Data Breach

- Network Security

- Cyber Extortion

- Business Interruption

- Media Liability

- Privacy Liability

- Funds Transfer Fraud

- Regulatory Fines

- By Organization Size:

- SMEs (Small and Medium-sized Enterprises)

- Large Enterprises

- By Industry Vertical:

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

- Retail and E-commerce

- IT and Telecom

- Manufacturing

- Government and Public Sector

- Energy and Utilities

- Others (Education, Media and Entertainment)

Regional Highlights

North America is anticipated to dominate the Cyber Security Insurance market, driven by a high concentration of technologically advanced enterprises, stringent regulatory frameworks like HIPAA and various state-specific data breach notification laws, and a heightened awareness of cyber risks among businesses and consumers. The region experiences a significant number of high-profile cyberattacks, compelling businesses to seek robust insurance coverage. Moreover, a mature insurance industry ecosystem and early adoption of innovative risk management solutions contribute to the region's leading position, with both large corporations and a growing number of SMEs investing in comprehensive cyber insurance policies to mitigate financial and reputational damages.

Europe is expected to exhibit substantial growth, primarily fueled by the pervasive influence of the General Data Protection Regulation (GDPR), which imposes significant penalties for data breaches and mandates strict data protection practices. This regulatory imperative has made cyber insurance a critical compliance tool for European businesses. Countries such as the UK, Germany, and France are at the forefront of adoption, driven by increasing cyber threat sophistication and a strong emphasis on corporate accountability for data security. The region's diverse economic landscape and the increasing digitalization of industries further contribute to the escalating demand for tailored cyber insurance solutions, with an emphasis on policies that cover both direct financial losses and regulatory fines.

The Asia Pacific (APAC) region is projected to be the fastest-growing market for Cyber Security Insurance, attributed to rapid digital transformation across countries like China, India, Japan, and Australia. The burgeoning e-commerce sector, expanding cloud adoption, and growing internet penetration are creating vast digital attack surfaces, leading to an increased incidence of cybercrimes. While awareness levels are still developing in some parts of the region, the rising cost of data breaches and the introduction of new data privacy laws (e.g., in Singapore, Australia, India) are compelling organizations to consider cyber insurance as an essential part of their risk management strategy. Investments in critical infrastructure and the rise of smart cities also underscore the need for advanced cyber protection, presenting significant opportunities for insurers.

Latin America and the Middle East & Africa (MEA) regions are also witnessing nascent but accelerating growth in the Cyber Security Insurance market. In Latin America, increasing internet penetration, growing digital economies, and emerging data protection regulations are slowly but surely driving demand. Brazil and Mexico are leading the charge in this region. In MEA, the push for digital transformation, particularly in Saudi Arabia and UAE, alongside efforts to diversify economies away from oil, is leading to significant investments in digital infrastructure, consequently increasing cyber exposure. As these regions continue to mature digitally, awareness of cyber risks and the necessity of insurance will grow, fostering market expansion over the forecast period, albeit at a slower pace compared to more developed markets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cyber Security Insurance Market.- Global Insurance Solutions Inc.

- CyberShield Corporation

- Digital Risk Protection Group

- SecureCover Underwriting

- OmniRisk Management Ltd.

- Integrated Cyber Insurance Providers

- Sentinel CyberProtect

- Quantum Shield Assurance

- Apex Cyber Liability

- Prime Digital Indemnity

- Elite Cyber Solutions

- Frontier Risk Partners

- Universal Cyber Safeguard

- Nexus Cyber Insurance

- Pioneer Digital Risk

Frequently Asked Questions

What is Cyber Security Insurance?

Cyber Security Insurance, also known as Cyber Liability Insurance, is a specialized type of insurance coverage designed to protect businesses from the financial losses and liabilities arising from cyberattacks, data breaches, and other cyber incidents. It typically covers costs associated with data recovery, legal fees, regulatory fines, business interruption, public relations, and notification expenses for affected parties.

What are the primary drivers of the Cyber Security Insurance market?

The key drivers include the escalating frequency and sophistication of cyberattacks (e.g., ransomware), increasingly stringent data privacy regulations (e.g., GDPR, CCPA) imposing hefty fines, widespread digital transformation and cloud adoption expanding attack surfaces, and a growing general awareness among businesses of their cyber risk exposure and the potential financial and reputational damages.

How does AI impact the Cyber Security Insurance market?

AI impacts the market in two key ways: it enhances insurers' capabilities for more accurate risk assessment, underwriting, and claims processing through advanced data analysis. However, it also empowers cybercriminals to execute more sophisticated and evasive attacks, leading to new threat vectors and increasing the complexity and potential costs of claims, requiring continuous adaptation of insurance offerings.

What are the main challenges facing the Cyber Security Insurance market?

Major challenges include the rapidly evolving and unpredictable nature of cyber threats, the difficulty in accurately quantifying cyber risks and the financial impact of incidents, the global shortage of skilled cybersecurity professionals who can implement robust defenses, and the systemic risk that could arise from widespread simultaneous cyber events impacting numerous policyholders.

Which regions are leading in Cyber Security Insurance adoption?

North America currently leads in market adoption due to its mature digital economy, stringent regulations, and high awareness of cyber risks. Europe follows closely, driven significantly by GDPR compliance. The Asia Pacific region is projected to be the fastest-growing market, propelled by rapid digital transformation and emerging data privacy legislations across its diverse economies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted